Broadwind Stock: $943,000 in Cash — and the Wind-Tower Maker Steps Out of the Wind Business

Broadwind sounds like a wind-power comeback: steel towers for wind turbines, a price-to-sales ratio around 0.6, strong price momentum. We read the annual report and the quarterly report at the SEC — and found a completely different story: $943,000 in cash as of March 31, 2026, a Wells Fargo credit line whose covenants have been loosened twice, a legislated end to subsidies, and the sale of both tower plants. Not investment advice — just the story the price tag doesn't tell.

There's a reflex that costs more in investing than any brokerage fee: buying the label instead of what's in the box. "Broadwind" — the name sounds like wind power, like the energy transition, like the big story that surely has to arrive sooner or later. Add a price-to-sales ratio around 0.6, a stock that has climbed noticeably over the past year, and a voice in your head starts whispering: "A forgotten wind-power stock, right before the sector turns." For exactly that reflex, let's make a deal: before you touch a single share of Broadwind (NASDAQ: BWEN), let's read together what's in the reports Broadwind filed with the U.S. securities regulator, the SEC — the annual report for 2025 and the quarterly report as of March 31, 2026. A filing to the SEC is honest under penalty of law. And at Broadwind it says something that has little to do with the label: $943,000 in cash, a bank credit line as the lifeline — and the farewell to wind-tower manufacturing. In the end, you decide for yourself.

What Broadwind actually does

Broadwind is a classic industrial manufacturer out of Cicero, Illinois — 341 employees at year-end 2025, welding robots instead of software. The company grew out of a shell incorporated in Nevada in 1996, became "Broadwind Energy" in 2008, and built itself three legs through acquisitions: Heavy Fabrications — where the huge steel-tube segments that make up wind-turbine towers get welded (picture steel tubes as tall as a church steeple and as heavy as a freight-rail car); Gearing — precision gears and gearboxes for oil and gas companies, mining and power generation; and Industrial Solutions — assemblies, wiring and installation kits, mainly for gas-turbine power plants. In 2020 the company dropped "Energy" from its name — even then a sign it wanted to shed the wind label. How serious that was is showing up right now: in September 2025 Broadwind sold its Manitowoc (Wisconsin) plant, and on April 30, 2026 also the Abilene (Texas) tower plant — and starting in the second quarter of 2026 it officially reports the wind business as a "discontinued operation". The wind-tower builder Broadwind became known as is ceasing to be one. Why, the filings explain remarkably openly — more on that shortly.

Where the stock shows up in our scanner

Every day we run about 3,500 stocks through our scanners. Broadwind lights up in three scanners (data as of July 8, 2026) — and this combination is a lesson in ambivalence. First, in the Insolvency Radar "Cash Running Out": the scanner divides cash on hand by the average operating cash outflow of the last four reporting quarters. For Broadwind, $0.9 million in cash as of March 31, 2026 stood against a cumulative operating cash flow of −$4.4 million over the last four reporting quarters — arithmetically about $1.1 million of outflow per quarter, or a runway of roughly 0.8 quarters. That's the smallest cash balance of all ten companies in our round-up article on the Insolvency Radar. Important before your pulse spikes: the radar is a smoke detector, not an insolvency verdict — it measures a single balance-sheet date and sees neither credit lines nor sale proceeds that arrive after that date. Broadwind has exactly these two escape routes, and we'll look at them in detail below.

Second, Broadwind shows up in the P/S ranking — the list of the cheapest stocks in our universe measured against revenue: a price-to-sales ratio around 0.63 (data as of July 6, 2026) means you pay just 63 cents for every dollar of annual revenue. And third, the stock sits on the Beneish M-Score watch list: the statistical early-warning model for possible earnings cosmetics shows −1.31 — above the warning threshold of −1.78. That's not an accusation of manipulation; at Broadwind it's mainly the one-off gain from the plant sale and the swings in working capital that trigger it. But it fits the finding that the reported 2025 profit didn't come from ongoing operations. Two more metrics round out the twilight picture: the Altman Z-Score sits at −2.45 (values below 1.8 count as distressed — negative values are rare), while the relative-strength rating stands at 95 and the earnings-trend rating at 97: the stock has recently outrun 95 percent of the market. So the market sees a turnaround story. The balance sheet sees a patient. Remember this tension — it's the thread running through this analysis.

