Micron Stock: $28 Billion in Profit in a Single Quarter — and the Old Rule That Cyclicals Look Cheapest at the Peak

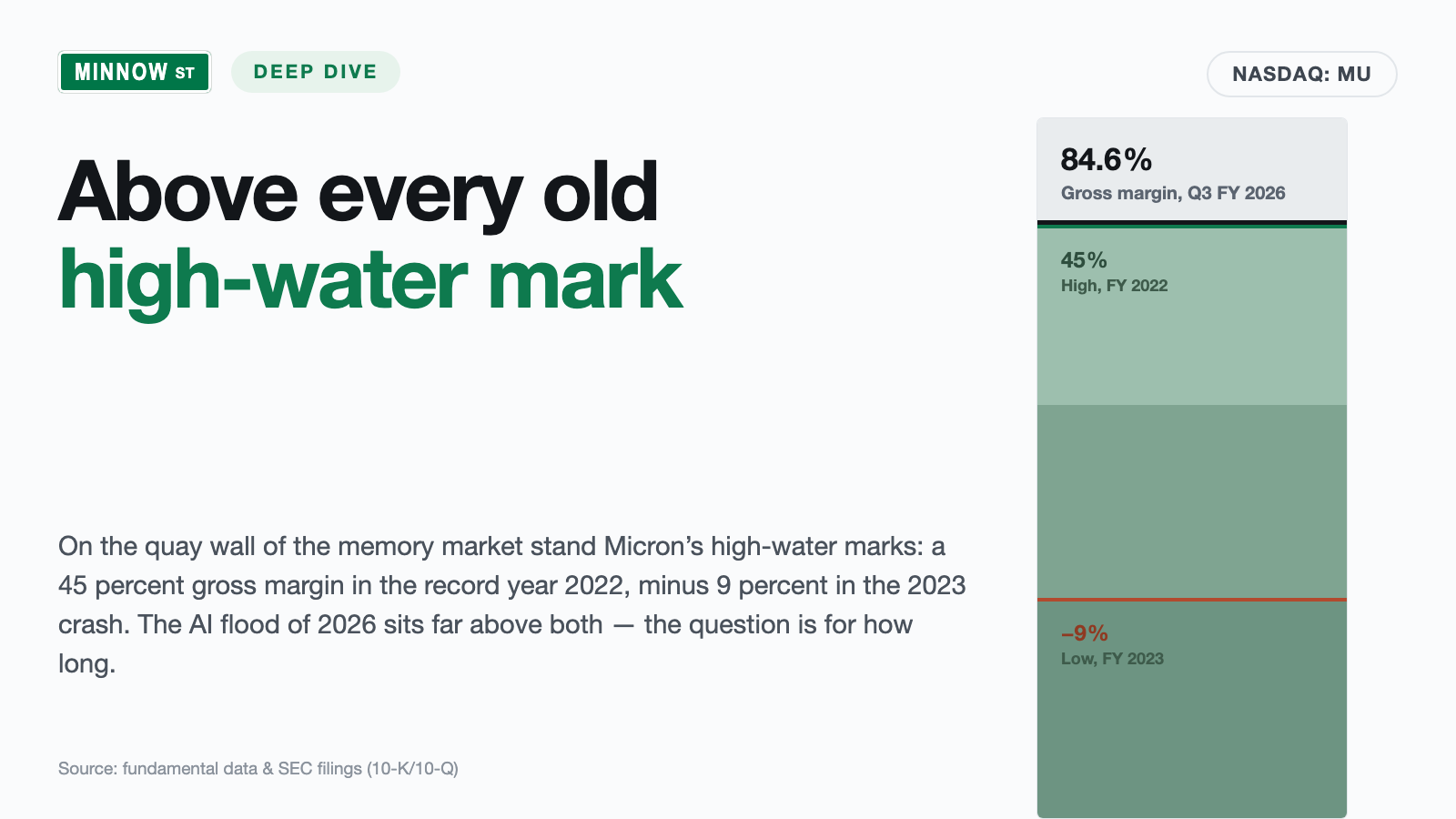

In the AI boom, memory-chip giant Micron earns more in one quarter than it previously did in its best full years: $41.5 billion in revenue, an 84.6 percent gross margin, $28.2 billion in net income (quarter ended May 28, 2026). Our value scanner for Joel Greenblatt's Magic Formula lights up — high return on capital, plenty of profit for the money. We read the annual report (10-K) and the quarterly reports (10-Q): they also say that memory prices have fallen by up to 50 percent a year within the past five years, that a single customer accounts for 17 percent of revenue — and that China partly banned Micron long ago. Not investment advice — just an attempt to tell a ruler from a roller coaster.

