Affirm Stock: The First Profit — and What It Doesn't Tell You

Affirm is the U.S. market leader for installment payments at checkout — "Buy Now, Pay Later." Volume grew 81 percent in two years to $36.7 billion, and 2025 brought the first GAAP profit in company history: $52 million. Sounds like a turning point. But operations still ran a loss, the company's own "Adjusted Operating Income" of $778 million adds back nearly half a billion dollars in stock-based compensation — and the actual business is lending money. We read the filings: credit quality, dilution, the Amazon concentration risk and valuation. Not investment advice — just the arithmetic behind a first profit that spent nearly half a billion dollars to happen.

There's a reflex that catches us investors especially easily with growth stocks. A company that spent years posting losses suddenly reports its first profit — right next to a shinier "adjusted" number, several hundred million dollars large. We breathe a sigh of relief, check the box marked "finally profitable," and stop reading. I call this reflex the adjusted-profit illusion: we see the word "profit" next to a fat "Adjusted" figure and stop asking which profit we're actually looking at. It fits today's company with a certain irony: Affirm (Nasdaq: AFRM) makes its money by letting people buy now and pay later — "Buy Now, Pay Later." In a small way, we investors do the same thing with profit: we take the pretty number now and push the uncomfortable questions to later. Let's do it the other way around today. Here's the deal: we read together what the company told the U.S. securities regulator, the SEC — a filing is honest under penalty of law — and at every headline number we ask: what did it cost? In the end, you decide for yourself.

What Affirm actually does

Affirm is an installment lender at the point of sale — at the checkout counter and in the online shopping cart. You buy a couch, a Peloton bike or a pair of sneakers, and instead of paying it all at once, you split the amount into installments with one click: "Buy Now, Pay Later" (BNPL). For you as the buyer that's often interest-free; the big partners are Amazon, Shopify and Walmart. Affirm earns money in several ways — and a close look pays off here, because it reveals what Affirm really is. The largest revenue block in fiscal year 2025 wasn't a referral fee, it was interest income: $1.61 billion out of $3.22 billion total. Add to that merchant fees ($883 million — the store pays for the privilege of you buying right now), gains on loan sales ($382 million), fees from Affirm's virtual payment card network ($231 million) and servicing income ($121 million).

Translated, that means: Affirm dresses up as a tech platform, but at its core it's a lender. It borrows money, lends it back out as consumer credit, and lives on the spread — minus the customers who don't pay it back. About 72 percent of volume is interest-bearing loans, roughly 13 percent interest-free installment purchases (0 percent offers), and 14 percent short-term "Pay in 4" splits. Remember this tension, it's the connecting thread for everything that follows: Affirm is growing at a breathtaking pace — but the road to a real, sustainable profit runs through a loan book that gets bigger and riskier with every growth step. Is this a software miracle growing here, or a very fast-growing bank? That's exactly the question.

Where the stock shows up in our scanner

Every day we run thousands of stocks through our in-house stock scanner, and Affirm lights up strikingly green there (data as of July 9, 2026): a full 13 filters fire at once. It's a pure growth-and-momentum picture. On the fundamentals side, the "High Revenue Growth" filter fires, along with "EPS Acceleration" (earnings per share improving at an accelerating pace), the "Quality Growth" filter and "Fundamental Rank." On the trend side, "Above 50- & 200-Day SMA" (the price sits above its key moving averages), a "Bullish Reversal Bar" and several trader lists join in. All told, Affirm even lands in the catch-all filter "Best of All."

The honest read: thirteen green lights sound like a home run — but they largely measure the same thing. Fast revenue growth, a rising share price and improving earnings are three faces of the same coin: momentum. What the scanner does not measure are the questions that will decide the next several years — the quality of the loan book, the dilution from stock-based compensation, and the valuation. That's exactly what we look at next. To find the stock yourself: open one of the filters named above in our scanner and search for the row AFRM.

