Nvidia Stock: $120 Billion in Profit — and More Than Half the Revenue Hangs on Three Customers

Nvidia is the star witness of the AI boom: $215.9 billion in revenue (+65 percent) and $120.1 billion in net income for fiscal year 2026, roughly 90 percent of it from the data center business. We read the mandatory filings to the U.S. securities regulator — and that is where the other half of the story lives: three direct customers who most recently made up 54 percent of revenue, an investment book that doubled to $43.4 billion in a single quarter, $13 billion for a non-refundable license from rival Groq, a China business that export controls have effectively cut to zero, and $119 billion in purchase commitments. Our value scanner based on Joel Greenblatt's Magic Formula lights up anyway. Not investment advice — just a sober walk through a loop in which sellers, customers and financiers increasingly carry the same names.

There is a thinking trap that shapes almost every investor conversation in the summer of 2026. Call it the star-witness trap: when we want to prove the AI boom is real, we point to Nvidia's numbers. When we want to justify why Nvidia's numbers keep climbing, we point to the AI boom. The witness confirms the story, the story authenticates the witness — and at some point nobody checks what the star witness actually put on the record. That is exactly what we are catching up on today. Let's make a deal: we drop the headlines and read only what NVIDIA Corporation (Nasdaq: NVDA) reported, under penalty of law, to the U.S. securities regulator, the SEC — the annual report (10-K, the mandatory yearly filing) for fiscal year 2026 and the quarterly reports (10-Q). The occasion is serious: our in-house stock scanner based on Joel Greenblatt's Magic Formula — a value filter that hunts for good companies at fair prices, not a warning system — carries the stock in its hit list. The most valuable company in the world as a value candidate? That deserves a real read. And that read surfaces sentences you won't find in any celebratory press release: about three customers who make up more than half of revenue, about billion-dollar stakes in its own buyers, and about a government that expects 15 percent of the China revenue. In the end, you decide for yourself.

What Nvidia actually does — and why its fiscal year ends in January

For three decades Nvidia built graphics chips for computer games — and almost incidentally invented the computing architecture that artificial intelligence runs on today. Graphics processors (GPUs) can perform thousands of computing steps simultaneously instead of one after another; that is exactly what training and running large AI models requires. In its own annual report the company long ago stopped describing itself as a chipmaker and instead calls itself a "data center scale AI infrastructure company" — it sells not just chips, but complete data center systems made of GPUs, its own processors, networking technology (InfiniBand, Spectrum-X) and the software layer CUDA, which for nearly two decades has bound developers to Nvidia's platform — like a power-tool maker whose batteries only fit its own devices. The figures behind it: of fiscal year 2026's total revenue of $215.9 billion, $193.7 billion — about 90 percent — came from the data center business; the former core segment, gaming, still contributed $16.0 billion, professional visualization $3.2 billion and the automotive business $2.3 billion. At the end of the fiscal year the company employed about 42,000 people in 38 countries.

One peculiarity up front, so the year labels don't confuse you: Nvidia has an offset fiscal year that ends in late January. "Fiscal year 2026" therefore ran from January 27, 2025 to January 25, 2026 and essentially covers calendar year 2025; the "first quarter of 2027" ended on April 26, 2026. And note right away the central tension of this analysis, it runs through every chapter: Nvidia delivers perhaps the most flawless growth numbers in stock market history — but the customers, stakes and obligations of that growth form an ever-tighter loop in which the same few names appear on both sides of the ledger.

Where the stock shows up in our scanner

Every day we run about 3,500 stocks through our scanners. NVDA lit up on July 8, 2026 in seven scanners — every one of them a value, quality or growth filter, not a single warning scanner: "Joel Greenblatt: Magic Formula", "Peter Lynch: PEG ≤ 1", "Martin Zweig: Growth with Reason", "Buffett criteria", "Altman-Z: Balance Sheet Fortress", "Quality Stocks" and the EBIT margin ranking (in the live cross-check on July 14, 2026 the Greenblatt membership was confirmed; the scanner set drifts slightly day to day). Greenblatt's formula measures only two things: the return on capital (how much profit per dollar of operating capital employed?) and the earnings yield (how much profit per dollar of enterprise value?). Nvidia posts exceptional values on both: about 66 percent operating margin — of $100 in revenue, $66 remain as operating profit — and a price-to-earnings ratio of about 29, which looks almost modest for 65 percent growth. This is exactly where the second look pays off, because the formula has blind spots, and they are different every time: at Micron it misses the memory cycle, at Alphabet the antitrust courts. At Nvidia it is the structure of the growth itself: the formula sees the record profits — but not from how few buyers they come, and how much of Nvidia's own money now sits inside the customer loop.