There is a tool every investor always carries and almost always uses wrong: the ruler in the head. You see three points climbing steeply, lay the ruler against them — and extend the line into the future. Psychologists call it extrapolation; on the stock market it usually goes by "this time it's different". In the summer of 2026, hardly any stock invites the mental ruler as much as Micron Technology (Nasdaq: MU), one of the world's three big memory-chip makers: $41.5 billion in revenue in a single quarter, $28.2 billion in net income, an 84.6 percent gross margin (quarter ended May 28, 2026) — numbers the semiconductor industry has never seen. And this time the impulse doesn't even come from a hot tip but from a serious tool: our in-house stock scanner for Joel Greenblatt's Magic Formula — a value filter, not a warning system — lists Micron among its hits. Quality at a fair price, says the formula. So let's make a deal: before you lay down the ruler, we read together what Micron itself reported to the U.S. securities regulator, the SEC — in the annual report (10-K, the yearly mandatory filing) and in the quarterly reports (10-Q). An SEC filing is honest under penalty of law. And this one contains a sentence about the past five years of memory prices that makes the ruler look rather old. In the end, you decide for yourself.

What Micron actually does

If the processor is a computer's brain, then Micron sells the memory: DRAM is the working memory — lightning-fast, but forgetful the moment the power goes; in fiscal year 2025 it stood for $28.6 of $37.4 billion in revenue, a good three quarters. NAND is the long-term memory — the storage cells in SSDs and smartphones that remember even without power ($8.5 billion in revenue). And then there is the product everything in the AI boom revolves around: HBM, "High-Bandwidth Memory" — DRAM chips stacked like a high-rise and mounted right next to the AI processor so the data doesn't have to commute. Every big AI accelerator needs this turbo memory, and only three companies in the world can build it at scale: Samsung, SK hynix — and Micron, the only one of them headquartered in the United States (Boise, Idaho, about 53,000 employees, plants from Taiwan via Singapore and Japan to Virginia).

So much for the story. Now the property that explains everything else in this analysis: memory chips — unlike processors — are largely commodity goods. A gigabyte of DRAM from Micron does the same as one from Samsung. Memory is the wheat harvest of the digital economy: the price is set not by the maker but by the balance of supply and demand — and because new fabs take years to build and then deliver all at once, that balance has swung in brutal cycles for decades. Remember this central tension, it is the connecting thread: Micron is living the best year of its history — and the market prices it as if this best year were the new normal. One important detail for all figures in this text: Micron has an offset fiscal year ending in late August/early September. "Fiscal year 2026" thus means: August 29, 2025 through September 3, 2026 — the third quarter of that fiscal year ended May 28, 2026.

Where the stock shows up in our scanner

Every day we run about 3,500 stocks through our scanners. Micron lights up in 6 scanners (data as of July 8, 2026) — and this time not a single warning scanner is among them. The most interesting hit is the Magic Formula of value investor Joel Greenblatt. His idea, in plain words: buy good companies at a fair price — measured by exactly two numbers. First, the return on capital: how much operating profit comes out per dollar of working capital employed? Second, the earnings yield: how much operating profit do I get per dollar of enterprise value? Micron currently shines in both disciplines — the EBIT margin of the last four quarters sits around 80 percent, which is why the stock simultaneously leads our EBIT-margin ranking. Add hits in the scanners "Quality Stocks", "Buffett criteria", "Martin Zweig: Growth with Reason" and the Levermann ranking. Six seals of quality at once — sounds like an open-and-shut case.

Before you reach for the ruler, you need to know the best-known weakness of this formula — Greenblatt himself never concealed it: with cyclicals, the Magic Formula preferentially fires at the earnings peak. The formula computes with the most recently reported profits. When a memory maker is collecting record prices, return on capital and earnings yield look fantastic — not because the company suddenly got better, but because the cycle stands at its top. When the cycle turns, both metrics vanish as fast as they came. A cyclical always looks cheapest at the peak. The remaining metrics carry the same double face: the Piotroski F-Score, a nine-point test of balance-sheet quality, stands at a solid 6 of 9 — okay, not outstanding. The Altman Z-Score, a classic early warning of insolvency, sits at a thoroughly healthy 11.7 (danger begins below 1.8) — insolvency really is not the issue here. And the relative strength of 99 says: hardly any stock in the market has run better over the last twelve months — plus 761 percent (data as of July 8, 2026). This is not an overlooked value gem. This is the star of the market, waved through by a value filter because of its record profits.

