Shoals Stock: $758 Million in Orders in the Shop Window — and $1.9 Million in the Till

Shoals Technologies builds the nervous system of large solar farms: the complete wiring between solar module and inverter. The order book is fuller than ever at $758 million, revenue jumped 74.9 percent in the first quarter of 2026 — and still the stock shows up in our warning scanner "Insolvency Radar: Cash Running Out". We read the annual report (10-K) for 2025 and the quarterly report (10-Q) as of March 31, 2026: $1.9 million in cash, $181.8 of the $200 million credit line drawn, a worked-off $73 million warranty drama, a $70 million settlement with its own shareholders — and a tax law that stamps an expiry date on U.S. solar subsidies. Not investment advice — just the look behind the shop window before you step into the store.

There is a way of looking that costs us investors money again and again: the shop-window glance. We see a richly stocked shop window — record orders, double-digit growth, a megatrend as the backdrop — and conclude that the store must be doing well. What we do not see: the till behind the counter. Shoals Technologies Group (NASDAQ: SHLS) is currently the perfect shop window: a $758.0 million order book, revenue up 74.9 percent in the first quarter of 2026, plus the prettiest backdrop the stock market currently knows — solar farms, battery storage and power for AI data centers. And yet the stock sits in our warning scanner "Insolvency Radar: Cash Running Out". How does that fit together? Let's make a deal: we walk past the shop window together, into the store, and read what Shoals itself reported to the U.S. securities regulator, the SEC — in the annual report (10-K) for 2025 and the quarterly report (10-Q) as of March 31, 2026. An SEC filing is honest under penalty of law. And in there stands a sentence about $1.9 million that you should have read before the shop window casts its spell on you. In the end, you decide for yourself.

What Shoals actually does

Picture a solar farm the size of a thousand soccer fields. The solar modules are the muscles — but muscles alone produce no usable power. It takes veins and nerve fibers: cable harnesses, connectors, junction boxes, disconnect switches and monitoring technology that collect the direct current from hundreds of thousands of modules and carry it to the inverter. This inconspicuous layer is called EBOS in industry jargon — "electrical balance of systems", the electrical everything-around-it. That is exactly Shoals' business, since its founding in 1996 in Portland, Tennessee, where about 1,480 people work today (as of December 31, 2025). The core product, the patented "Big Lead Assembly" trunk line, is prefabricated in the factory so that on the construction site unskilled workers can plug in where electricians would otherwise have to crimp — a real argument in a country with a chronic shortage of skilled trades. 78.8 percent of revenue comes from such complete system solutions, almost all of it in the United States; the customers are above all the big construction groups (EPCs) that build solar farms and pay 10 to 20 percent up front at order.

Add two younger playing fields: battery storage (BESS) — there Shoals sells, among other things, a "recombiner" platform that ties together solar power, batteries and other direct-current sources — and, since 2025, expressly data centers. The annual report frames the backdrop itself: "we are seeing an acceleration of artificial intelligence (AI) adoption, driving an unprecedented increase in energy demand as each new data center gets built". Hyperscalers increasingly build their own power plants next to their data centers, and their wiring looks strikingly similar to a solar farm's. Sounds like the perfect story? In part it is. But remember the central tension of this analysis, it runs through every chapter: a full order book and genuine growth — financed from a till that held $1.9 million as of March 31, 2026, and a credit line that is more than 90 percent drawn. How differently suppliers of the energy transition can stand on the balance sheet is shown by our analysis of the wind-power supplier Broadwind — and what the data-center power business looks like when it is the main engine, by our look at Solaris Energy Infrastructure.

