Western Digital Stock: AI Fills the Hard Drives — and Over Two-Thirds of the Record Profit Is a Paper Gain

Western Digital is now a pure-play hard-drive maker after the Sandisk spin-off — and one of the biggest winners of the AI data-center boom: revenue +45 percent, gross margin above 50 percent for the first time, debt cut from $4.75 billion to $1.6 billion. We read the annual report (10-K) and the quarterly reports (10-Q): of the $6.2 billion earned in the last nine months, $4.45 billion comes from the markup on the retained Sandisk stake, three customers supply 43 percent of revenue — and this same business was posting losses just two years ago. Not investment advice — just the reminder that even the best cycle of all time is still a cycle.

Your memory works like an overfull hard drive: once space runs short, it overwrites the oldest files first. On the stock market that means: a chart that has climbed nearly tenfold in twelve months overwrites everything that came before it — the loss years, the price wars, the warehouses full of unsold drives. What's left is a single thought: this company apparently cannot lose. That is exactly the state many investors are in right now looking at Western Digital (NASDAQ: WDC), the hard-drive maker whose storage fills the world's AI data centers. So let's make a deal: before your head deletes the old files for good, let's read together what the company itself reported to the U.S. securities regulator, the SEC — in the annual report (10-K) for the fiscal year that ended in June 2025, and in the quarterly reports (10-Q) through April 3, 2026. A filing to the SEC is honest under penalty of law, and at Western Digital it holds both truths: the best hard-drive cycle in years. And the word the chart is busy forgetting right now. In the end, you decide for yourself.

What Western Digital actually does

Western Digital was founded in 1970, is headquartered in San Jose, California, belongs to the S&P 500 index, and employed roughly 40,000 people as of the end of fiscal year 2025 — 88 percent of them in Asia, where its plants sit in Thailand, Malaysia, the Philippines and Shenzhen. The product is as unglamorous as it is indispensable: hard disk drives (HDDs) — spinning magnetic platters on which the cloud stores its data mountains, because they cost meaningfully less per terabyte than flash chips. Important for your bearings: the company you'd be buying today is not the Western Digital of two years ago. On February 21, 2025, the group spun off its entire flash-storage business as Sandisk — since then Western Digital has been a pure-play hard-drive maker with a single reporting segment. The annual report describes the new company like this:

"We are a leading developer, manufacturer, and provider of data storage devices and solutions based on hard disk drive ('HDD') technology. […] As global data creation continues to accelerate, particularly in the age of AI, and as the need to store and retain data also grows, we believe HDDs will continue to remain the preferred technology for storing large volumes of data as the most economical solution to the large cloud data centers for their mass storage needs."

— Western Digital, SEC annual report 10-K for fiscal year 2025, Item 1 "Business"

Three end markets remain: Cloud (high-capacity drives for data centers — the dominant business), Client (drives for PCs and notebooks) and Consumer (external storage off the shelf at the electronics store). The technology behind it — ePMR, OptiNAND, UltraSMR — all points at one goal: more terabytes per platter, meaning falling cost per stored data point. Only two serious competitors still build hard drives worldwide: Seagate and Toshiba. A three-supplier market with exploding demand — that sounds like a money-printing machine. Sounds like marketing? Partly, yes. But the numbers below show: right now, it actually is one. The question this analysis asks is what you're paying for that — and what happens when the cycle turns. One more housekeeping detail that will save you confusion: Western Digital's fiscal year does not end in December, but on the Friday closest to June 30 — sometimes 52 weeks, sometimes 53. "Fiscal year 2025" ran from late June 2024 to June 27, 2025; the current fiscal year 2026 exceptionally has 53 weeks and ends July 3, 2026. Wherever you see "Q3 2026," it means the quarter from January through early April 2026.

Where the stock shows up in our scanner

We run about 3,500 stocks through our scanners every day. Western Digital lights up in 3 scanners (data as of July 9, 2026) — and the selection is notable: Joel Greenblatt: Magic Formula (high return on capital at a reasonable price), Martin Zweig: Growth With Reason, and the Buffett criteria (Buffettology). These are not overheated momentum filters, but quality and value strategies. On top of that, the data sheet shows a relative strength of 97 — the stock has outrun 97 percent of the market lately, up a good 260 percent in six months and nearly tenfold in twelve months (data as of July 9, 2026). Before you read that as a double seal of approval, an honest note from the engine room: value scanners run on the most recently reported earnings. For a cyclical stock at its peak, every metric looks healthiest exactly when the cycle has run the farthest — the formula has no way of knowing whether record margins are the new normal or the summit. That is precisely the tension at the heart of this analysis: a real, potentially multi-year AI demand boom — priced as if it were no longer a cycle at all, but a permanent state. Hold onto that sentence; it's the thread running through everything that follows. And two more numbers from the same data sheet that don't fit the celebration: the price-to-sales ratio sits around 21.6, and recent insider filings (Form 4) count 19 sales against 1 purchase (data as of July 9, 2026). More on that later.