The numbers over the years — honestly appraised

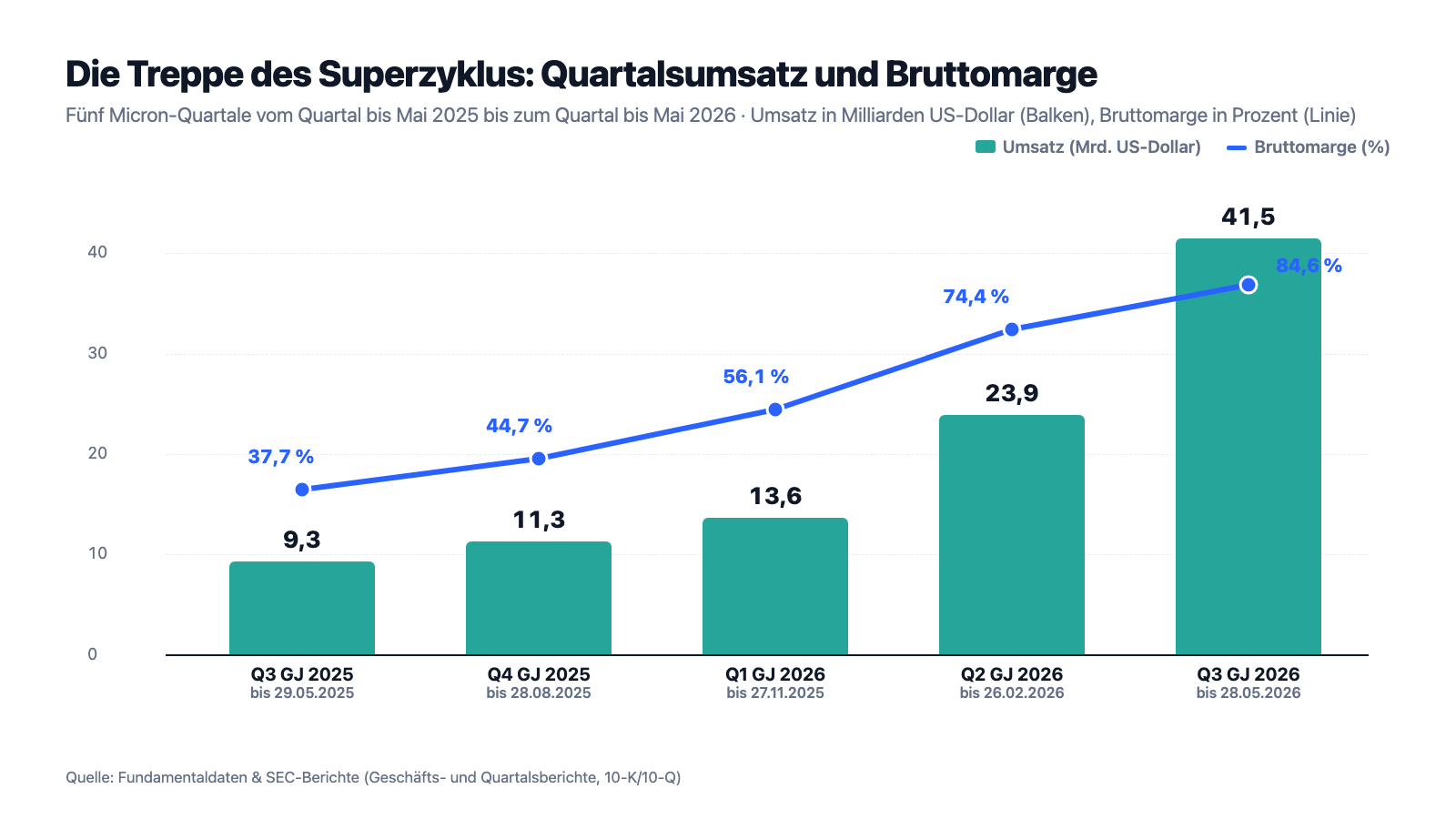

First, what genuinely impresses — and here that is a lot. The number series of fiscal year 2026 (which began August 29, 2025) reads like a rocket launch: revenue of $13.6 billion in the first quarter (through November 27, 2025), $23.9 billion in the second (through February 26, 2026), $41.5 billion in the third (through May 28, 2026) — plus 74 percent within a single quarter, plus 346 percent against the prior-year quarter. The gross margin climbed over the same span from 56.1 via 74.4 to 84.6 percent — for context: a software company would be content with that, and a chip manufacturer with its own fabs has historically simply never reached such levels. After nine months the books show $79.0 billion in revenue, $47.3 billion in net income and $45.7 billion in operating cash flow. The driver stands in the very first sentence of the quarterly report's management discussion: "AI-driven memory and storage growth is outpacing industry supply." The AI companies' data centers are buying faster than the industry can build; Micron is by now actively rationing the scarce goods ("supply allocation") and with the windfall has, in passing, repaid $9.4 billion of debt in nine months. What remains of the debt load: $5.7 billion — against $30.1 billion in cash and securities. Equity has grown from $54.2 to $100.7 billion since the end of August 2025 alone.

