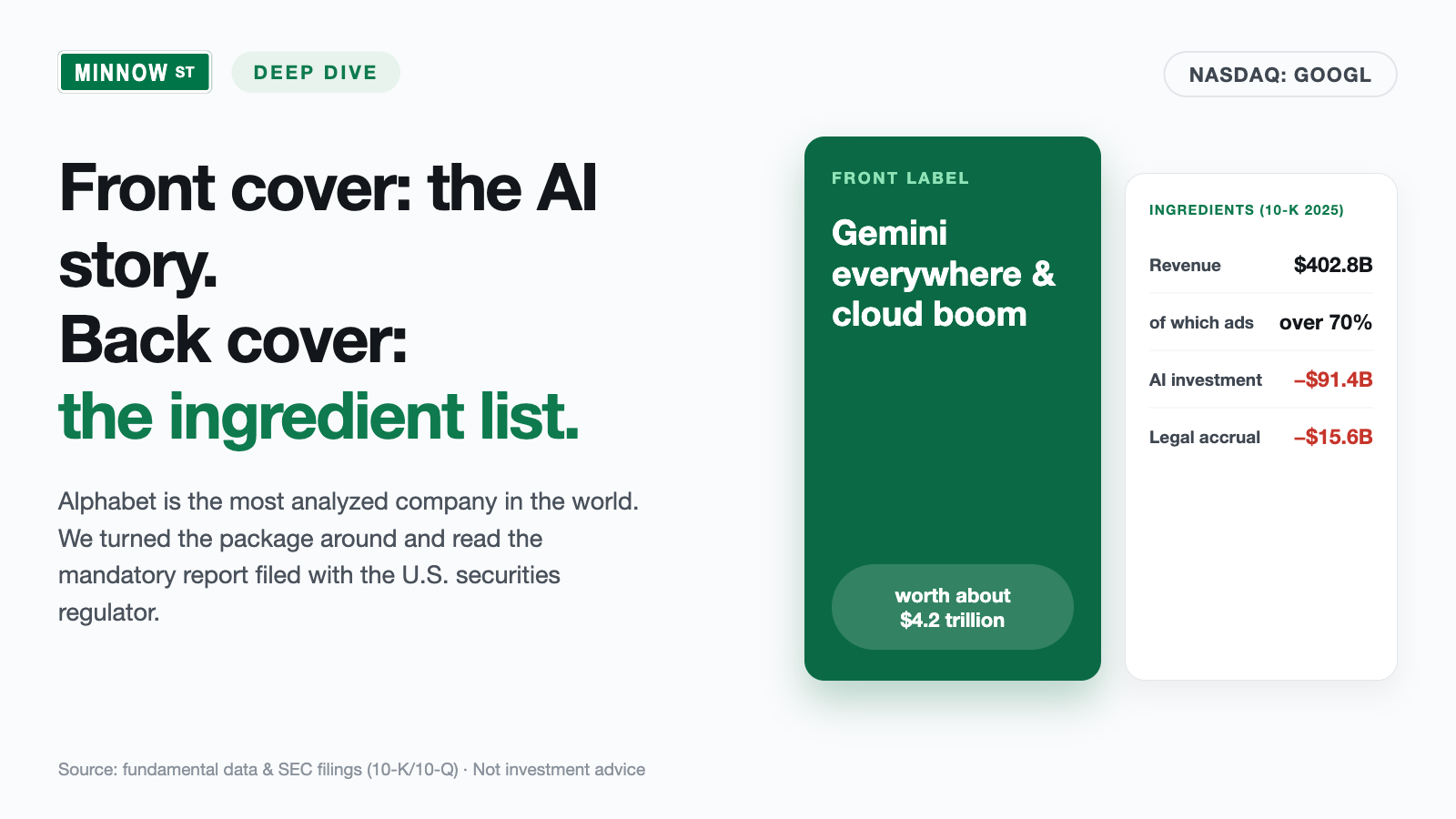

Alphabet Stock: $132 Billion in Profit, Antitrust Rulings on Three Continents — and the Most Expensive Construction Site in Stock Market History

Alphabet is the most analyzed company in the world — and precisely for that reason hardly anyone actually reads what its annual report (10-K) says. We did: $402.8 billion in revenue and $132.2 billion in net income for 2025, a cloud order backlog that quintupled to $467.6 billion in 15 months — but also $91.4 billion in AI investment with a growing depreciation burden, a final antitrust judgment in Washington, a threatened partial break-up of the ad business, $15.6 billion in legal accruals and a quarterly profit more than half of which consisted of unrealized valuation gains on stakes. Our value scanner based on Joel Greenblatt's Magic Formula lights up anyway. Not investment advice — we merely read the back of the most famous package on the market.