Where the stock shows up in our scanner

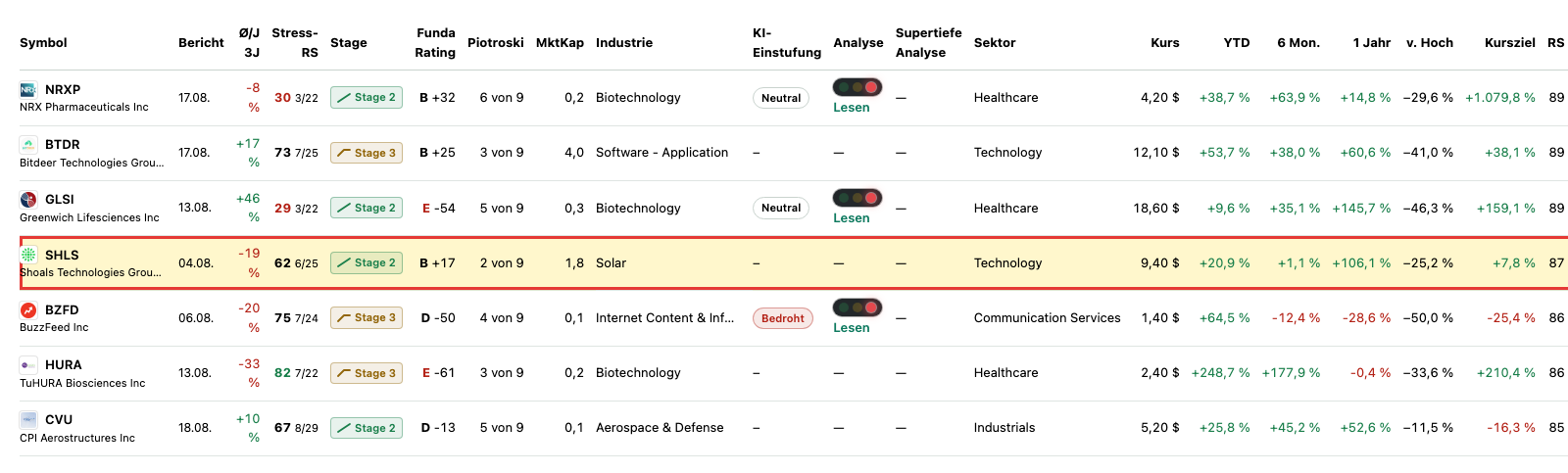

Every day we run about 3,500 stocks through our scanners. With Shoals, two worlds report at once. On the warning side stands the "Insolvency Radar: Cash Running Out" (membership verified live on July 14, 2026). The radar is deliberately built simple: it fires when the operating business has burned money in sum over the last four quarters and the till, at an unchanged burn rate, will not last four more quarters. Both are true: the four quarters through March 2026 sum to minus $39.9 million of operating cash flow, and $1.9 million of cash is a rounding error against that. Important for context: the radar measures the till, not creditworthiness — an untapped credit line it does not see. How to read such warning lists — a smoke detector, not a demolition notice — we explained in the article "Insolvency Radar: the Top 10". Alongside it comes the Beneish M-Score scanner, a statistical warning indicator that probes balance sheets for patterns of the kind found in embellished accounts — at Shoals well explained by the jump in revenue and inventory, but not to be argued away either.

On the other side, eight momentum and quality scanners celebrate the same stock: Weinstein Stage 2 (an intact uptrend), "Character Change", "High ADR" (about 9 percent daily range), "Institutional accumulation", Dual Momentum, "Pros 80%", "Top Performers 3/6 Month" and the "Super Stock Universe". The RS rating of 87 means: stronger than 87 percent of all stocks. And the Piotroski F-Score, a nine-point test of balance-sheet quality, nonetheless stands at 2 of 9 — a thoroughly healthy company stands at 8 or 9. Two honest footnotes belong here: first, scanner membership shifts daily — in the data set of July 8, Shoals was not yet in the radar; only with the Q1 figures in the four-quarter sum did the picture tip. Second, the radar here deliberately contradicts the classic early-warning scores: the Altman Z-Score sits at a comfortable 6.6 (danger zone: below 1.8), the equity ratio at 58 percent. The radar is still right about what it measures: the till is nearly empty. The exciting question is why — and the numbers answer it.

