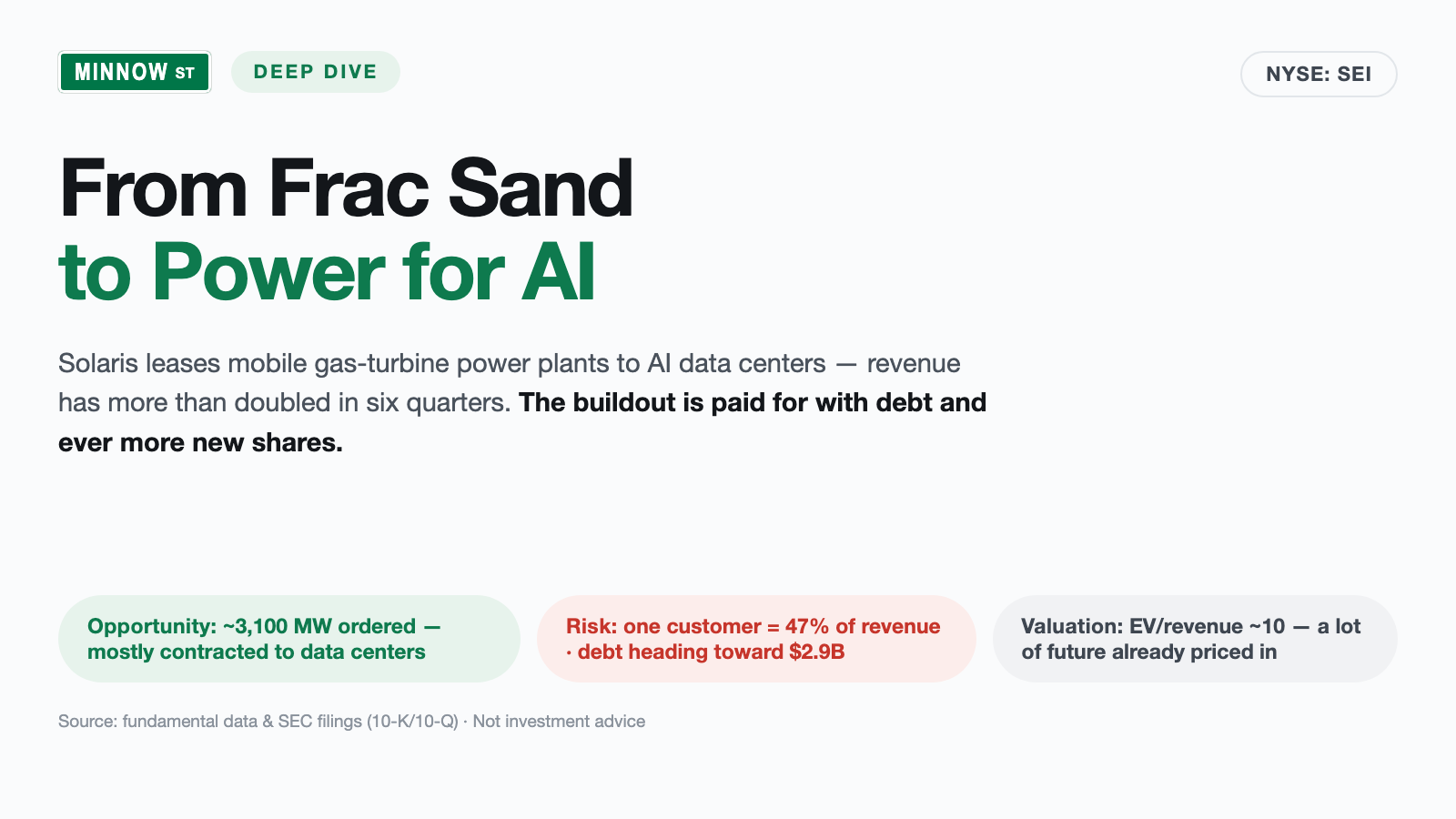

Solaris Energy Stock: Power for AI — Built on Borrowed Money

In 18 months, Solaris Energy turned from a frac-sand logistics company into a lessor of mobile gas-turbine power plants for AI data centers. Revenue has more than doubled over six quarters — our scanner flags triple-digit growth. We read the annual report (10-K) and the quarterly report (10-Q): behind the AI-power story stand capital expenditures above annual revenue, deeply negative cash flow, a debt tower heading toward $2.9 billion — and a single customer who is almost half the company. Not investment advice, just the second look.

There are two words that make many investors briefly check their judgment at the door: "power" and "AI." Everyone knows by now that artificial intelligence guzzles staggering amounts of electricity, and that data centers wait years for a grid connection. So when you find a company that appears to solve exactly this bottleneck, and whose revenue has just doubled, you feel that familiar tug in your stomach — the fear of missing out on the next big trend. Let's call it by its name: FOMO. It whispers, "buy now, before everyone else notices." That reflex is expensive precisely because it skips one simple question: what is paying for this growth? A company can grow for real — and still overextend itself financially at the same time. So let's make a deal: before you touch a single share of Solaris Energy Infrastructure (NYSE: SEI), we read together what its reports to the U.S. securities regulator, the SEC, actually say. An SEC filing is honest under penalty of law. And at Solaris it tells a fascinating, but also uncomfortable, story. In the end, you decide for yourself.

What Solaris actually does

Solaris spent years as an unremarkable service provider to the fracking industry: the company leased mobile silo and conveying systems that store and dose frac sand at oil and gas well sites — a solid but cyclical niche business with about $300 million in annual revenue; to this day the company is registered with the SEC as "Solaris Oilfield Infrastructure, Inc." Then, in September 2024, came the acquisition of Mobile Energy Rentals ("MER" for short) — and within 18 months it turned the company upside down.