The numbers: growth that deserves to be taken seriously

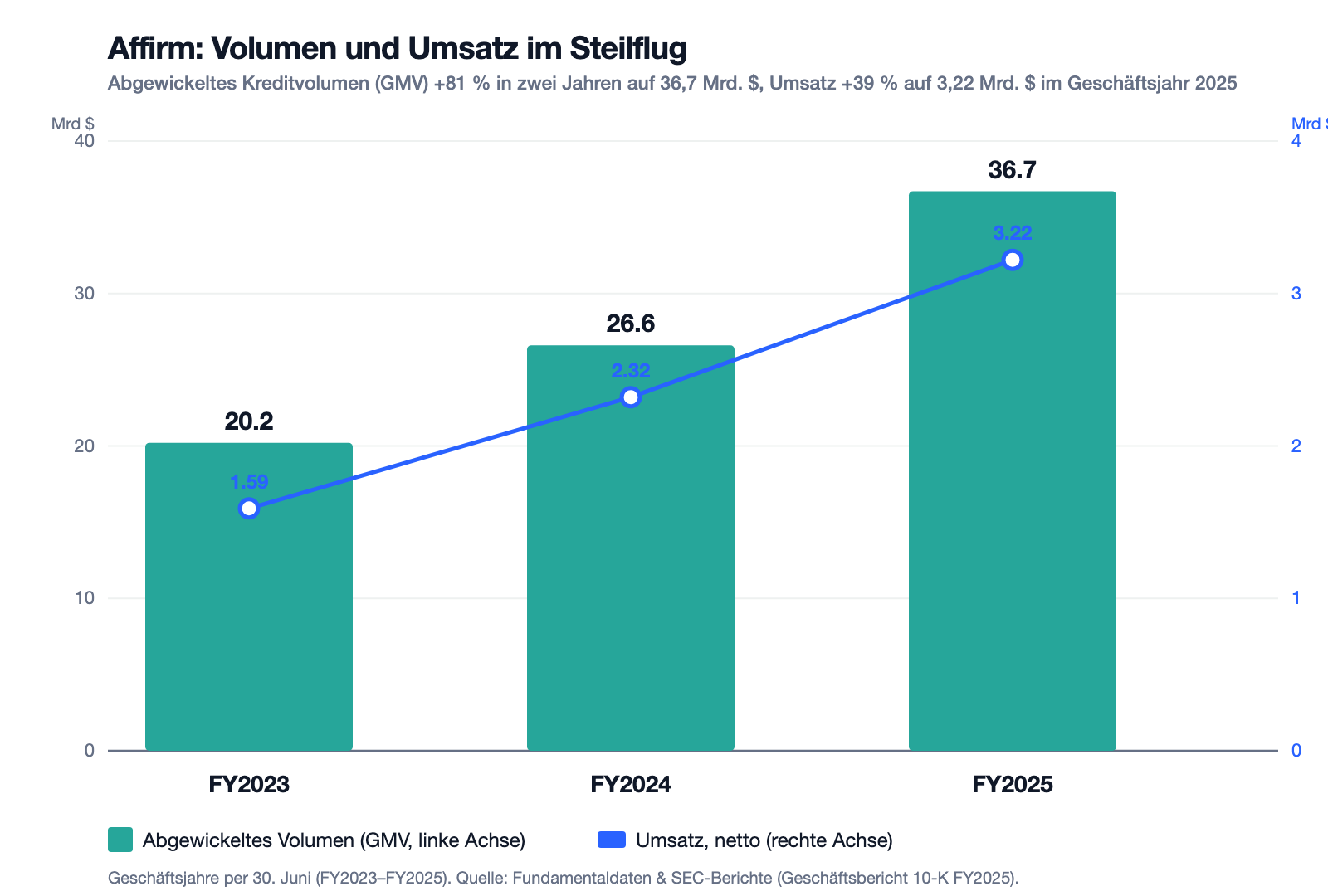

Let's start with what genuinely impresses — that's part of being honest, too. Affirm's gross merchandise volume (GMV — the total of all purchases financed through the platform) rose 81 percent in just two years: from $20.2 billion (fiscal year 2023) through $26.6 billion (2024) to $36.7 billion (2025). Revenue climbed over the same period from $1.59 to $3.22 billion, up 39 percent in 2025 alone. This isn't a flash in the pan — it's sustained, high growth: the third quarter of fiscal year 2026 kept the pace, with volume up 35 percent.