The remaining metrics read like a textbook on balance sheet quality: the Piotroski F-Score, a nine-point test for the health of the books, stands at a strong 7 of 9. The Altman-Z score, a classic bankruptcy early-warning gauge, sits at 16.4 — danger begins below 1.8; Nvidia plays in a league of its own here, net debt is negative (more cash than debt, $8.5 billion in notes against $62.6 billion in cash and securities at fiscal year end). The return on equity of about 114 percent means: annual profit exceeds the entire book equity at the start of the year — a figure almost no large company in the world reaches. Two details cloud the picture: the relative strength of 62 says the price recently only outran a bit more than half of the market — up 38 percent over twelve months, but about 15 percent below the all-time high and, in the month before the data cut-off, down nearly 9 percent (all scanner figures: data as of July 8, 2026). And in the insider filings (Form 4, the mandatory disclosure of board and executive transactions) there were most recently 16 sells versus 4 buys. At tech companies with stock-based compensation this is normal noise — but a buy signal from inside still looks different.

The numbers over the years — honestly appraised

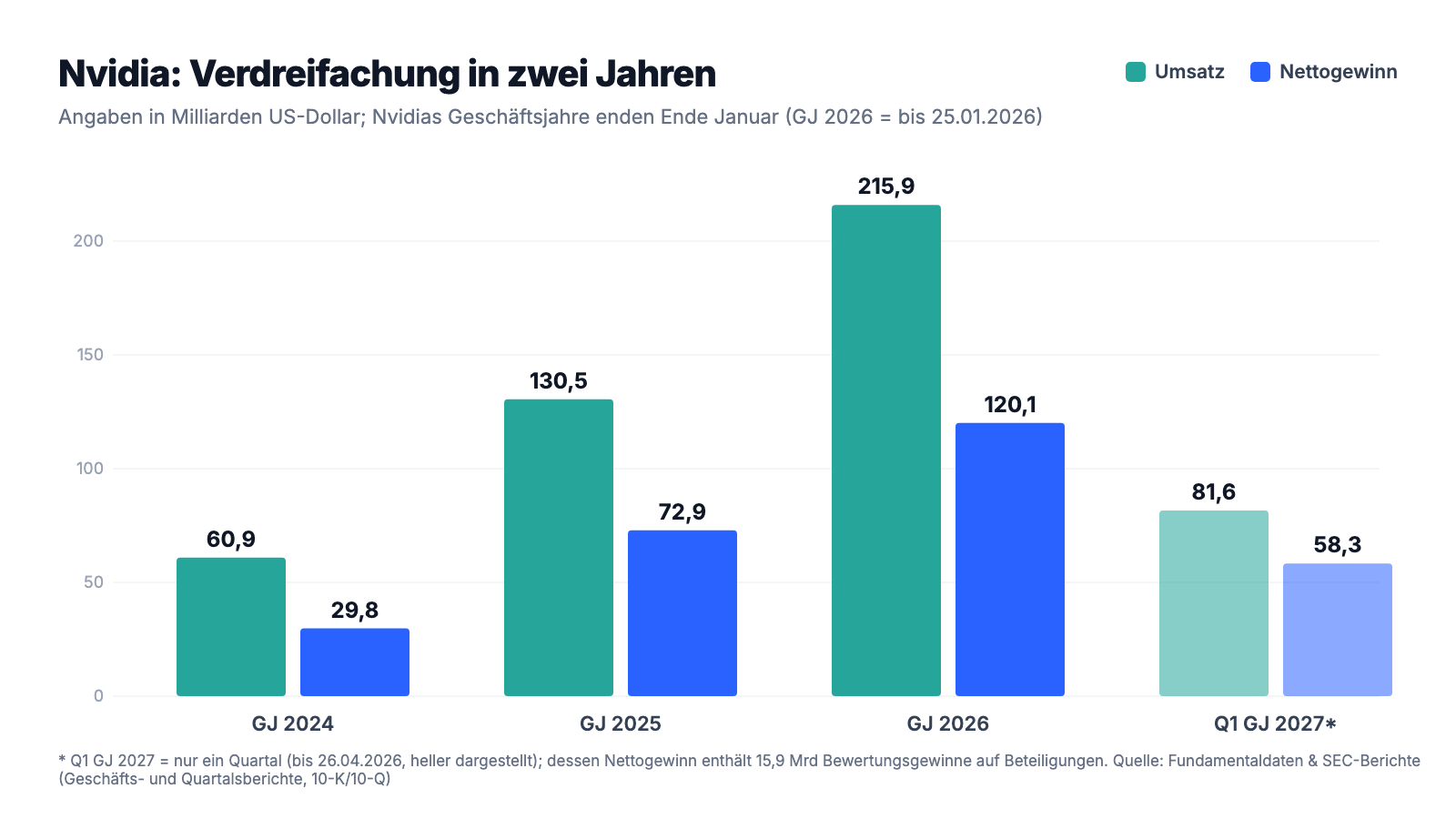

First, what is genuinely impressive — and at Nvidia that is more than at any other company of this size. Revenue rose from $60.9 billion (fiscal year 2024) via $130.5 billion (2025) to $215.9 billion (2026) — more than tripled in two years. Net income climbed over the same period from $29.8 via $72.9 to $120.1 billion; the net margin is 56 percent — of every dollar of revenue, 56 cents remain as profit, a figure other industries don't even have a word for. Operating cash flow reached $102.7 billion (after $64.1 and $28.1 billion in the two prior years). And the first quarter of fiscal year 2027 kept it up: $81.6 billion in revenue (+85 percent), of which $75.2 billion in the data center business (+92 percent), carried by the ramp of the new Blackwell systems; the gross margin bounced back to 74.9 percent after the prior-year quarter's China write-down had pushed it down to 60.5 percent. Interesting for the breadth of demand: about 50 percent of data center revenue comes, per the filing, from hyperscalers — the large cloud operators — and the other half from AI clouds, industry, enterprises and governments.

Honesty requires three footnotes to this fairy tale. First: the full-year gross margin fell from 75.0 to 71.1 percent — because of the shift to complete Blackwell data center systems (more material, more third-party parts per revenue dollar) and because of the $4.5 billion China write-down; total inventory write-downs reached $7.2 billion after $3.7 billion the prior year. Second: the record quarterly profit of $58.3 billion in the first quarter of 2027 includes $15.9 billion in valuation gains on securities — more than a quarter of the profit thus arose not from chips sold but from risen prices of stakes, above all the previously announced Intel position; operationally (actually earned) it was $53.5 billion, itself a record. Third, the company no longer grows out of its own balance sheet alone: the web of stakes and obligations meant to secure this growth has itself become worth billions — the next chapters are about that.