The numbers over the years — honestly appraised

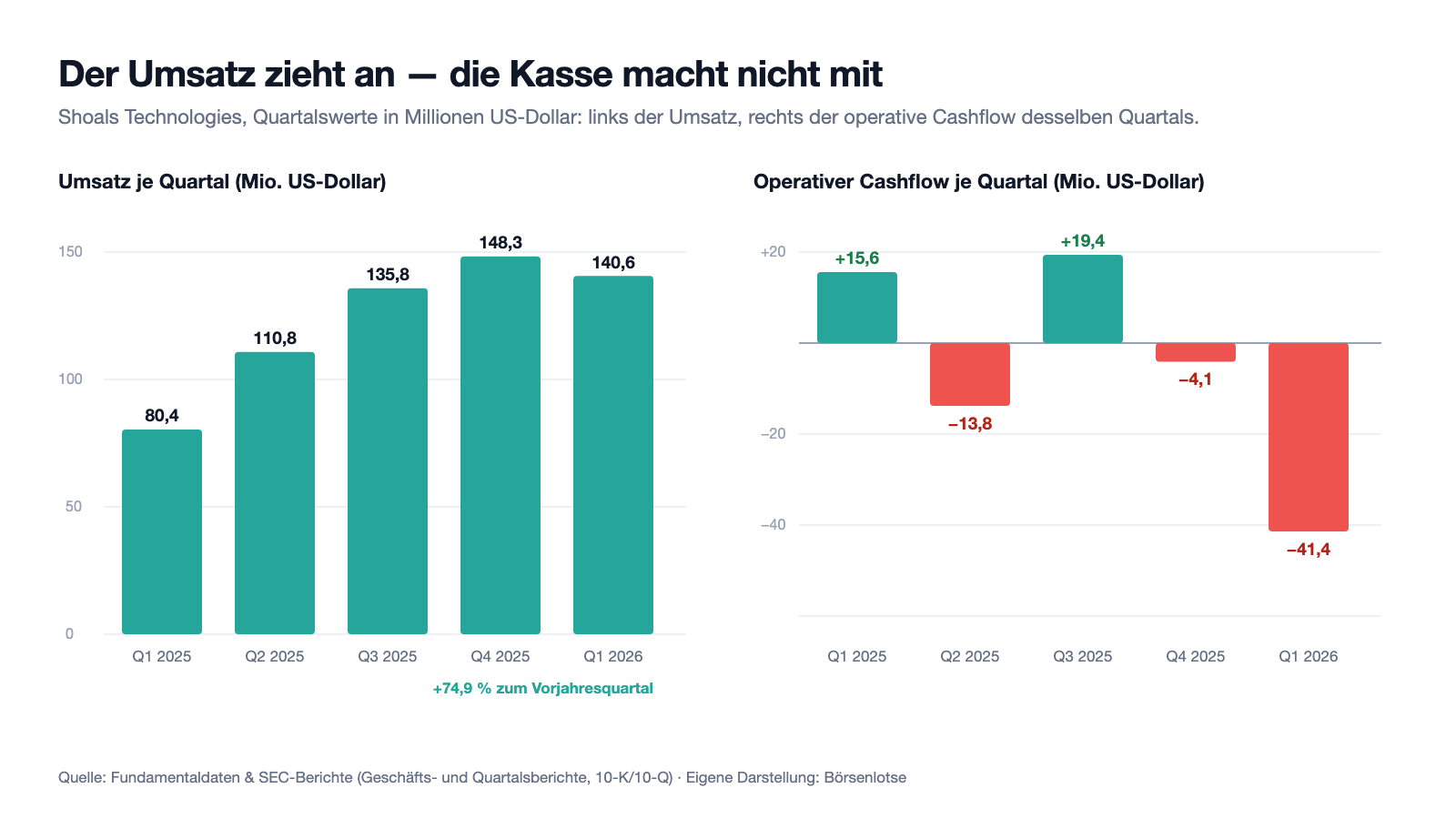

First, what genuinely impresses. Shoals is no loss-maker: in 2025 the group earned $33.6 million net (after $24.1 million in 2024), equity is solidly positive at $600.0 million, and the only financial debt is the credit line. Revenue tells a V-shaped story: $488.9 million (2023), $399.2 million (2024, minus 18 percent in the industry slump), $475.3 million (2025, plus 19 percent) — and then the jump: $140.6 million in the first quarter of 2026, plus 74.9 percent versus the prior-year quarter. The order book grew to $758.0 million as of March 31, 2026 (plus 17.5 percent within a year), of which $390.3 million is firmly signed and the rest awarded but not yet signed; a good $375 million of the firm orders is due for delivery within twelve months. That is real, documented growth — no story fog.

Now the two catches. Catch number one: the margin pays for the growth. The gross margin adjusted for the warranty costs fell from 47.0 percent (2023) via 39.0 percent (2024) to 35.0 percent (2025) — and in the first quarter of 2026 to a reported 29.2 percent. The quarterly report names the reasons itself: $3.8 million in additional tariffs, start-up costs of the new factory — and, remarkably openly, "market share capture initiatives" — in plain terms: Shoals is buying market share through price. Growth paid for with discounts is never entirely free. Catch number two sits in the cash flow statement: operating cash flow shrank from $92.0 million (2023) via $80.4 million (2024) to $17.1 million (2025) — and turned to minus $41.4 million in the first quarter of 2026. The main driver is not a loss (the bottom line showed only a mini-minus of $0.3 million) but $69.6 million of inventory build-up in a single quarter: material and components for exactly the record orders in the shop window. Remember the sentence: revenue is an opinion, cash is a fact. Which brings us to the uncomfortable truths.