There is a thinking trap that works most powerfully on precisely the most famous stocks. Call it delegated diligence: "Alphabet? Thousands of analysts watch it, millions of investors, every regulator in the world. If something were wrong, we would have known long ago." So you check — nothing. Everyone relies on everyone else, and in the end the most watched company in the world has astonishingly few real readers. That is exactly why we are making a deal: today we treat Alphabet (Nasdaq: GOOGL and GOOG — more on the two tickers in a moment) like an unknown small cap. No headlines, no price-target studies, only what the company itself reported, under penalty of law, to the U.S. securities regulator, the SEC: the annual report (10-K, the mandatory yearly filing) for 2025 and the quarterly reports (10-Q). The occasion is serious enough: our in-house stock scanner based on Joel Greenblatt's Magic Formula — a value filter, not a warning system — carries the stock in its hit list. A four-trillion-dollar company as a value candidate? That deserves a real read. And that read brings things to light that appear in hardly any headline: guarantees for third-party data centers, a final antitrust judgment with a double appeal, and a record quarterly profit more than half of which consists of paper gains. In the end, you decide for yourself.

What Alphabet actually does — and why there are two tickers

Alphabet has been the holding company above Google since 2015, and its business model can be told in one sentence: the company operates the world's largest collection points for attention and sells that attention to advertisers. Google Search and partner services alone brought in $224.5 billion in 2025, YouTube advertising $40.4 billion, the ad network on third-party sites $29.8 billion — together that is the lion's share of the $402.8 billion in total revenue. Add $48.0 billion from subscriptions, platforms and devices (YouTube Premium, Google One, Play Store, Pixel), the growth jewel Google Cloud at $58.7 billion — the rental of computing power, storage and AI models to businesses — and the bets on the future ("Other Bets" such as the robotaxi subsidiary Waymo) with a modest $1.5 billion in revenue against a $7.5 billion operating loss. The company's own ambition is stated in the first paragraph of the annual report: since 2016 Google has seen itself as an "AI-first company," and by now, per the filing, the in-house Gemini models sit in all 15 products with more than half a billion users. At the end of 2025 the company employed 190,820 people worldwide.

And why two tickers? Alphabet has three share classes of the same company: GOOGL is the Class A share with one vote apiece, GOOG the Class C share with no voting rights at all — both participate identically in profit and dividend, and both trade at nearly the same price on the Nasdaq. The third class (Class B, ten votes per share) is not listed and sits almost entirely with the founders: per the annual report, Larry Page and Sergey Brin held about 89.3 percent of the B shares at the end of 2025 and thereby controlled about 52.7 percent of all voting rights — an absolute majority, however the remaining shareholders vote. So whether you buy GOOGL or GOOG is economically almost irrelevant; either way you have practically no say. This analysis covers both classes. Note in advance the central tension of this analysis, it runs through every chapter: Alphabet is the most reliable profit machine on the stock market — and is currently using its records to finance two open mega-bets at once: that the most expensive investments in company history in AI will pay a return, and that the courts will merely file at the foundation instead of tearing it down.

Where the stock shows up in our scanner

Every day we run about 3,500 stocks through our scanners. GOOGL lit up on July 8, 2026 in three scanners — value/quality scanners without exception, not a single warning scanner: "Joel Greenblatt: Magic Formula", "Martin Zweig: Growth with Reason" and "Buffett criteria" (in the live cross-check on July 14, 2026, Greenblatt and Zweig were still active; the stock had meanwhile dropped out of the Buffett scanner). Greenblatt's formula hunts, put plainly, for good companies at fair prices — measured by exactly two numbers: the return on capital (how much profit per dollar of operating capital employed?) and the earnings yield (how much profit per dollar of enterprise value?). Alphabet delivers both: about 36 percent operating margin, just under 39 percent return on equity — and a price-to-earnings ratio of about 26, which does not sound like exuberance for this quality. This is exactly where the second look pays off, because the formula has blind spots, and they are different every time: at Micron the memory cycle tricked the formula, at MSG Entertainment the balance sheet structure. At Alphabet it is subtler: the formula sees the profit — but it sees neither the court sawing at the distribution model behind that profit, nor the question of how much of the latest profit jump is paper.

The remaining metrics paint the picture of a quality giant in robust but not euphoric shape: the Piotroski F-Score, a nine-point test of balance sheet quality, stands at a solid 6 of 9. The Altman-Z score, a classic bankruptcy early-warning gauge, sits at a thoroughly healthy 10.1 (danger begins below 1.8) — payment problems are simply not a topic here. The relative strength of 79 says: better than four-fifths of the market, without overheating; over twelve months the price has roughly doubled, but trades about 14 percent below the all-time high (all scanner figures: data as of July 8, 2026). Two details still deserve a look: the fundamental rating stands at only B (47), mid-table — the profit quality has scratches, more on that shortly. And in the insider filings (Form 4, the mandatory disclosure of board and executive transactions) there were most recently 17 sells versus 3 buys; the CEO sold too. At tech companies with stock-based compensation this is normal noise — but a buy signal from inside still looks different.