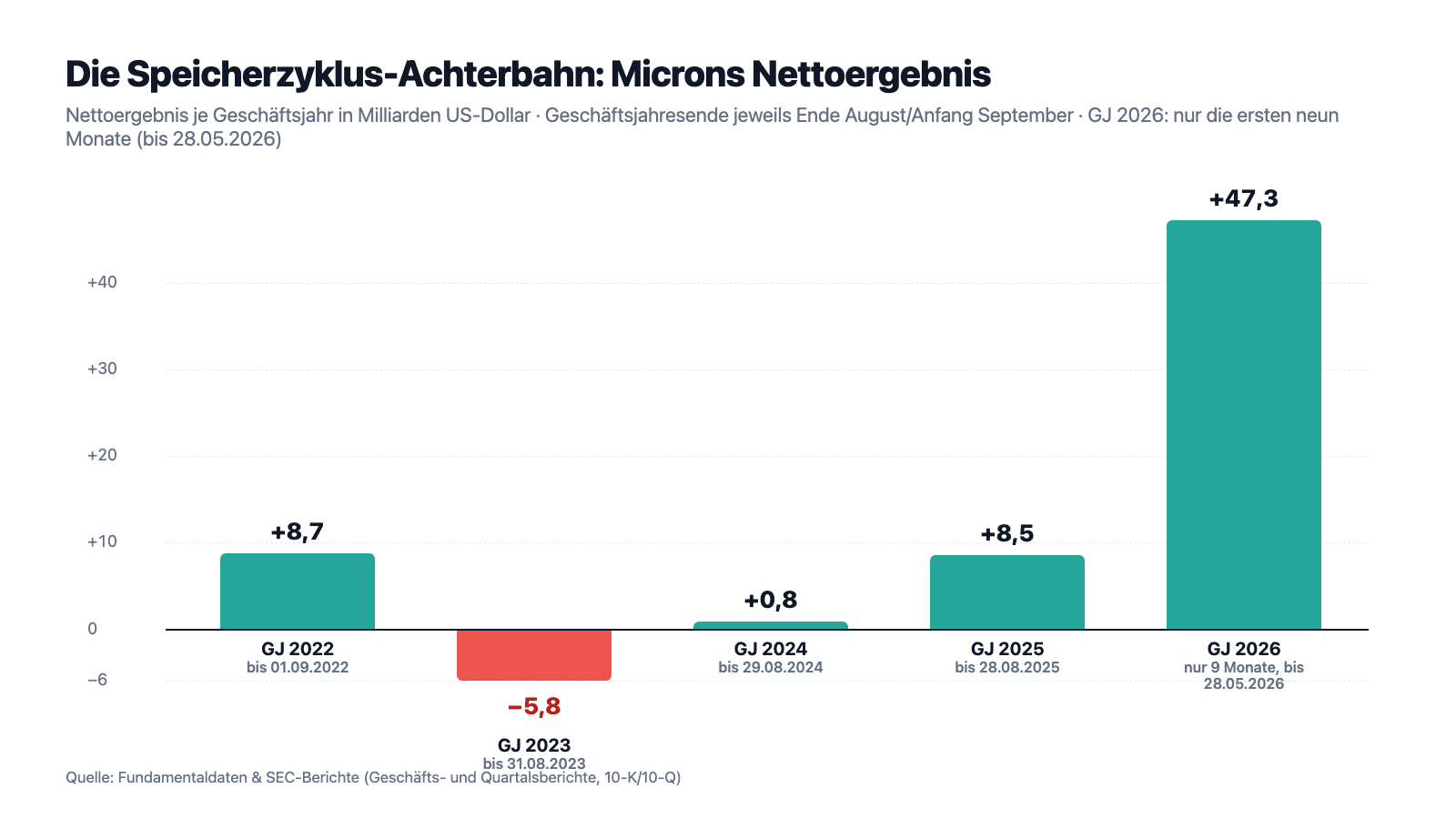

And now the same company, just three years earlier. Fiscal year 2023 (through August 31, 2023): revenue of $15.5 billion — a gross margin of minus 9 percent, meaning Micron sold its chips below manufacturing cost — and a net result of minus $5.8 billion. One year before that, in fiscal year 2022: $30.8 billion in revenue and $8.7 billion in profit. From record to loss and back, this market needed only twelve months each way. Exactly this roller coaster is what the next picture shows — and it is the reason why, with all respect for the 2026 numbers, we read the filings especially thoroughly:

What the filings say — the uncomfortable truths

Uncomfortable truth no. 1: it is a price boom, not a volume explosion — and the prices, per the company's own filing, are a roller coaster

Break the third quarter's 346 percent revenue jump into its parts, as the quarterly report itself does: in DRAM, selling prices rose about 260 percent, the volume sold only about 20 percent; in NAND, prices rose about 310 percent on a low-double-digit volume gain. Almost the entire boom thus sits in the price — the one variable Micron controls least. How little, the annual report describes in a paragraph you should have read before laying down the mental ruler:

"We have experienced significant volatility in our average selling prices and may continue to experience such volatility in the future. In the past five years, annual percentage changes in DRAM average selling prices have ranged from plus low 40% to a minus high 40% range. In the past five years, annual percentage changes in NAND average selling prices have ranged from plus low 30% to a minus low 50% range. In some prior periods, average selling prices for our products have been below our manufacturing costs and we may experience such circumstances in the future."