The numbers: a cycle revs up

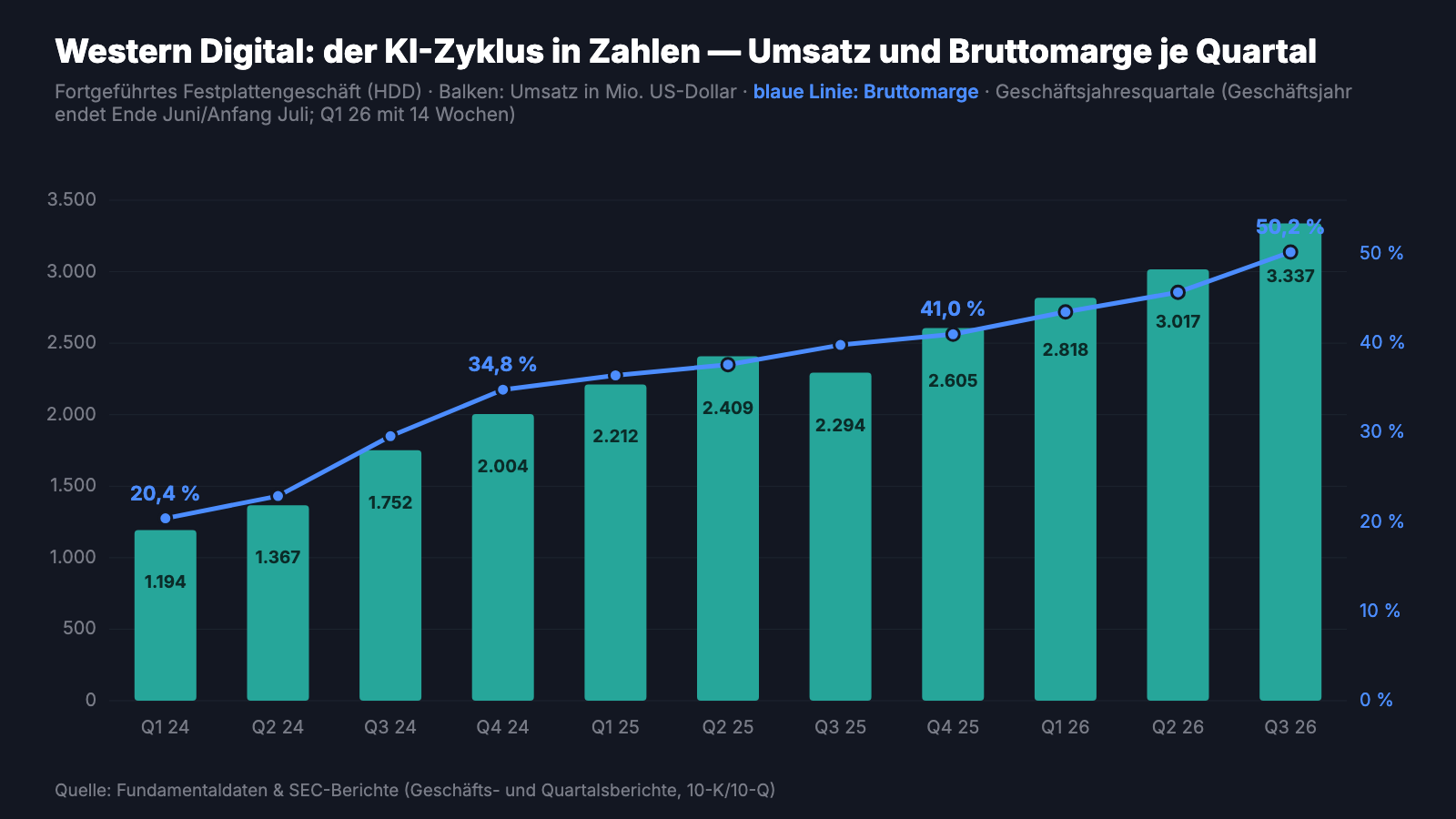

First, what genuinely impresses — and it rightly does. In the third quarter of fiscal year 2026 (January through early April 2026), Western Digital generated $3.34 billion in revenue, 45 percent more than the year-ago quarter. The driver isn't an accounting trick but physics and pricing power: exabytes shipped rose 34 percent (an exabyte is a billion gigabytes), and the price per exabyte climbed 9 percent. When a manufacturer sells more and pushes through higher prices at the same time, that's scarcity. The Cloud business — hard drives for data centers — grew 48 percent and now accounts for 89 percent of group revenue. Gross margin climbed to 50.2 percent; a year earlier it was 39.8 percent, two years earlier 29.6 percent. For context: 50 percent gross margin is software territory — for a hardware maker with factories, clean rooms and 40,000 employees, that's an exceptional number.

