Riot Platforms Stock: AI Label on the Front, Ingredient List on the Back

Riot Platforms has already reinvented itself twice — from a biotech company to a Bitcoin miner, and now to an AI data center landlord. The AMD lease is real, and the stock has gained about 196 percent in twelve months. We read the annual report (10-K) and the quarterly report (10-Q): of $33.2 million in data center revenue in the first quarter of 2026, $32.2 million was cost reimbursement — and a self-mined bitcoin costs Riot more than it's worth. Not investment advice: we're just turning the package around.

It happens every day at the supermarket: a bright sticker gets slapped on a familiar old package — "New!" — and suddenly everyone reaches for it. On the stock market, that sticker currently reads "AI data center," and hardly any company has slapped it on with as much conviction as Riot Platforms (NASDAQ: RIOT). A Bitcoin miner that suddenly leases data centers to chipmaker AMD, a stock up roughly 196 percent in twelve months (data as of July 8, 2026) — and inside you, herd instinct kicks in: everyone's reaching for it, so it must be good. That reflex is the most expensive one in the whole store, because it makes you skip the one move every purchase deserves: turning the package around and reading the ingredient list. So let's make a deal. Before you touch a single Riot share, we'll read together what the company told the U.S. securities regulator, the SEC — filings are honest under penalty of law. AI label on the front, ingredients on the back. In the end, you decide for yourself.

Remember the central tension of this analysis: the market is already paying Riot like a data center operator — the numbers so far show a Bitcoin miner that mines below full cost and sells its bitcoin treasury to fund the pivot. That's the thread running through everything that follows.

What Riot Platforms actually does

At its core, Riot is an industrial Bitcoin miner. Picture huge warehouses full of specialized computers ("miners") solving computational puzzles around the clock; as a reward, the Bitcoin network credits the winner with newly minted bitcoin. It's a gold-rush business where the pickaxe is an electricity bill: whoever gets the cheapest power and runs the most efficient machines wins. Riot runs three sites for this, together more than 1.2 gigawatts of developed capacity — the Rockdale Facility in Texas (700 megawatts, including the land itself, owned outright since January 2026), the Corsicana Facility in Texas (400 megawatts, with a planned build-out to about 1 gigawatt) and two sites in Kentucky (about 137 megawatts, with an expansion to 232 megawatts planned by the end of 2026). In 2025, Riot mined 5,686 bitcoin this way, up 17.8 percent from the prior year. On top of that sits its own engineering division, which builds power-distribution equipment — for its own facilities and for outside customers.

So much for the old package. The new sticker arrived in two steps: in 2025 Riot built its own data center team, and in January 2026 came the first real tenant — and what a tenant it is:

"In January 2026, the Company entered into the AMD Lease, a long-term data center lease agreement with AMD, a leading innovator in high-performance computing, graphics, and visualization technologies, at the Rockdale Facility. The AMD Lease includes an initial deployment of 25 MW of critical IT load capacity […] The AMD Lease carries a term of 10 years, with three five-year extension options."

— Riot Platforms, Inc., SEC quarterly report 10-Q, Q1 2026, Note 3 "Data Center Operations"

In April 2026, AMD already exercised an expansion option: another 25 megawatts, bringing the total to 50 — with reserved capacity and first-refusal rights on up to 200 megawatts in total. Since the first quarter of 2026, Riot has reported "Data Center" as its own segment, alongside Bitcoin Mining and Engineering. That's the same narrative as other energy-infrastructure bets in the AI boom: AI data centers wait years for grid interconnection, and Riot is sitting on power that's already built out. Sounds like marketing? Partly, yes. But the AMD lease is real, the segment is real — and that's why we classify Riot in our company-specific AI rating as "Sells AI": data center capacity for AI and high-performance computing has demonstrably become a revenue source here. The interesting question isn't whether the story exists. It's how much of it is already showing up in the numbers. By the way: reinventing itself is practically a tradition at Riot — the company was founded in Colorado in 2000 as the biotech company AspenBio, turned into "Riot Blockchain" in 2017 amid crypto fever, and has been called Riot Platforms since late 2022. The current pivot is already its second major transformation.

Where the stock shows up in our scanner

Every day we run about 3,500 stocks through our scanners. Riot lights up in 15 scanners (data as of July 8, 2026) — and the pattern is unmistakable: with almost no exception, they are momentum and trend-following filters. The stock sits in the RS-Leader scanner (relative strength 88 out of 99 on a one-month view), in Power Trend, on the Weinstein Stage 2 list, among the "Doublers" with a doubled share price, and in the institutional-accumulation filter — 14 quarters of big investors adding to positions stand against just 2 quarters of selling. Translated: the big money is buying, the trend points steeply upward, and the stock trades only about 8 percent below its 52-week high. To replicate it yourself: open the RS-Leader scanner and search for the row RIOT.

Just as telling is where Riot doesn't show up: in not a single quality or substance filter. The Levermann score sits at a meager 2 points, the price-to-sales ratio at around 16, and the insider signal reads a clear sell — the filings on record show 7 insider sales against 0 purchases (data as of July 8, 2026). A scanner only measures that the herd is running, not where to. For the where, we have to go into the filings.

The numbers: a record year — and a roller coaster

First, what genuinely impressed in 2025: revenue jumped from $376.7 million to $647.4 million — up 72 percent. The driver was simple: the average annual bitcoin price was $101,350, up from $66,488 the year before, and on top of that Riot's hashrate grew to 38.5 exahash per second (42.5 by the end of March 2026). The engineering division grew too, from $38.5 million to $64.7 million — demand for power-distribution equipment for other companies' data centers is, per the 10-Q, at a record level. A real, growing business, not an accounting mirage.