— Micron Technology, SEC annual report 10-K, fiscal year 2025, Item 1A "Risk Factors"

Add the second ingredient of every memory cycle: supply. The report names it soberly — Micron and its competitors are building new fabs and ramping up existing ones, and if worldwide supply grows faster than demand, it "could lead to declines in average selling prices". Exactly that script ran in 2022/2023: first record prices, then overcapacity, then a gross margin below zero. The AI demand is real, and it can stretch the cycle. But a commodity market remains a commodity market: growth that comes almost entirely from price can leave with the price.

Uncomfortable truth no. 2: "this time it's different" now stands verbatim in the mandatory filing — as a margin promise

And here it gets genuinely exciting, because in the latest quarterly report Micron claims, in effect, exactly that — with a construction this industry has never seen before: multi-year "take-or-pay" contracts with the big buyers. Take-or-pay means literally what it says: the customer commits bindingly to fixed volumes over several years — and if it doesn't take delivery, it has to pay anyway. Add price bands with floors and ceilings and, per the report, expected customer funds of $22 billion, about $18 billion of it as cash prepayments. The decisive sentence stands in the middle of the management discussion:

"Strategic customer agreements are structured as take-or-pay agreements, with binding commitments for specific volumes over the multi-year contract terms. Pricing for most agreements is either fixed, or is subject to minimum and maximum pricing. […] We expect gross margins from our strategic customer agreements with price bands, even at floor pricing levels, to yield gross margins well above our peak quarterly margins in any past cycle."

— Micron Technology, SEC quarterly report 10-Q as of May 28, 2026, Item 2 MD&A "Industry Conditions — Strategic Customer Agreements"

Be fair to both sides here. In favor: contracts like these are a structural break with memory history — the prior year's annual report still noted that customers were generally reluctant, given volatile industry conditions, to enter into long-term fixed-price contracts. If buyers are now prepaying billions and binding themselves for years, the fear of memory scarcity is evidently greater than the fear of overcapacity. Against: part of the contracts has no price bands at all, the ceilings are anchored to the market price of spring 2026 of all things — the highest in industry history —, and a promise about future margins is a management forecast, not a balance-sheet item. Industry history also knows a pattern: long-term contracts signed at the cycle peak tend to get renegotiated in the downturn — by precisely the big customers we are about to discuss. "This time it's different" has taken contract form here for the first time. Whether it holds will be decided exactly when it is needed: in the next downturn.

Uncomfortable truth no. 3: a single customer accounts for 17 percent of revenue — and a good part of the record still sits in the balance sheet as an unpaid bill

Who actually buys all these chips? The annual report answers that in two terse sentences — and they pack a punch:

"Revenue from one customer was 17% (primarily included in the CMBU segment) of total revenue for 2025. […] In each of the last three years, approximately one-half of our total revenue was from our top ten customers."

— Micron Technology, SEC annual report 10-K, fiscal year 2025, Note 28 "Certain Concentrations" and Item 1 "Business"

Customer concentration, translated: if your market stall makes half its revenue with ten regulars and a single one of them brings almost a fifth — how firm is your pricing power once that guest is less hungry? Micron's big customers are the hyperscalers and AI-chip companies, precisely the names whose data-center budgets carry the boom. They order in panic today because memory is scarce — the report speaks openly of Micron allocating the goods. But the same concentration works in reverse, too: a single throttled investment plan immediately hits a fifth of the business. And one more detail from the balance sheet as of May 28, 2026 belongs in this picture: trade receivables — revenue already booked that the customers have not yet paid — swelled within nine months from $7.2 to $26.9 billion, almost fourfold. With exploding revenue that is arithmetically normal (payment terms simply lag behind), but it also means: a substantial part of the record year exists so far as an open invoice to a handful of large customers. It becomes cash only if those customers are still liquid and willing next quarter, too.

Uncomfortable truth no. 4: China has partly banned Micron — and is breeding tomorrow's competition at the same time

The fourth truth is geopolitical, and it has stood in every Micron filing for three years. In May 2023, China's cyberspace regulator CAC decided after a "cybersecurity review" that operators of critical information infrastructure in China may no longer buy Micron products:

"Following the May 2023 decision of its cybersecurity review of our products sold in China, the CAC determined that critical information infrastructure operators in China may not purchase Micron products, impacting our revenue with companies headquartered in mainland China and Hong Kong, including direct sales as well as indirect sales through distributors."