The longer-run lines hold up too: in fiscal year 2025 (through June 27, 2025), revenue grew 51 percent to $9.52 billion, operating income was $2.33 billion, net income $1.89 billion. The first nine months of fiscal year 2026 brought $9.17 billion in revenue (+33 percent — with one small assist: the first quarter had 14 weeks instead of 13 because of the 53-week fiscal year). Nine-month operating cash flow: $2.54 billion; in the third quarter alone, $978 million of free cash flow remained after capital spending. And management is now handing out money with both hands: $1.92 billion in buybacks over nine months (a $6 billion program in total, of which $3.93 billion remained authorized as of April 3, 2026), plus a quarterly dividend introduced in spring 2025 that was raised 20 percent to $0.15 per share as of June 2026. For the final quarter of fiscal year 2026, management guided in late April to another 36 to 44 percent revenue growth and 51 to 52 percent adjusted gross margin. Anyone judging only the present has little to complain about. So let's look where the SEC filings are more honest than any chart: the fine print.

What the filings say — the uncomfortable truths

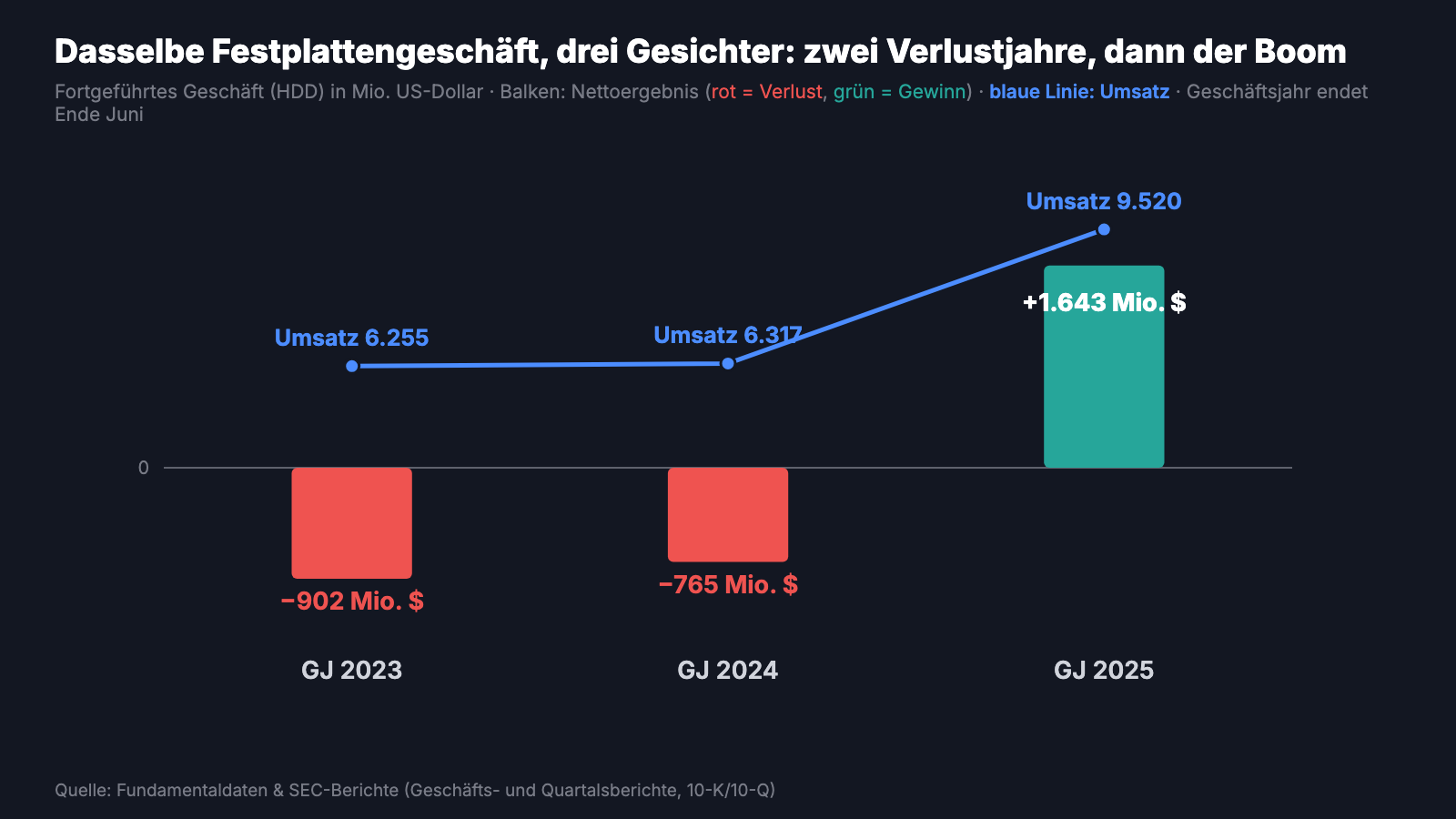

Uncomfortable truth no. 1: this same business posted losses two years ago — hard drives remain cyclical