What the filings say — the uncomfortable truths

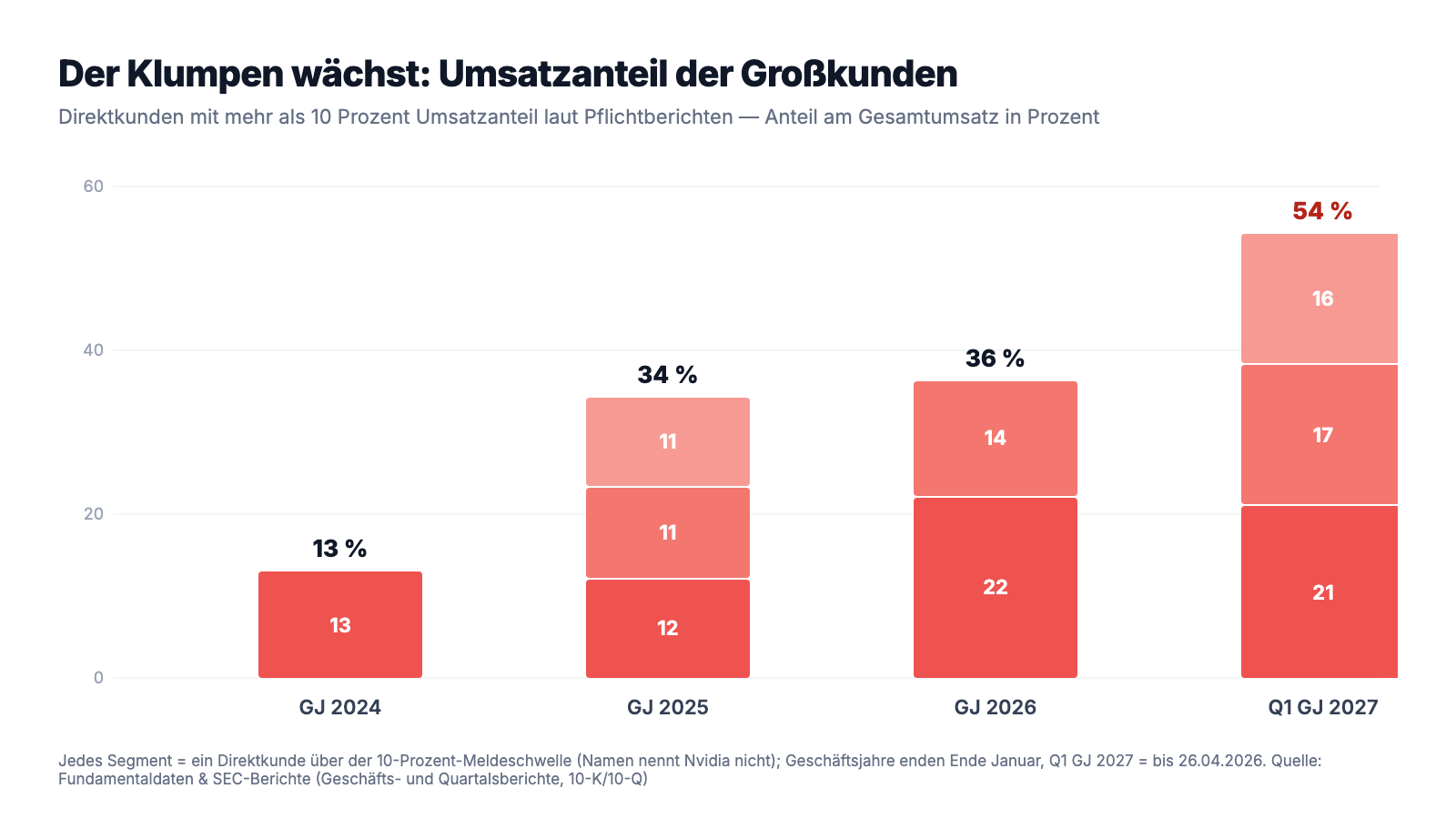

Uncomfortable truth no. 1: three customers, 54 percent of revenue — and 64 percent of the open invoices

Customer concentration sounds abstract, so let's make it concrete: picture a baker whose shop keeps getting busier — but more than every second roll is now bought by just three big buyers. That is exactly what the latest quarterly report says, in sober regulatory English:

"For the first quarter of fiscal year 2027, three direct customers represented 21%, 17%, and 16% of total revenue, all of which was primarily attributable to the Compute & Networking segment. For the first quarter of fiscal year 2026, sales to two direct customers represented 16% and 14% of total revenue, which were attributable to the Compute & Networking segment."

— NVIDIA Corporation, SEC quarterly report 10-Q as of April 26, 2026, Item 2 MD&A "Concentration of Revenue"

21 plus 17 plus 16: 54 percent of revenue from three buyers — and the trend points steeply upward: in fiscal year 2024 a single direct customer crossed the 10 percent reporting threshold (13 percent), in 2025 there were three totaling 34 percent, in 2026 two totaling 36 percent — including, for the first time, one at 22 percent. The picture is even more concentrated for the open invoices: three direct customers accounted for 30, 18 and 16 percent of receivables as of April 26, 2026 — 64 percent combined of $40.7 billion. Important to understand: at Nvidia, "direct customers" are often intermediaries — contract manufacturers and system integrators who build data centers for third parties; the filing does not name them. But the actual demand behind them