The numbers over the years — first the good news

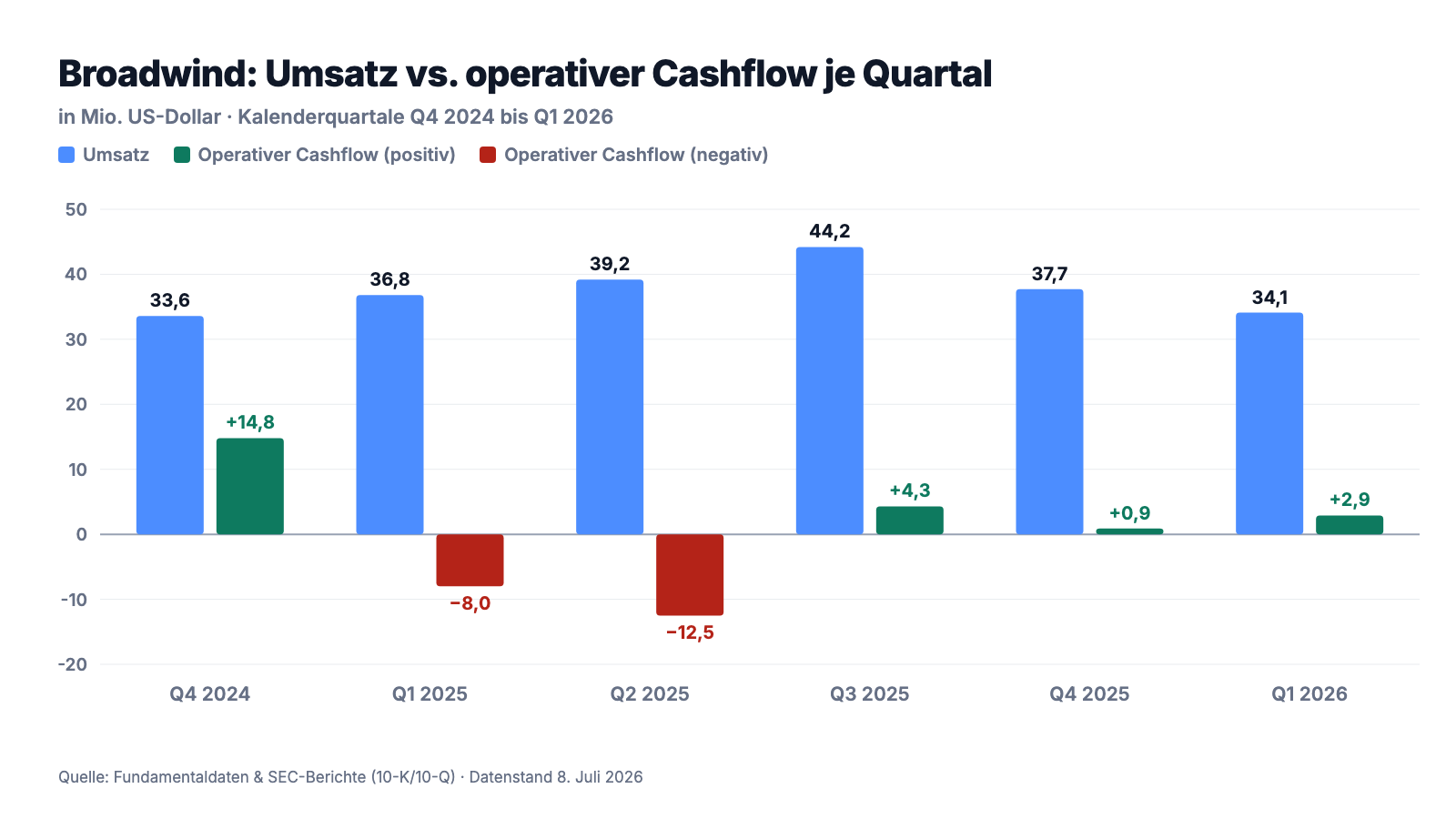

Honesty first, so here's what genuinely went well in 2025: Broadwind booked $131.4 million in new orders, 22 percent more than in 2024. The Industrial Solutions segment — assemblies for gas-turbine power plants that benefit from data centers' appetite for electricity — grew its order intake by 79 percent, the gearing business by 52 percent. Revenue rose 10 percent in 2025 to $158.1 million, and in the first quarter of 2026 the ratio of new orders to revenue (book-to-bill) stood at 1.1 — more is coming in than is being worked off. The order backlog stood at $99.1 million at the end of March 2026. That truth cuts both ways, though: a year earlier it was still $117.0 million, and at the end of 2025 the backlog of $96 million sat 24 percent below the prior-year figure — the order pile here swells and shrinks in waves, depending on when large customers place orders.

And now the side the label doesn't show — the quarterly view of revenue and cash:

What you're looking at is a business that breathes with revenue but lives on customer deposits: at the end of 2024, +$14.8 million still flowed in operationally — mainly because customers made advance payments for the large tower order announced in 2023. That reversed in 2025: once the deposits had been worked through, $15.4 million flowed out operationally for the full year — the same year in which the income statement showed 5.2 million dollars of net income. The small inflows since then (Q3 2025 through Q1 2026 add up to about $8 million) weren't enough to refill the till: $943,000 as of March 31, 2026. For comparison: that's less than the business moves in payroll and materials in an average month. An industrial company with $150 million in revenue and a six-figure cash balance — that only works if somebody else is absorbing the swings. That somebody is the bank.