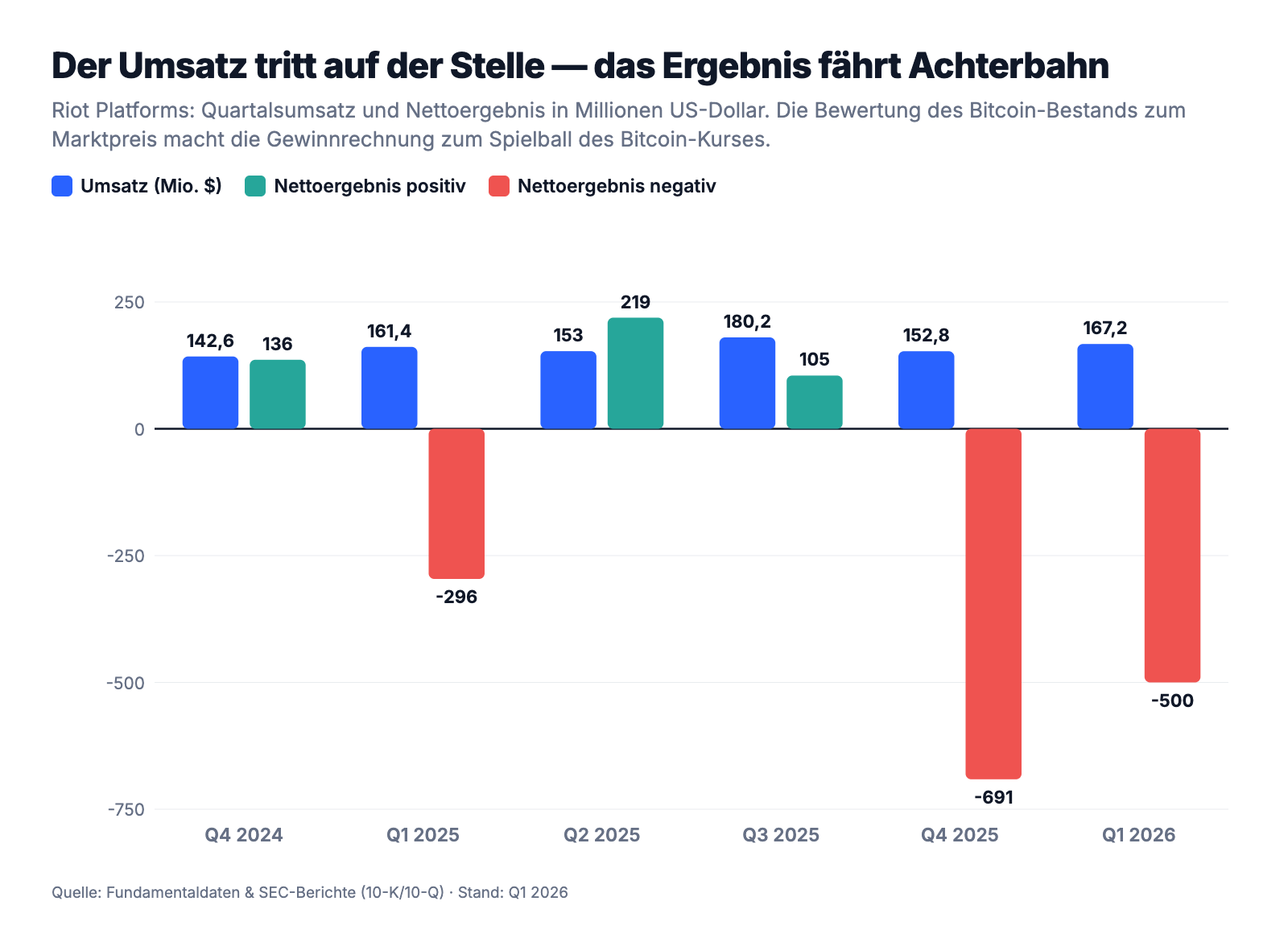

But since the fourth quarter of 2024, the quarterly numbers tell a different story: revenue has been moving sideways between $142.6 million and $180.2 million — in the first quarter of 2026 it was $167.2 million, only 3.6 percent more than the same quarter a year earlier. And underneath that, a roller coaster is raging:

The reason for these wild swings is an accounting rule: Riot marks its bitcoin holdings to market on every reporting date, and the change in value flows straight through the income statement. When bitcoin rises, paper gains appear — $457.4 million of them in 2024. When it falls, the same mechanism turns into a loss accelerator: $115.9 million of write-downs sat in the books for 2025, with another $326.7 million in the first quarter of 2026 alone. On the bottom line, Riot lost $663.2 million in fiscal year 2025 and another $500.5 million in the first quarter of 2026. Buy Riot stock, and to a significant degree you're buying a leveraged bitcoin price with an attached electricity bill. Which brings us to the ingredient list.