The new business is as simple as it is timely: mobile gas-turbine power plants for lease. Anyone building an AI data center today often waits years for a grid connection. Solaris instead places containerized gas turbines, along with control and distribution equipment, "behind the meter" — meaning directly on the site, bypassing the public grid — and leases the mobile equipment fleet out under long contracts. Picture it as an emergency-power fleet on wheels, only it is not a backup, but a permanent primary supply. The annual report sums up the dual business soberly:

"We provide modular and scalable equipment-based solutions for power generation, control and distribution, and the management of raw materials in oil and natural gas well completions."

— Solaris Energy Infrastructure, Inc., SEC annual report 10-K, fiscal year 2025, Item 1 "Our Company"

Since then, Solaris has run two segments: Solaris Power Solutions — the turbine-leasing business for data centers and industry, the entire growth engine — and Solaris Logistics Solutions, the legacy frac-sand business, which is stagnating to mildly shrinking. The company is run by a dual leadership: founder William A. Zartler as Chairman and Co-CEO, alongside Amanda Brock (formerly CEO of Aris Water Solutions) as Co-CEO. A real, sought-after business — the catch is not in the turbine container, but in the balance sheet.

Where the stock shows up in our scanner

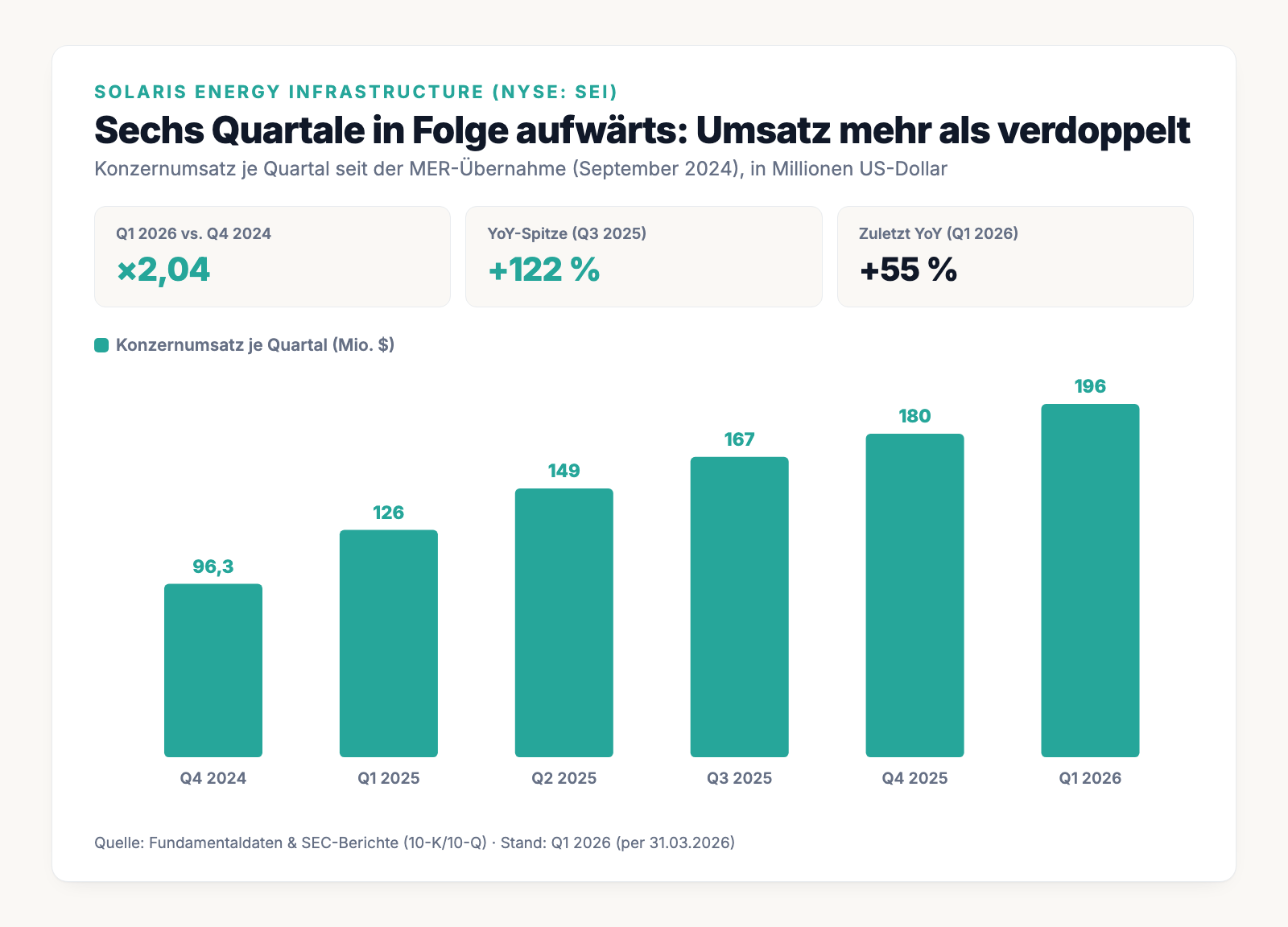

We run about 3,500 stocks through our scanners every day. Solaris lights up in more than twenty of them (data as of July 8, 2026), including our strictest growth filter, "Triple-Digit Revenue Growth." This filter looks for companies whose quarterly revenue has at least doubled compared to roughly a year and a half earlier while climbing quarter after quarter. Solaris cleanly satisfies both conditions: revenue climbed from $96.3 million (fourth quarter of 2024) over six consecutive quarters to $196.2 million (first quarter of 2026) — a clean doubling.