The most important file your memory is overwriting right now carries the years 2023 and 2024. Today's celebrated hard-drive business — the same factories, the same customers, at its core the same products — lost $902 million in fiscal year 2023 and $765 million in fiscal year 2024 (continuing operations, i.e. excluding the now-spun-off flash segment). Revenue back then sat at $6.3 billion — a third below today's run rate. What happened? Nothing exotic: after the pandemic boom, cloud companies simply stopped reordering for roughly two years, warehouses filled up, prices fell, factories ran under capacity. The annual report describes this recent past dryly — in the very same paragraph that celebrates the AI upswing:

"In fiscal 2025, we saw an improvement in the supply and demand dynamic relative to the prior year, and we anticipate that digital transformation, including the AI data-cycle, will drive improved market conditions in the long term. […] As an example, in fiscal 2024, we and our industry experienced a supply-demand imbalance, which led to reduced shipments, negatively impacted pricing, and resulted in business realignment charges and charges for unabsorbed manufacturing overhead costs due to the underutilization of facilities as we temporarily scaled back production […]."

— Western Digital, SEC annual report 10-K 2025, Item 7 "Management's Discussion and Analysis"

The point isn't that the old losses have to return — AI demand is real, customers are now signing longer-term contracts according to the quarterly report (10-Q), and the report speaks of greater predictability. The point is: a business that swings from plant-closure charges to a 50 percent gross margin within 24 months can swing in both directions. And notably, even in the middle of the boom, Western Digital booked another $103 million in restructuring charges in the first nine months of fiscal year 2026, mostly severance — management itself keeps the cost structure on a diet, as if it doesn't fully trust the calm.

Uncomfortable truth no. 2: three customers supply 43 percent of revenue

Customer concentration translates like this: if your neighbor tells you business is booming, but three buyers account for almost half of the revenue — would you wince a little? That's exactly the structure Western Digital has after the spin-off, and the annual report names it explicitly as a risk factor:

"As a result of the Separation, there is increased revenue concentration in our Cloud end market and among our top customers. For the year ended June 27, 2025, the Cloud end market accounted for 88% of our total revenue and our top 10 customers accounted for 68% of our net revenue, with three customers each accounting for 10% or more of the Company's net revenue."

— Western Digital, SEC annual report 10-K 2025, Item 1A "Risk Factors"

And the concentration is rising, not falling: in the third quarter of fiscal year 2026, the ten largest customers accounted for 71 percent, three customers for 17, 15 and 11 percent — 43 percent combined — of revenue. For comparison: in fiscal years 2023 and 2024, not a single customer crossed the 10 percent mark. The report doesn't name names — the profile (Cloud, hyperscale data centers) points to the large platform companies, whose creditworthiness isn't the issue. The issue is their bargaining power and their ordering rhythm: this exact buyer group collectively paused orders in 2023/2024 and triggered the loss years by doing so. In fairness, this belongs to the honest picture too: per the quarterly report, customers are now committing earlier and for longer — the filing speaks of extended supply agreements, with most of the revenue running through long-term contracts with fixed order commitments. That dampens the risk; it doesn't remove it: even a long-term contract eventually comes up for renegotiation — and then three customers with 43 percent of revenue are sitting at the table. We dissected how quickly a customer cluster like this can turn in our analysis of Applied Optoelectronics — there it was two customers, and the mechanism is the same, just one size smaller.