What the filings say — the uncomfortable truths

Uncomfortable truth no. 1: $943,000 in cash — Broadwind is living on the credit line

The quarterly report describes the situation itself, soberly and completely:

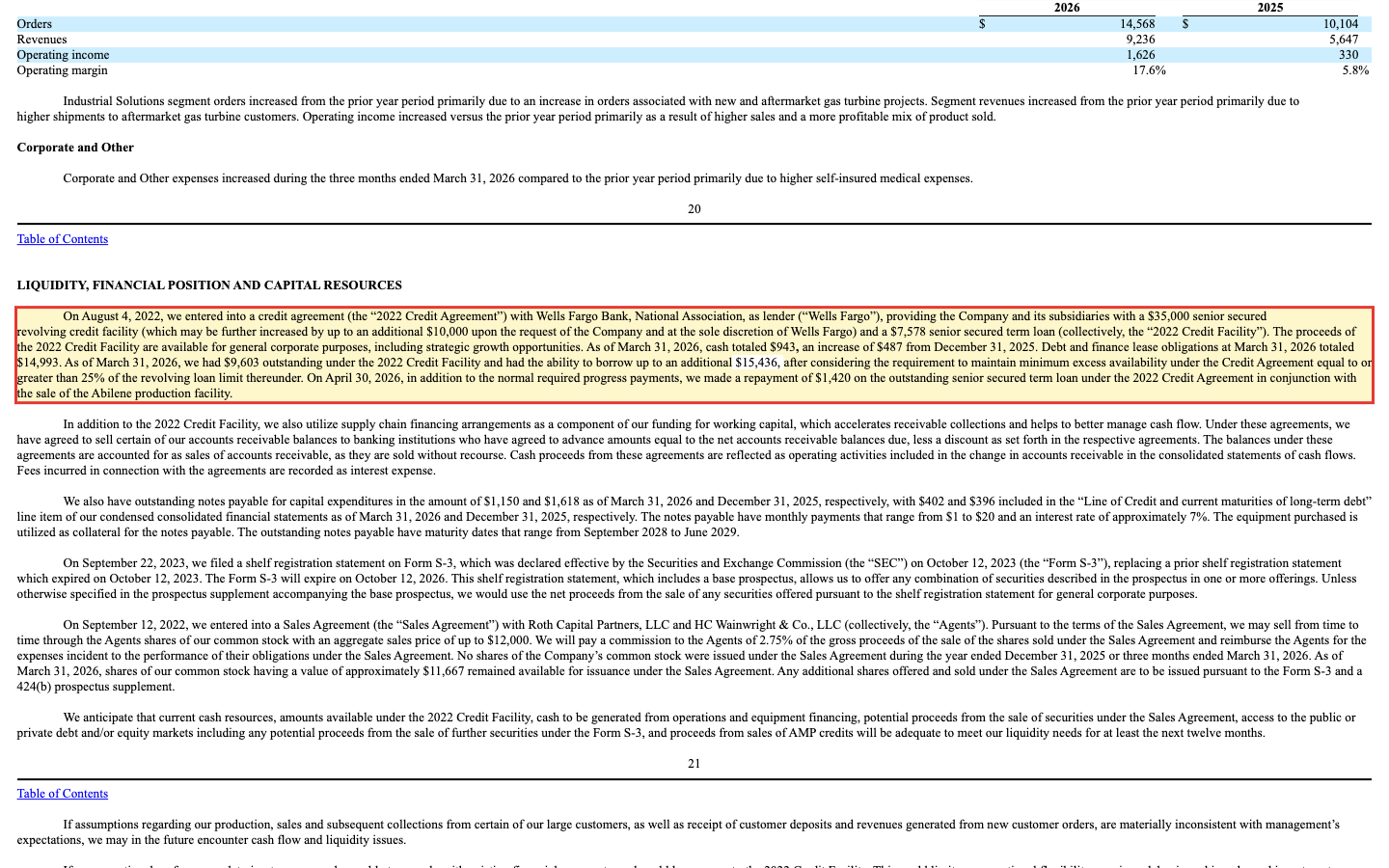

"As of March 31, 2026, cash totaled $943, an increase of $487 from December 31, 2025. Debt and finance lease obligations at March 31, 2026 totaled $14,993. As of March 31, 2026, we had $9,603 outstanding under the 2022 Credit Facility and had the ability to borrow up to an additional $15,436, after considering the requirement to maintain minimum excess availability under the Credit Agreement equal to or greater than 25% of the revolving loan limit thereunder."