What the filings say — the uncomfortable truths

Uncomfortable truth no. 1: $1.9 million in cash — and the credit line is 91 percent drawn

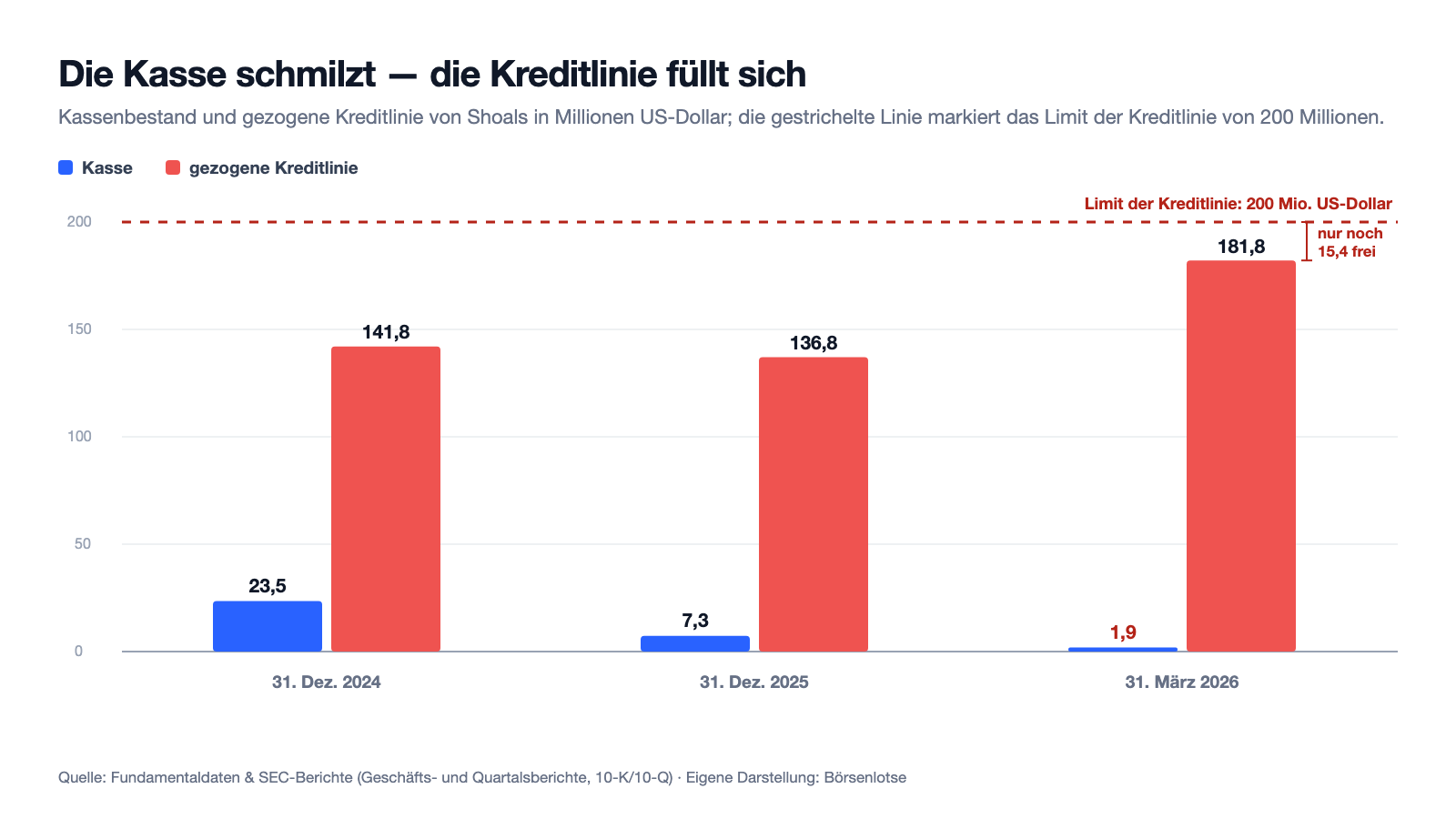

The quarterly report (10-Q) as of March 31, 2026 describes the liquidity position with a sobriety that makes you sit up:

"As of March 31, 2026, our cash and cash equivalents were $1.9 million, a decrease from $7.3 million as of December 31, 2025. As of March 31, 2026 we had outstanding borrowings of $181.8 million, a $45.0 million increase from outstanding borrowings of $136.8 million as of December 31, 2025. As of March 31, 2026, we also had $15.4 million available for additional borrowings under our $200.0 million Revolving Credit Facility."

— Shoals Technologies Group, SEC quarterly report 10-Q as of March 31, 2026, Item 2 MD&A "Liquidity and Capital Resources"

Let's do the math of the shop window against the till: available are $1.9 million plus $15.4 million of undrawn credit line — together a buffer of $17.3 million, in a quarter that alone burned $41.4 million operationally. Management writes in the same report: "Based on our past performance and current expectations, we believe that operating cash flows and availability under our Revolving Credit Facility will be sufficient to meet our near and long-term future cash needs." That is not an empty phrase: the inventory mountain is supposed to turn back into delivered orders and thus into money in the second half of the year, the customer deposits of 10 to 20 percent help, and the credit line runs until March 2029 (interest: SOFR plus 2.5 percentage points). There is no going-concern qualification, and there is no real mountain of debt either. But you should have understood the mechanics: Shoals finances its record growth almost entirely on the edge. Every order delay, every tariff push, every supply-chain disruption directly hits a buffer of $17 million — at a group with almost half a billion dollars of annual revenue. Exactly this line is what our radar measures.