is also bundling up: per the filing, single indirect customers also buy more than 10 percent of revenue, and one sentence stands out — Nvidia estimates that a single "AI research and deployment company" contributed a "significant" share of revenue via the cloud services of Nvidia's customers, in fiscal year 2026 as in the latest quarter. Who is meant, the filing does not say. Remember the image: the larger the revenue, the fewer shoulders carry it — and if one gives way, it isn't a fifth that wobbles, but half.

Uncomfortable truth no. 2: the seller takes stakes in its customers — the AI financing loop

The second truth is the most important of this analysis, because it touches the star-witness trap directly. Nvidia no longer just sells to the AI boom — it increasingly helps finance it. The traces run right across the filings: in fiscal year 2026 Nvidia bought $17.5 billion in non-publicly-traded stakes (prior year: $1.5 billion) and additionally paid $13 billion to the chip startup Groq for a non-exclusive technology license — non-refundable, as the risk chapter itself stresses. In the first quarter of 2027 alone another $18.6 billion in stake purchases were added; the book of non-publicly-traded stakes doubled within three months from $22.3 to $43.4 billion. As of April 26, 2026 there were also $27 billion in already-committed, not-yet-paid investments on the books — more than twice as much as three months earlier ($11.4 billion). And the biggest name is still to come:

"We are finalizing an investment and partnership agreement with OpenAI. There is no assurance that we will enter into an investment and partnership agreement with OpenAI or that a transaction will be completed."