What the filings say — the uncomfortable truths

Uncomfortable truth no. 1: 97 percent of the AI revenue is cost reimbursement

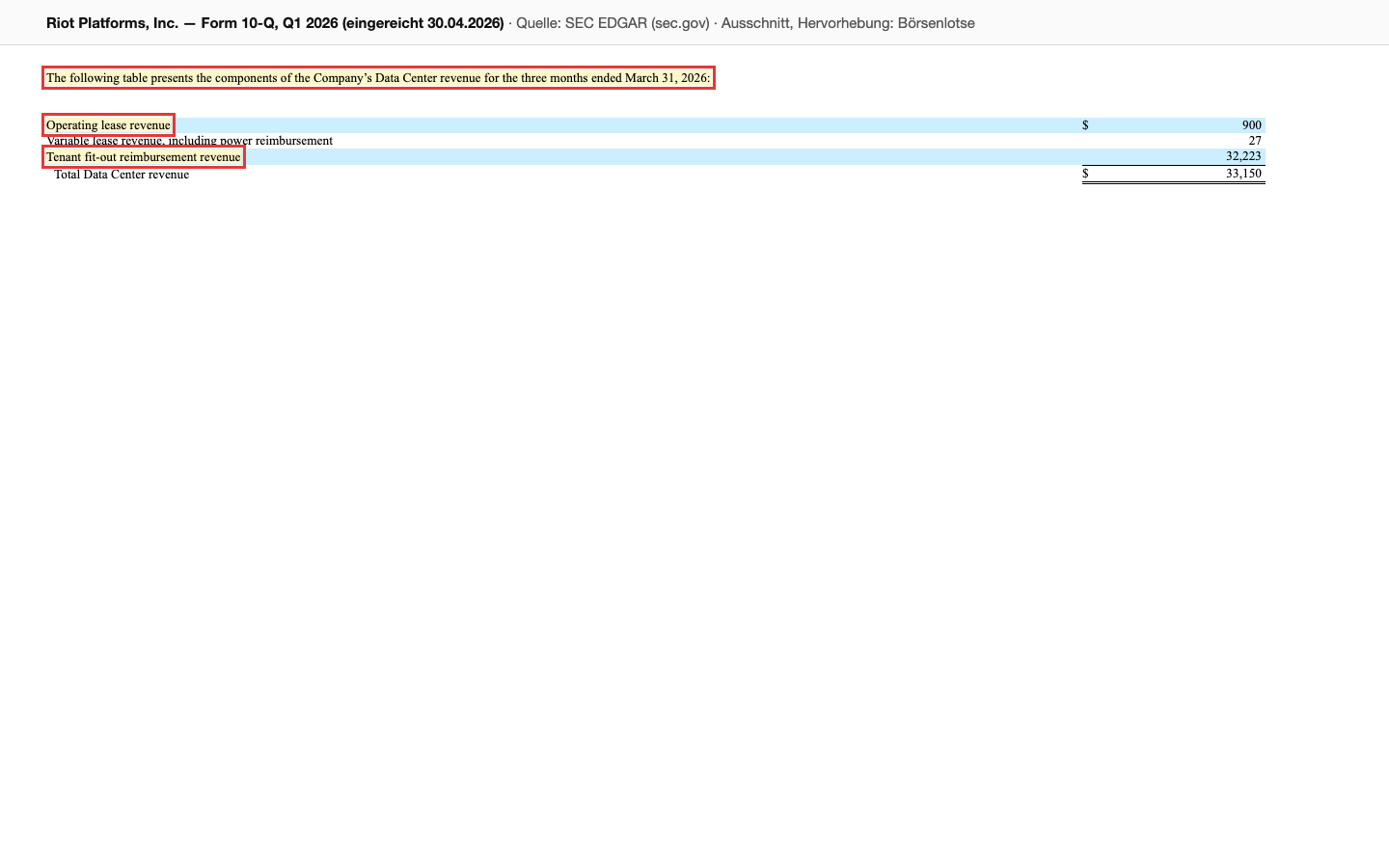

The headline of the first quarter of 2026 read: 33.2 million dollars in data center revenue — out of nowhere. Sounds like the AI business had already taken off. Now let's turn the package around. In Note 3 of the quarterly report, Riot breaks down that $33.2 million: $32.2 million is "tenant fit-out reimbursement revenue" — AMD reimburses Riot for the cost of building out the leased space ($30.7 million spent, plus a markup). Real rent payments ("operating lease revenue"): $0.9 million. On top of that, $27,000 in pass-through electricity costs.

This isn't fraud or an accounting trick — the reimbursement is contractually agreed, and having a tenant pay for its own build-out is standard in the industry. But it's pass-through revenue: costs in, costs plus a markup out, once. The report itself puts a number on the recurring substance behind it: the contractually committed minimum lease payments from the AMD lease add up to about $310 million — spread over more than a decade, or roughly $28 million a year in the first full years. For context, that's less than what Riot's Bitcoin mining generated in an average month of 2025. The 200-megawatt fantasy could turn that into considerably more — but as things stand today, the AI label is carrying a single-tenant lease with build-out rent. We dissected what real, recurring AI revenue looks like in our Credo Technology analysis — the contrast is worth reading.