Uncomfortable truth no. 2: the $73 million warranty drama — paid, but not reimbursed

Why is the till so thin in the first place, when Shoals has been posting profits for years? A large part of the answer is called "wire insulation shrinkback": starting in 2023, customers reported that on part of the installed cable harnesses the insulation contracts and exposes bare metal — in facilities designed for 30 years of operation, a serious safety and warranty problem. Shoals traces the defect to faulty wire that the cable maker Prysmian supplied between roughly 2019 and 2022. The annual report (10-K) for 2025 puts a number on the damage:

"[...] the Company believes the potential estimated loss for this matter is $73.0 million, which represents the best estimate of the potential loss as of December 31, 2025, of which $69.7 million has been incurred to date."

— Shoals Technologies Group, SEC annual report 10-K for 2025, Note 8 "Warranty Liability"

Three things make this footnote bigger than it looks. First, the history of the estimate: in 2023 Shoals named a range of $59.7 to $184.9 million; by now $73.0 million counts as the best estimate — but the report expressly warns that further affected solar farms may surface. Second: Shoals has no insurance for product warranties. The $69.7 million ran entirely through its own till — crews of technicians criss-crossing America to inspect and replace cable harnesses. Exactly this money is missing from today's buffer. Third, the irony of the accounting rules: the lawsuit against Prysmian (filed October 31, 2023 in Nashville) could one day claw the costs back — but as a "gain contingency", not a cent of it may be booked as long as success is not practically certain. The damage thus stands fully in the numbers, the possible reimbursement nowhere. At least: the remaining warranty provision has melted to $1.6 million (March 31, 2026), and in 2025, for the first time since the problem broke out, zero new shrinkback expense was incurred. The drama has been worked off — the shareholder paid for it.

Uncomfortable truth no. 3: a $70 million settlement with its own shareholders — the insurance pays almost all of it

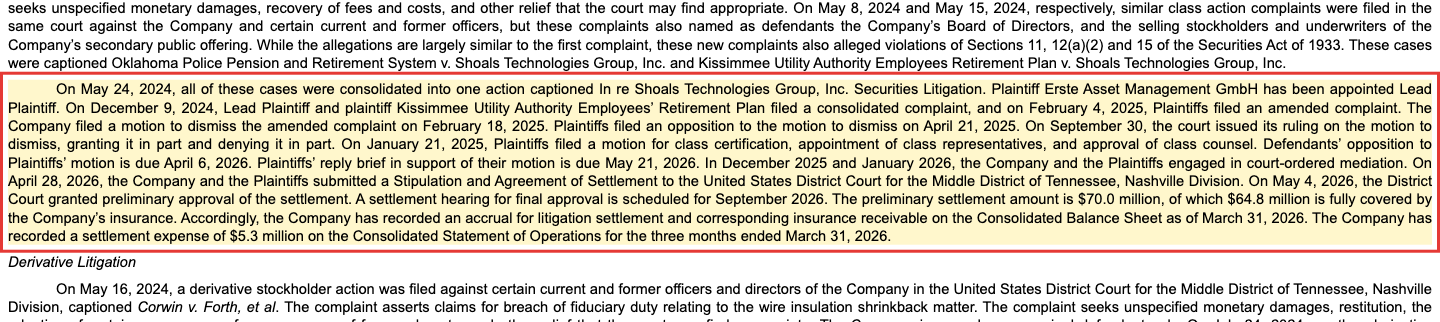

The warranty drama had a legal twin: starting in March 2024, shareholders — led by the Westchester road builders' pension fund, later consolidated under the lead of Vienna-based Erste Asset Management — sued the group for having informed wrongly or too late about the shrinkback problem. In spring 2026 the lid went on:

"The preliminary settlement amount is $70.0 million, of which $64.8 million is fully covered by the Company's insurance. [...] The Company has recorded a settlement expense of $5.3 million on the Consolidated Statement of Operations for the three months ended March 31, 2026."