The numbers over the years — honestly appraised

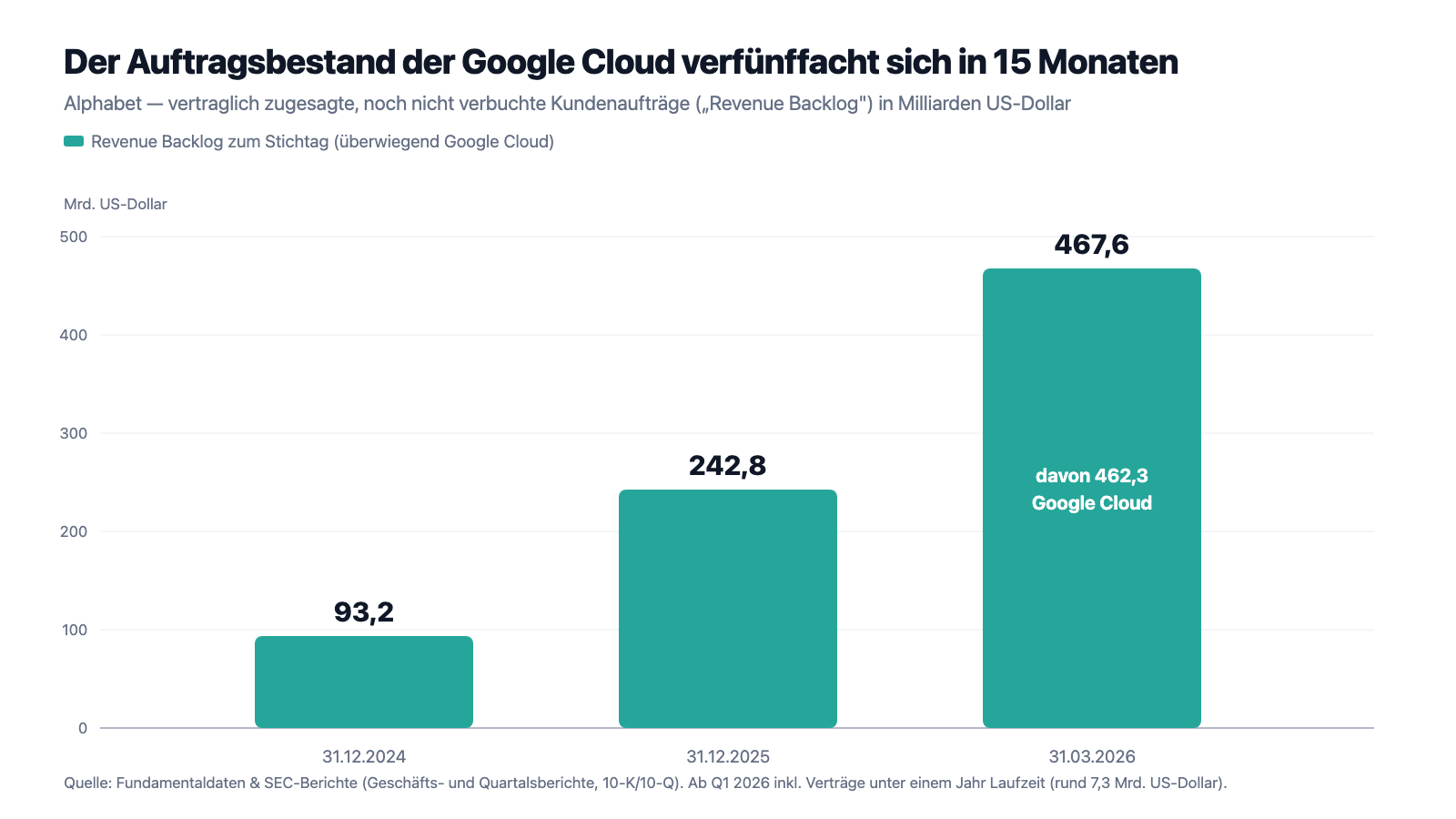

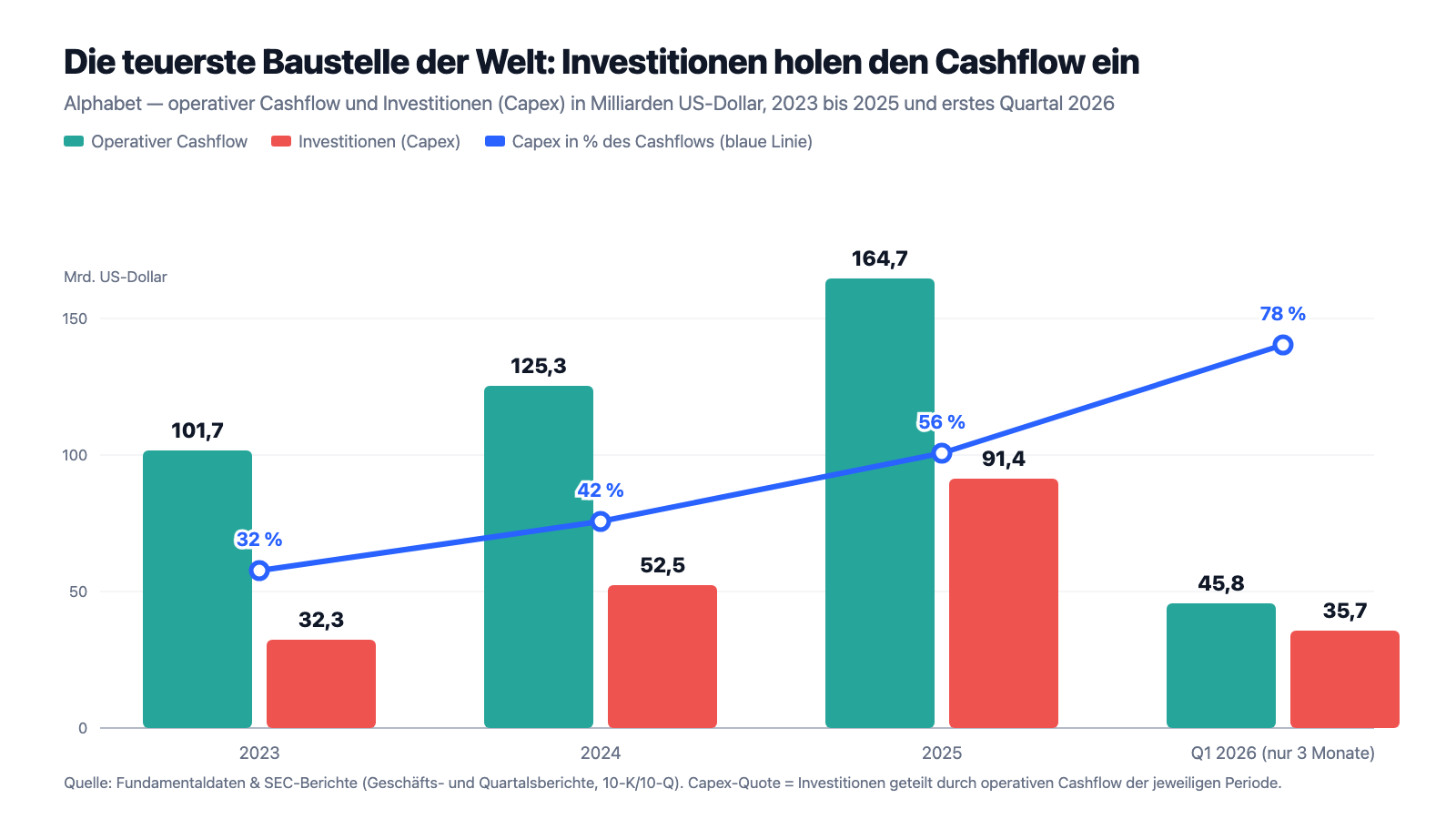

First, what is genuinely impressive — and at Alphabet that is a lot. Revenue rose from $307.4 billion (2023) via $350.0 billion (2024) to $402.8 billion (2025), plus 15 percent in the last step. Net income climbed over the same period from $73.8 via $100.1 to $132.2 billion — a third more in a single year —, earnings per share from $5.80 to $10.81, in part because ongoing buybacks ($45.4 billion in 2025 alone) keep reducing the share count. Operating cash flow reached $164.7 billion. And the first quarter of 2026 kept it up: $109.9 billion in revenue (+22 percent versus the prior-year quarter), $39.7 billion in operating income (+30 percent). The star is Google Cloud: $20.0 billion in quarterly revenue (+63 percent), $6.6 billion in quarterly operating profit — three years ago the segment was still posting losses. Most spectacular of all, though, is a number hardly anyone knows because it sits only in the fine print: the revenue backlog — contractually committed, not yet booked customer orders, overwhelmingly cloud contracts. End of 2024: $93.2 billion. End of 2025: $242.8 billion. As of March 31, 2026: $467.6 billion. Quintupled in 15 months — the AI companies and large enterprises of this world have reserved computing power at Google for years to come.

The balance sheet behind it remains a fortress — with a new crack in the masonry. As of March 31, 2026, $126.8 billion sat in cash and short-term securities; equity stood at $478.7 billion. But for the first time in its history the company is taking on