— NVIDIA Corporation, SEC annual report 10-K for fiscal year 2026, Item 1A "Risk Factors"

Why is this explosive? Put the pieces together: OpenAI is, per the same body of filings, that unnamed "AI research and deployment company" whose indirect purchases contribute a "significant" share of revenue — and at the same time the target of a billion-dollar investment. The supplier takes a stake in the customer whose purchases drive its revenue, whose valuation in turn depends on the AI boom, whose most important proof is Nvidia's revenue. On top of this: Nvidia has signed cloud contracts worth $30 billion with cloud providers — so it buys computing power from the very companies that are its largest buyers; officially for research and development. It guarantees up to $3.5 billion for partners' data center rents — and gets paid for it with rights to acquire shares in those very partners. And the risk chapter reveals that the market demands even more: it has been asked to offer financing to customers and partners for their data center build-out — "we have not entered into any financing arrangements," it says, as of the annual report. To be fair: none of this is illegal or hidden, ecosystem investments are common in the platform business, and Nvidia discloses everything — including the warning that its own portfolio carries "industry concentration risks." But the competition authorities in the EU, the U.S., the U.K., China and South Korea are, per the filing, already making "broad information requests" — expressly also about Nvidia's "investments, partnerships, and other arrangements with foundation model developers." Remember the mechanism: a loop amplifies every move — the one upward, and the one downward.

Uncomfortable truth no. 3: China is practically gone — and Washington wants 15 percent of what's left

As recently as fiscal year 2022, China was a quarter of Nvidia's market; today the topic fills the longest passages of the risk chapter. The short version of the escalation since 2022: first U.S. export controls banned the top chips A100 and H100, then their throttled China versions, and finally, in April 2025, even the H20 chip developed specifically for China. The consequences are in the annual report — one of the most expensive passages in the company's history:

"As a result of these requirements, we incurred a $4.5 billion charge in the first quarter of fiscal year 2026 associated with H20 for excess inventory and purchase obligations, as the demand for H20 products diminished. In August 2025, the USG granted licenses that would allow us to ship certain H20 products to certain China-based customers. We generated approximately $60 million in H20 revenue under those licenses. USG officials expressed an expectation that the USG will receive 15% or more of the revenue generated from licensed sales of our products, but the USG did not publish a regulation codifying such requirement."

— NVIDIA Corporation, SEC annual report 10-K for fiscal year 2026, Item 1A "Risk Factors"

Read the numbers again: $4.5 billion written down, $60 million earned — for every dollar earned under license, $75 were written off to the scrap heap. The H200 shipments approved in February 2026 stand even worse: each chip must be physically inspected in the United States before export and thereby carries a 25 percent import tariff — revenue through the filing of the latest quarterly report: zero. And Beijing pushes from the other side: per the filing, the Chinese government has encouraged customers to buy from Chinese competitors and "discouraged" the purchase of Nvidia's data center products — in the latest quarter no more Hopper data center chips went to China, after $4.6 billion in the prior-year quarter. The good news lies in the contrast: despite the total loss of a once-billion-dollar market, group revenue grew 85 percent — the rest of the world has more than replaced China. The bad news: what grows in its place is exactly the customer concentration from truth no. 1. And should China ever return, Nvidia negotiates there with two governments at once — one that advises customers against, and another that expects 15 percent of the revenue.

Uncomfortable truth no. 4: $119 billion in purchase commitments — the advance outlay grows faster than revenue

Chips for data centers don't come on demand: Nvidia owns no factories of its own but orders from contract manufacturers like TSMC and from memory makers like Micron — with lead times that, per the filing, have already reached more than twelve months. Anyone who wants to deliver in a boom must reserve, prepay and commit years in advance. The scale of this bet is in the commitments note of the latest quarterly report:

"Manufacturing, supply, and capacity commitments reflect data center-scale production and longer future ordering horizons across current and future product architectures. […] As of April 26, 2026, these commitments were $119 billion for which $95 billion will be paid in the remainder of fiscal year 2027 and the remaining balance will be paid in fiscal years 2028 through 2031."

— NVIDIA Corporation, SEC quarterly report 10-Q as of April 26, 2026, Note 10 "Commitments and Contingencies"

At fiscal year end (January 25, 2026) these commitments stood at $95.2 billion — so within one quarter another $24 billion were added. At the same time inventories grew from $21.4 to $25.8 billion. Why this is more than accountant's prose is shown doubly by the recent past: the H20 episode from truth no. 3 demonstrated what happens when ordered goods lose their market — $4.5 billion written down with a stroke of the pen from Washington. And even Nvidia's own auditor declared the valuation of inventories and excess purchase obligations in the annual report an explicit "Critical Audit Matter" — a critical audit focus, because it depends on management assumptions about future demand. Add the competition from within: Nvidia's largest customers — the cloud giants — are developing their own AI chips, Alphabet for instance is betting heavily on its in-house TPU processors. The filing puts it dryly: "Some of our customers have in-house expertise and internal development capabilities similar to some of ours and can use or develop their own solutions to replace those we are providing." $119 billion in advance outlay, ordered from suppliers, sold to customers who are also competitors — that is the point at which the growth miracle becomes a lever that works in both directions.