Unlike some other companies in this scanner, this growth is not a bookkeeping trick: the Power segment delivered $333.5 million in revenue in 2025 (up from just $38.6 million in 2024) and is even profitable, at an Adjusted EBITDA margin of about 56 percent. And yet the second look is worthwhile, because the scanner only measures that revenue rose, not how expensively it was bought. Remember this tension — real growth, but entirely prefinanced. It is the connecting thread for everything that follows. Here is how to get there yourself: open our "Triple-Digit Revenue Growth" scanner and search for the row SEI.

What the filings say — the uncomfortable truths

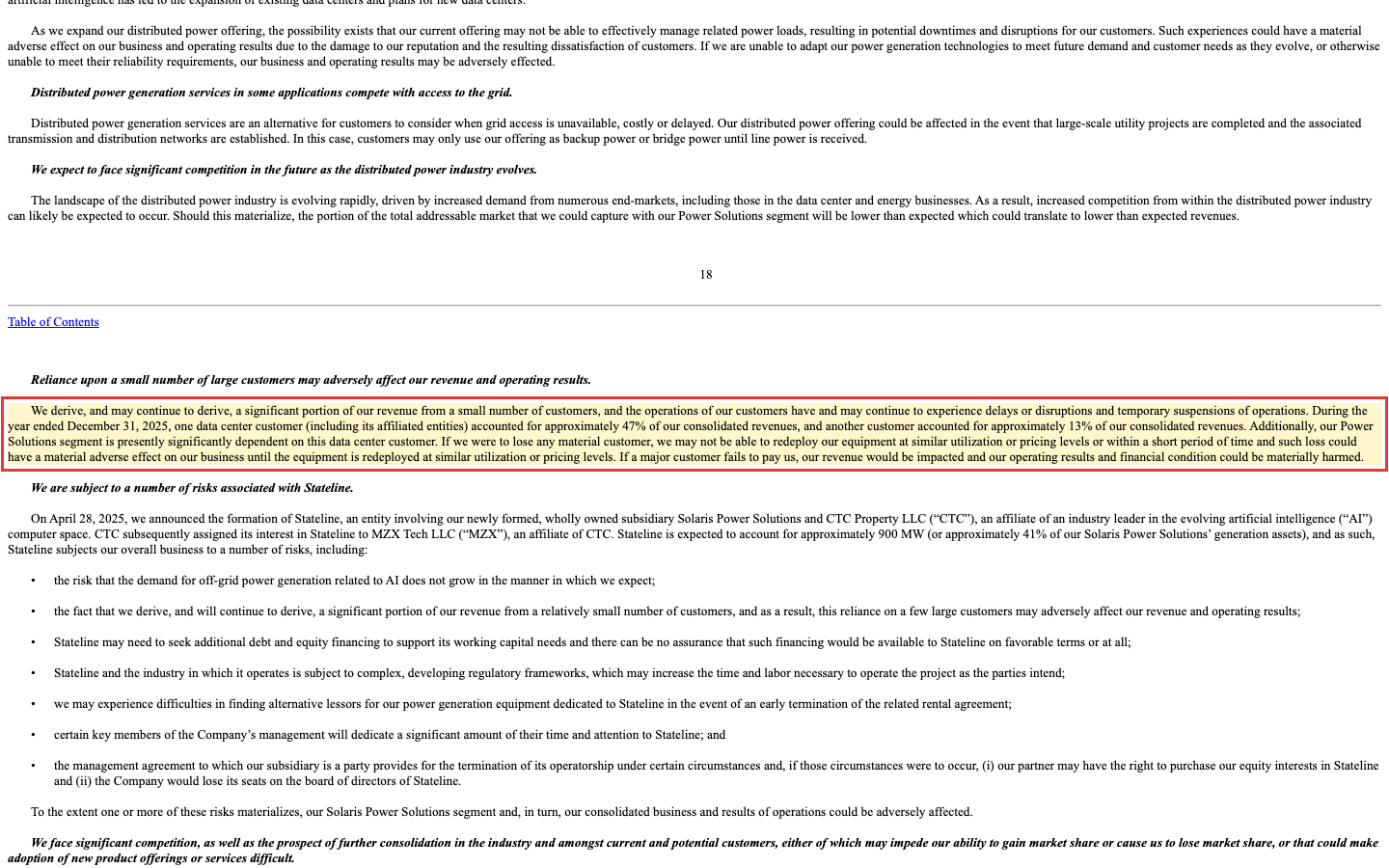

Uncomfortable truth no. 1: a single customer is almost half the company

The finest growth story counts for little if it hangs by a single thread. At Solaris that thread is spelled out in black and white under the risk factors:

"During the year ended December 31, 2025, one data center customer (including its affiliated entities) accounted for approximately 47% of our consolidated revenues, and another customer accounted for approximately 13% of our consolidated revenues. Additionally, our Power Solutions segment is presently significantly dependent on this data center customer."