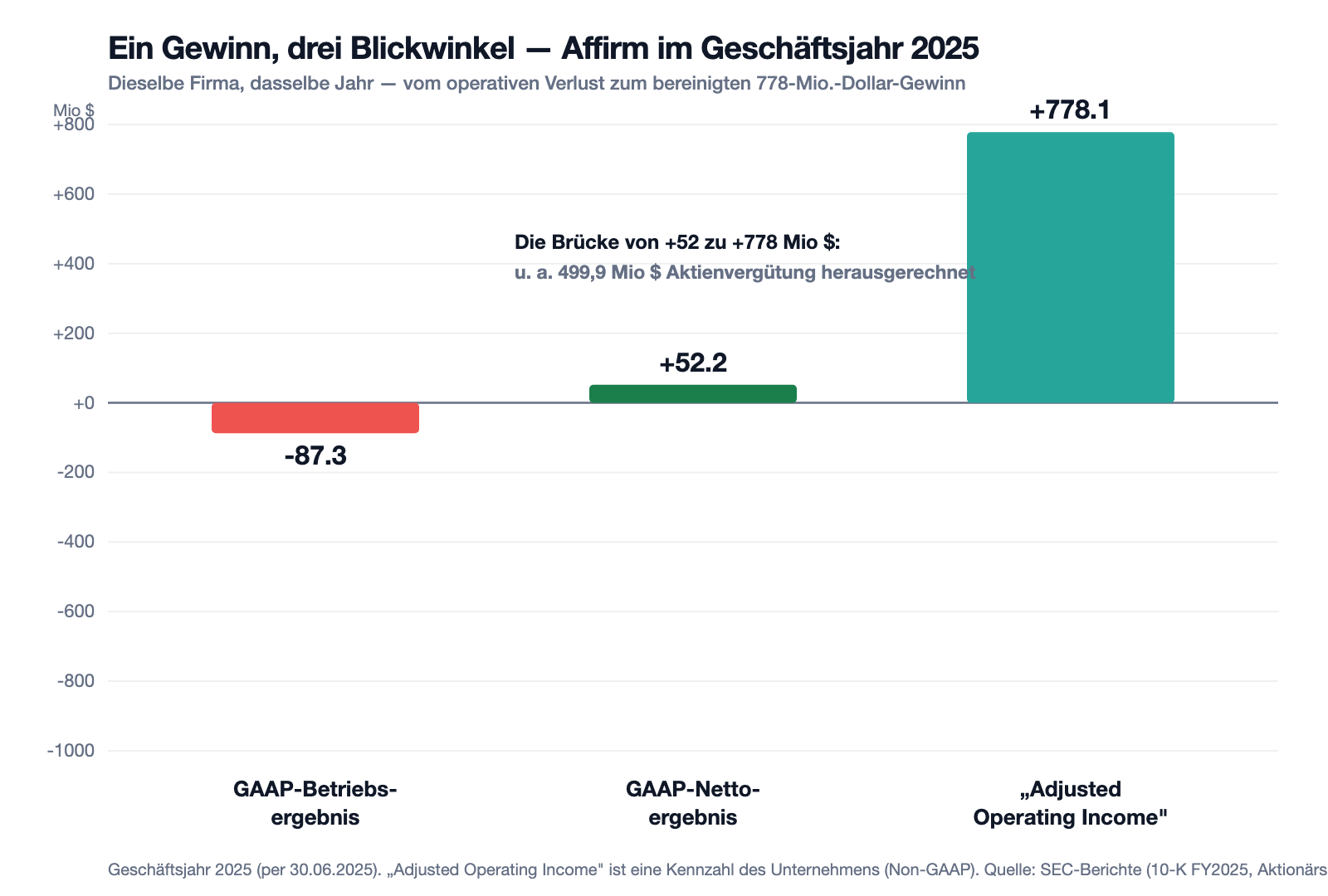

And then the event fans had waited years for: in fiscal year 2025, Affirm reported the first positive GAAP net income in company history at +$52.2 million — after a loss of $517.8 million the year before and $985.3 million in 2023. On paper, a turning point. But now let's apply the frame from the opening — the adjusted-profit illusion — and look more closely. Because one and the same company shows three very different bottom-line numbers in the same year, depending on where you look.

Let's be clear about this: the operating business lost money in 2025. The small plus at the bottom line came from effects below the operating line. And the $778 million "Adjusted Operating Income" isn't cash sitting somewhere — it's the operating loss with a series of real expenses added back. Why that's neither a sleight of hand nor a free pass is spelled out in the filings.

What the filings say — the uncomfortable truths

Uncomfortable truth no. 1: the first profit — paid for with half a billion dollars in stock

Affirm states with refreshing clarity, right in its own annual report, where profitability actually stands — in the risk factors chapter, as its own heading no less:

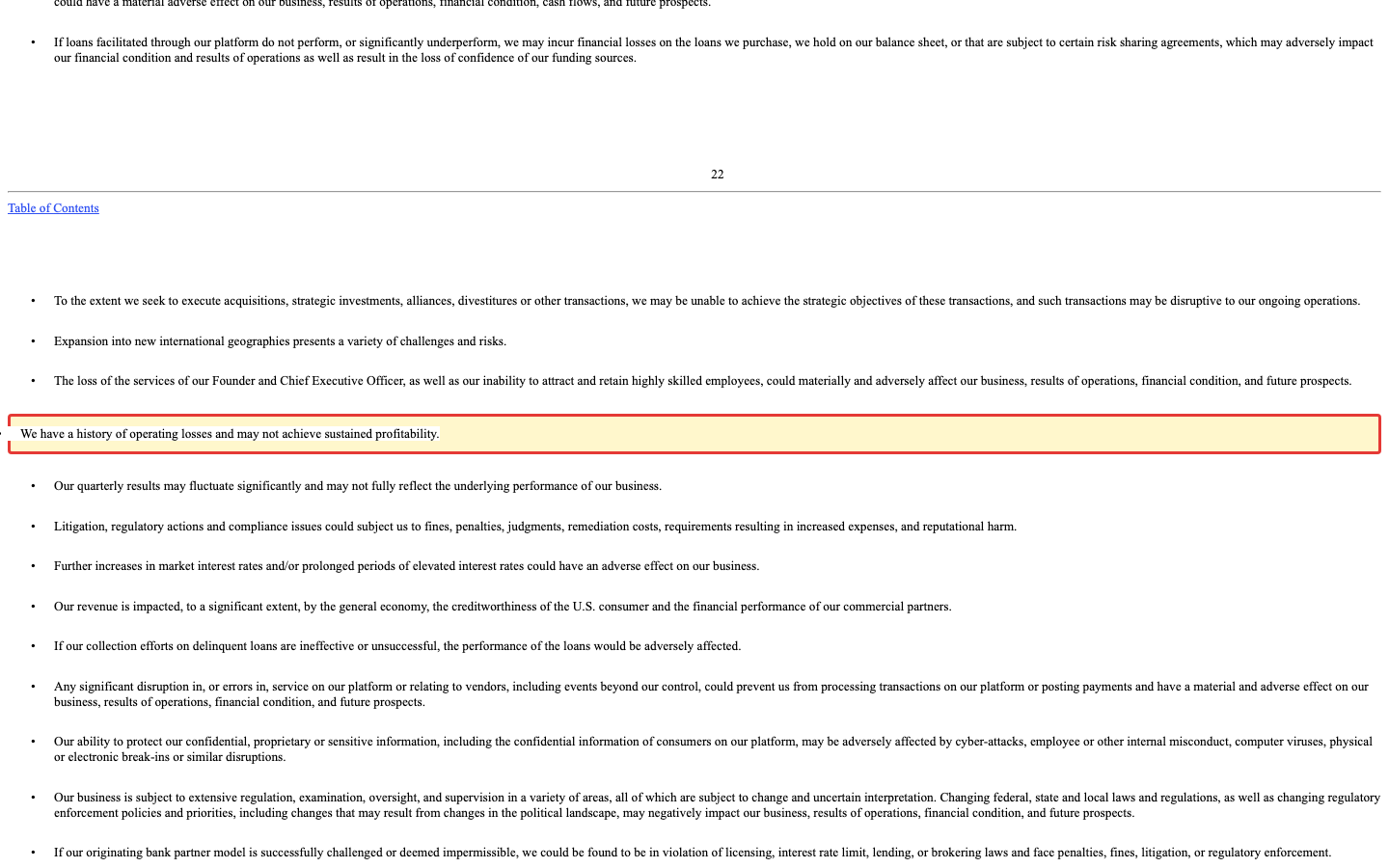

"We have a history of operating losses and may not achieve sustained profitability. We incurred net income of approximately $52.2 million for the fiscal year ended June 30, 2025 and net losses of approximately $517.8 million and $985.3 million for the fiscal years ended June 30, 2024 and 2023 respectively. As of June 30, 2025 […] our accumulated deficit was approximately $3.1 billion."

— Affirm Holdings, Inc., SEC annual report 10-K, fiscal year 2025, Item 1A "Risk Factors"

The reason the operating loss (−$87.3 million) and the adjusted figure (+$778.1 million) sit so far apart has a name: stock-based compensation. Affirm pays a substantial share of its workforce not in cash but in freshly issued shares. In 2025 that came to $499.9 million — about 15.5 percent of total revenue. The adjusted metric strips this expense out, as if it weren't real. It is real, though — just not a cash payment, but dilution: your slice of the pie gets smaller, because new slices are constantly cut off and handed to staff. Growth paid for with fresh stock is never entirely free. We dissected a related pattern — a profit that shines on paper and evaporates on contact — at the Medicare broker eHealth; there the catch sat in the cash-flow statement, here it sits in the share count.

Uncomfortable truth no. 2: the business is lending — and loans go bad

Because interest income is Affirm's largest revenue block, the company is exposed, above all, to credit risk. The faster the loan book grows, the more money Affirm has to set aside for expected losses. The filing puts a number on it:

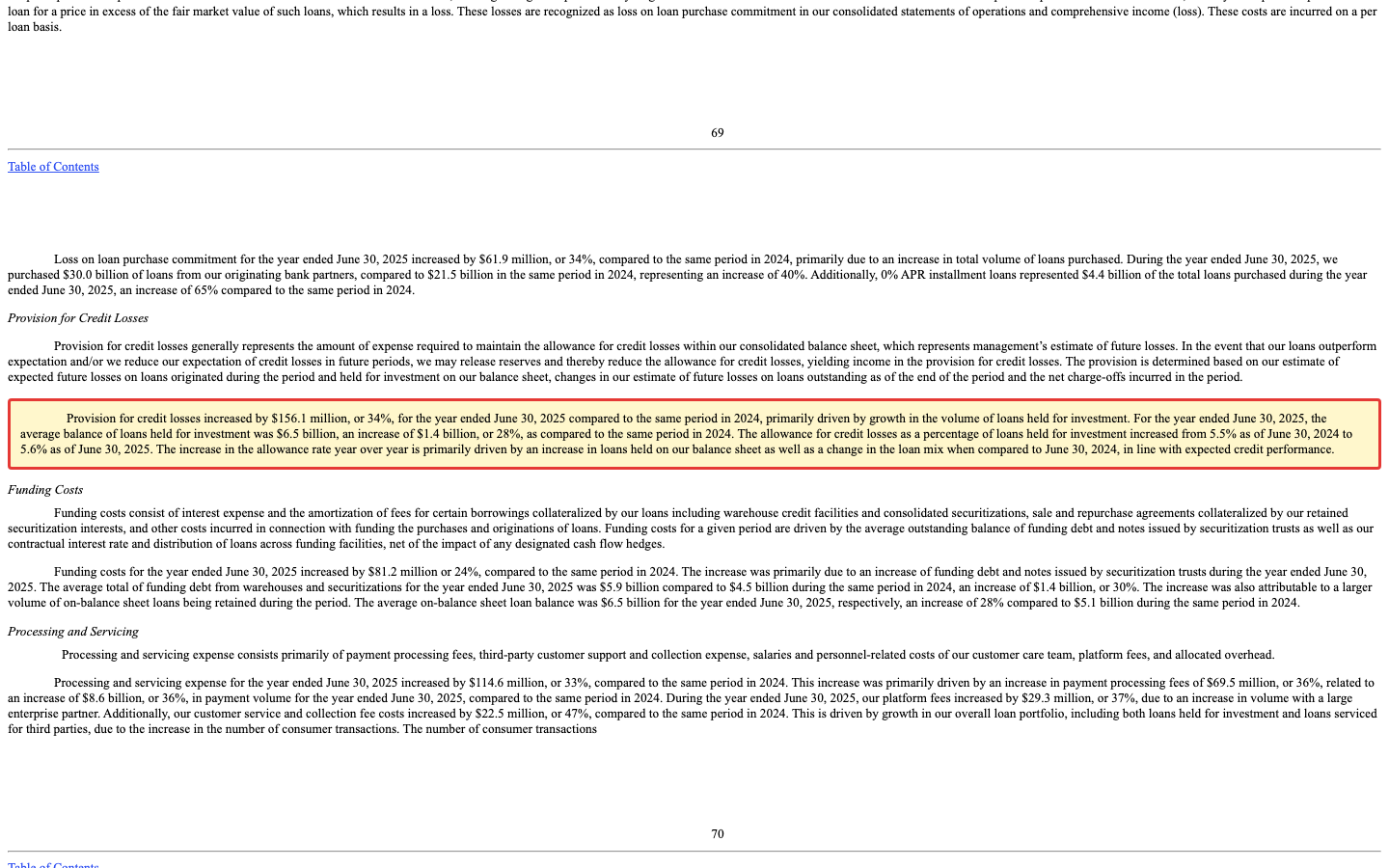

"Provision for credit losses increased by $156.1 million, or 34%, for the year ended June 30, 2025 compared to the same period in 2024, primarily driven by growth in the volume of loans held for investment. […] The allowance for credit losses as a percentage of loans held for investment increased from 5.5% as of June 30, 2024 to 5.6% as of June 30, 2025."

— Affirm Holdings, Inc., SEC annual report 10-K, fiscal year 2025, MD&A — Provision for Credit Losses

By the end of March 2026, the allowance for credit losses had climbed further, to 6.0 percent of loans, and the 30-day delinquency rate (the share of loans where a payment is more than a month overdue) had risen from about 2.3 to 2.8 percent. Those are manageable levels so far — but they show the direction. On top of that comes rate sensitivity: Affirm funds its loans through a web of warehouse credit facilities (up to $4.9 billion in capacity), forward-flow agreements with institutional buyers, and securitizations — about $28 billion in total funding capacity. Rising rates make that money more expensive. To its credit, Affirm hedges a large portion and estimates the effect of a 1-percentage-point rate jump at less than $65 million of cash-flow impact over twelve months. That's not an acute danger — but it's the reason a BNPL provider trembles with every rate cycle in a way that genuine software companies don't.

Uncomfortable truth no. 3: one partner, one fifth of the volume

Picture your neighbor proudly telling you business is booming — and when you ask, it turns out a single customer accounts for more than a fifth of his revenue. Would you wince a little? At Affirm, that customer is Amazon. The filing is specific:

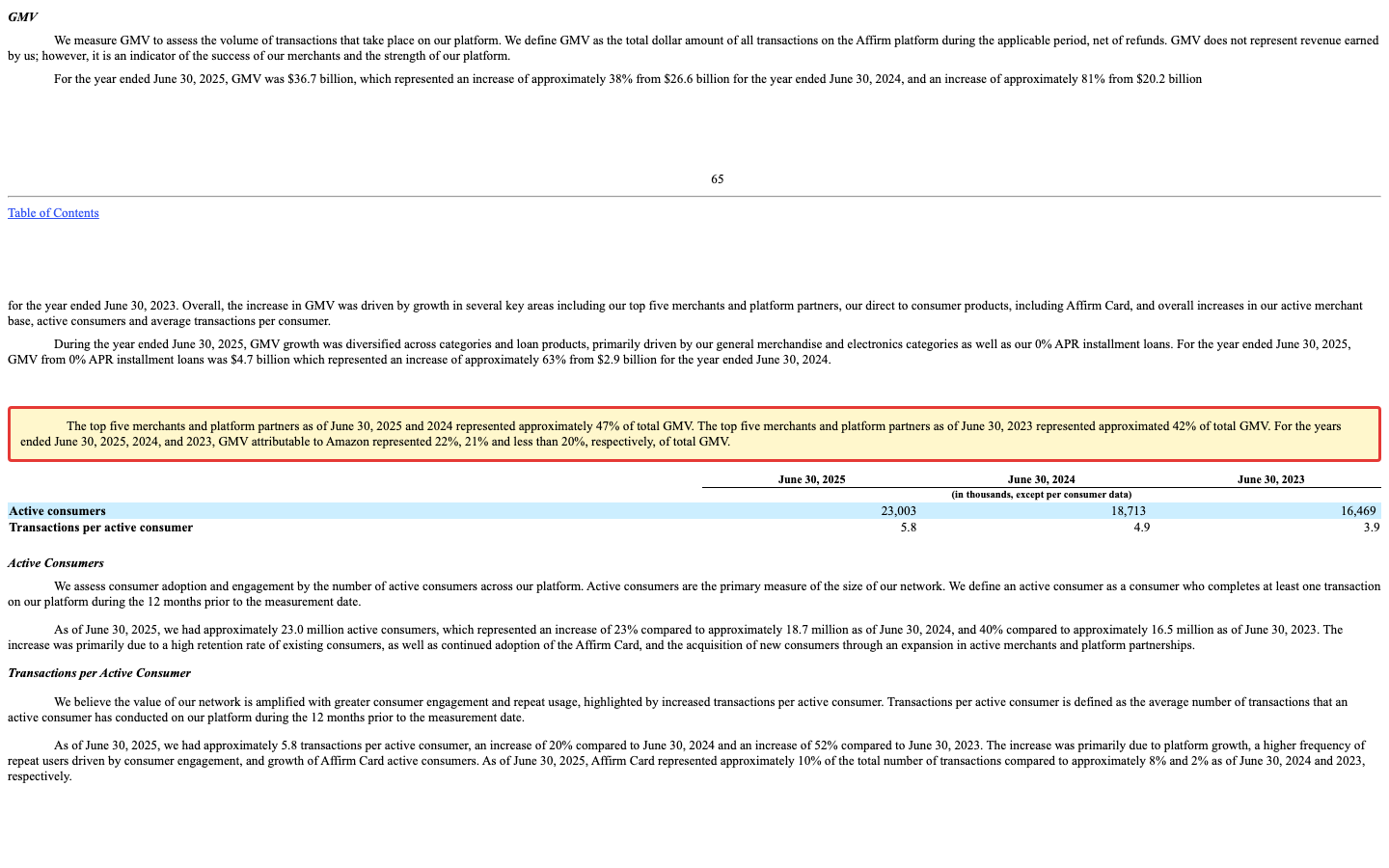

"The top five merchants and platform partners as of June 30, 2025 and 2024 represented approximately 47% of total GMV. […] For the years ended June 30, 2025, 2024, and 2023, GMV attributable to Amazon represented 22%, 21% and less than 20%, respectively, of total GMV."

— Affirm Holdings, Inc., SEC annual report 10-K, fiscal year 2025, MD&A — Key Operating Metrics

A fifth of volume hangs on a single partner, almost half on five. Now, Amazon is no shaky bet, and the relationship is bound together through warrants — Affirm even absorbed a special charge for that. But you know the pattern from every concentration-risk story: partnerships like this are rarely exclusive and rarely permanent. For scale: a 22 percent share is a serious dent, not a broken neck — Affirm has more than 377,000 merchants and 23 million customers, the business wouldn't collapse if Amazon added a second provider alongside it. But it would be a noticeable drag on the growth story this stock rides on.

Valuation — what the market demands for the growth

Back to the adjusted-profit illusion — it has a sibling on the stock market: valuation. In mid-2026 Affirm carries a market value of about $28 billion against trailing-twelve-month revenue of about $3.97 billion. That works out to a price-to-sales ratio around 7 and an enterprise value (market value plus debt minus cash) of roughly 8.5 times revenue. For a software company, that wouldn't be unusual. For a lender, it's ambitious — banks typically trade at a fraction of those multiples because their earnings depend on the credit cycle. The market, in other words, is explicitly paying Affirm for the story of being a technology company with network effects, not merely a fast-growing consumer-credit factory. Whether that premium holds comes down to exactly one question: can Affirm make GAAP profitability durable without the adjusted crutch and without constantly issuing new shares? For a look at what a business that genuinely throws off free cash surplus looks like, our analysis of the document specialist Consensus Cloud is worth a look — a very different case, but a useful yardstick for what "real" profit looks like.

A word on control that belongs on the price tag: Affirm has a dual-class structure. Founder and CEO Max Levchin holds shares carrying 15 votes each and controls about 44.4 percent of all votes; the entire management team controls nearly 47 percent. As a public shareholder, you have an economic stake but are, in practice, a bystander at the ballot. That's common at founder-led tech companies and not inherently bad — but you should know that this company's direction is set by one person.

Opportunities and risks at a glance

What speaks for Affirm:

- Sustained high growth: gross merchandise volume up 81 percent in two years to $36.7 billion, revenue up 39 percent to $3.22 billion in fiscal year 2025 — continued with volume up 35 percent in the third quarter of 2026 as well.

- First GAAP net profit in company history (+$52.2 million in 2025, after −$517.8 million the year before) and an adjusted operating income of $778.1 million — the earnings trajectory clearly points upward.

- Strong platform and data foundation: more than 23 million active consumers, about 377,000 merchants, risk models built on more than 343 million loans; top partners including Amazon, Shopify and Walmart.

- Solid liquidity and broad funding: about $2.2 billion in cash (30.06.2025), roughly $28 billion in funding capacity across about 15 lenders and about 20 institutional loan buyers; a 1-percentage-point rate jump is largely hedged, with less than $65 million of cash-flow impact.

- Credit quality has remained under control so far: 30-day delinquency in the 2 to 3 percent range despite strong growth in the loan book.

What speaks against it:

- The profit is still fragile: an operating loss of $87.3 million in 2025, an accumulated deficit of about $3.1 billion; the positive net income arose below the operating line, not from the ongoing business.

- Dilution: $499.9 million in stock-based compensation (about 15.5 percent of revenue) gets stripped out as "adjusted" — in reality, shareholders pay for it with a shrinking ownership share.

- Credit risk and rate sensitivity: provision for credit losses up 34 percent to $616.7 million, allowance for credit losses risen to 6.0 percent (31.03.2026); as a lender, Affirm depends on the economic cycle and interest rates — unlike a pure software company.

- Concentration risk: Amazon about 22 percent, top-five partners about 47 percent of volume — the growth story noticeably hangs on a handful of relationships.

- Ambitious valuation and concentrated power: a price-to-sales ratio around 7 (enterprise value about 8.5 times revenue) for a business that is, at its core, credit-driven; a dual-class structure with about 44.4 percent of votes held by the founder.