Uncomfortable truth no. 2: a mined bitcoin costs more than it's worth

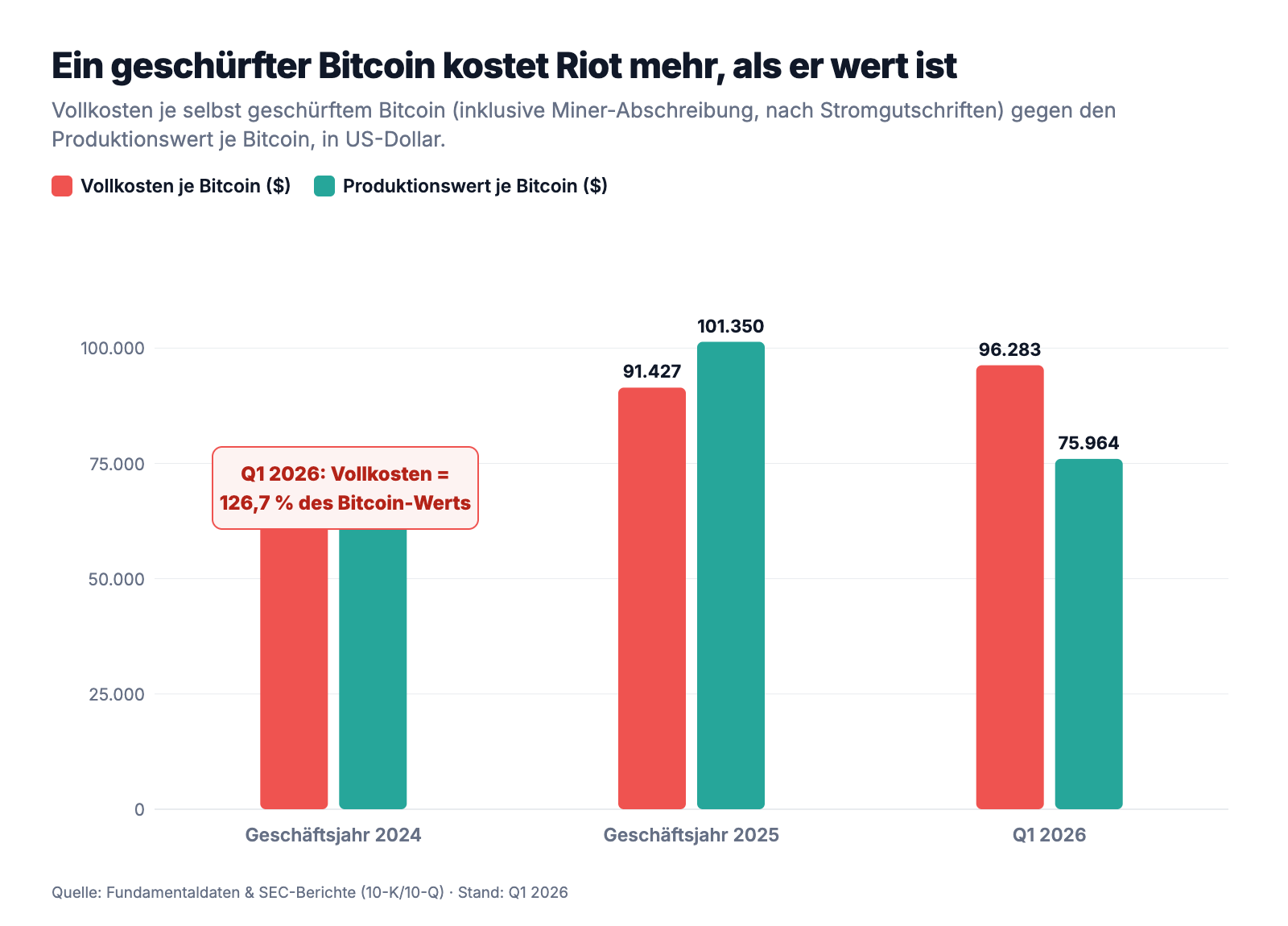

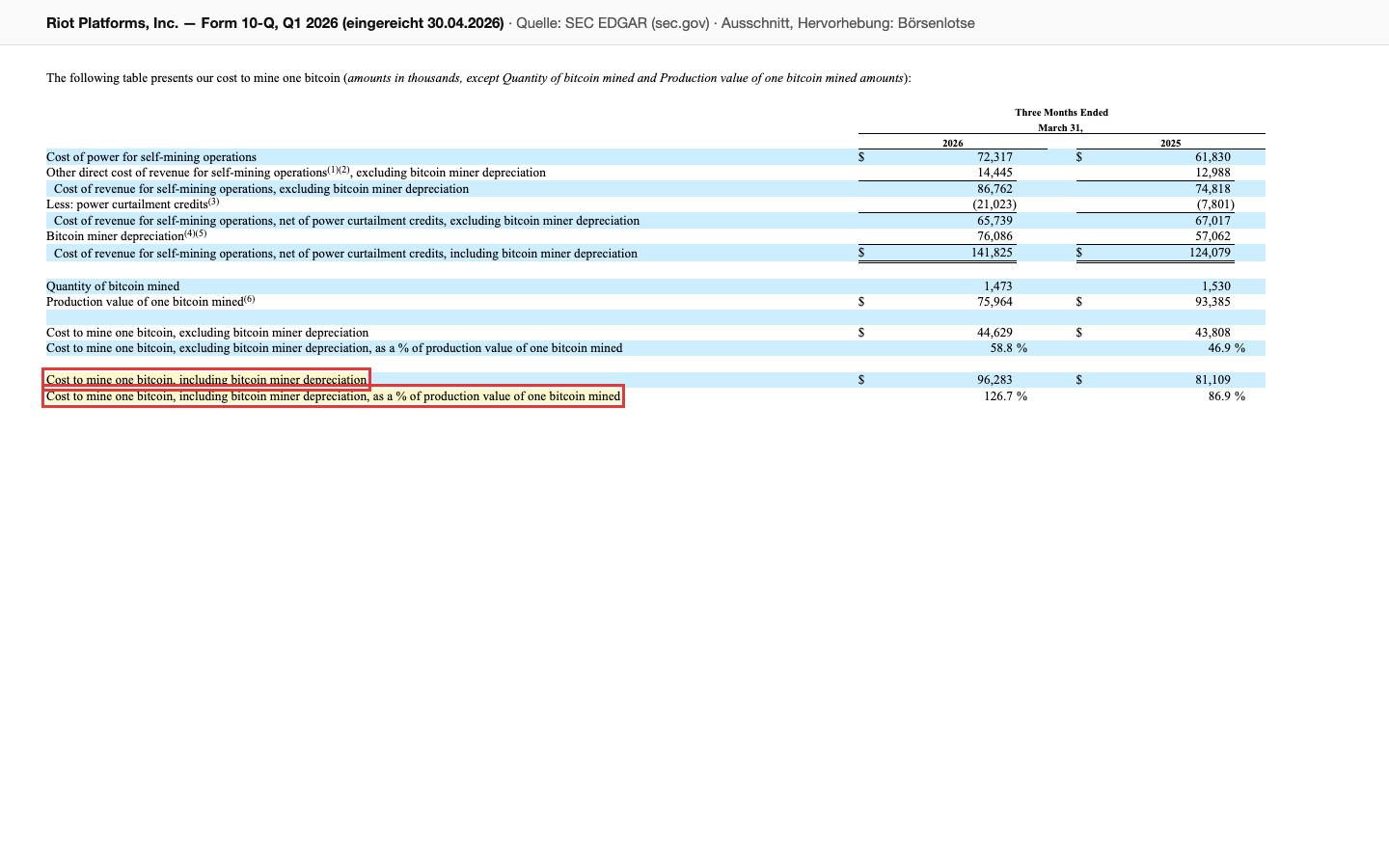

Now to the core business, which still accounts for a good two-thirds of revenue. Bitcoin mining has a built-in harshness: every four years the network halves the reward ("the halving," most recently in April 2024), and the more hashing power comes online worldwide, the smaller everyone's individual slice gets. Riot itself discloses a remarkably honest metric because of it: the full cost per self-mined bitcoin. In the first quarter of 2026 that figure, including miner depreciation, was $96,283 — against a production value of $75,964 per bitcoin. That's 126.7 percent. On a fully loaded basis, every bitcoin Riot mined destroyed roughly a quarter of its own value.