— Micron Technology, SEC annual report 10-K, fiscal year 2025, Item 1A "Risk Factors"

The ban is only half the China story. The other half is called CXMT and YMTC — China's state-financed memory makers, which the annual report explicitly names as a growing threat: massive state capital, aggressive prices, growing market shares first in the home market. YMTC is by now fighting the conflict in court as well and is suing Micron for alleged patent infringement twice over — before a U.S. federal court in California and before the Beijing Intellectual Property Court, including a demand for sales bans in China. For the ruler in your head this means: today's supercycle lives on the fact that only three suppliers in the West can deliver. China's declared goal is that, in the long run, there will be more — with subsidies that never have to earn a return. That is not a 2026 problem. But memory fabs are built for decades — and so are stock valuations of $1.6 trillion.

Valuation: $1.58 trillion — the price of permanence

In early July 2026 the Micron stock cost about $1,214; at about 1.3 billion shares that makes a market value of about $1,576 billion — a good $1.5 trillion, more than forty times the market value of summer 2023 and a place in the top league of the world's exchanges (all valuation figures: data as of July 8, 2026). The exciting question is what you measure that price against. On the last four quarters, the price-to-earnings ratio sits around 26 — not even conspicuous for the most profitable phase in company history. Simply annualize the third quarter and it would be below 13. And the professionals' estimates (37 analysts, consensus on average "buy") see about $73 in earnings per share for the current fiscal year and about $149 for the next — that would be a price-to-earnings ratio of just over 8. You see the pattern: the further you extend the ruler, the cheaper the stock gets. The counter-test comes from the substance metrics: the price-to-sales ratio sits around 27 — the market pays $27 for every dollar of annual revenue — and the price-to-book ratio around 12.7. For context: measured against fiscal year 2023 revenue, the price-to-sales ratio would be about 100 — and even against the record revenue of about $79 billion from only nine months of fiscal year 2026 it stays high in the double digits for a company whose product is a commodity. To be fair: about $24 billion in net cash, ongoing share buybacks (a $10 billion program) and a small quarterly dividend of $0.15 cushion the picture; on top of that, up to $6.4 billion in CHIPS grants from the U.S. government flow into the new fabs. But the planned $27 billion of capital expenditures in fiscal year 2026 alone are a reminder of how this cycle ends when it ends: all three suppliers are currently building for all they are worth. How differently the market prices perfection, by the way, is something we already dissected at the chip-equipment maker KLA — and at memory neighbor Western Digital we showed how quickly a record profit can turn into a book-gain riddle.

Opportunities and risks at a glance

What speaks for Micron:

- Structural scarcity with a genuine tailwind: per the quarterly report, AI demand exceeds industry supply and Micron is actively allocating the goods; only three suppliers worldwide master HBM at scale, and Micron is the only one headquartered in the United States (10-Q as of May 28, 2026; 10-K, fiscal year 2025).

- Historic earning power: $41.5 billion in revenue and $28.2 billion in net income in the quarter ended May 28, 2026, an 84.6 percent gross margin, $45.7 billion in operating cash flow in nine months — and an EBIT-margin level (around 80 percent) that leads our ranking.

- Fortress balance sheet: $30.1 billion in cash and securities against $5.7 billion of debt (May 28, 2026), $9.4 billion repaid in nine months, equity of $100.7 billion, an Altman Z around 11.7 — plus up to $6.4 billion in CHIPS grants for the U.S. fabs.

- Contract security in the memory market for the first time: multi-year take-or-pay contracts with price floors and $22 billion in expected customer funds (about $18 billion as cash prepayments) — a structural break with the industry's previous logic.

- Six hits in value/quality scanners (Greenblatt, Buffett criteria, Quality Stocks, EBIT margin, Zweig, Levermann), Piotroski 6 of 9, fundamental rating A, 37 analysts on average at "buy" (data as of July 8, 2026).

What speaks against it:

- The boom is almost exclusively a price boom (DRAM prices +260 percent, volume +20 percent year over year in the third quarter) — and the company's own risk history cites price swings from plus 40 to minus a good 50 percent a year, at times below manufacturing cost (10-K, fiscal year 2025).

- The Magic Formula systematically rates cyclicals as "cheap" at the earnings peak: as recently as fiscal year 2023 the gross margin stood at minus 9 percent and the bottom line at minus $5.8 billion — the same market, three years earlier.