— Broadwind, Inc., SEC quarterly report (10-Q) as of March 31, 2026, Item 2 "Liquidity, Financial Position and Capital Resources"

In plain English: Broadwind has a checking account that's nearly empty and an overdraft line at Wells Fargo — up to $35 million revolving, plus a term loan. Of that overdraft line, $9.6 million was drawn at the reporting date, with $15.4 million still free. That's the one escape route, and it's real. But there are three details you should know. First: the credit line expires on August 4, 2027 — within the next year and a half after the reporting date, Broadwind has to extend it or refinance. Second: the bank has already had to loosen the terms twice. In December 2024 the so-called fixed charge coverage ratio — simplified, how many times operating profit covers the interest and principal payments coming due — was lowered from 1.1 to 1.0; in February 2026 it was lowered again, to 0.75 for all of 2026, and in exchange Broadwind has had to leave a quarter of the credit line untapped ever since. A bank that lowers its own bar twice believes in the customer — but it doesn't do that out of generosity, it does it because the original bar would have been missed. Third, the same report carries the sentence for the worst case: if the business deteriorates, Broadwind could breach the covenants "and could lose access to the 2022 Credit Facility". Management expressly expects the funds to be sufficient for at least the next twelve months — the other funding sources named include an at-the-market equity program of up to $12 million (with $11.7 million still unused as of March 31, 2026 — though fresh shares dilute your stake: your slice of the pie gets smaller when new slices get cut) and the sale of tax credits. Which brings us to the government.

Uncomfortable truth no. 2: the government is shutting off the subsidy tap — and it recently propped up the entire result

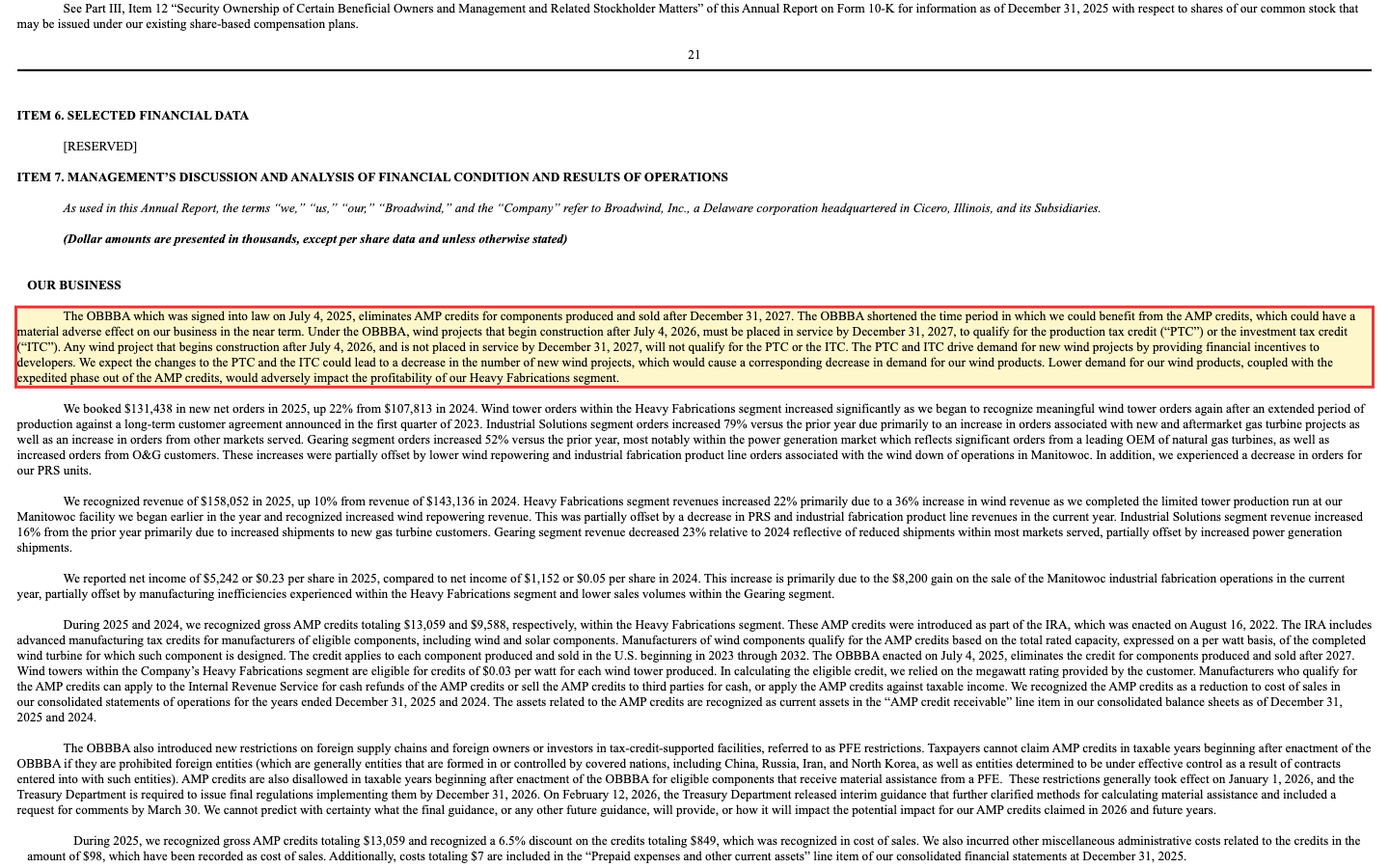

Wind power in the United States is a subsidy business — that's not the competition saying it, that's Broadwind itself. Two support programs carry the tower business: the tax credits for wind-farm operators (PTC/ITC), which drive demand for new wind farms, and the AMP production credits — 3 cents per watt for every tower made in the U.S., which the manufacturer collects directly or can sell. In 2025 Broadwind booked $13.1 million from this (2024: $9.6 million) — as a reduction of manufacturing costs. For context: total net income in 2025 was $5.2 million. Without the government credits, the tower business would be deep in the red. And exactly this support structure was wiped out by law on July 4, 2025:

"The OBBBA which was signed into law on July 4, 2025, eliminates AMP credits for components produced and sold after December 31, 2027. […] Any wind project that begins construction after July 4, 2026, and is not placed in service by December 31, 2027, will not qualify for the PTC or the ITC. […] Lower demand for our wind products, coupled with the expedited phase out of the AMP credits, would adversely impact the profitability of our Heavy Fabrications segment."

— Broadwind, Inc., SEC annual report (10-K) for 2025, Item 7 (MD&A), "Our Business"

For the wind-power comeback the company name promises, that's poison: new U.S. wind projects lose their most important financing basis unless they're started by mid-2026 and completed by the end of 2027. The annual report notes drily that the restrictions have already had a negative effect on demand for future wind projects. So Broadwind didn't wait for better weather — it drew the consequence. Which brings us to the biggest surprise in this analysis.

Uncomfortable truth no. 3: the wind-tower builder sold both of its tower plants — the 2025 profit is a sale proceed

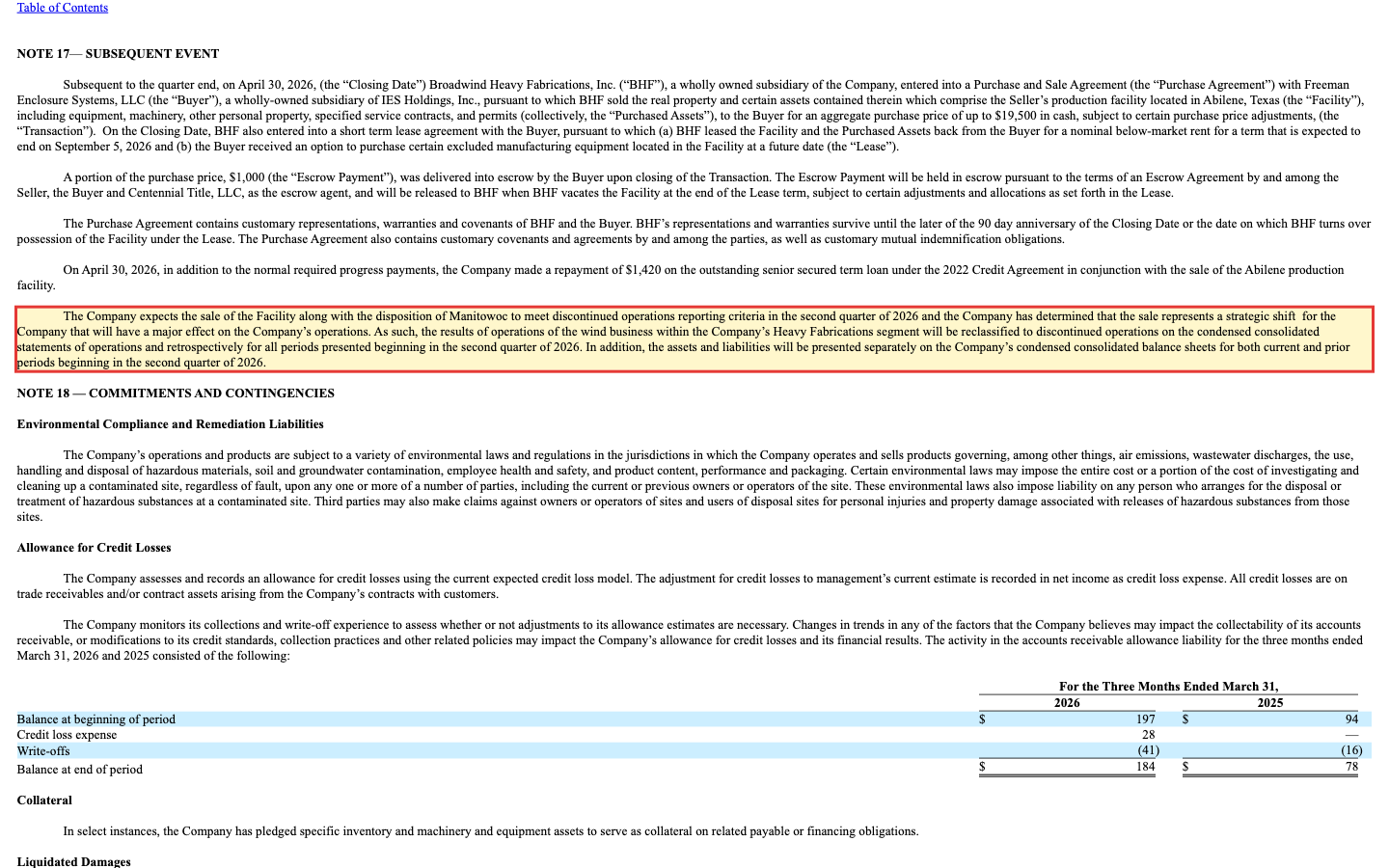

In September 2025 Broadwind first sold the industrial-manufacturing plant in Manitowoc for $13.5 million — that produced a gain on sale of $8.2 million. Hold that number next to the full-year 2025 net income of $5.2 million: without the plant sale, the bottom line would have been a loss. The optically tidy "profit year 2025" wasn't one operationally — the income statement was carried by a one-off gain while $15.4 million flowed out operationally. And on April 30, 2026, four weeks after the quarter-end reporting date, came the real bombshell: the sale of the Abilene tower plant for up to $19.5 million to a subsidiary of IES Holdings — including a leaseback expected to run through September 5, 2026 to complete ongoing orders. The quarterly report frames it this way:

"The Company expects the sale of the Facility along with the disposition of Manitowoc to meet discontinued operations reporting criteria in the second quarter of 2026 and the Company has determined that the sale represents a strategic shift for the Company that will have a major effect on the Company's operations. As such, the results of operations of the wind business within the Company's Heavy Fabrications segment will be reclassified to discontinued operations […]"

— Broadwind, Inc., SEC quarterly report 10-Q as of March 31, 2026, Note 17 "Subsequent Event"

"Discontinued operations" is balance-sheet language for: this business now belongs to the past — it gets reported separately in the income statement, like a room that's been closed off. The scope is enormous: wind power still accounted for 51 percent of Broadwind's revenue in 2025. So roughly half of the company you buy under the ticker BWEN is currently saying goodbye to the continuing-operations numbers. What remains are gearing and gas-turbine supply (Industrial Solutions) — businesses with recently fast-growing orders, but together only about half of prior revenue. For the cash position, the Abilene proceeds are the good news: up to $19.5 million (less a $1 million escrow holdback and adjustments) flowed in after the balance-sheet date — $1.42 million of it went straight into an accelerated paydown of the bank loan. So the smoke detector from March 31 should be noticeably quieter in the next report. The catch: you can only sell a plant once. After that, the remaining business has to earn the money itself.

Uncomfortable truth no. 4: five customers, 80 percent of revenue