In fairness: without the (non-cash) depreciation of the miners, a bitcoin cost only $44,629, and Riot is clever about trimming its power bill — in the first quarter of 2026 the company collected $21.0 million in credits by powering down its machines during peak demand and selling electricity back to the Texas grid. But miners simply wear out after about three years and have to be replaced; the depreciation isn't accounting sleight-of-hand, it's reality on a delay. The trend in the original 10-Q:

There's also a concentration risk hardly anyone has on their radar: about 89 percent of total 2025 group revenue flowed through a single Bitcoin mining pool — the service provider that pools Riot's hashing power and pays out the rewards. Riot can switch pools at any time, the report emphasizes. Still: one business, two dependencies — one pool in the old business, one tenant in the new one.

Uncomfortable truth no. 3: Riot sells its bitcoin treasury to pay for operations

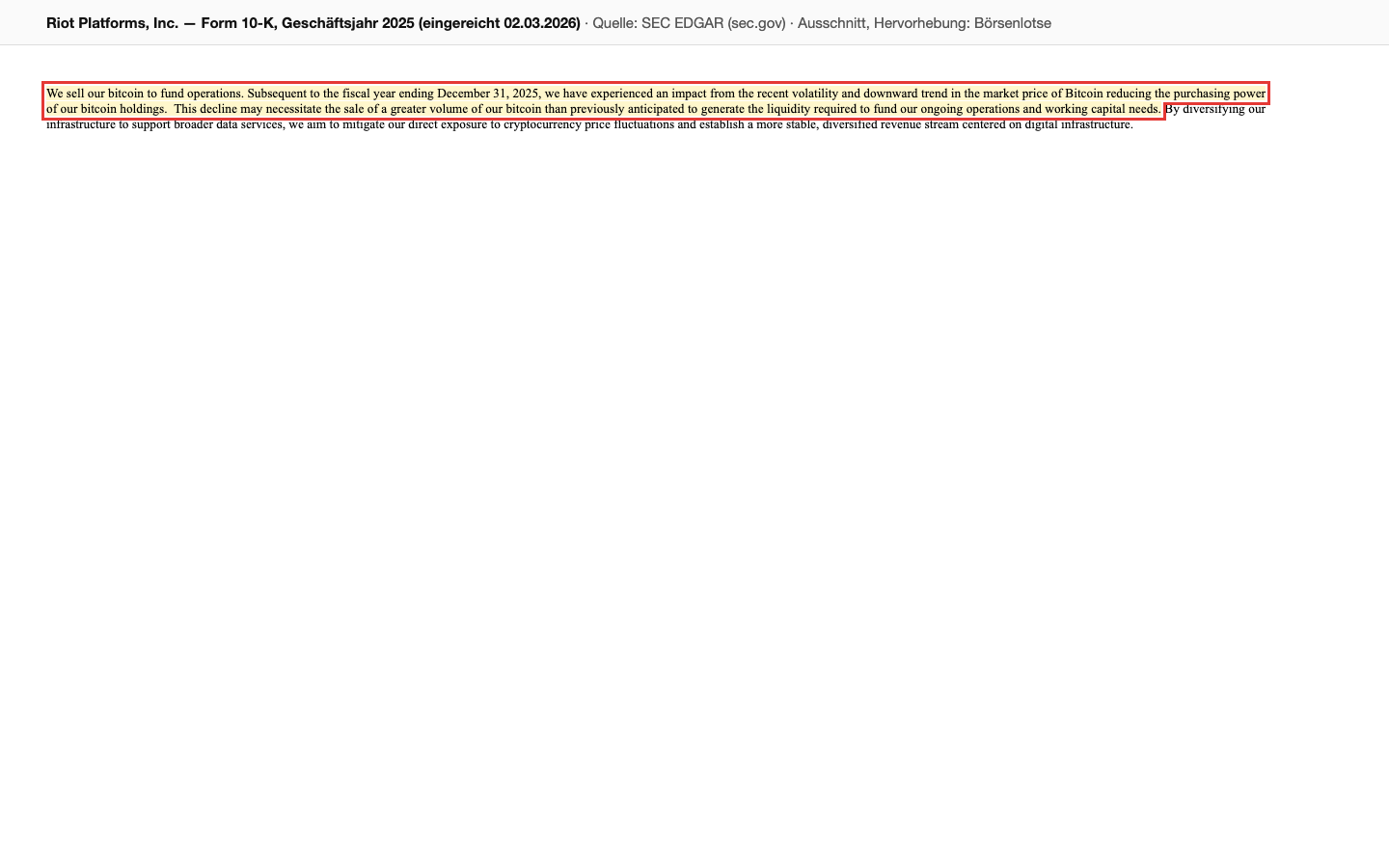

Riot's largest asset is its bitcoin holdings. And here the annual report (10-K) contains a sentence worth reading twice:

"We sell our bitcoin to fund operations. Subsequent to the fiscal year ending December 31, 2025, we have experienced an impact from the recent volatility and downward trend in the market price of Bitcoin reducing the purchasing power of our bitcoin holdings. This decline may necessitate the sale of a greater volume of our bitcoin than previously anticipated to generate the liquidity required to fund our ongoing operations and working capital needs."

— Riot Platforms, Inc., SEC annual report 10-K, fiscal year 2025, Item 7 (MD&A)

That's exactly what happened: between December 31, 2025 and March 31, 2026, the treasury shrank from 18,005 to 15,679 bitcoin — Riot mined 1,473 new ones and sold for $289.5 million. The remaining hoard was still worth $1.1 billion at quarter-end (down from $1.6 billion three months earlier — a mix of the falling price and the sales). Notice the unpleasant mechanics behind that: the deeper bitcoin falls, the more bitcoin Riot has to sell to pay the same bills — it's hard to get more procyclical than that. And part of the treasure isn't even freely available: 5,802 bitcoin were pledged as collateral for a $200 million loan from Coinbase as of March 31, 2026, which at times carried an 8.3 percent interest rate (fixed at 6.15 percent in April 2026, with collateral reduced to 4,258 bitcoin). A curious footnote: Coinbase is, at the same time, one of the two custodians holding Riot's bitcoin — lender and vault-keeper under one roof.