- The valuation prices in permanence: a market value of about $1,576 billion, a price-to-sales ratio around 27, price-to-book around 12.7, plus 761 percent in twelve months, daily swings around 7 percent — small doubts about the margin thesis produce large price moves (data as of July 8, 2026).

- Concentration and prepayment: one customer stood for 17 percent of fiscal year 2025 revenue, the top ten for about half; trade receivables swelled from $7.2 to $26.9 billion in nine months; $27 billion of capital expenditures in 2026 alone raise the stakes further.

- China twice over: a CAC purchase ban for critical infrastructure since May 2023, state-financed rivals CXMT/YMTC with aggressive prices — and YMTC patent suits in Beijing and California including demanded sales bans (10-K, fiscal year 2025; 10-Q as of May 28, 2026).

A human conclusion

Back to the ruler in the head. The mean thing about it: it never feels like speculation, it feels like mathematics — three points, one line, done. Micron is the stress test for that feeling, in both directions. Whoever buys today extends the line of the last three quarters and gets real arguments for it: signed take-or-pay contracts, $22 billion in customer money, net cash, a product without which no AI data center runs. Whoever waves it off simply lays the ruler down earlier — against fiscal year 2023, with a gross margin below zero and a $5.8 billion loss — and extends that line instead. Both are using the same tool. That is exactly why the roller coaster was the most honest picture of this analysis: with a cyclical, every straight line is a bet on where on the curve you happen to be sitting. The Greenblatt scanner did its job — it found a highly profitable company at a price that is moderate relative to the current profit. What it cannot do and never could: say whether this profit is a new plateau or the top of the track. That answer is in no scanner and in no filing — it hangs on whether AI has truly turned memory from a commodity into a contract good. The filings hand you both halves of the truth; which one you give more weight is your decision. And that is exactly as it should be.

Sources

All original documents used in this analysis — to read for yourself:

- Micron Technology — SEC annual report 10-K for fiscal year 2025 (ended August 28, 2025; filed October 3, 2025)

- Micron Technology — SEC annual report 10-K for fiscal year 2024 (ended August 29, 2024; filed October 4, 2024)

- Micron Technology — SEC quarterly report 10-Q as of May 28, 2026 (filed June 25, 2026)

- Micron Technology — SEC quarterly report 10-Q as of February 26, 2026 (filed March 19, 2026)

- Micron Technology — SEC quarterly report 10-Q as of November 27, 2025 (filed December 18, 2025)

- Micron Technology — SEC quarterly report 10-Q as of May 29, 2025 (filed June 26, 2025)

- Micron's complete SEC filing history: EDGAR overview (sec.gov)

- Fundamental data (metrics, quarterly series, valuation; data as of July 8, 2026), reconciled with the SEC filings.

- Screener and rating data: in-house stock scanner (data as of July 8, 2026; scanner membership checked live on July 14, 2026).

Transparency & disclaimer: This analysis is a journalistic contextualization of publicly available information and is not investment advice, not a financial analysis in the regulatory sense, and not a solicitation to buy or sell securities. Stock investments carry substantial risks up to total loss. All information without guarantee; the data cut-off is noted in the text in each case. The author holds no position in Micron stock at the time of publication.

Our Bottom Line at a Glance

- Market position & product positive

- One of only three manufacturers worldwide able to build HBM high-performance memory for AI accelerators at scale — and the only one headquartered in the United States. Per the quarterly report, AI demand exceeds industry supply; Micron is actively allocating the scarce goods (10-Q as of May 28, 2026).

- Earning power & balance sheet positive

- $41.5 billion in revenue and $28.2 billion in net income in the quarter ended May 28, 2026 (an 84.6 percent gross margin), $45.7 billion in operating cash flow in nine months; $30.1 billion in cash/securities against $5.7 billion of debt, equity of $100.7 billion, an Altman Z around 11.7.

- Cyclicality & price dependence negative

- The boom is almost entirely a price boom (DRAM prices +260 percent, volume +20 percent year over year in the third quarter of FY 2026). The company's own five-year history in the 10-K cites price swings down to minus a good 50 percent a year, at times below manufacturing cost; in FY 2023 the gross margin was negative.

- Valuation & expectations negative

- A market value of about $1,576 billion, a price-to-sales ratio around 27, price-to-book around 12.7, plus 761 percent in twelve months (data as of July 8, 2026): the price presumes that the best margins in industry history become the permanent state. An optically moderate P/E is, with cyclicals at the peak, the Magic Formula's classic trap.

- Contracts & customer structure neutral

- Multi-year take-or-pay contracts with price floors and $22 billion in committed customer funds are a genuine structural break — but one customer stood for 17 percent of FY 2025 revenue, the top ten for half, trade receivables swelled to $26.9 billion in nine months, and China remains a double risk (the CAC ban, state-financed rivals CXMT/YMTC complete with patent suits).