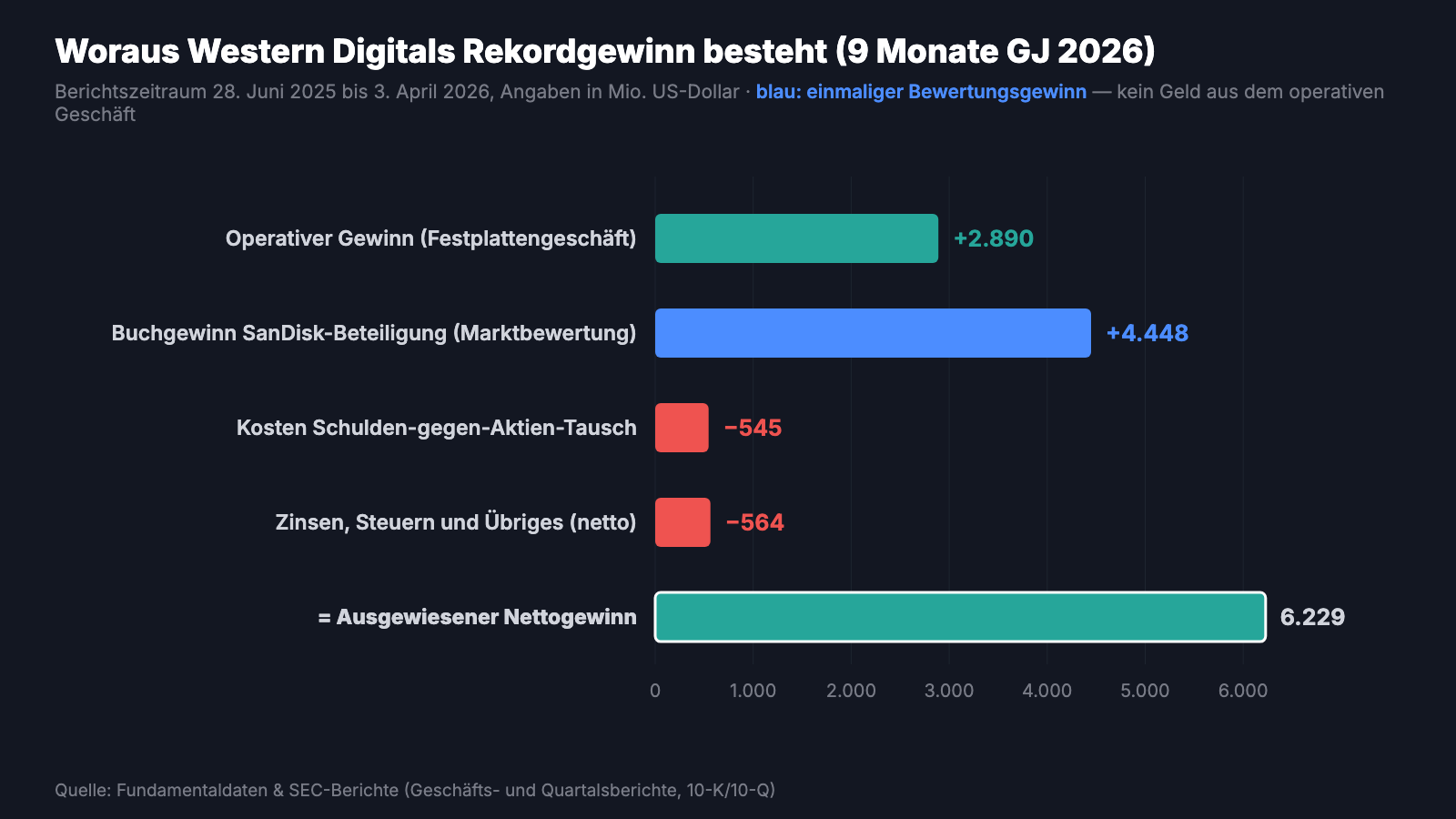

Uncomfortable truth no. 3: more than two-thirds of the record profit is a paper gain, not hard-drive money

Now for the number making headlines: $6.23 billion in net income in just nine months (June 28, 2025 through April 3, 2026), reported earnings per share of $16.05. Sounds like earning power has quintupled. It hasn't. At the spin-off, Western Digital initially kept a 19.9 percent stake in Sandisk — and because flash storage is exploding right along with the AI boom, the market value of that retained stake has multiplied. Accounting rules require Western Digital to mark that stake to market every quarter and run the change through the income statement as a gain or loss. The quarterly report says it plainly:

"The change primarily reflects an unrealized gain of $4.45 billion on our retained interest in Sandisk in the current period based on the mark-to-market value as of April 3, 2026 […]. These changes were partially offset by $545 million of costs incurred in connection with the debt-for-equity exchange as described above."

— Western Digital, SEC quarterly report 10-Q as of April 3, 2026, Item 2 "Management's Discussion and Analysis"

Do the math: of $6.23 billion in net income, $4.45 billion — 71 percent — is a valuation gain on a stock position Western Digital is already winding down anyway. Operationally, from the actual hard-drive business, came $2.89 billion. Still excellent! But look at what that does to the ratios: in the third quarter Western Digital reported $8.20 in earnings per share — adjusted for the paper gain and other special items, the current report (8-K) accompanying the quarterly results put it at $2.72. A price-to-earnings ratio built on the reported earnings therefore looks roughly three times cheaper than it actually is operationally — and those exact numbers also feed value scanners (see above). By the way: the same position worked in the opposite direction in 2025 — in fiscal year 2025 the Sandisk stake dragged results down by a loss of $772 million. Mark-to-market is not a one-way street.

Uncomfortable truth no. 4: the $37.72 convertible note — and why $1.9 billion in buybacks barely dents the share count

The balance-sheet cleanup is the most elegant move in these filings — and it has one expensive detail. First, the elegance: Western Digital cut its debt from $4.75 billion (June 27, 2025) to $1.6 billion (April 3, 2026) without touching meaningful amounts of its own cash — payment came mostly in Sandisk shares: in June 2025, 21.3 million Sandisk shares retired about $800 million of term-loan debt; in February 2026, 5.8 million Sandisk shares worth $3.62 billion retired a bridge loan plus the remaining term loan. The price of speed: a discount of roughly $539 million to the exchange counterparties, booked as an expense. And even the last 1.7 million Sandisk shares are still working — per a current report (8-K) dated June 11, 2026, Western Digital is swapping just over a million of them directly for its own shares: a buyback paid with the ex-subsidiary's stock. What's left is a single debt position — and it has teeth:

"The 2028 Convertible Notes are convertible at the option of any holder beginning August 15, 2028, at a conversion price of approximately $37.72 per share of common stock as of April 3, 2026."