— Shoals Technologies Group, SEC quarterly report 10-Q as of March 31, 2026, Note 13 "Commitments and Contingencies — Securities Litigation"

The good news first: unlike in the warranty drama, Shoals was insured here — of $70 million, only $5.3 million sticks to the group, and the court preliminarily approved the settlement on May 4, 2026; the final hearing is set for September 2026. That would take the biggest litigation risk off the table without seriously burdening the already thin till. The honest footnote: the chapter is not entirely closed. A shareholder derivative suit against officers and directors of the company ("Corwin v. Forth") continues, the defense cost $1.6 million in the first quarter alone — and a $70 million settlement is, for all the insurance coverage, also a price tag for how seriously the accusations around the shrinkback communication were taken. For you as a reader, the pattern is what counts: the two big legacy burdens — warranty and lawsuit — are by now quantified and largely worked off. What remains is the risk nobody can settle or insure: politics.

Uncomfortable truth no. 4: Washington has stamped an expiry date on solar subsidies — and a fifth of revenue hangs on one customer

Shoals' end market lives on U.S. tax credits for solar projects. In 2025 the U.S. Congress tightened the rules with the law H.R. 1 — the "One Big Beautiful Bill Act". The annual report sums up the consequences:

"In 2025, H.R. 1, the One Big Beautiful Bill Act, was enacted into law. H.R. 1 significantly modifies certain energy tax provisions aforementioned in the IRA. Changes to the IRA made by H.R. 1 include an accelerated phaseout or termination of the PTC and TC for solar projects placed in service after 2027."

— Shoals Technologies Group, SEC annual report 10-K for 2025, Item 1A "Risk Factors"

Here lies the double-edged explanation for the boom: part of the record demand is presumably pulled-forward demand — project developers are stepping on the gas so their farms connect to the grid before the deadline at the end of 2027 and still collect the credits. What comes after 2027, nobody knows; the report additionally names the still-unfinished "Foreign Entity of Concern" rules, whose interpretation is expected only in 2026, and warns that the loss of the incentives could lead to lower demand for its products. Add a concentration risk every supplier knows and none likes: "For the year ended December 31, 2025, our largest customer and five largest customers constituted approximately 19.1% and 53.7% of total revenue, respectively." — the largest customer stood for about 19.1 percent of 2025 revenue, the five largest for 53.7 percent. Imagine your neighbor tells you his business is running splendidly — but a single client provides a fifth of the income and half of it hangs on five names. Would you swallow for a second? Exactly. At least: in 2023 the largest customer still stood at 36.3 percent — the dependence is falling. And the new legs, BESS and data centers, are the attempt to escape the solar subsidy cycle before it ends.

Valuation: a $1.76 billion market value — three times revenue for a cable assembler

In early July 2026 the Shoals stock cost about $9.90, which makes a market value of about $1.76 billion (data as of July 8, 2026) — after plus 106 percent within twelve months, but still about 75 percent below the all-time high from the solar hype shortly after the January 2021 IPO. Measured against the revenue of the last four quarters, that yields a price-to-sales ratio of about 3.3 — for a maker of physical electrical infrastructure with a falling margin, that is no bargain price but a growth advance. Based on the earnings analysts expect for 2026, the price-to-earnings ratio lands in the order of the mid-twenties; 21 analysts cover the stock, their consensus leans toward "buy", but the median price target in mid-July 2026 sat only single-digit percent above the price. Translated: the professionals like the story but consider the price largely exhausted. The stock's nervousness fits the picture — a daily range of about 9 percent and a short interest of a good 10 percent of the free float (as of July 14, 2026) mean: both sides are betting here with real money. There is no dividend, and given this cash position that is just as well.

Opportunities and risks at a glance

What speaks for Shoals:

- A record order book with substance: $758.0 million of backlog and awarded orders (March 31, 2026, plus 17.5 percent year over year), of which $390.3 million firmly signed; customers pay 10 to 20 percent up front (quarterly report 10-Q).

- Real, profitable growth: plus 74.9 percent revenue in the first quarter of 2026, $33.6 million of net income in 2025, $600 million of equity, a 58 percent equity ratio, an Altman Z-Score around 6.6 — classic distress scores do not fire.

- The legacy burdens are quantified and largely worked off: the $73 million warranty drama is paid to the tune of $69.7 million (remaining provision $1.6 million), the $70 million shareholder settlement is insured for $64.8 million; on top, the damages lawsuit against the cable supplier Prysmian runs as an unbooked trump card.

- A second leg with AI tailwind: EBOS solutions for battery storage and data centers, whose power demand per the annual report grows at an "unprecedented" pace with every AI build-out stage — the wiring expertise from solar farms transfers directly.

- Pulled-forward solar demand through the end of 2027 supports utilization; an ITC administrative judge ruled in February 2026 that two Shoals patents are infringed by competitor Voltage (final decision expected by June 2026).