Micron is the opposite of a warning-scanner case: a world-class cyclical in record form, with a fortress balance sheet, a genuine scarcity position in the AI boom and, for the first time, contractually secured volumes. But the stock is valued at about $1.58 trillion — 27 times revenue and 12.7 times book value — as if the best quarter in industry history were the new normal. Exactly that permanence is unproven: the boom sits almost entirely in prices whose own five-year history includes crashes by half. The value scanner did its math correctly — whether it did the math at the peak, only the cycle knows. Not investment advice.

What Our Rating Means

- If you don't own the stock

- As long as the question raised in the bottom line stays open, we see no basis for an entry.

- If you hold it in your portfolio

- Our findings offer no acute reason to sell — the checkpoints named remain decisive.

A journalistic assessment by our editorial team at the time of the deep dive, based on public sources — not investment advice and not a solicitation to buy or sell. Your personal circumstances (investment goals, risk capacity, taxes) cannot be taken into account. What our categories mean, how verdicts are formed, and what conflicts of interest exist →

Worth Noting

- Micron reports in an offset fiscal year (ending late August/early September); "FY 2026" denotes the period from August 29, 2025 through September 3, 2026, and the nine-month figures end on May 28, 2026. Every period in the text is explicitly dated.

- The $47.3 billion of FY 2026 net income is a nine-month figure, not a full-year figure; the comparison with the prior full years in the roller-coaster chart is labeled accordingly.

- Price and valuation figures are dated July 8, 2026 (about $1,214 per share, about $1,576 billion in market value); analyses are evergreen, daily prices are not a buy argument.

- Analyst estimates (about $73 and $149 in earnings per share for the current and the next fiscal year) are consensus forecasts of 37 professionals, not facts — with cyclicals, estimates have historically been revised hardest at turning points.

Frequently Asked Questions

Micron (Nasdaq: MU) of Boise, Idaho, is one of the world's three big memory-chip makers. The company builds DRAM (working memory, a good three quarters of revenue), NAND (data storage for SSDs and smartphones) and HBM — stacked high-performance memory for AI accelerators. In fiscal year 2025 (ended August 28, 2025) Micron posted $37.4 billion in revenue; in the quarter ended May 28, 2026 alone it was $41.5 billion.

Joel Greenblatt's Magic Formula looks for companies with a high return on capital and a high earnings yield — that is, lots of operating profit per dollar of capital employed and per dollar of enterprise value. Micron's record profits in the AI boom (an EBIT margin around 80 percent) satisfy both criteria. The formula's known weakness: with cyclicals it preferentially fires at the earnings peak, because it treats current profits as a permanent state.

HBM ("High-Bandwidth Memory") consists of DRAM chips that are stacked on top of each other and mounted directly next to the processor. That delivers extreme data bandwidth at low power consumption — exactly what AI accelerators in data centers need. Per the annual report, HBM is ideally suited to AI applications; only Samsung, SK hynix and Micron master its production at scale.

Extremely: per Micron's own annual report, DRAM selling prices swung between roughly plus 40 and minus close to 50 percent a year over the past five years, at times sitting below manufacturing cost. In fiscal year 2023 the gross margin was negative at minus 9 percent and the bottom line stood at minus $5.8 billion — three years before the record quarter with an 84.6 percent gross margin.

Since 2026 Micron has been signing multi-year supply contracts in which customers must take fixed volumes bindingly — or pay anyway ("take or pay"). Most carry fixed prices or price bands with floors and ceilings; Micron expects $22 billion in customer funds from them (about $18 billion as cash prepayments) and gross margins that even at the lower price band are supposed to sit above all previous cycle peaks (quarterly report 10-Q as of May 28, 2026).

That depends on the yardstick: the price-to-earnings ratio sits around 26 on the basis of the last four quarters and would fall sharply if the record profits persisted; the price-to-sales ratio of about 27 and the price-to-book ratio of about 12.7, by contrast, already price in that the best margins in industry history become the permanent state (data as of July 8, 2026). With a cyclical, a low P/E at the peak is no proof of a bargain.

A double risk role: since May 2023, operators of critical information infrastructure in China may not buy Micron products (a CAC decision). At the same time China is building up state-financed memory makers in CXMT and YMTC, which per the annual report aim to win market share with aggressive prices — and YMTC is suing Micron over patents in Beijing and California, including demanded sales bans.

Micron has an offset fiscal year that ends in late August/early September. "Fiscal year 2026" runs from August 29, 2025 through September 3, 2026; the third quarter ended May 28, 2026. When comparing with the calendar-year figures of other chip companies you have to keep this shift in mind — which is why every period in this analysis is explicitly dated.

Found an error?

Did you spot a factual error, an outdated number, or a typo in this deep dive? Let us know briefly — your report goes straight to the editorial team.