Broadwind supplies giants — and hangs on them. The annual report quantifies the concentration risk precisely:

"Sales to GE Vernova represented greater than 10% of our consolidated revenues for the years ended December 31, 2025 and 2024. The loss of this customer could have a material adverse effect on our business, results of operation or financial condition."

— Broadwind, Inc., SEC annual report 10-K for 2025, Item 1 "Customers"

The full picture: the five largest customers accounted for 80 percent of revenue in 2025 (2020: 84 percent — diversification is happening, but at a snail's pace). The U.S. wind-turbine market itself is a duopoly — according to the industry data cited in the annual report, the two largest turbine makers most recently accounted for a combined 88 percent of the U.S. market. If your neighbor told you their business was doing well, but four out of every five dollars came from a handful of buyers, one of which alone accounted for more than ten percent — would you wince a little? Exactly. At least in the gas-turbine business, now the core, the customer sitting across the table is the leading turbine maker with a full order book. But the concentration risk remains — it just changes industries.

And AI? Only boilerplate paragraphs, no business

Because in 2026 almost every company puts "AI" in the window display, we check on every analysis what the SEC filings genuinely say about artificial intelligence. At Broadwind the finding is quickly told: in the annual report, AI appears exclusively in risk paragraphs. The company says it continues to evaluate the use of emerging technologies such as generative artificial intelligence, while warning that competitors with greater resources could adopt such technologies faster, and that it cannot predict the risks from implementing and using artificial intelligence. No AI product, no AI revenue, no AI strategy — standard caution clauses of the kind lawyers write into nearly every annual report today. For a steel-fabrication business, that's neither surprising nor damning. It just means: there's no AI story carrying this stock — the indirect connection runs through the gas-turbine customers, whose power plants also supply electricity to data centers.

Valuation: cheap by revenue, expensive by earnings

By mid-2026 Broadwind was valued at about $98 million (data as of July 6, 2026) — the smallest market value among the ten companies in our Insolvency Radar round-up. That produces two completely different price tags. Measured against revenue, the stock is cheap: price-to-sales ratio around 0.63, enterprise value to revenue around 0.86. Measured against earnings, it isn't: the reported P/E around 19 rests on the 2025 profit including the $8.2 million one-off sale gain; based on earnings estimates for the coming four quarters, the forward P/E sits around 43. The handful of analysts who cover the stock most recently saw a price target about 26 percent above the early-July-2026 price — with micro-caps and thin coverage, that's more a sentiment reading than a forecast. Then there's tradability: 23.4 million shares outstanding, 86 percent of them in public float, but daily swings of around 12 percent and a beta of 1.75 — the stock moves almost twice as violently as the market. The next big date is already set: the next quarterly report lands on August 11, 2026 — the first one to show the wind business as a discontinued operation and in which the Abilene proceeds become visible in the cash balance. That report will show what the "new Broadwind" without wind really looks like.