What speaks against it:

- Liquidity is sewn on the edge: $1.9 million in cash and $15.4 million of available credit line (March 31, 2026) against minus $41.4 million of operating cash flow in one quarter; the four-quarter sum sits at minus $39.9 million — exactly the pattern our "Cash Running Out" radar hunts for.

- Growth at the expense of margin: the adjusted gross margin fell from 47.0 (2023) via 39.0 (2024) to 35.0 percent (2025), a reported 29.2 percent in the first quarter of 2026 — pressed by tariffs ($3.8 million in the quarter) and expressly price-driven market-share gains; Piotroski F-Score 2 of 9.

- A policy cliff: the U.S. law H.R. 1 ends the solar tax credits for facilities placed in service after 2027; the "Foreign Entity of Concern" rules are not yet final — part of today's boom is presumably pulled-forward demand.

- Concentration risk: 19.1 percent of 2025 revenue hangs on the largest customer, 53.7 percent on the five largest; receivables concentrate similarly (largest debtor: 25.2 percent).

- Warning signs in the fine print: no insurance for product warranties, possible further shrinkback cases not ruled out per the 10-K, an ongoing derivative suit, a Beneish M-Score scanner hit and a short interest of a good 10 percent (as of July 14, 2026).

A human conclusion

Back to the shop-window glance from the beginning. It is not stupid — a full order book is a strong signal, and at Shoals the shop window is not even a prop: the orders are signed, the growth stands audited in the quarterly report, the legacy burdens are mostly paid or insured. But the case shows you what the shop-window glance systematically misses: between a signed order and money in the till lie months, material and risk — and exactly in that gap is where Shoals lives right now. $69.6 million of inventory build-up in one quarter, $1.9 million of remaining cash, 91 percent of the credit line drawn: that is the operating mechanics of a store growing so fast it is running out of change. If the plan works — inventory becomes delivery, delivery becomes revenue, revenue becomes cash — the radar hit will probably resolve itself in the second half of the year, and the shop window was right. If instead a big customer breaks away, a project year shifts, or Washington turns off the subsidies faster than expected, the shock hits a buffer of $17 million — and the growth miracle very quickly becomes a dilution or credit story. Both stand in the same report, just a few pages apart. So at the next full shop window, check the till first — the way you just did here. What you make of it is your decision. And that is exactly as it should be.

Sources

All original documents used in this analysis — to read for yourself:

- Shoals Technologies Group — SEC annual report 10-K for 2025 (filed February 24, 2026)

- Shoals Technologies Group — SEC annual report 10-K for 2024 (filed February 25, 2025)

- Shoals Technologies Group — SEC quarterly report 10-Q as of March 31, 2026 (filed May 5, 2026)

- Shoals Technologies Group — SEC quarterly report 10-Q as of September 30, 2025 (filed November 4, 2025)

- Shoals Technologies Group — SEC quarterly report 10-Q as of June 30, 2025 (filed August 5, 2025)

- Shoals Technologies Group — SEC quarterly report 10-Q as of March 31, 2025 (filed May 6, 2025)

- Shoals' complete SEC filing history: EDGAR overview (sec.gov)

- Fundamental data (metrics, quarterly series, valuation; data as of July 8, 2026), reconciled with the SEC filings.

- Screener and rating data: in-house stock scanner (data as of July 8, 2026; scanner membership verified live on July 14, 2026).

Transparency & disclaimer: This analysis is a journalistic contextualization of publicly available information and is not investment advice, not a financial analysis in the regulatory sense, and not a solicitation to buy or sell securities. It expressly contains no judgment on whether an insolvency will occur. Stock investments carry substantial risks up to total loss. All information without guarantee; the data cut-off is noted in the text in each case. The author holds no position in Shoals stock at the time of publication.

Our Bottom Line at a Glance

- Market position & order book positive

- Leading specialist for solar EBOS with the patented Big Lead Assembly system and expansion into battery storage and data centers: a $758.0 million order book as of March 31, 2026 (plus 17.5 percent year over year), 78.8 percent of revenue from system solutions, customer deposits of 10 to 20 percent (quarterly report 10-Q).

- Growth & profitability neutral

- Revenue plus 74.9 percent in the first quarter of 2026, net income of $33.6 million in 2025 — but the adjusted gross margin fell from 47.0 (2023) to 35.0 percent (2025) and a reported 29.2 percent in Q1 2026, pressed by tariffs and expressly price-driven market-share gains; Piotroski F-Score 2 of 9.

- Liquidity & cash flow negative

- $1.9 million in cash and $15.4 million of available credit line (March 31, 2026) against minus $41.4 million of operating cash flow in the quarter ($69.6 million inventory build-up); the $200 million credit line is 91 percent drawn. No going-concern qualification, the credit line runs until March 2029 — but the buffer is wafer-thin.