Uncomfortable truth no. 4: so far, shareholders have footed the bill — with 64 percent more shares

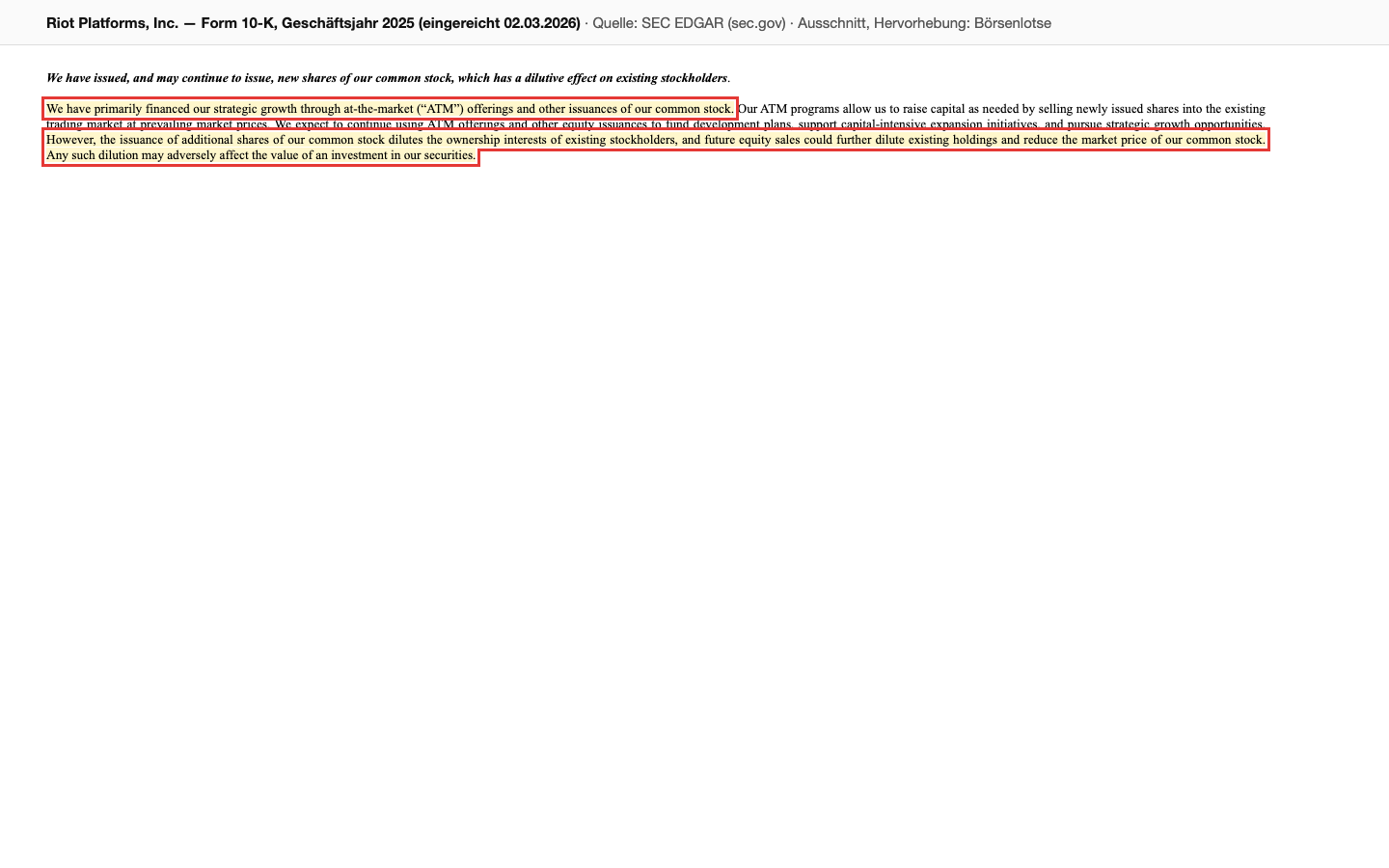

Where does the money for miners, facilities, and now the data center build-out come from, when the operating business is posting losses? The answer sits in the 10-K under risk factors, refreshingly blunt:

"We have primarily financed our strategic growth through at-the-market ('ATM') offerings and other issuances of our common stock. […] However, the issuance of additional shares of our common stock dilutes the ownership interests of existing stockholders, and future equity sales could further dilute existing holdings and reduce the market price of our common stock."

— Riot Platforms, Inc., SEC annual report 10-K, fiscal year 2025, Item 1A "Risk Factors"

Dilution means: your slice of the pie gets smaller every time new slices keep getting cut. At Riot it went like this: 230.8 million shares at the end of 2023, 344.9 million at the end of 2024, 371.6 million at the end of 2025, about 379 million in March 2026 — up 64 percent in a bit over two years. Growth paid for with fresh shares is never entirely free. To Riot's credit: in the first quarter of 2026 the company sold no new shares for once — the $500 million ATM program launched in December 2025 still sat untouched at quarter-end. That's the loaded chamber. On top of that came $125.7 million in stock-based compensation in 2025 alone — nearly a fifth of annual revenue went out as an equity bonus to staff and management, while the same filings record 7 insider sales and not a single purchase. By contrast, debt remains moderate at about $854 million in face value (including a $594 million convertible note carrying a 0.75 percent coupon through 2030) — the pivot wasn't financed through the bank, but through your brokerage account.