— Western Digital, SEC quarterly report 10-Q as of April 3, 2026, Note 7 "Debt"

Why this matters: the note, with $1.6 billion in face value, dates back to November 2023 — a $37.72 conversion price, hedged only up to $50.41. Insider filings (Form 4) from June 2026 document executives selling at prices above $500 — meaning noteholders can obtain shares at a fraction of the market price. Everything above the hedge ceiling is paid for by shareholders: in new shares or in cash. In June 2026, per a current report (8-K), Western Digital already retired $858.4 million of the note's face value — against cash for the principal plus shares for the entire remaining conversion value. That explains an unremarkable line in the quarterly report: despite buying back 13.1 million shares for $1.92 billion, the share count fell net only from 347 to 345 million — convertible-note conversions, the forced conversion of preferred stock in February 2026 (plus 7 million shares) and employee programs refilled almost all of it. Remember this: buybacks that merely soak up yesterday's dilution don't make your slice of the pie any bigger.

And AI? The profiteer that doesn't sell any AI itself

Western Digital doesn't sell artificial intelligence — no model, no chip that computes. The company sells the shelf where AI stores its memories. That's exactly how the filings put it: the quarterly report (10-Q) names AI adoption explicitly as a demand driver on top of Cloud growth ("The adoption of artificial intelligence ('AI') and workloads driven by hybrid data is driving additional growth in data storage as well."), and CEO Irving Tan got fundamental in the current report (8-K) accompanying the quarterly results: "Virtually every AI workload, from training, inference, agentic AI to physical AI, creates data that is stored persistently and cost-efficiently on HDDs." Internally, the company uses AI too — the annual report mentions "the AI technologies that we employ for business purposes," though notably in the chapter on cyber risk. And that's also where the report's most honest AI sentence sits: the effect of generative AI on storage markets "is still unfolding and could evolve unpredictably, and it is difficult to accurately forecast related demands." Hold those two sentences side by side: AI is the reason for the boom — and, at the same time, the reason nobody can seriously say how long it lasts. We described what it looks like when a supplier sits directly on the AI data stream in our Credo analysis; Western Digital is the more conservative, more physical version of the same bet.

Valuation: you're paying for the perfect cycle — in advance

Now the question your overwritten memory no longer asks: what does all of this cost? As of the July 9, 2026 data cutoff, Western Digital traded at roughly 21.6 times revenue and 35 times reported earnings of the trailing four quarters. Both numbers need the translation from uncomfortable truths no. 1 and 3: the price-to-earnings ratio runs on earnings that are largely Sandisk paper gains — measured against adjusted earnings ($2.72 instead of $8.20 per share in the third quarter), the real multiple is roughly three times what the raw number suggests. And a price-to-sales ratio around 21.6 prices a hardware cyclical like a software subscription business: it assumes 50 percent gross margin and double-digit price growth per exabyte are the normal state — not the peak of a cycle whose trough was two years ago. "The professionals' view" is nonetheless friendly: 25 analysts cover the stock, consensus is clearly on buy, with estimates penciling in nearly 80 percent earnings growth for the current fiscal year (data as of July 9, 2026). Against that stands a quieter signal from inside the company: recent insider filings (Form 4) count 19 sales against a single purchase. In early June 2026, for instance, chief operating officer Vidyadhara Gubbi sold 2,475 shares at $556.24, followed by general counsel Cynthia Tregillis and board member Martin Cole at prices around $528 to $546 — all properly disclosed, much of it routine and in small lots, but the direction is uniform: those who know the company from the inside are using these prices to exit more than to enter. Two dates belong on your calendar: fourth-quarter results with the first outlook for fiscal year 2027 arrive in late July 2026 — and starting November 15, 2026, Western Digital can call the convertible note early, which could finally close the dilution chapter.

Opportunities and risks at a glance

What speaks for Western Digital:

- Real, measurable AI tailwind: revenue +45 percent, exabytes shipped +34 percent, price per exabyte +9 percent in the third quarter of fiscal year 2026; customers are committing earlier and for longer per the quarterly report (10-Q).

- Record profitability: gross margin 50.2 percent (prior year: 39.8), operating margin 35.7 percent; guidance points to 51 to 52 percent adjusted gross margin for the final quarter.

- An oligopoly with only three suppliers (Western Digital, Seagate, Toshiba), roughly 4,500 active patents, vertical integration in read/write heads and platters — market entry for newcomers is practically impossible.

- A radically repaired balance sheet: debt cut from $4.75 billion to $1.6 billion (paid mostly with Sandisk shares), $2.05 billion in cash, $978 million of free cash flow in the third quarter alone.

- Shareholder-friendly capital allocation: a $6 billion buyback program ($3.93 billion remaining as of April 3, 2026), dividend +20 percent to $0.15 per quarter as of June 2026.