Opportunities and risks at a glance

What speaks for Broadwind:

- The restructuring is financed, not just hoped for: Manitowoc brought in $13.5 million (September 2025), Abilene up to $19.5 million (April 2026) — proceeds that pay down debt and refill the cash position after the March 31, 2026 reporting date.

- The remaining business is growing exactly where investment is happening: order intake up 79 percent at Industrial Solutions and 52 percent in gearing in 2025 — carried by the gas-turbine boom around electricity demand and data centers; book-to-bill of 1.1 in the first quarter of 2026.

- Very cheap measured against revenue: a price-to-sales ratio around 0.63, enterprise value to revenue around 0.86 (data as of July 6, 2026) — if the restructuring reaches decent margins, a lot of skepticism is already priced in.

- The market is already rewarding the strategic shift: relative strength of 95, earnings-trend rating of 97, an established uptrend (Stage 2) — the stock is among the strongest of 2026 in our universe (data as of July 8, 2026).

- Credit line with room to spare: $15.4 million additionally available (March 31, 2026), all covenants met at the reporting date, plus an unused equity program of $11.7 million as an extra cushion.

What speaks against it:

- Cash remains razor-thin: $943,000 as of March 31, 2026, −$4.4 million operationally over the last four reporting quarters, an Altman Z-Score of −2.45 — without the bank and the plant sales, the room to maneuver would be gone.

- Everything hangs on a credit line that expires on August 4, 2027 — and whose covenants the bank has had to loosen twice since late 2024 (fixed charge coverage ratio most recently from 1.1 to 0.75); the report itself warns of a possible loss of access if the business weakens.

- Half the company is disappearing from the numbers: 51 percent of 2025 revenue came from the wind business, which will be reported as a discontinued operation starting in the second quarter of 2026 — what remains still has to prove its profitability (operating margin recently around 1 percent, fundamental grade D in our scanner).

- Earnings quality is weak: 2025 net income only thanks to an $8.2 million one-off sale gain, operating cash flow of −$15.4 million, plus $13.1 million of government AMP credits that disappear after 2027; the Beneish M-Score (−1.31) sits above the warning threshold.

- Concentration risk and a thin market: five customers equal 80 percent of revenue, GE Vernova alone above 10 percent; a $98 million market value, daily swings around 12 percent, thin analyst coverage — disappointments hit without a cushion.

A human conclusion

Back to the label. Whoever buys "Broadwind" because the name sounds like a wind-power comeback is buying a company that no longer exists: the tower plants are sold, the subsidies are ending, the wind business is moving into the "discontinued" column. Whoever instead takes the stock for what's really in the box — a small, cash-strapped supplier to gas turbines and gearing in the middle of a restructuring, with growing orders, a nearly empty till, and a bank that has gone along so far —, can arrive at an honest judgment. The smoke detector from our Insolvency Radar has done its job: it beeped, we checked, and we found both — the real bottleneck at the reporting date and the real escape routes (the credit line, the Abilene proceeds, the order intake). Whether the restructuring turns into a profitable "new Broadwind" won't be decided by the company name, but by the next quarterly reports, starting on August 11, 2026 — the first one to show the company as it actually is now. Until then: never buy the label. Read the fine print. What you make of it is your decision. And that's exactly as it should be.

Sources

- Broadwind, Inc. — SEC annual report 10-K for fiscal year 2025 (filed March 11, 2026)

- Broadwind, Inc. — SEC quarterly report 10-Q as of March 31, 2026 (filed May 12, 2026)

- Broadwind, Inc. — SEC annual report 10-K for fiscal year 2024 (filed March 5, 2025)

- Fundamental data (metrics, valuation, analyst consensus; data as of July 6–8, 2026) and our in-house stock scanner (data as of July 8, 2026)

- Minnow Street — Insolvency Radar: Ten Companies Running Out of Money (methodology of the smoke-detector scanner)

Transparency & disclaimer: This analysis is a journalistic contextualization of publicly available information and is not investment advice, not a financial analysis in the regulatory sense, and not a solicitation to buy or sell securities. It expressly contains no judgment about whether an insolvency is imminent. Stock investments carry substantial risks up to total loss. All information without guarantee; the data cut-off is noted in the text in each case. The author holds no position in Broadwind stock at the time of publication.

Our Bottom Line at a Glance

- Order book positive

- $131.4 million in order intake in 2025 (+22 percent), Industrial Solutions +79 and gearing +52 percent, book-to-bill of 1.1 in the first quarter of 2026 — the remaining business is benefiting from the gas-turbine boom; order backlog of $99.1 million (March 31, 2026).

- Restructuring financing positive

- Manitowoc sale of $13.5 million (September 2025), Abilene sale of up to $19.5 million (April 30, 2026) plus $15.4 million of free credit line and an unused $11.7 million equity program — the exit from wind is paid for, not just decided.