A human conclusion

Remember the adjusted-profit illusion from the opening — the reflex to breathe a sigh of relief at the word "profit" next to a fat "Adjusted" number and stop reading? Affirm is the invitation to resist it. Yes, an impressive company is growing here: fast, with a strong platform, real value for millions of buyers, and a first profit that's a genuine milestone. None of that is a facade.

But the profit has a price, and it's printed in fine text in the same filings: the business is still losing money operationally, nearly half a billion dollars in stock-based compensation gets converted into "adjusted" beauty every year, the actual business is interest- and default-dependent lending, and a fifth of volume hangs on Amazon. For that, the market demands a growth price tag that only pays off if the first profit becomes a lasting one — without the adjusted crutch.

What you make of it is your decision. And that's exactly as it should be. What matters is that you read the right line: at Affirm, the truth doesn't live in the word "profitable" — it lives in the gap between the operating loss, the tiny net profit, and the adjusted headline number. Whoever keeps that gap in view — along with the delinquency rates, the dilution and the Amazon share — reads Affirm more honestly than any headline about the "first profit."

Sources

- Affirm Holdings, Inc. — SEC annual report 10-K, fiscal year 2025 (ended June 30, 2025; filed August 28, 2025): Item 1 Business, Item 1A Risk Factors, Item 7 MD&A, Item 7A Quantitative and Qualitative Disclosures About Market Risk, financial statements and notes.

- Affirm Holdings, Inc. — SEC quarterly report 10-Q (as of March 31, 2026; filed May 7, 2026): volume, revenue and credit quality for the third quarter of fiscal year 2026.

- Affirm Holdings, Inc. — proxy statement DEF 14A of October 24, 2025: dual-class voting rights, beneficial ownership (Levchin 44.41%), the "Value Creation Award."

- Shareholder letters (exhibits to SEC Form 8-K) for the fourth quarter of fiscal year 2025 (August 28, 2025) and the third quarter of fiscal year 2026 (May 7, 2026): non-GAAP reconciliation of "Adjusted Operating Income" and the delinquency series.

- Fundamental data (metrics, valuation, annual and quarterly series); in-house stock scanner, data as of July 9, 2026.

Transparency & disclaimer: This analysis is a journalistic contextualization of publicly available information and is not investment advice, not a financial analysis in the regulatory sense, and not a solicitation to buy or sell securities. Stock investments carry substantial risks up to total loss. All information without guarantee; the data cut-off is noted in the text in each case. The author holds no position in Affirm stock at the time of publication.

Our Bottom Line at a Glance

- Business model & market positive

- A clear U.S. market leader for "Buy Now, Pay Later" with a strong platform (more than 23 million active consumers, about 377,000 merchants) and top partners including Amazon, Shopify and Walmart. At its core, though, a lender — interest income, at $1.61 billion, is the largest revenue block, not a software fee.

- Growth positive

- Sustained and documented: gross merchandise volume up 81 percent in two years to $36.7 billion, revenue up 39 percent to $3.22 billion in fiscal year 2025, continuing with volume up 35 percent in the third quarter of 2026. This is the stock's strongest side.

- Earnings quality & dilution negative

- First GAAP net profit (+$52.2 million in 2025), but still an operating loss of $87.3 million and an accumulated deficit of about $3.1 billion. The company's own headline figure, "Adjusted Operating Income" ($778.1 million), strips out $499.9 million in stock-based compensation — about 15.5 percent of revenue, borne in reality as dilution.

- Credit quality & rate sensitivity negative

- As a lender, Affirm depends on the economic cycle and interest rates: provision for credit losses up 34 percent to $616.7 million, allowance for credit losses risen to 6.0 percent (31.03.2026), 30-day delinquency risen to about 2.8 percent. Under control so far; a 1-percentage-point rate jump is largely hedged, with under $65 million of cash-flow impact.

- Concentration & governance negative

- Concentration risk: Amazon about 22 percent, top-five partners about 47 percent of volume — the growth story hangs on a handful of relationships. On top of that, a dual-class structure: founder Max Levchin controls about 44.4 percent of all votes through shares carrying 15 votes each, management nearly 47 percent.

- Valuation neutral

- Price-to-sales ratio around 7, enterprise value about 8.5 times revenue (mid-2026, about $28 billion in market value). Normal for a software company, high for a business that's credit-driven at its core — the market is explicitly paying for the tech narrative, which still needs to be backed by durable GAAP profits.

Affirm is the U.S. market leader for installment payments at checkout and is growing impressively: gross merchandise volume up 81 percent in two years to $36.7 billion, revenue up 39 percent to $3.22 billion in fiscal year 2025. A GAAP net profit showed up in the filing for the first time (+$52.2 million), but operations still ran a loss of $87.3 million, and the company's own "Adjusted Operating Income" metric of $778.1 million adds back $499.9 million in stock-based compensation. The business is, at its core, interest- and default-dependent lending (provision for credit losses up 34 percent), a fifth of volume hangs on Amazon, and at a price-to-sales ratio around 7 the market is paying a growth premium. Strong growth meets a still-fragile, dilution-carried profitability. Not investment advice.

What Our Rating Means

- If you don't own the stock

- As long as the question raised in the bottom line stays open, we see no basis for an entry.

- If you hold it in your portfolio

- Our findings offer no acute reason to sell — the checkpoints named remain decisive.