Uncomfortable truth no. 5: the pivot itself has already cost money — and its success is uncertain

The pivot to data centers isn't a free sticker. First, quite concretely: because Riot decided to build out Corsicana for data centers instead of mining, already-ordered build-out components became worthless — a $29.7 million write-off in fiscal year 2025, according to the 10-K. Second, structurally: Riot is now competing against established data center giants with decades of operating experience and cheaper financing. The report says as much with disarming clarity:

"However, this initiative is in its early stages, and the success of our data center strategy is uncertain and may not develop as anticipated."

— Riot Platforms, Inc., SEC annual report 10-K, fiscal year 2025, Item 1A "Risk Factors" ("Our data center business strategy may not perform as planned")

Add to that the customer concentration of the new world: AMD is so far the only data center tenant and, per the 10-Q, already accounted for more than 10 percent of group revenue in the first quarter of 2026. If things go well, AMD fills the 200 megawatts and further tenants follow at Corsicana. If things go badly, Riot has built out billions of dollars of capacity whose anchor tenant can walk away from its expansion options at any time. Neither outcome shows up in the numbers yet — which is exactly why valuation is the real question of price.

Valuation — what the market is actually paying for here

At mid-year 2026, the market values Riot at a price-to-sales ratio of about 16 — with roughly 379 million shares outstanding, that works out to a market capitalization in the neighborhood of a good $10 billion (data as of July 8, 2026), against trailing-twelve-month revenue of about $653 million. Mentally subtract the bitcoin treasury ($1.1 billion as of March 31, 2026) and you're still left with a good thirteen times revenue for a business that's posting losses on a fully loaded basis. The price-to-book ratio sits around 4.4 — equity stood at just under $2.4 billion as of March 31, 2026 and shrank by almost half a billion in the first quarter alone.

A word on "the professionals' view": 16 analysts cover the stock, and the consensus sits near "Strong Buy" — Wall Street loves the data center story. Those same professionals, however, expect further losses per share for the current and the coming fiscal year; only after that do the estimates show a small profit. And one last anchor against herd instinct: despite roughly 196 percent in price gains over twelve months, the stock was still down about 19 percent on a five-year view as of July 8, 2026. Anyone who bought during the last big hype of 2021 is still waiting to break even. Momentum is a direction, not a value — the same lesson we already drew with the AI power landlord Solaris Energy, whose valuation likewise prices in a future that hasn't arrived yet.

Opportunities and risks at a glance

What speaks for Riot:

- A real, scarce resource: more than 1.2 gigawatts of developed power capacity in Texas and Kentucky, with the Rockdale site and its 700-megawatt grid connection owned outright since January 2026 — exactly what AI data centers wait years for.

- The AMD lease is a real vote of confidence: a ten-year term, expanded from 25 to 50 megawatts, options up to 200 megawatts — and a "Data Center" segment that already delivered a contribution margin in the first quarter; the engineering division (revenue up 68 percent in 2025) benefits twice over from the data center boom.

- Real substance on the balance sheet: 15,679 bitcoin ($1.1 billion as of 03/31/2026), just under $2.4 billion in equity, moderate debt with a cheap convertible note (0.75 percent through 2030) — plus clever power arbitrage ($56.7 million in credits in 2025).

- Momentum and institutional tailwind: 15 scanner hits, relative strength of 88, 14 quarters of institutional buying against 2 quarters of selling (data as of July 8, 2026); if bitcoin rises, the holdings and fair-value accounting lever earnings upward.

What speaks against it:

- The story is running ahead of the numbers: $33.2 million in data center revenue in the first quarter of 2026 consists of 97 percent cost reimbursement; the agreed minimum lease payments of about $310 million are spread over more than ten years — against a market value of a good $10 billion.

- The core business mines below full cost: $96,283 per bitcoin against a $75,964 production value (126.7 percent, Q1 2026); the halving and record network hashrate press structurally on the margin.

- Procyclical financing: bitcoin sales pay for operations (holdings fell from 18,005 to 15,679 BTC in one quarter), and the lower the price, the more has to be sold; $663.2 million in net losses for 2025 plus $500.5 million in the first quarter of 2026.

- Dilution as a business principle (shares up 64 percent since the end of 2023, a new $500 million ATM program ready to go, $125.7 million in stock-based compensation in 2025), 7 insider sales against 0 purchases, plus concentration risks: one mining pool for about 89 percent of revenue, a single data center tenant.

A human conclusion

Back to the supermarket. The sticker on Riot's package isn't a lie: there is an AMD lease, there is a new segment, there is more than a gigawatt of real power — and a company that has already successfully reinvented itself once before, when the biotech company of pre-2017 became a Bitcoin miner. If Riot turns 50 leased megawatts into 200 and fills up Corsicana, a second, plannable leg of the business grows here that would take the gamble out of the stock. That's the front of the package, and it's better than at many other AI relabeling stories.

But you've now also read the ingredient list: $0.9 million in real rent behind $33 million in headline revenue. A core business that, fully loaded, produces a loss on every bitcoin it mines. A treasury that gets sold off to pay the bills — fastest of all, of course, exactly when bitcoin is falling. And a shareholder base that has paid for the pivot with 64 percent more shares, while the herd stares at the label. The herd instinct from the opening now gets its answer: the herd reads front labels. You can now read back labels. What you make of it is your decision. And that is exactly as it should be.

Sources

- Riot Platforms, Inc. — SEC annual report 10-K, fiscal year 2025 (filed March 2, 2026)

- Riot Platforms, Inc. — SEC quarterly report 10-Q, Q1 2026 (as of March 31, 2026; filed April 30, 2026)

- Riot Platforms, Inc. — SEC annual report 10-K, fiscal year 2024 (filed February 28, 2025)

- Riot Platforms, Inc. — SEC quarterly report 10-Q, Q3 2025 (filed October 30, 2025)

- Fundamental data (metrics, valuation, analyst consensus, quarterly series); in-house stock scanner, data as of July 8, 2026.

Disclaimer: This analysis is journalistic and not investment advice. It is not a recommendation to buy or sell, nor a solicitation to buy or sell securities. Stocks and cryptocurrencies are subject to significant price swings; a total loss is possible. Make your investment decisions on your own responsibility, and when in doubt, seek independent advice.