Valuation: $4.9 trillion — surprisingly ordinary pricing for an exceptional company

In early July 2026 the stock cost about $196, the market value stood at roughly $4,945 billion — nearly $5 trillion, the most valuable company in the world, after plus 38 percent over twelve months and at the same time about 15 percent below the all-time high (all valuation figures: data as of July 8, 2026). And now the paradox: the price-to-earnings ratio is about 29 — for a company that last grew 65 percent and earns a 56 percent net margin, that is not a euphoria valuation but almost the normal measure; this is exactly why the Magic Formula lights up, and the price/earnings-to-growth ratio (PEG) of our Lynch scanner is also below 1. The counter-check belongs here: the price-to-sales ratio of about 19.5 and the price-to-book ratio of about 24 tell how much perfection is already priced in — on free cash flow, the market pays about 42 times. A P/E of 29 is cheap only if profit keeps growing or at least holds; if Nvidia's net margin fell even to the level of other world-class tech companies (30 to 40 percent), a P/E of 45 to 55 would sit on the price tag at the same revenue. And remember the $15.9 billion in valuation gains in the latest quarterly profit — paper, not chip revenue. Real money does flow back, at least: $40.4 billion in share buybacks in fiscal year 2026, another $20.2 billion in the first quarter of 2027 alone, and in May 2026 came $80 billion in fresh buyback authorization and a twenty-five-fold increase of the mini-dividend from $0.01 to $0.25 per quarter. The "professionals' view": 63 analysts, consensus clearly on "buy" — but for the star witness of the boom that is more choral singing than second opinion. Remember the core: what is paid for here is not the past — what is paid for is the assumption that three customers, one loop and $119 billion in advance outlay will keep pointing in the same direction for years.

Opportunities and risks at a glance

What speaks for Nvidia:

- Growth and profitability without historical precedent: $215.9 billion in revenue (+65 percent) and $120.1 billion in net income in fiscal year 2026, another +85 percent to $81.6 billion in the first quarter of 2027 — at a 74.9 percent gross margin and a 56 percent net margin (10-K 2026; 10-Q as of April 26, 2026).

- A deep moat of software and systems: the CUDA platform has bound developers for nearly two decades, and it sells complete data center systems including networking technology — half of data center revenue now comes from customers beyond the large cloud giants (10-Q as of April 26, 2026).

- Fortress balance sheet: $62.6 billion in cash and securities at fiscal year end against $8.5 billion in notes, Altman-Z about 16, Piotroski 7 of 9 — plus $40.4 billion in buybacks in fiscal year 2026, $80 billion in new buyback authorization and a dividend raised to $0.25 per quarter (May 2026).

- The China loss is already digested: despite the loss of a once-billion-dollar market (Hopper China revenue in the latest quarter: zero, after $4.6 billion) the company grew 85 percent — any easing would be extra upside, not a prerequisite (10-Q as of April 26, 2026).

- Seven value/quality scanner hits on July 8, 2026 (among them Greenblatt — confirmed live on July 14 —, Lynch PEG, Buffett criteria, Altman-Z), P/E about 29 and PEG below 1: for this growth and margin class that is not a euphoria valuation.

What speaks against it:

- Extreme customer concentration: three direct customers together made up 54 percent of revenue and 64 percent of receivables in the first quarter of 2027; on top of that a single AI company contributes a "significant" share of revenue via cloud detours (10-Q as of April 26, 2026).

- Circular AI financing: $43.4 billion investment book (doubled in one quarter), $27 billion in committed investments, $13 billion non-refundable Groq license, $30 billion in cloud purchases from its own customers, $3.5 billion in lease guarantees for warrants, OpenAI agreement being finalized — competition authorities in five jurisdictions are already making information requests (10-K 2026; 10-Q as of April 26, 2026).

- Geopolitics as a permanent state: $4.5 billion H20 write-down, only $60 million in license revenue, Washington's uncodified 15 percent expectation, H200 only after U.S. inspection plus 25 percent tariff, Beijing actively advising customers against buying (10-K 2026; 10-Q as of April 26, 2026).

- Advance-outlay lever: $119 billion in purchase commitments (plus $24 billion in one quarter), $25.8 billion in inventories, $7.2 billion in inventory write-downs in fiscal year 2026 — the valuation of these items is a disclosed critical audit matter of the auditor (10-K 2026).