— Solaris Energy Infrastructure, Inc., SEC annual report 10-K, fiscal year 2025, Item 1A "Risk Factors"

In the growth segment the dependence is even starker: per the 10-K, the same customer accounted for 88 percent of Power-segment revenue in 2025. At the core of the relationship is a contract for up to roughly 900 megawatts with an initial seven-year term, run through the Stateline Power joint venture. That sounds like stability — and it is, as long as the customer keeps paying. But it also means: a single data center decides half of group revenue. The filing itself warns that if that customer were lost, Solaris could not quickly re-lease its turbines "at similar utilization or similar rates." A textbook concentration risk.

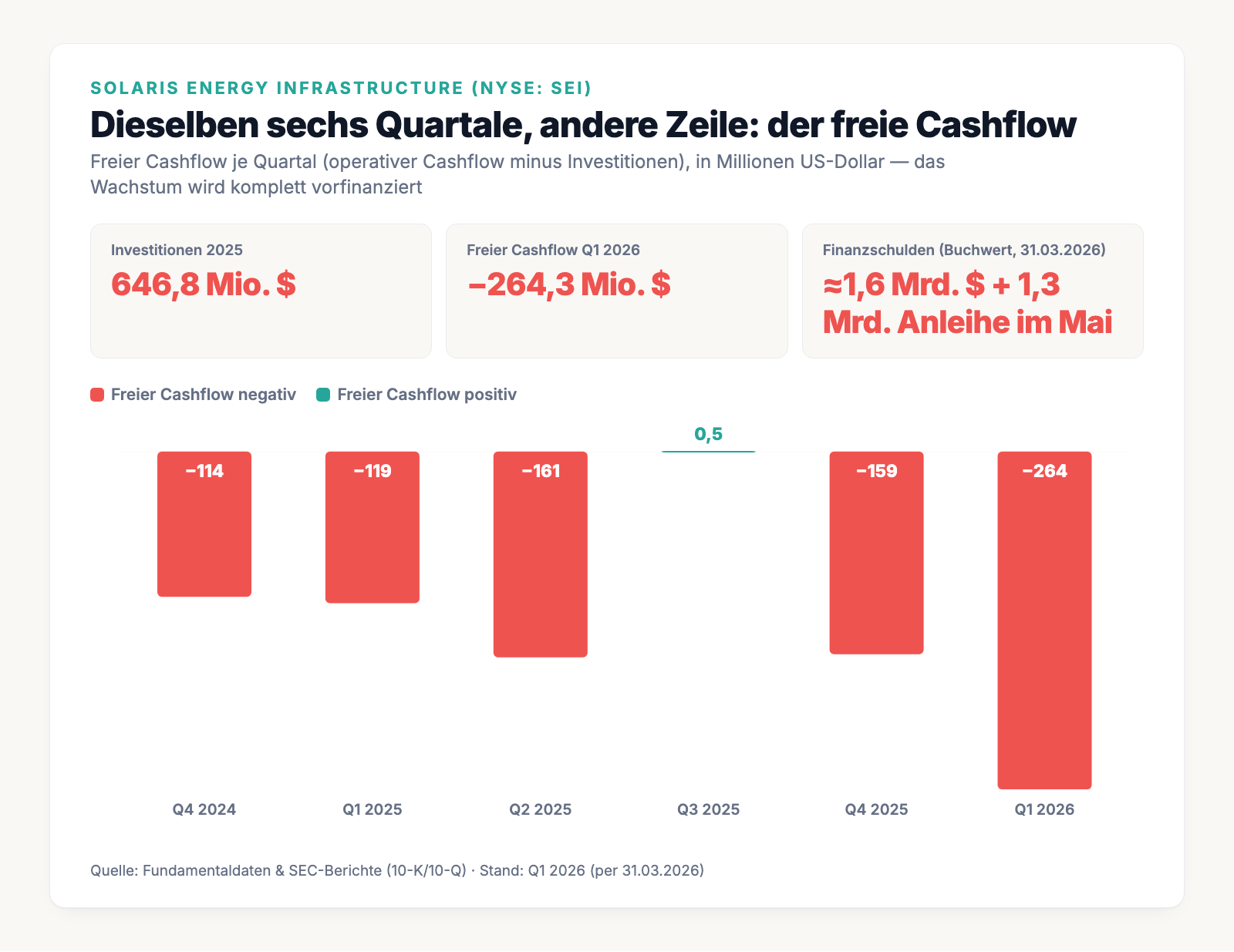

Uncomfortable truth no. 2: this growth is built on borrowed money — free cash flow is deeply negative

Now to the price tag on this growth. Turbines, containers, control equipment — all of it has to be bought and installed before the first lease contract brings in money. How expensive that is, the 10-K states itself:

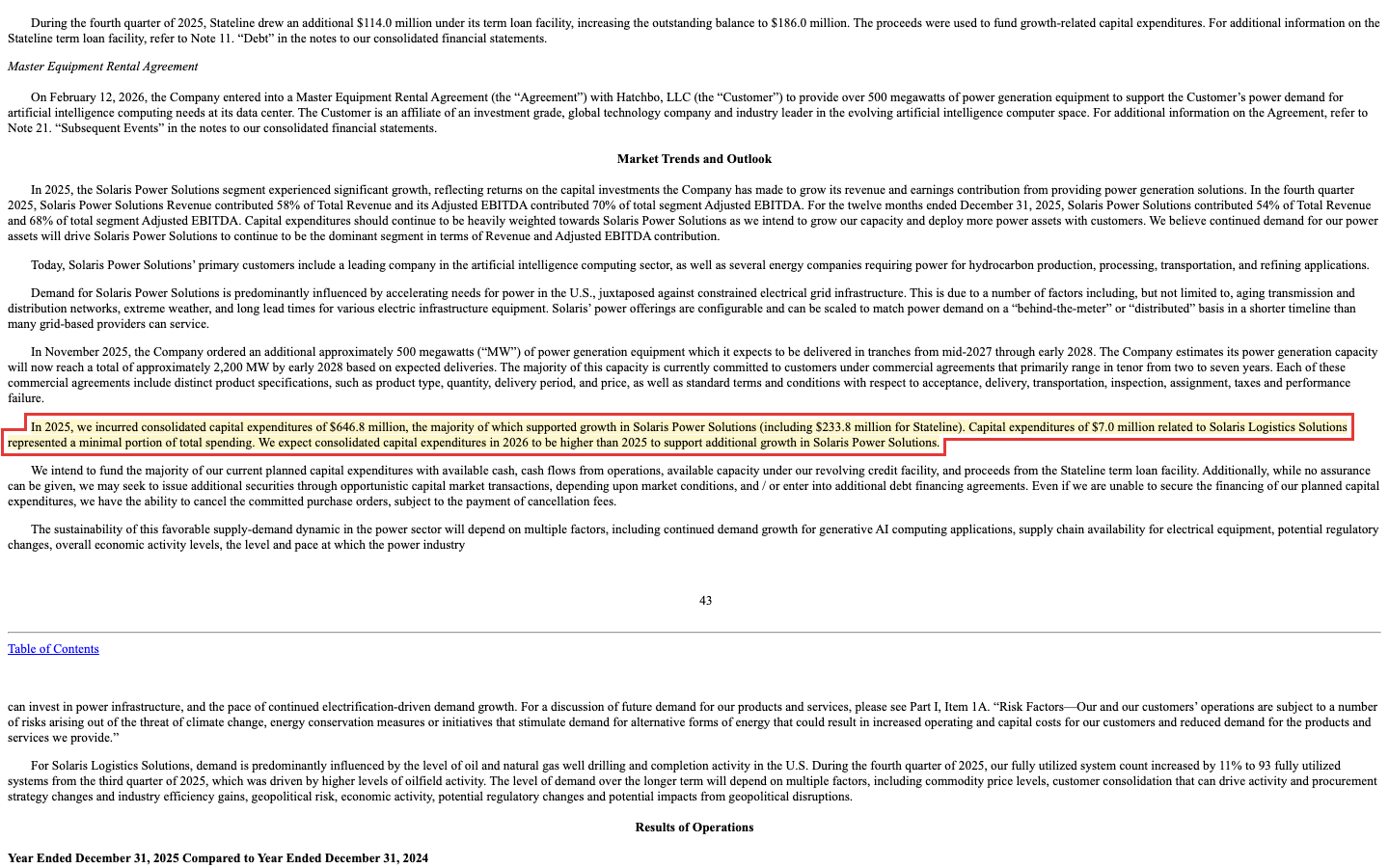

"In 2025, we incurred consolidated capital expenditures of $646.8 million, the majority of which supported growth in Solaris Power Solutions (including $233.8 million for Stateline). […] We expect consolidated capital expenditures in 2026 to be higher than 2025 to support additional growth in Solaris Power Solutions."

— Solaris Energy Infrastructure, Inc., SEC annual report 10-K, fiscal year 2025, Item 7 (Liquidity)

Let that order of magnitude sink in: capital expenditures of $646.8 million in 2025 exceeded the entire annual revenue of $622.2 million — and even more is planned for 2026. In the first quarter of 2026 alone, $343.4 million flowed into new capacity. The consequence shows up in free cash flow — what is genuinely left over after all spending: it was deeply negative in five of six quarters, and in the first quarter of 2026, at minus $264.3 million, more negative than ever:

That is not a scandal in itself — every capital-intensive build-out phase looks this way. But it is why this stock is no sure thing: as long as the turbines are still being installed, the money does not come from the business — it comes from outside, from loans and new shares. And that is exactly where it gets tight.