A journalistic assessment by our editorial team at the time of the deep dive, based on public sources — not investment advice and not a solicitation to buy or sell. Your personal circumstances (investment goals, risk capacity, taxes) cannot be taken into account. What our categories mean, how verdicts are formed, and what conflicts of interest exist →

Worth Noting

- Materiality gate (10.07.2026) — finding by finding: (1) Operating loss despite the first net profit (−$87.3 million operating, +$52.2 million net, accumulated deficit about $3.1 billion): an earnings-quality finding, not an existential finding, since $2.2 billion in cash and 39 percent revenue growth carry it → a pricing/structural finding. (2) Dilution from stock-based compensation ($499.9 million, about 15.5 percent of revenue, stripped out in "Adjusted Operating Income"): under the gate, a pricing finding that shifts the verdict at most one notch. (3) Credit risk/rate sensitivity (provision up 34 percent to $616.7 million, allowance for credit losses 6.0 percent, 30-day delinquency about 2.8 percent; a 1-percentage-point rate shock hedged below $65 million): currently under control → a pricing/cyclical finding; it would become an existential finding only in a funding or credit crisis (a jump in delinquency, the loss of warehouse facilities). (4) Partner concentration, Amazon at about 22 percent of volume (top five about 47 percent): per the gate's calibration (21 percent = a dent), a dent — the company would stay intact with more than 377,000 merchants → a concentration-risk dent. (5) Valuation (P/S around 7, enterprise value about 8.5× revenue) and dual-class control (Levchin about 44.4 percent of votes): a pricing/structural finding. Result: no existential finding, but a cluster of pricing/structural findings pointing the same direction against documented growth → not a "vorsicht" classification, but not a "buy" either; "beobachten," tied to sustained GAAP profitability without the adjusted crutch, the trajectory of delinquency, and the Amazon share.

- Data basis: annual report (10-K) for fiscal year 2025 (ended June 30, 2025; filed August 28, 2025) and quarterly report (10-Q) as of March 31, 2026 (filed May 7, 2026); non-GAAP figures ("Adjusted Operating Income" $778.1 million, the delinquency series) from the shareholder letters (exhibits to Form 8-K) for the fourth quarter of FY2025 and the third quarter of FY2026. Revenue breakdown FY2025: interest income $1,608.2 million, merchant network revenue $882.7 million, gains on loan sales $381.6 million, card network $231.3 million, servicing income $120.6 million.

- Special-situation screening via the EDGAR submissions index (as of 10.07.2026): no activist Schedule 13D, only passive 13G filings from institutional holders (including Vanguard and BlackRock); no announced takeover, no strategic review. Governance: founder/CEO Max Levchin controls about 44.41 percent of all votes through Class B shares carrying 15 votes each (all directors and officers combined: 46.80 percent); reincorporation from Delaware to Nevada effective 01.07.2025.

- Price and valuation figures are dated mid-2026 (market value about $28 billion on about 294 million outstanding Class A shares plus about 41 million Class B shares); analyses are evergreen, daily prices are not a buy argument.

Frequently Asked Questions

Affirm (Nasdaq: AFRM) is the U.S. market leader for "Buy Now, Pay Later" — installment payments right at the checkout counter and in the online shopping cart. Customers split a purchase into installments, often interest-free; Affirm earns money from interest, merchant fees, the resale of loans and a payment card network. Major partners include Amazon, Shopify and Walmart.

For the first time, yes — but with a catch. In fiscal year 2025 (ended June 30, 2025), Affirm reported $52.2 million in GAAP net income, its first-ever positive year. Operating income stayed negative, though, at minus $87.3 million, and the company's own "Adjusted Operating Income" metric of $778.1 million adds back, among other things, $499.9 million in stock-based compensation. Sustained profitability hasn't been proven yet.

A company-defined, non-standardized (non-GAAP) metric. It takes operating income and strips out several real expenses — chiefly the $499.9 million in stock-based compensation, plus depreciation/amortization and warrant expense. That's how an operating loss of $87.3 million turns, arithmetically, into $778.1 million of "adjusted" profit. The expenses are real; stripped out doesn't mean gone.

It's the core of the business, since interest income is Affirm's largest revenue block. The provision for credit losses rose 34 percent to $616.7 million in 2025, the allowance for credit losses reached 6.0 percent of loans (31.03.2026), and the 30-day delinquency rate reached about 2.8 percent. Manageable so far, but as a lender Affirm depends on the economic cycle and interest rates.

Heavily: Amazon accounted for about 22 percent of total gross merchandise volume in fiscal year 2025, the top five partners for 47 percent combined. Losing it wouldn't be a broken neck — Affirm has more than 377,000 merchants — but it would be a noticeable drag on the growth story the valuation rests on.

Ambitiously. In mid-2026, Affirm carries a market value of about $28 billion against roughly $3.97 billion in revenue (trailing twelve months) — a price-to-sales ratio around 7, an enterprise value of roughly 8.5 times revenue. Normal for a software company, high for a business that's credit-driven at its core. The market is paying for the tech narrative.

Founder and CEO Max Levchin. Through a dual-class structure, he holds shares carrying 15 votes each and controls about 44.4 percent of all votes; the entire management team controls nearly 47 percent. Public shareholders have an economic stake but, in practice, no real weight at the ballot.

Found an error?

Did you spot a factual error, an outdated number, or a typo in this deep dive? Let us know briefly — your report goes straight to the editorial team.