debt at scale: outstanding notes grew from $11.9 billion (end of 2024) via $48.5 billion (end of 2025) to $79.1 billion as of March 31, 2026 — sextupled in 15 months. Why the most profitable advertising machine in the world is borrowing money is shown in the next section: it is building. So much, in fact, that even its cash flow stream no longer comfortably covers it.

What the filings say — the uncomfortable truths

Uncomfortable truth no. 1: more than 70 percent advertising share — and courts on three continents are working on the distribution model

First the sober self-disclosure from the risk chapter: "We generated more than 70% of total revenues from online advertising in 2025." The foundation of this advertising empire is distribution: Google pays so-called traffic acquisition costs (TAC) — $59.9 billion in 2025 — above all to be the preset search engine on smartphones and in browsers. Translated: the company rents the front doors through which billions of people enter the internet. It is precisely this model that U.S. courts have ruled anticompetitive, and since December 2025 there has been an enforceable final judgment on it:

"In August 2024, the US District Court for the District of Columbia ruled against Google. A final judgment was entered in December 2025, which, among other things, imposes restrictions on how Google distributes its services and requires Google to share certain search data with and offer syndication services to certain competitors. In January 2026, we appealed the final judgment and moved to pause implementation of certain remedies. In February 2026, the DOJ and state Attorneys General also appealed."