Uncomfortable truth no. 3: the debt tower is growing fast

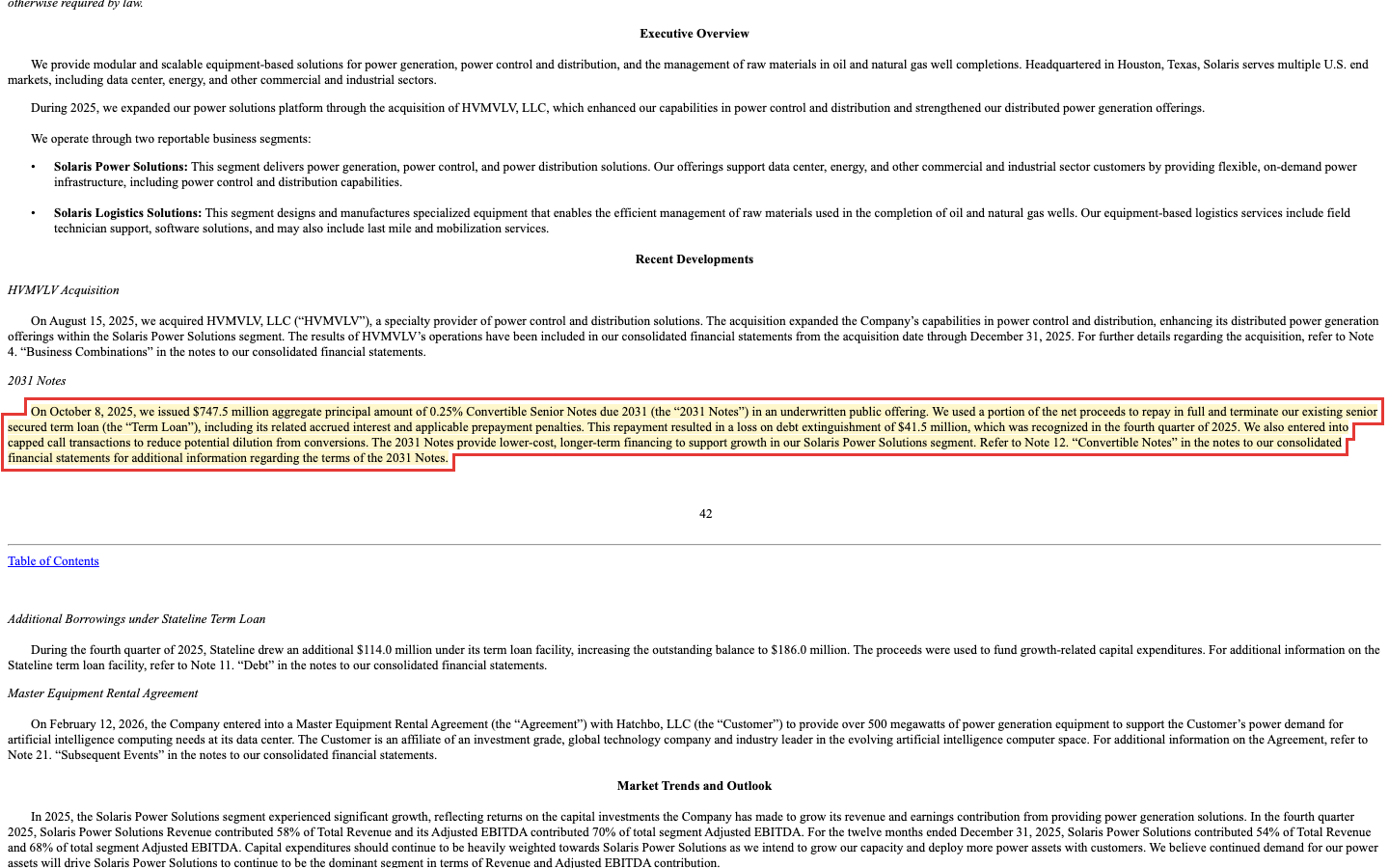

Where does the money for $647 million a year in capital spending come from if cash flow is negative? To a large extent, from debt — and it is piling up at a breathtaking pace. One building block is a convertible note that simultaneously closed an expensive legacy chapter:

"On October 8, 2025, we issued $747.5 million aggregate principal amount of 0.25% Convertible Senior Notes due 2031 (the "2031 Notes") in an underwritten public offering. We used a portion of the net proceeds to repay in full and terminate our existing senior secured term loan (the "Term Loan"), including its related accrued interest and applicable prepayment penalties. This repayment resulted in a loss on debt extinguishment of $41.5 million, which was recognized in the fourth quarter of 2025."

— Solaris Energy Infrastructure, Inc., SEC annual report 10-K, fiscal year 2025, Item 7 ("2031 Notes")

That is only one piece. Add it all up, and financial debt has climbed from about $0.2 billion (term loans, end of 2025) to a run rate of $2.9 billion: as of March 31, 2026, about $1.6 billion was already on the books (including a $300 million bridge loan from Goldman Sachs with a term of only 364 days — a sign of how tightly the financing was timed). In May 2026 came a $1.3 billion note at 6.375 percent on top. One detail worth knowing: most of the interest is currently being "capitalized" into the turbine book values and therefore does not yet weigh on the income statement — in 2025, only $22.4 million in net interest was actually paid in cash. The full interest burden will not hit the balance sheet until the turbines are running. By the way, this same debt lever shapes other AI-infrastructure bets too — we dissected it in our Bitdeer analysis, where a bitcoin miner turned data-center operator burned $1.7 billion in cash in a single year.

Uncomfortable truth no. 4: ever more shares — and part of the profit isn't even yours

The second money spigot besides debt is new shares. And it is running hard: Class A shares rose about 61 percent in 18 months — through an equity placement, through shares used as purchase price for acquisitions (Genco, GESA), and through stock-based compensation. On top come $902.5 million in convertible notes that can one day turn into further shares. For you as a shareholder, that means dilution — picture a pizza that keeps getting cut into more slices: your slice gets smaller even if you sell nothing.

Even more uncomfortable is the corporate structure behind it, the so-called "Up-C" structure. Simplified: alongside the ordinary Class A shareholders (that's you), there are legacy owners around founder Zartler who hold their stake as an interest in the underlying operating company and own voting Class B shares. The 10-K discloses that they can exchange and sell these interests one-for-one into Class A shares — further dilution potential. And already today a large part of the profit belongs to them: of $58.4 million in group net income in 2025, $28.2 million went to these minority holders, with only the remainder going to shareholders of the publicly traded Inc. On top there is a tax liability (a "Tax Receivable Agreement") of $75 million that passes most future tax benefits on to the legacy owners. Nearly half the profit and a chunk of future tax benefits, in other words, flow to a group that is not the same as the shareholders who buy the stock on the exchange.

Uncomfortable truth no. 5: the core business is shrinking — and part of the revenue is only passed through

That leaves the question of how solid the foundation under the AI story really is. Two observations from the quarterly report (10-Q) cloud the picture. First: the old leg, the frac-sand business, no longer carries its weight. Logistics revenue fell to $67.7 million in the first quarter of 2026, down from $77.0 million in the year-earlier quarter — minus 12 percent. The entire growth burden therefore rests on the Power segment alone.