- Valuation neutral

- A price-to-sales ratio around 0.63 and EV/revenue around 0.86 are cheap — but the P/E around 19 lives off the one-off gain, and the forward P/E sits around 43 (data as of July 6, 2026). Cheap by revenue, expensive by earnings: the price is a bet on a successful restructuring.

- Liquidity negative

- $943,000 in cash as of March 31, 2026, −$4.4 million operationally over four reporting quarters, an Altman Z of −2.45; the Wells Fargo credit line expires on August 4, 2027, and its covenants have been loosened twice since late 2024 (most recently to 0.75).

- Subsidy landscape negative

- The OBBBA law of July 4, 2025 eliminates the AMP credits after 2027 (2025: $13.1 million — more than double net income) and ends PTC/ITC for new wind projects — the foundation of the tower business has collapsed politically.

- Earnings quality negative

- 2025 net income ($5.2 million) only thanks to an $8.2 million one-off sale gain; operating cash flow of −$15.4 million; a Beneish M-Score of −1.31 above the warning threshold; a fundamental grade of D in our in-house scanner — the ongoing business isn't making money yet.

Broadwind is no longer a wind-power bet — it's a cash-strapped restructuring story: the tower plants are sold, the subsidies are running out, and whether gearing plus gas-turbine supply alone can carry a profit still has to be proven by the reports starting in August 2026. Until then, the thin cash position hangs on the credit line and sale proceeds. Not investment advice.

What Our Rating Means

- If you don't own the stock

- At the current price level, we don't see a sufficient margin of safety for an entry.

- If you hold it in your portfolio

- Our findings offer no reason to sell.

A journalistic assessment by our editorial team at the time of the deep dive, based on public sources — not investment advice and not a solicitation to buy or sell. Your personal circumstances (investment goals, risk capacity, taxes) cannot be taken into account. What our categories mean, how verdicts are formed, and what conflicts of interest exist →

Worth Noting

- Smoke-detector note: the Insolvency Radar measures the balance-sheet date of March 31, 2026 — the Abilene proceeds (up to $19.5 million, April 30, 2026) flowed in afterward and improve the cash position in the following quarter; this analysis contains no insolvency verdict.

- Starting in the second quarter of 2026, the wind business (51 percent of 2025 revenue) will be reported as a discontinued operation — revenue and earnings series are then reclassified retroactively and only comparable to prior periods to a limited extent.

- AI finding: in the annual report (10-K) for 2025, artificial intelligence appears only in standard risk clauses (evaluation of "emerging technologies", competitive and legal risks) — no AI product, no AI revenue.

Frequently Asked Questions

Broadwind, based in Cicero, Illinois, manufactures large steel and precision components: historically mainly steel towers for wind turbines, plus gearing for oil, gas and mining customers and assemblies and installation kits for gas-turbine power plants. After the sale of both tower plants (September 2025 and April 2026), gearing and gas-turbine supply form the core; the wind business is reported as a discontinued operation starting in the second quarter of 2026.

We expressly do not render an insolvency verdict. The facts: as of March 31, 2026, only $943,000 sat in the till, and over the last four reporting quarters $4.4 million flowed out operationally. Against that stand $15.4 million of free credit line, the Abilene sale proceeds of up to $19.5 million (received after the reporting date), and growing order intake. Per the quarterly report (10-Q), management expects sufficient funds for at least twelve months.

Our Insolvency Radar is a smoke detector: it divides cash on hand by the average operating cash outflow of the last four reporting quarters. For Broadwind, $0.9 million in cash and about $1.1 million of outflow per quarter yield a calculated runway of about 0.8 quarters (data as of July 8, 2026). The radar measures a single balance-sheet date and doesn't see credit lines or later sale proceeds — which is exactly why every alarm deserves a look into the filings.

Because the subsidy landscape is collapsing: the U.S. law OBBBA of July 4, 2025 eliminates the AMP production credits for components after 2027 and ends the PTC/ITC tax credits for wind projects that start after July 4, 2026 and aren't in service by the end of 2027. Broadwind responded by selling Manitowoc ($13.5 million) and the Abilene tower plant (up to $19.5 million) and is concentrating on gearing and gas-turbine components.

Very important: in 2025 Broadwind booked $13.1 million of AMP credits as a cost reduction (2024: $9.6 million) — more than double the net income of $5.2 million, which also included an $8.2 million one-off gain from the Manitowoc sale. Without the credits and the sale proceeds, 2025 would have been clearly in the red; the credits end for components sold after 2027.

Depends on the price tag: measured against revenue it's cheap, with a price-to-sales ratio around 0.63 (data as of July 6, 2026), which is why it shows up in our P/S ranking. Measured against earnings it isn't: the P/E around 19 includes the one-off sale gain; based on earnings estimates the forward P/E sits around 43. Add to that roughly 12 percent of daily price swings and the ongoing corporate restructuring.

Found an error?

Did you spot a factual error, an outdated number, or a typo in this deep dive? Let us know briefly — your report goes straight to the editorial team.