— Alphabet Inc., SEC annual report 10-K 2025, Note 10 "Commitments and Contingencies — Antitrust: Search"

And that is just one front. In the second U.S. antitrust case, on ad tech, a federal court in Virginia ruled in April 2025 that Google's tools for website operators "unfairly excluded" competitors; as a remedy the U.S. Department of Justice explicitly demands structural relief — in plain language: the forced sale of parts of the ad business — which per the filing could have "a material adverse effect on our business"; the decision was still pending at the annual report's editorial close. In Europe, the EU Commission imposed a fine of 3.0 billion euros in September 2025 (Alphabet booked a $3.5 billion expense for it) for self-preferencing in ad tech, two proceedings under the Digital Markets Act (DMA) are ongoing, Australia forced changes to the Android contracts via settlement, and Japan's antitrust authority issued a cease-and-desist order. The balance sheet trace of all this: $15.6 billion in short-term accruals for legal and regulatory penalties at the end of 2025. Honesty also requires the other side: the December judgment stayed far short of the maximum demands — a forced sale of the Chrome browser, for instance, did not come —, and Google is fighting the data-sharing obligations just as the other side is fighting remedies it considers too mild. But the direction is unmistakable: the distribution model that carries more than 70 percent of revenue is being rebuilt worldwide as we speak — only the extent is still open.

Uncomfortable truth no. 2: the most expensive construction site in stock market history — and its depreciation is still to come

Alphabet invested $91.4 billion in 2025, almost twice as much as the year before ($52.5 billion) and almost three times as much as in 2023 ($32.3 billion) — overwhelmingly in data centers, servers and networking technology for AI. In the first quarter of 2026 alone another $35.7 billion was added, and for the full year the filing announces a significant increase versus 2025. What that means for future profits the company writes itself — it is perhaps the most important sentence of the entire annual report:

"We invested heavily in capital expenditures in 2025 and in 2026, we expect to significantly increase, relative to 2025, our investment in our technical infrastructure, including servers and network equipment, and data centers. The costs associated with operating our technical infrastructure — depreciation, energy, equipment, and network capacity — are expected to significantly increase as developing and serving AI offerings require more compute power than our historical consumer and enterprise offerings."

— Alphabet Inc., SEC annual report 10-K 2025, Item 7 MD&A "Trends in Our Business — Increased Investment in Technical Infrastructure"

Depreciation is the mechanism by which today's construction spending eats into the profit statements of the coming years: at Alphabet a server is depreciated over about six years — so what is built in 2025 weighs on the margin until roughly 2031. The number series has started to run: $11.9 billion in depreciation on property and equipment in 2023, $15.3 billion in 2024, $21.1 billion in 2025, $6.5 billion in the first quarter of 2026 alone. And the pipeline behind it is enormous: $149.1 billion in purchase and contract commitments (of which $113.0 billion short-term, predominantly for technical infrastructure), plus already-signed but not yet commenced data center leases of a further $58.5 billion with terms of up to 25 years. To finance it, the company issued notes of $22.5 billion and 13.25 billion euros in 2025, and another $31.1 billion in the first quarter of 2026. To be fair: Alphabet is not building into the blue — the quintupled cloud backlog from the last chapter is the order list for exactly this construction site. But a backlog is a promise, not a guarantee, and data centers are built for decades. Remember the mechanism: if AI demand grows merely normally instead of spectacularly, "significantly rising" fixed costs meet overbuilt capacity — that is the script with which every infrastructure euphoria in stock market history has ended.

Uncomfortable truth no. 3: the record quarterly profit was more than half paper

$62.6 billion in net income in a single quarter — the first quarter of 2026 looked like the best in company history, almost a doubling versus the prior year. Anyone who read only the headline missed the decisive sentence in the management discussion:

"OI&E of $37.7 billion for the three months ended March 31, 2026 included net gains on equity securities of $36.9 billion, primarily related to unrealized gains on our non-marketable equity securities."

— Alphabet Inc., SEC quarterly report 10-Q as of March 31, 2026, Item 2 MD&A "Executive Overview"

Unrealized gains on non-marketable equity securities — translated: Alphabet's startup stakes became more valuable on paper because other investors paid higher prices in new funding rounds. Nothing was sold; no customer money flowed for it. The portfolio of these stakes stood at $101.3 billion on the books as of March 31, 2026; in the first quarter alone, holdings with a carrying value of $73.6 billion were remeasured. The filing names no names — from prior years only the direction is known: Alphabet holds stakes in numerous AI companies whose valuations have exploded in the boom. The AI boom is thus valuing Alphabet's stakes in that very boom — a feedback loop that works in both directions: full-year 2025 already had $24.1 billion of such valuation gains in net income; if euphoria pops, book gains become book losses, with the same force. Honesty requires: even without any paper effect the quarter would have been strong — $39.7 billion in operating income was genuinely earned. But for the price-to-earnings ratio it means: whoever computes the optically low P/E on the basis of the last four quarters is computing with profits of which a growing share is other people's valuation fantasy.