Second: a significant part of Power revenue is not even earned with the company's own turbines. Of the $105.4 million in leasing revenue in the first quarter of 2026, $44.6 million was "sublease" revenue — that is, re-leased third-party capacity, about 42 percent. That is a clever growth lever, but it typically brings thinner margins and more dependence on suppliers. And on the company's own turbine supply there is a disclosed single-supplier risk: one supplier provides a material part of the equipment. The much-cited pipeline of roughly 3,100 megawatts through the end of 2029 is also, for the most part, only ordered, not delivered — about 630 megawatts were deployed at the end of 2025. Much of it today is still paper that has yet to become electricity.

Valuation — what the market is actually paying for here

The valuation deserves a close look, because one commonly cited data point is misleading. Multiplying the actually outstanding Class A and Class B shares (roughly 76 million shares combined after the most recent acquisitions) by mid-2026 price levels yields a market value on the order of about $5 billion. Against that stands trailing-twelve-month revenue of about $692 million. Adding net debt after the May note gets you to an enterprise value implying an EV/revenue of roughly 10 and an EV/EBITDA around 24. Put in context: that is no longer a valuation on substance, but a pronounced growth premium.

In other words: the market is already paying for the contracted roughly 3,100 megawatts as though they were long since on the grid and earning rent — but only about 600 to 700 megawatts have actually been delivered and deployed so far. That can work out if the turbines arrive as planned and the long contracts hold. It can also disappoint if deliveries slip or the one large customer wavers. Notably, a significant part of the market is betting against it — short interest recently stood at about 22 percent of the float, one of the highest in the momentum universe. At the same time, eight analysts rate the stock a consensus "Buy." Two camps, one stock — another sign of how much future is priced in here.

Opportunities and risks at a glance

What speaks for Solaris:

- Structural tailwind: AI data centers wait years for grid connections; "behind the meter" generation is often the only fast route. Solaris fills the gap with an already-ordered turbine pipeline of about 3,100 megawatts through the end of 2029 — and turbine slots are scarce.

- Contracted, long-term deals instead of spot business: several major contracts of 7 to 10 years plus options; one new customer prepaid $45.4 million in rent — a sign of negotiating power.

- The economics already work: the Power segment posted $71.9 million in Adjusted EBITDA on $128.5 million of revenue in the first quarter of 2026 — a margin of about 56 percent; the group earns real operating profit.

- Founder-led with skin in the game (insider ownership of about 10 percent, a buy signal in the scanner), an experienced dual leadership; the high short interest also carries squeeze potential if deliveries continue.

What speaks against it:

- Concentration risk: a single data-center customer accounted for about 47 percent of group revenue and 88 percent of Power-segment revenue in 2025; losing that customer would be hard to replace quickly.

- Growth built on borrowed money: capital expenditures above annual revenue, free cash flow deeply negative in five of six quarters (minus $264 million in the first quarter of 2026).

- Rapidly rising debt: from about $0.2 billion to a run rate of $2.9 billion, including a $1.3 billion note at 6.375 percent; part of the interest is still being capitalized and will hit the income statement only later.

- Massive dilution (Class A up 61 percent in 18 months, $902.5 million in convertible notes) and an Up-C structure through which nearly half the profit and future tax benefits flow to legacy owners; on top, a shrinking legacy business and single-supplier risk on turbines.

A human conclusion

Remember the FOMO from the beginning — that tug at the words "power" and "AI"? Having looked into the filings, you now know that both halves of the story are true. Yes, Solaris has reinvented itself and delivers real, even profitable growth at one of the most exciting points of the AI boom: the power without which no data center computes. That is not hot air. But this growth is paid for with everything a balance sheet can give — with capital expenditures above revenue, with a debt tower that has multiplied, and with ever more new shares. And a large part of it hangs on a single customer.

What you make of it is your decision. And that is exactly as it should be. If you buy Solaris, you are not buying a comfortable cash-flow machine, but a leveraged bet on the AI-power boom: a bet that the ordered megawatts arrive on time, that the long contracts hold, and that cash flow eventually reaches shareholders after interest and build-out. If the bet works out, a rare capability scales into a huge market. If it doesn't, a wobbling major customer and a mountain of debt collide. What matters is simply that you know what you are betting on — both halves, not just the two magic words. By the way, we dissected what real growth on a razor-thin cash cushion feels like in our Shoals Technologies analysis too — a second case where a genuine order-book boom and a till that held just $1.9 million at the time sit inside the very same stock.

Sources

- Solaris Energy Infrastructure, Inc. — SEC annual report 10-K, fiscal year 2025 (filed February 27, 2026)

- Solaris Energy Infrastructure, Inc. — SEC quarterly report 10-Q, Q1 2026 (as of March 31, 2026, filed May 1, 2026)

- Fundamental data (metrics, valuation, analyst consensus, quarterly series); in-house stock scanner, data as of July 8, 2026.

Transparency & disclaimer: This analysis is a journalistic contextualization of publicly available information and is not investment advice, not a financial analysis in the regulatory sense, and not a solicitation to buy or sell securities. Stock investments carry substantial risks up to total loss. All information without guarantee; the data cut-off is noted in the text in each case. The author holds no position in Solaris Energy stock at the time of publication.

Our Bottom Line at a Glance

- Business model & market positive

- Genuine structural tailwind: AI data centers wait years for grid connections, and "behind the meter" gas turbines are often the only fast route. Solaris fills the gap with an ordered pipeline of about 3,100 megawatts through the end of 2029 and long contracts; turbine slots are scarce.