Our Bottom Line at a Glance

- Business model & pivot neutral

- An industrial Bitcoin miner with more than 1.2 gigawatts of developed power capacity that's pivoting into a data center landlord — its third transformation after biotech (through 2017) and blockchain. The power bottleneck in the AI industry is a genuine tailwind, but per its own risk factor the data center strategy is "in its early stages" and its success is uncertain.

- Data center launch & AMD positive

- The AMD lease (January 2026) is a genuine vote of confidence: a ten-year term, expanded from 25 to 50 megawatts in April 2026, options up to 200 megawatts. But: of $33.2 million in segment revenue in the first quarter of 2026, $32.2 million was build-out cost reimbursement and only $0.9 million was rent; agreed minimum lease payments are about $310 million over more than ten years.

- Mining economics & profitability negative

- On a fully loaded basis, a self-mined bitcoin cost $96,283 in the first quarter of 2026, against a $75,964 production value (126.7 percent). Net loss of $663.2 million in 2025 plus $500.5 million in the first quarter of 2026; fair-value accounting for the bitcoin treasury turns results into a plaything of the bitcoin price.

- Balance sheet & bitcoin treasury neutral

- 15,679 bitcoin ($1.1 billion as of 03/31/2026), just under $2.4 billion in equity and moderate debt ($854 million face value, of which $594 million is a 0.75 percent convertible note). But the treasury is shrinking: bitcoin sales fund operations — the lower the price, the more has to be sold; at times 5,802 BTC were pledged as loan collateral.

- Dilution & insiders negative

- Share count from 230.8 to about 379 million since the end of 2023 (+64 percent); per the annual report (10-K), growth is financed primarily through ATM share programs, and a new $500 million program stands ready. Stock-based compensation of $125.7 million in 2025; the scanner shows 7 insider sales against 0 purchases (data as of July 8, 2026).

- Valuation & momentum negative

- Price-to-sales ratio around 16, market value a good $10 billion (order of magnitude, July 8, 2026) against $653 million in trailing-twelve-month revenue and ongoing losses. 15 momentum-scanner hits and an analyst consensus near "Strong Buy" stand against roughly minus 19 percent on a five-year view — the market is paying for the 200-megawatt future, and 50 has been delivered so far.

Riot Platforms wears the stock market's most coveted label right now — AI data center — and unlike with some other relabeling stories, there's something behind it: the AMD lease, more than a gigawatt of its own power, a new reporting segment. But the ingredient list shows a Bitcoin miner that mines below full cost, sells its bitcoin treasury to fund operations, and has paid for its pivot with 64 percent more shares. The market is already valuing the finished future at a good $10 billion. Not investment advice.

What Our Rating Means

- If you don't own the stock

- As long as the question raised in the bottom line stays open, we see no basis for an entry.

- If you hold it in your portfolio

- Our findings offer no acute reason to sell — the checkpoints named remain decisive.

A journalistic assessment by our editorial team at the time of the deep dive, based on public sources — not investment advice and not a solicitation to buy or sell. Your personal circumstances (investment goals, risk capacity, taxes) cannot be taken into account. What our categories mean, how verdicts are formed, and what conflicts of interest exist →

Worth Noting

- One-off items in 2025 earnings: a $158.1 million loss from the Rhodium settlement (a legacy item from the discontinued hosting business), $20 million from another settlement, and a $29.7 million write-off on Corsicana build-out components resulting from the data center pivot.

- The five-year performance of about −19 percent and the relative strength figure come from our in-house scanner (data as of July 8, 2026); the database field "distance to all-time high" (−99 percent) is a data artifact and was not used.

- The $200 million Coinbase loan was extended to April 2027 in April 2026 and switched to a fixed 6.15 percent rate; the bitcoin collateral fell from 5,802 to 4,258 BTC. Part of the interest is capitalized into the data center build-out ($4.7 million in the first quarter of 2026).

Frequently Asked Questions

Riot Platforms is one of the largest industrial Bitcoin miners in North America, with sites in Texas (Rockdale, Corsicana) and Kentucky — together more than 1.2 gigawatts of developed power capacity. In 2025, Riot mined 5,686 bitcoin. On top of that comes an engineering division for power-distribution equipment and, since 2026, a third segment: leasing data center capacity, initially to chipmaker AMD.

In the first quarter of 2026, Riot reported $33.2 million in data center revenue from the AMD lease. But per the quarterly report (10-Q), $32.2 million of that was cost reimbursement for the tenant build-out (AMD pays back Riot's build-out costs plus a markup), and only $0.9 million was real rent. The agreed minimum lease payments of about $310 million are spread over more than ten years.

As of March 31, 2026, Riot held 15,679 bitcoin worth about $1.1 billion — three months earlier it was still 18,005. Per the annual report (10-K), Riot sells bitcoin to fund its operations ($289.5 million in proceeds in the first quarter of 2026 alone); 5,802 bitcoin were at times pledged as loan collateral to Coinbase.

No. Fiscal year 2025 posted a net loss of $663.2 million, and the first quarter of 2026 added another $500.5 million. Because the bitcoin treasury is marked to market, results swing wildly with the bitcoin price — between plus $219 million and minus $691 million per quarter within a span of six quarters.

In the first quarter of 2026, a self-mined bitcoin cost Riot $96,283, including miner depreciation — against a production value of $75,964, or 126.7 percent. Without depreciation it was $44,629. After the 2024 halving and the rising network hashrate, the full cost has climbed from $64,421 to over $96,000 within two years.

Yes, significantly. The share count rose from 230.8 million at the end of 2023 to about 379 million in March 2026 — up 64 percent. Per the 10-K, Riot finances its growth primarily through at-the-market share programs; a new $500 million program has stood ready since December 2025. On top of that came about $125.7 million in stock-based compensation in 2025.

Found an error?

Did you spot a factual error, an outdated number, or a typo in this deep dive? Let us know briefly — your report goes straight to the editorial team.