Uncomfortable truth no. 4: Alphabet now guarantees billions for third-party data centers

The fourth truth is the least known, and it appeared in this form for the first time in the updated risk chapter of the latest quarterly report. Alphabet does not just build itself — it now also guarantees the obligations of third-party data center and energy projects, so that others pre-finance the infrastructure of the AI boom:

"We also have a number of large, long-duration commercial agreements, which could increase our liabilities and obligations in the event of nonperformance by us, our counterparties, or vendors. These include certain financial guarantees, such as backstops to support the build-out of third-party data centers and power infrastructure. In the event of such nonperformance or industry challenges, we may incur additional liabilities, have excess capacity that we cannot easily redeploy, and not receive payments from our counterparties or customers."

— Alphabet Inc., SEC quarterly report 10-Q as of March 31, 2026, Part II, Item 1A "Risk Factors"

The scale is in the derivatives note: at the end of 2025 these guarantees amounted to at most $16.9 billion (credit derivatives for data centers) plus $5.7 billion in financial guarantees; as of March 31, 2026 it was already $28.4 plus $9.0 billion — and in April 2026, per the filing, new data center guarantees of roughly $15.3 billion were added, with terms of up to 15 years. Added up, the guarantee book is approaching a good $50 billion — arisen out of nothing in a little over a year. Why does a company with $126.8 billion in cash do such a thing? Because even Alphabet cannot and does not want to build everything itself at once: third parties erect data centers and power plants, banks finance them — but only if a first-class debtor assumes the default risk. The AI boom is increasingly cross-financed, and Alphabet has quietly become the credit insurer of its own supply chain. As long as the boom carries, this costs nothing. If it doesn't, the guarantees materialize exactly when the company's own business is weakening too — the same uncomfortable simultaneity we know from every credit-cycle lesson.

Valuation: $4.2 trillion — plenty of quality, fairly priced, two open bets

In early July 2026 the A share cost about $344; the market value stood at roughly $4,194 billion — a good $4.2 trillion, after roughly a doubling of the price within twelve months and at the same time about 14 percent below the all-time high (all valuation figures: data as of July 8, 2026). The price-to-earnings ratio of about 26 on the basis of the last four quarters is anything but excessive for a company with 15 percent revenue growth, a 36 percent operating margin and net cash — which is exactly why the Magic Formula lights up. But run the counter-check: first, this profit contains the paper share from truth no. 3 — adjusted for valuation gains, the P/E would sit noticeably higher. Second, a look at free cash flow shows what the construction site costs: of the 2025 operating cash inflow ($164.7 billion), after $91.4 billion in investments only a good $73 billion remained — measured on free cash flow, the market thus pays about 57 times, and in the current year, with the build ratio rising again, rather more. The price-to-sales ratio sits at about 9.9, price-to-book at about 8.8. Set against this are tangible shareholder returns: $45.4 billion in buybacks in 2025 (a further $69.5 billion is authorized) and a young, small dividend of $0.22 per quarter (raised in April 2026). The "professionals' view": 68 analysts, consensus on average clearly at "buy" — though for the most analyzed company in the world that is ambient temperature rather than information. Remember the core: a P/E of 26 is only cheap if the "E" keeps running — and it is precisely the "E" that the courts, the depreciation and the question of how much AI demand ultimately gets paid for in real money are all working on at once.

Opportunities and risks at a glance

What speaks for Alphabet:

- An earnings machine of historic proportions: $402.8 billion in revenue (+15 percent) and $132.2 billion in net income in 2025, $39.7 billion in operating income in the first quarter of 2026 alone (+30 percent) — at a 32 percent group operating margin (10-K 2025; 10-Q as of March 31, 2026).

- The cloud/AI surge is contractually underpinned: Google Cloud grew 63 percent in the first quarter of 2026 to $20.0 billion in quarterly revenue and is profitable; the revenue backlog quintupled in 15 months to $467.6 billion (10-Q as of March 31, 2026).

- Fortress balance sheet despite the construction offensive: $126.8 billion in cash and short-term securities, $478.7 billion in equity, Altman-Z about 10 — plus $45.4 billion in buybacks in 2025, $69.5 billion in authorized buyback volume and a growing quarterly dividend ($0.22 since April 2026).

- A Gemini ecosystem with unique reach: per the annual report, all 15 products with more than half a billion users run on the in-house Gemini models; in-house TPU chips reduce dependence on external AI processors (10-K 2025).

- Three value/quality scanner hits on July 8, 2026 (Greenblatt, Zweig, Buffett criteria; Greenblatt and Zweig confirmed live on July 14), Piotroski 6 of 9, P/E about 26 — no euphoria valuation for this quality.

What speaks against it:

- More than 70 percent of revenue hangs on online advertising whose distribution model is being legally rebuilt: a Search final judgment with data-sharing obligations (December 2025, both sides appealing), threatened structural remedies in ad tech, a $3.5 billion EU fine, DMA proceedings, $15.6 billion in legal accruals (10-K 2025).