- Legal risks & legacy burdens neutral

- The $73 million warranty drama is paid to the tune of $69.7 million (remaining provision $1.6 million), the $70 million shareholder settlement is insured for $64.8 million (final hearing September 2026). Open: the derivative suit, possible further shrinkback cases, no product-warranty insurance — and, as an unbooked opportunity, the Prysmian lawsuit plus the ITC patent win against Voltage.

- Politics & concentration risk negative

- H.R. 1 ends the solar tax credits for facilities placed in service after 2027 — part of the boom is presumably pulled-forward demand; the FEOC rules are still unfinished. Add 19.1 percent of revenue on the largest customer (top 5: 53.7 percent) and tariff pressure on the margin (annual report 10-K for 2025).

Shoals is the opposite of a zombie company: profitable, growing, with a record order book, positive equity and worked-off legacy burdens. The radar hit is still no false alarm but to be taken literally: $1.9 million in cash, 91 percent of the credit line drawn, minus $41.4 million of operating cash flow in one quarter — Shoals finances its own boom on the edge, while the margin falls and Washington has stamped an expiry date on solar subsidies. Not investment advice.

What Our Rating Means

- If you don't own the stock

- In our view, the documented risks clearly outweigh — we see no basis for an entry.

- If you hold it in your portfolio

- In our view, the findings carry enough weight to warrant a critical look at your own position.

A journalistic assessment by our editorial team at the time of the deep dive, based on public sources — not investment advice and not a solicitation to buy or sell. Your personal circumstances (investment goals, risk capacity, taxes) cannot be taken into account. What our categories mean, how verdicts are formed, and what conflicts of interest exist →

Worth Noting

- Scanner membership shifts daily: in the data set of July 8, 2026 SHLS was not yet in the Insolvency Radar; on July 14, 2026 (verified live) the row is included, because the Q1 figures pushed the four-quarter sum of operating cash flow below zero.

- Price and valuation figures dated July 8, 2026 (about $9.90, about $1.76 billion market value); short interest and scanner screenshot dated July 14, 2026. Analyses are evergreen, daily prices are not a buy argument.

- The class-action settlement ($70.0 million, of which $64.8 million insured) has preliminary court approval; the final hearing is set for September 2026.

Frequently Asked Questions

Shoals (NASDAQ: SHLS) of Portland, Tennessee, manufactures the electrical infrastructure (EBOS) of large solar farms: prefabricated cable harnesses, connectors, junction boxes and monitoring technology between solar module and inverter. Add solutions for battery storage and data centers. In 2025 the group generated $475.3 million in revenue and earned $33.6 million net; about 1,480 people work there.

The radar literally measures the till: the operating cash flow of the last four quarters through March 2026 sums to minus $39.9 million, and only $1.9 million was left in cash. The main cause is not a loss but $69.6 million of inventory build-up in one quarter for the record order book — financed through the credit line, which is drawn to $181.8 of $200 million.

On part of the cable harnesses installed up to about 2022, the insulation contracts and exposes metal. Shoals puts the damage at $73.0 million in the annual report (10-K) for 2025, of which $69.7 million already paid — without insurance. The wire, per Shoals, was supplied by the cable maker Prysmian, which has been sued for damages since October 2023; a success is not on the balance sheet.

The U.S. class action over the shrinkback communication was resolved in April 2026 through a settlement of $70.0 million; the court gave preliminary approval on May 4, 2026, and the final hearing is set for September 2026. The insurance pays $64.8 million; $5.3 million of expense stuck with Shoals in the first quarter of 2026. A derivative suit against officers and directors continues.

H.R. 1 ends the central solar tax credits (PTC/ITC) for facilities placed in service after 2027 and tightens rules on foreign entities (FEOC). That likely pulls demand forward into the years through 2027 — exactly what supports Shoals' record order book — and makes the time after that uncertain. Shoals is therefore building out its battery storage and data center legs.

At a price of about $9.90 (data as of July 8, 2026), the market value comes to about $1.76 billion — roughly 3.3 times the revenue of the last four quarters and roughly the mid-twenties multiple of the earnings expected for 2026. After plus 106 percent in twelve months, the stock still trades about 75 percent below the high from the solar hype of early 2021.

This analysis expressly issues no insolvency verdict. The facts: no going-concern qualification, positive equity of $600 million, an Altman Z-Score around 6.6, profitable operations — but only a $17.3 million liquidity buffer (cash plus available credit line, March 31, 2026) against $41.4 million of operating cash outflow in the quarter. Whether the inventory mountain converts back into money as planned is the decisive question of the coming quarters.

Found an error?

Did you spot a factual error, an outdated number, or a typo in this deep dive? Let us know briefly — your report goes straight to the editorial team.