- Revenue growth & profitability positive

- Not a bookkeeping trick but a genuine ramp-up: group revenue rose for six quarters in a row, from $96.3 to $196.2 million; Power revenue rose from $38.6 million (2024) to $333.5 million (2025). The Power segment operates profitably at an Adjusted EBITDA margin of about 56 percent.

- Cash flow & financing negative

- This growth is built on borrowed money: 2025 capital expenditures of $646.8 million exceeded annual revenue, and free cash flow was deeply negative in five of six quarters (minus $264.3 million in the first quarter of 2026). Financial debt rose from about $0.2 billion to a run rate of $2.9 billion, including a $1.3 billion note at 6.375 percent.

- Customer concentration negative

- A single data-center customer accounted for about 47 percent of group revenue and 88 percent of Power-segment revenue in 2025. At its core is a contract for up to 900 megawatts; per the risk factor, losing that customer could hardly be replaced quickly on similar terms.

- Dilution & structure negative

- Class A shares up 61 percent in 18 months, with $902.5 million in convertible notes forming a further share pipeline. Through the Up-C structure, $28.2 million of $58.4 million in profit went to minority holders in 2025, plus a $75 million tax receivable liability to legacy owners. The legacy business (Logistics) is shrinking, and there is single-supplier risk on turbines.

- Valuation neutral

- About $5 billion in market value (order of magnitude, mid-2026) against roughly $692 million in trailing-twelve-month revenue works out, including debt, to an EV/revenue of about 10 and an EV/EBITDA around 24 — the market is paying for the contracted megawatts as if they were already on the grid. Short interest sits around 22 percent, yet the analyst consensus is still "Buy".

Solaris Energy is both things at once: a genuine, even profitable growth story at one of the most exciting points of the AI boom — power for data centers — and a highly leveraged bet. Revenue has doubled over six quarters, but it is paid for with capital expenditures above annual revenue, deeply negative cash flow, debt on a run rate toward $2.9 billion and ongoing dilution. On top of that, almost half the company hangs on a single customer. Not investment advice.

What Our Rating Means

- If you don't own the stock

- As long as the question raised in the bottom line stays open, we see no basis for an entry.

- If you hold it in your portfolio

- Our findings offer no acute reason to sell — the checkpoints named remain decisive.

A journalistic assessment by our editorial team at the time of the deep dive, based on public sources — not investment advice and not a solicitation to buy or sell. Your personal circumstances (investment goals, risk capacity, taxes) cannot be taken into account. What our categories mean, how verdicts are formed, and what conflicts of interest exist →

Worth Noting

- Was named "Solaris Oilfield Infrastructure, Inc." until 2024; the turn toward power leasing began with the MER acquisition in September 2024.

- The database field for market capitalization ($7.83 billion) is a data artifact and does not match the share count on the SEC cover pages; the reliable figure is the calculation via Class A plus B shares (roughly 76 million shares) to about $5 billion in market value.

- Most of the interest is currently being capitalized into the turbine book values (2025 cash-paid net interest was only $22.4 million); the full interest burden will not hit the income statement until the equipment is in operation.

Frequently Asked Questions

Solaris spent years as a service provider to the fracking industry, leasing mobile silo systems for frac sand. Since acquiring Mobile Energy Rentals (September 2024), the company also leases mobile gas-turbine power plants placed "behind the meter" directly on the grounds of AI data centers and industrial customers, operated under 7- to 10-year contracts. There are two segments: Solaris Power Solutions (power generation, the growth engine) and Solaris Logistics Solutions (the legacy sand business).

Because the new Power segment is taking off: group revenue rose for six quarters in a row, from $96.3 to $196.2 million, and Power revenue alone rose from $38.6 million (2024) to $333.5 million (2025). Unlike some other scanner hits, this is not a bookkeeping trick but a genuine business ramp-up — deployed turbine capacity grew from about 230 to 630 megawatts. That growth, however, is entirely prefinanced.

Financial debt has climbed rapidly — from about $0.2 billion (term loans, end of 2025) to about $1.6 billion as of March 31, 2026, including a $300 million bridge loan from Goldman Sachs. A $1.3 billion note at 6.375 percent was added in May 2026, putting debt on a run rate toward $2.9 billion. Part of the interest is currently being capitalized and will not hit the income statement until the turbines are running.

The concentration risk: per the annual report (10-K), about 47 percent of group revenue and 88 percent of Power-segment revenue came from a single data-center customer in 2025. At its core is a contract for up to about 900 megawatts with an initial seven-year term. If that customer were to fall away, Solaris's own risk factor states it could not quickly re-lease its turbines on similar terms.

No, it carries a pronounced growth premium. At a market value of about $5 billion (order of magnitude, mid-2026) and trailing-twelve-month revenue of about $692 million, including debt that works out to an EV/revenue of roughly 10 and an EV/EBITDA around 24. The market is paying for the contracted roughly 3,100 megawatts as if they were already on the grid — only about 600 to 700 megawatts have actually been delivered.

Yes, noticeably. Class A shares rose about 61 percent in 18 months through equity placements, stock-funded acquisitions and compensation; on top of that, $902.5 million in convertible notes form a future share pipeline. Through the "Up-C" structure, $28.2 million of the group's $58.4 million net income went to minority holders in 2025, and a $75 million tax liability channels future tax benefits mostly to the legacy owners.

Found an error?

Did you spot a factual error, an outdated number, or a typo in this deep dive? Let us know briefly — your report goes straight to the editorial team.