- The investment avalanche weighs for years: $91.4 billion in capex in 2025, "significantly more" for 2026, depreciation up from $15.3 to $21.1 billion and per the filing rising further "significantly"; $149.1 billion in purchase commitments plus $58.5 billion in future data center leases (10-K 2025).

- The capital structure is turning: note debt sextupled to $79.1 billion within 15 months, plus guarantees for third-party data centers and power plants of by now roughly $37 billion plus about $15.3 billion newly added in April 2026 (10-Q as of March 31, 2026).

- Profit quality with a paper share: $36.9 of the $62.6 billion quarterly profit in the first quarter of 2026 were unrealized book gains on stakes, and 2025 already included $24.1 billion from valuation gains — the same mechanics work in reverse in a downturn (10-Q as of March 31, 2026; 10-K 2025).

- AI is opportunity and attack at once: the company's own filing warns that competitors could develop similar or better AI products at lower cost and that users could change how they seek information — this is about precisely the search queries that carry the bulk of the profit today; add voting concentration: the founders control 52.7 percent of the votes (10-K 2025).

A human conclusion

Back to delegated diligence. Its trick is that it feels like reason: who am I to doubt the most analyzed company in the world — or to trust it without reading? After reading the filings, the picture is in any case clearer than any headline: Alphabet is operationally stronger than ever — Search is growing, YouTube is growing, the cloud is booming with a contractually secured backlog of nearly half a trillion dollars. Anyone holding the stock holds an exceptional company at a price that values this strength fairly but not megalomaniacally. And yet this company has rarely had so much open at the same time: a final judgment tinkering with its distribution model, under double appeal; a possible forced restructuring of the ad-tech business; a construction site whose depreciation is guaranteed to weigh on the margins of the coming years while its returns still have to be earned; a profit statement in which other people's valuation fantasy resonates; and a quiet guarantee book for the infrastructure of the entire boom. None of this is hidden — it all sits in the same mandatory filings the records come from. The Greenblatt scanner did its job: it found a very good company at a price that is fair relative to reported profit. What it could not do and never can: price court judgments, depreciation waves and the durability of a boom. Nobody can take that check off your hands — not even a thousand analysts who all thought the same thing. Now you have read both sides of the package. What you make of it is your decision. And that is exactly as it should be.

Sources

All original documents used in this analysis — to read for yourself:

- Alphabet Inc. — SEC annual report 10-K for the year 2025 (filed February 5, 2026)

- Alphabet Inc. — SEC annual report 10-K for the year 2024 (filed February 5, 2025)

- Alphabet Inc. — SEC quarterly report 10-Q as of March 31, 2026 (filed April 30, 2026)

- Alphabet Inc. — SEC quarterly report 10-Q as of September 30, 2025 (filed October 30, 2025)

- Alphabet Inc. — SEC quarterly report 10-Q as of June 30, 2025 (filed July 24, 2025)

- Alphabet Inc. — SEC quarterly report 10-Q as of March 31, 2025 (filed April 25, 2025)

- Alphabet's complete SEC filing history: EDGAR overview (sec.gov)

- Fundamental data (metrics, valuation, analyst consensus; data as of July 8, 2026), reconciled with the SEC filings.

- Screener and rating data: in-house stock scanner (data as of July 8, 2026; scanner membership checked live on July 14, 2026).

Transparency & disclaimer: This analysis is a journalistic contextualization of publicly available information and is not investment advice, not a financial analysis in the regulatory sense, and not a solicitation to buy or sell securities. Stock investments carry substantial risks up to total loss. All information without guarantee; the data cut-off is noted in the text in each case. The author holds no position in Alphabet stock at the time of publication.

Our Bottom Line at a Glance

- Market position & product positive

- Globally dominant attention platforms (Search, YouTube, Android) plus the fastest-growing segment, Google Cloud (+63 percent in the first quarter of 2026), with its own AI stack of Gemini models and TPU chips; the cloud order backlog of $467.6 billion is contractually underpinned (10-Q as of March 31, 2026).

- Earning power & balance sheet positive

- $402.8 billion in revenue and $132.2 billion in net income in 2025, $164.7 billion in operating cash flow, $126.8 billion in cash/securities and Altman-Z about 10 — plus $45.4 billion in buybacks in 2025 and a growing dividend ($0.22 per quarter since April 2026).

- Legal & regulatory risk negative

- More than 70 percent advertising share while the distribution model is being legally rebuilt: a Search final judgment with data-sharing obligations (both sides appealing), threatened structural remedies in the ad-tech business, a $3.5 billion EU fine, DMA proceedings — and $15.6 billion in short-term legal accruals (10-K 2025).

- AI capex & debt negative

- $91.4 billion in investments in 2025, "significantly more" for 2026; depreciation rising significantly per the company's own filing; notes sextupled to $79.1 billion within 15 months, plus data center and energy guarantees of roughly $37 billion plus about $15.3 billion newly added in April 2026 (10-K 2025; 10-Q as of March 31, 2026).