What speaks against it:

- A cyclical business with a fresh history of losses: minus $902 million (FY 2023) and minus $765 million (FY 2024) in the same hard-drive business; the annual report (10-K) documents underutilization and falling prices as recently as 2024.

- Concentration risk: Cloud equals 89 percent of revenue, the top-10 customers 71 percent, three customers 43 percent (Q3 FY2026) — the same buyer group that collectively paused orders in 2023/2024.

- The record profit is misleading: $4.45 of the $6.23 billion nine-month profit is a paper gain on the Sandisk stake; adjusted, Western Digital earned $2.72 rather than $8.20 per share in the third quarter — value ratios and scanner hits rest on a flattered denominator.

- Valuation prices in perfection: price-to-sales around 21.6, reported P/E around 35 (roughly three times that on an adjusted basis), after the stock nearly tenfolded in twelve months (data as of July 9, 2026).

- Dilution and signals: the convertible note ($1.6 billion, $37.72 conversion price, hedged only up to $50.41) partly offsets the buybacks — the share count fell only from 347 to 345 million despite $1.92 billion of repurchases; add 19 insider sales against 1 purchase and a $539 million discount in the debt exchange; a shift to HAMR technology and unpredictable generative-AI demand remain open risks flagged in the 10-K.

A human conclusion

Back to your internal hard drive. Over the past twelve months it has saved a beautiful file: a three-supplier market, exploding AI demand, 50 percent margins, a repaired balance sheet, a rising dividend — all of it is real, all of it is in the SEC filings, and none of it is something we want to talk you out of. But before you buy, restore the files the price chart has overwritten: the same company with two loss years, plants running short-time and falling prices — not twenty years ago, but not even two. Add three customers carrying 43 percent of revenue; a record profit that is 71 percent the market value of a stock position; a convertible note quietly printing new shares while buybacks retire old ones out front; and insiders who, at these prices, would rather sell than buy. None of it is a scandal — it's simply the complete picture of an excellent cyclical business at the best point of its cycle so far, priced as if the cycle no longer existed. Maybe AI demand really does carry these record margins for years more — management is guiding toward it, and the order book supports it. Or maybe a single pause quarter from the three big customers is enough for the market to suddenly remember the word buried in the fine print. The next reality check lands in late July 2026, when Western Digital reports full-year results and its first outlook for 2027. Until then: save both files — the boom and the trough. What you make of it is your decision. And that is exactly as it should be.

Sources

All original documents used in this analysis — to read for yourself:

- Western Digital Corporation — SEC annual report 10-K for fiscal year 2025 (ended June 27, 2025; filed August 14, 2025)

- Western Digital Corporation — SEC quarterly report 10-Q as of April 3, 2026 (filed May 1, 2026)

- Western Digital Corporation — SEC quarterly report 10-Q as of January 2, 2026 (filed January 30, 2026)

- Western Digital Corporation — SEC quarterly report 10-Q as of October 3, 2025 (filed October 31, 2025)

- Western Digital Corporation — Current report (8-K) with press release on Q3 2026 results (April 30, 2026)

- Western Digital Corporation — Current report (8-K) on the $858.4 million convertible-note exchange (June 3, 2026)

- Western Digital Corporation — Current report (8-K) on the Sandisk-share-for-own-share exchange (June 11, 2026)

- Western Digital Corporation — Proxy statement (DEF 14A) for the 2025 annual meeting (October 6, 2025)

- Insider filings (Form 4) and the complete SEC filing history: EDGAR overview for Western Digital (sec.gov)

- Fundamental data (metrics, valuation, analyst consensus; data as of July 9, 2026), reconciled with the SEC filings and the SEC's XBRL data.

- Screener and rating data: in-house stock scanner (data as of July 9, 2026).

Transparency & disclaimer: This analysis is a journalistic contextualization of publicly available information and is not investment advice, not a financial analysis in the regulatory sense, and not a solicitation to buy or sell securities. Stock investments carry substantial risks up to total loss. All information without guarantee; the data cut-off is noted in the text in each case. The author holds no position in Western Digital stock at the time of publication.

Our Bottom Line at a Glance

- AI demand & pricing power positive

- Revenue +45 percent, exabytes shipped +34 percent and price per exabyte +9 percent in the third quarter of fiscal year 2026; customers are committing earlier and for longer per the quarterly report (10-Q) — scarcity with pricing power in a three-supplier market.

- Profitability positive

- Gross margin 50.2 percent (prior-year quarter: 39.8), operating margin 35.7 percent, $978 million of free cash flow in the quarter; guidance points to 51 to 52 percent adjusted gross margin for the final quarter of 2026.

- Balance sheet & capital allocation positive

- Debt cut from $4.75 billion to $1.6 billion (mostly in exchange for Sandisk shares), $2.05 billion in cash, a $6 billion buyback program and a 20 percent dividend increase to $0.15 per quarter (June 2026).