- Customers as competitors and paper in the profit: the large buyers are developing their own AI chips ("can use or develop their own solutions to replace those we are providing"), and of the record quarterly profit $15.9 billion came from valuation gains on stakes; insiders most recently reported 16 sells versus 4 buys (10-K 2026; 10-Q as of April 26, 2026).

A human conclusion

Back to the star-witness trap. It is so powerful precisely because the witness isn't lying: Nvidia's numbers are real, audited, and in their combination of size, growth and margin without example. Anyone who has held the stock for years holds a company for the ages — and nothing in the mandatory filings says that ends tomorrow. But the same filings lay bare what the choral singing drowns out: more than half of revenue comes from three buyers. The most important end customer of the boom is set to become an equity stake too. The company buys cloud capacity from its customers, guarantees for its partners, licenses for $13 billion non-refundable from the challenger, and has signed $119 billion in advance outlays — all trusting that demand will hold, of which it is itself the most important proof. The Greenblatt scanner did its job: it found an unusually profitable company at a price that is fair relative to reported profit. What it cannot do: check whether the witness and the story hold each other up — or merely cite each other. You have now done that check yourself, with the original documents on the table. What you make of it is your decision. And that is exactly as it should be.

Sources

All original documents used in this analysis — to read for yourself:

- NVIDIA Corporation — SEC annual report 10-K for fiscal year 2026, ended January 25, 2026 (filed February 25, 2026)

- NVIDIA Corporation — SEC annual report 10-K for fiscal year 2025, ended January 26, 2025 (filed February 26, 2025)

- NVIDIA Corporation — SEC quarterly report 10-Q as of April 26, 2026 (filed May 20, 2026)

- NVIDIA Corporation — SEC quarterly report 10-Q as of October 26, 2025 (filed November 19, 2025)

- NVIDIA Corporation — SEC quarterly report 10-Q as of July 27, 2025 (filed August 27, 2025)

- NVIDIA Corporation — SEC quarterly report 10-Q as of April 27, 2025 (filed May 28, 2025)

- Nvidia's complete SEC filing history: EDGAR overview (sec.gov)

- Fundamental data (metrics, valuation, analyst consensus; data as of July 8, 2026), reconciled with the SEC filings.

- Screener and rating data: in-house stock scanner (data as of July 8, 2026; Greenblatt membership verified live on July 14, 2026).

Transparency & disclaimer: This analysis is a journalistic contextualization of publicly available information and is not investment advice, not a financial analysis in the regulatory sense, and not a solicitation to buy or sell securities. Stock investments carry substantial risks up to total loss. All information without guarantee; the data cut-off is noted in the text in each case. The author holds no position in Nvidia stock at the time of publication.

Our Bottom Line at a Glance

- Market position & product positive

- The de facto standard of AI infrastructure: 90 percent of revenue from the data center business, CUDA software as a developer moat, complete systems instead of single chips; half of data center revenue now comes from customers beyond the hyperscalers (10-K 2026; 10-Q as of April 26, 2026).

- Earning power & balance sheet positive

- $215.9 billion in revenue (+65 percent) and $120.1 billion in net income in fiscal year 2026, $102.7 billion in operating cash flow, $62.6 billion in cash/securities against $8.5 billion in notes, Altman-Z about 16 — plus $40.4 billion in buybacks and a dividend raised to $0.25 per quarter in May 2026.

- Customer concentration & loop negative

- Three direct customers = 54 percent of quarterly revenue and 64 percent of receivables; at the same time $43.4 billion investment book, $27 billion in committed investments, $13 billion non-refundable Groq license, $30 billion in cloud purchases from its own customers, OpenAI agreement being finalized — and information requests from competition authorities in five jurisdictions (10-K 2026; 10-Q as of April 26, 2026).

- Geopolitics & advance-outlay lever negative

- China data center business practically zero ($4.5 billion H20 write-down, $60 million license revenue, Washington's 15 percent expectation, Beijing advising customers against); plus $119 billion in purchase commitments (+$24 billion in one quarter) and $25.8 billion in inventories, whose valuation is a critical audit matter of the auditor (10-K 2026; 10-Q as of April 26, 2026).

- Valuation & profit quality neutral

- A P/E of about 29 and PEG below 1 are moderate for 65 percent growth (data as of July 8, 2026) — but a P/S of about 19.5 and P/B of about 24 price in sustained perfection, the latest quarterly profit included $15.9 billion in valuation gains on stakes, and insiders reported 16 sells versus 4 buys.