- Valuation & profit quality neutral

- A P/E of about 26 is fair for this quality, not a euphoria price (data as of July 8, 2026) — but the quarterly profit in early 2026 consisted of more than half unrealized valuation gains on stakes, and measured on free cash flow the stock costs about 57 times; insiders most recently reported 17 sells versus 3 buys.

Alphabet is the rare double of quality company and value-scanner hit: dominant platforms, a booming cloud with nearly half a trillion dollars in order backlog, a fortress balance sheet and a P/E of about 26 that is fair for this strength. Set against this are two open mega-bets no scanner can price: whether the most expensive investment wave in company history ($91.4 billion in capex in 2025, "significantly more" in 2026, fast-rising depreciation, sextupled note debt, billions in guarantees for third-party data centers) converts into real returns — and whether the courts merely file at the advertising foundation or cut deeper. The reported record profit moreover contains a growing paper share from valuation gains on stakes. Not investment advice.

What Our Rating Means

- If you don't own the stock

- At the current price level, we don't see a sufficient margin of safety for an entry.

- If you hold it in your portfolio

- Our findings offer no reason to sell.

A journalistic assessment by our editorial team at the time of the deep dive, based on public sources — not investment advice and not a solicitation to buy or sell. Your personal circumstances (investment goals, risk capacity, taxes) cannot be taken into account. What our categories mean, how verdicts are formed, and what conflicts of interest exist →

Worth Noting

- The analysis covers both listed share classes: GOOGL (Class A, voting) and GOOG (Class C, non-voting) represent the same economic interest in Alphabet; the unlisted Class B secures the founders 52.7 percent of the votes.

- The net income of the first quarter of 2026 ($62.6 billion) included $36.9 billion in unrealized book gains on non-marketable stakes; the operating income of $39.7 billion is the more reliable measure. The 2025 profit also included $24.1 billion in valuation gains.

- Price and valuation figures are dated to July 8, 2026 (about $344 per A share, about $4,194 billion in market value); analyses are evergreen, daily prices are not a buy argument.

- The scanner membership was checked twice: data as of July 8, 2026 (Greenblatt, Zweig, Buffett criteria) and a live check on July 14, 2026 (Greenblatt and Zweig confirmed; the Buffett criteria had meanwhile dropped out).

Frequently Asked Questions

Alphabet (Nasdaq: GOOGL/GOOG) is the holding company above Google. In 2025 the group generated $402.8 billion in revenue — more than 70 percent of it from online advertising (Google Search, YouTube, the ad network). Added to that are subscriptions, platforms and devices ($48.0 billion), Google Cloud ($58.7 billion, +36 percent) and bets on the future such as the robotaxi subsidiary Waymo.

Both are shares of the same company, Alphabet: GOOGL is the Class A share with one vote apiece, GOOG the Class C share without voting rights. Both participate identically in profit and dividend and trade at nearly the same price. The unlisted Class B (ten votes per share) sits almost entirely with the founders, who thereby control 52.7 percent of all votes.

Joel Greenblatt's Magic Formula hunts for companies with a high return on capital and a high earnings yield. Alphabet delivers both: about 36 percent operating margin, just under 39 percent return on equity and a price-to-earnings ratio of about 26 (data as of July 8, 2026). The formula's weakness: it prices neither antitrust risks nor the question of how much of the profit comes from book gains.

In the U.S. Search case a final judgment with distribution restrictions and data-sharing obligations was entered in December 2025; both sides appealed in early 2026. In the ad-tech case the U.S. Department of Justice demands structural remedies; the decision is pending. Added to that are an EU fine of 3.0 billion euros, two EU proceedings under the DMA, and obligations in Australia and Japan (10-K 2025).

In 2025 it was $91.4 billion — almost twice as much as in 2024 ($52.5 billion). For 2026 the annual report announces a significant increase; $35.7 billion flowed in the first quarter alone. In addition there are $149.1 billion in purchase commitments and $58.5 billion in future data center leases. Depreciation rose to $21.1 billion in 2025 and, per the filing, is expected to keep rising significantly.

The revenue backlog comprises contractually committed but not yet booked customer orders — at Alphabet overwhelmingly multi-year cloud contracts. It grew from $93.2 billion (end of 2024) via $242.8 billion (end of 2025) to $467.6 billion as of March 31, 2026. A good half is expected to be recognized as revenue within 24 months (10-Q as of March 31, 2026).

More than half from paper: $36.9 of the $62.6 billion were unrealized book gains on non-marketable equity stakes whose value was marked up after new funding rounds. Operationally, Alphabet genuinely earned $39.7 billion in the first quarter of 2026 — strong, but well below the headline number (10-Q as of March 31, 2026).

Measured by the price-to-earnings ratio of about 26, it is fairly valued for 15 percent growth and a 36 percent operating margin (data as of July 8, 2026). Two caveats: the profit contains a growing share of book gains, and measured on free cash flow — after $91.4 billion in investments — the market pays about 57 times. The stock is cheap only if the AI construction site pays a return.

Found an error?

Did you spot a factual error, an outdated number, or a typo in this deep dive? Let us know briefly — your report goes straight to the editorial team.