- Cyclicality & history negative

- The same hard-drive business lost a combined roughly $1.7 billion in fiscal years 2023 and 2024; the annual report (10-K) documents underutilization and falling prices as recently as 2024 — and even during the boom, $103 million in restructuring charges hit the books (9M FY 2026).

- Concentration risk negative

- Cloud end market equals 89 percent of revenue, the top-10 customers 71 percent, three customers 43 percent (Q3 FY2026); this same hyperscaler buyer group collectively paused orders in 2023/2024 and triggered the loss years.

- Valuation, paper gains & signals negative

- Price-to-sales around 21.6 and a reported P/E around 35 (data as of July 9, 2026), with 71 percent of the nine-month profit being a Sandisk paper gain (adjusted: $2.72 instead of $8.20 per share in Q3); the $37.72 convertible note keeps diluting, and insider filings (Form 4) show 19 sales versus 1 purchase.

Western Digital is the rare case where the boom story is fully backed by SEC filings: real AI demand, record margins, a repaired balance sheet, rising payouts. But the price paid for that assumes the best hard-drive cycle in years is a permanent state — while the reported profit is mostly a paper gain, three customers carry 43 percent of revenue, and insiders are mostly selling. Not investment advice.

What Our Rating Means

- If you don't own the stock

- At the current price level, we don't see a sufficient margin of safety for an entry.

- If you hold it in your portfolio

- Our findings offer no reason to sell.

A journalistic assessment by our editorial team at the time of the deep dive, based on public sources — not investment advice and not a solicitation to buy or sell. Your personal circumstances (investment goals, risk capacity, taxes) cannot be taken into account. What our categories mean, how verdicts are formed, and what conflicts of interest exist →

Worth Noting

- Fiscal-year quirk: a 52/53-week year ending on the Friday closest to June 30; "Q3 2026" means January through early April 2026, and fiscal year 2026 ends July 3, 2026 (53 weeks, with a 14-week Q1 — a small assist to nine-month growth).

- The Sandisk wind-down is nearly complete: as of April 3, 2026 Western Digital still held 1.7 million Sandisk shares (market value $1.19 billion) and swapped just over a million of them for its own shares in June 2026; mark-to-market effects can keep swinging reported earnings in either direction (FY 2025: minus $772 million, 9M FY 2026: plus $4.45 billion).

- From November 15, 2026, Western Digital can call the 2028 convertible note early; in June 2026 it already exchanged $858.4 million of face value for cash plus shares. Daily share-price swings of 6.8 percent (data as of July 9, 2026) — this is not a low-volatility name.

Frequently Asked Questions

Western Digital has been a pure-play hard-disk-drive (HDD) maker for cloud data centers, PCs and consumers since February 21, 2025. Its entire flash-storage business was spun off as Sandisk and is now a separate publicly traded company; Western Digital initially kept a 19.9 percent stake but has all but wound it down by mid-2026 — mostly by exchanging it for its own debt and its own shares.

Because AI data centers need to store enormous, permanent volumes of data, and hard drives are the cheapest technology for that. In the third quarter of fiscal year 2026 (January through April 2026), revenue rose 45 percent to $3.34 billion, exabytes shipped grew 34 percent, and the price per exabyte rose 9 percent — gross margin hit a record 50.2 percent. The stock has climbed nearly tenfold in twelve months (data as of July 9, 2026).

Very: the same continuing hard-drive business that earned $1.64 billion in net income in fiscal year 2025 posted losses of $902 million and $765 million in fiscal years 2023 and 2024. The annual report (10-K) documents a supply-demand imbalance for 2024, with pricing pressure, throttled production and costs from underutilized plants.

More than two-thirds of it is a paper gain: of the $6.23 billion in net income for the first nine months of fiscal year 2026, $4.45 billion comes from the markup on the retained Sandisk stake (mark-to-market as of April 3, 2026), not from the hard-drive business. Western Digital earned $2.89 billion operationally; adjusted earnings per share in the third quarter were $2.72 rather than the reported $8.20.

Debt fell from $4.75 billion (June 27, 2025) to $1.6 billion (April 3, 2026), paid mostly with Sandisk shares instead of cash. A $6 billion buyback program is running ($3.93 billion remaining), and the quarterly dividend rose 20 percent to $0.15 as of June 2026. One caveat: the remaining convertible note ($1.6 billion, $37.72 conversion price) keeps creating new shares — the share count barely moved despite $1.92 billion in buybacks.

Western Digital uses a 52/53-week fiscal year ending on the Friday closest to June 30. "Fiscal year 2025" ended June 27, 2025; fiscal year 2026 exceptionally has 53 weeks (a 14-week first quarter) and ends July 3, 2026. Quarter labels like "Q3 2026" therefore mean January through early April 2026 — worth remembering when comparing against calendar-year figures.

Found an error?

Did you spot a factual error, an outdated number, or a typo in this deep dive? Let us know briefly — your report goes straight to the editorial team.