Nvidia is the rare case in which the most valuable company in the world is at the same time a value scanner hit: 65 percent growth, 56 percent net margin, a fortress balance sheet and a P/E of about 29 — the Magic Formula does find genuinely exceptional quality at a fair price here. Set against this are findings no scanner can price: more than half of revenue comes from three direct customers, the company increasingly takes stakes in its own buyers ($43.4 billion investment book, $27 billion in commitments, OpenAI agreement being finalized), the China business is politically cut to zero, and $119 billion in purchase commitments bet that demand will hold, of which Nvidia's own revenue is the most important proof. Not investment advice.

What Our Rating Means

- If you don't own the stock

- At the current price level, we don't see a sufficient margin of safety for an entry.

- If you hold it in your portfolio

- Our findings offer no reason to sell.

A journalistic assessment by our editorial team at the time of the deep dive, based on public sources — not investment advice and not a solicitation to buy or sell. Your personal circumstances (investment goals, risk capacity, taxes) cannot be taken into account. What our categories mean, how verdicts are formed, and what conflicts of interest exist →

Worth Noting

- Nvidia has an offset fiscal year (ending in late January): "fiscal year 2026" ended on January 25, 2026, "first quarter of 2027" on April 26, 2026 — the periods are dated in the text in each case.

- The net income of the first quarter of 2027 ($58.3 billion) included $15.9 billion in unrealized valuation gains on securities (among them the Intel stake); the operating result of $53.5 billion is the more reliable measure.

- Price and valuation figures are dated to July 8, 2026 (about $196 per share, about $4,945 billion market value); analyses are evergreen, daily prices are not a buy argument.

- The scanner membership was checked twice: data as of July 8, 2026 (seven value/quality scanners) and a live check on July 14, 2026 (Greenblatt confirmed; the rest of the scanner set drifts day to day).

- Nvidia does not name the three big customers in the mandatory filings; the "AI research and deployment company" with a significant indirect revenue contribution also remains unnamed there.

Frequently Asked Questions

Nvidia (Nasdaq: NVDA) sells data center-scale AI infrastructure: graphics processors (GPUs), complete server systems, networking technology and the CUDA software platform. In fiscal year 2026 (ended January 25, 2026), $193.7 of $215.9 billion in revenue — about 90 percent — came from the data center business; gaming contributed $16.0 billion.

Nvidia uses an offset fiscal year that closes in late January each time — a practice common among U.S. tech companies. "Fiscal year 2026" ran from January 27, 2025 to January 25, 2026 and thus essentially covers calendar year 2025. The "first quarter of 2027" ended on April 26, 2026. All figures in this analysis name the respective cut-off date.

Very concentrated and increasingly so: in the first quarter of fiscal year 2027, three direct customers made up 21, 17 and 16 percent of revenue — 54 percent combined — and 64 percent of open receivables. In fiscal year 2024 only one customer was above the 10 percent threshold. On top of that, per the filing, a single AI company contributes a "significant" share via cloud purchases from Nvidia's customers.

The 2026 annual report names an investment and partnership agreement with OpenAI "being finalized" — with no assurance of completion. The explosive part is the dual role: the same body of filings estimates that a single AI company already contributes a significant part of revenue via cloud detours. The supplier would thus take a stake in one of its most important end customers.

Nvidia increasingly invests in its own customer ecosystem: $43.4 billion investment book (April 26, 2026, doubled in one quarter), $27 billion in committed investments, $30 billion in cloud purchases from its own buyers, $3.5 billion in lease guarantees for partners in exchange for warrants and $13 billion in license payments to Groq. Money thus flows in a circle — which amplifies both upswing and downswing.

The China data center business has all but disappeared: a $4.5 billion H20 write-down in spring 2025, then only about $60 million in revenue under U.S. licenses; in the quarter ended April 26, 2026 no more Hopper chips went to China (prior year: $4.6 billion). The U.S. government also expects 15 percent of licensed revenue — with no published regulation. Even so, group revenue grew 85 percent.

Joel Greenblatt's Magic Formula hunts for companies with a high return on capital and a high earnings yield. Nvidia posts extreme values: about 66 percent operating margin, 114 percent return on equity and a price-to-earnings ratio of about 29 (data as of July 8, 2026). The formula's weakness: it sees neither the customer concentration nor the financing loop behind the profit.

Measured by the price-to-earnings ratio of about 29 at 65 percent growth it looks moderately valued, and the PEG is below 1 (data as of July 8, 2026). But the price-to-sales ratio of about 19.5 shows how much perfection is priced in: the math only works as long as the 56 percent net margin and the demand of the three big customers hold. The latest quarterly profit also included $15.9 billion in valuation gains.

Found an error?

Did you spot a factual error, an outdated number, or a typo in this deep dive? Let us know briefly — your report goes straight to the editorial team.