Deckers Stock: HOKA and UGG Deliver a Record Year — and the Stock Still Hangs on the Clearance Rack

Deckers Outdoor earned more than a billion dollars for the first time in fiscal year 2026 (through March 31) — carried by exactly two brands: HOKA and UGG account for 97.3 percent of revenue. At the same time the stock trades more than half below its early-2025 high, and no fewer than three of our value scanners light up, first among them Joel Greenblatt's Magic Formula. We ran the cross-check — in the annual report (10-K) and the quarterly reports (10-Q): this time the value label is genuine. But the original also shows what the red price tag conceals: a U.S. market that has practically stalled, a HOKA growth staircase that leads downward, and tariffs gnawing at the margin. Not investment advice — just a fitting at the original document before the clearance-sale reflex grabs hold.

There is a color signal that takes a shortcut in our heads: the red price tag. A pair of shoes, $200 yesterday, $100 today — and the mind celebrates the hundred saved instead of asking the only question that counts: are the shoes worth $100? Psychologists call this the anchoring effect: the old price is the anchor, everything below it feels like a gift — yet the anchor only tells you what something used to cost, not what it is worth. On the stock market, that red tag currently hangs, of all places, on a company that earns its money with shoes: Deckers Outdoor (NYSE: DECK), the group behind the running-shoe brand HOKA and the sheepskin icon UGG. The stock trades more than half below its early-2025 high — and no fewer than three of our value scanners light up, first among them Joel Greenblatt's Magic Formula. So let's make a deal: before the clearance-sale reflex grabs hold, we do the fitting together — in the annual report (10-K, the yearly mandatory filing to the U.S. securities regulator SEC) and in the quarterly reports (10-Q). An SEC filing is honest under penalty of law. And this fitting yields both: a value label that this time is genuinely real — and three reasons why the market still refuses to believe it. In the end, you decide for yourself.

What Deckers actually does

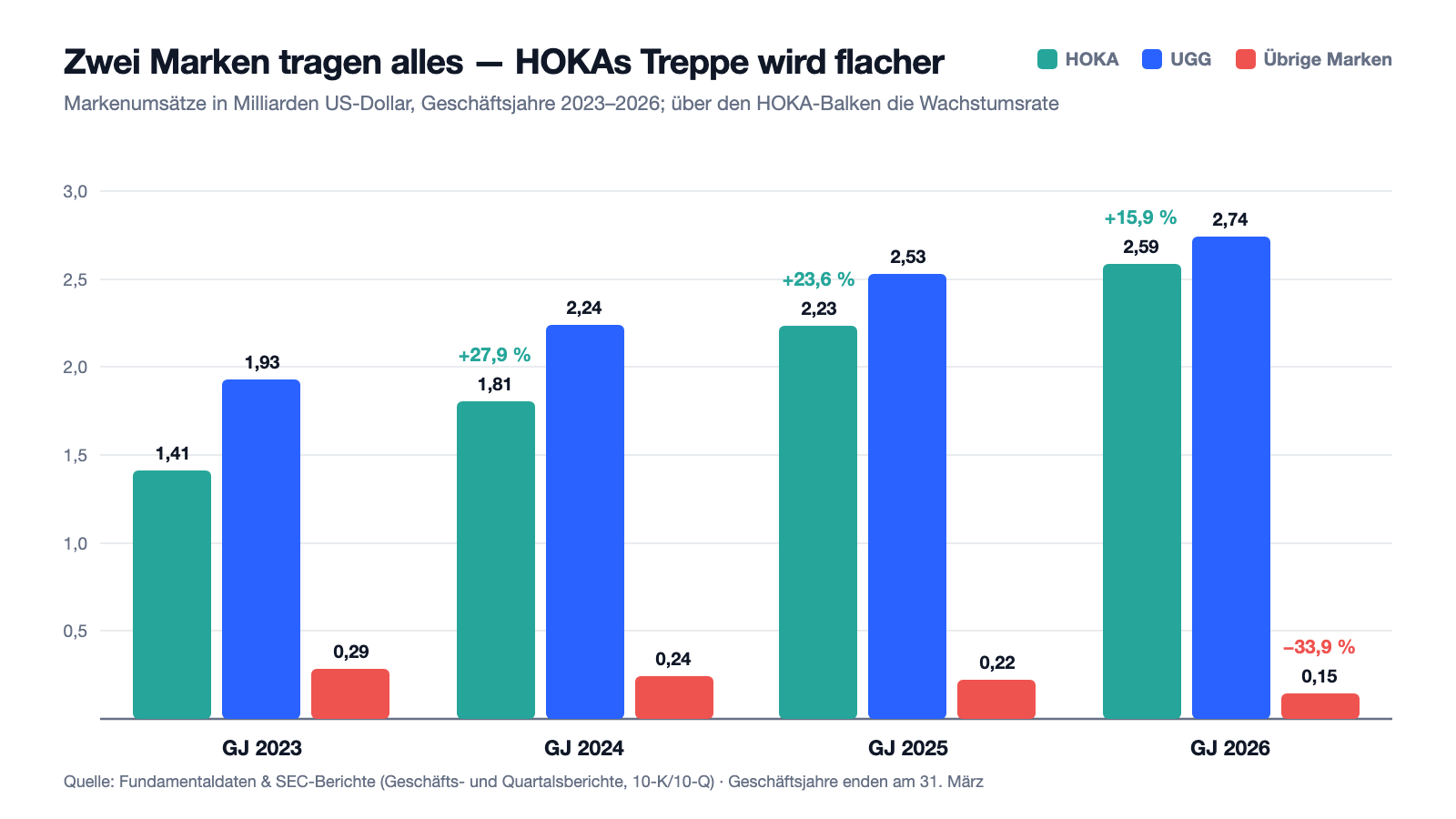

Deckers of Goleta, California, owns not a single factory. The group designs and markets shoes, has them made by independent manufacturers in Southeast Asia and sells them through two channels: wholesale (sporting-goods retailers, department stores, international distributors — 59 percent of revenue) and directly to end customers (its own stores and online shops, "DTC" for direct-to-consumer in filing jargon — 41 percent). About 6,000 employees, of whom roughly 2,200 work in its own stores, listed on the New York Stock Exchange since 1993. The business is carried by two very different brands: HOKA, the running-shoe brand with the strikingly thick cushioning soles that went from ultramarathon niche product to outfitter of everyday runners and posted $2.59 billion in revenue in fiscal year 2026. And UGG, the boot brand with the Australian sheepskin, born on the Californian surf coast, sometimes a fashion wave, sometimes a perennial — at $2.74 billion still the larger of the two. Together that is 97.3 percent of group revenue. The rest — the outdoor sandal brand Teva and two mini-brands — is shrinking: Sanuk was sold in 2024, Koolaburra and AHNU were wound down as standalone brands in fiscal year 2026.

One peculiarity up front, so no number slips: Deckers has an offset fiscal year ending on March 31. "Fiscal year 2026" therefore means April 2025 through March 2026 — the holiday season falls in the third quarter. And note the central tension of this analysis, it runs through every chapter: a two-brand group in record form, debt-free, with a genuine value signal — but the home market stands still, the growth staircase of the locomotive HOKA leads downward, and fashion as well as tariff policy can shake exactly the two pillars that carry everything.

Where the stock shows up in our scanner — and what the cross-check says

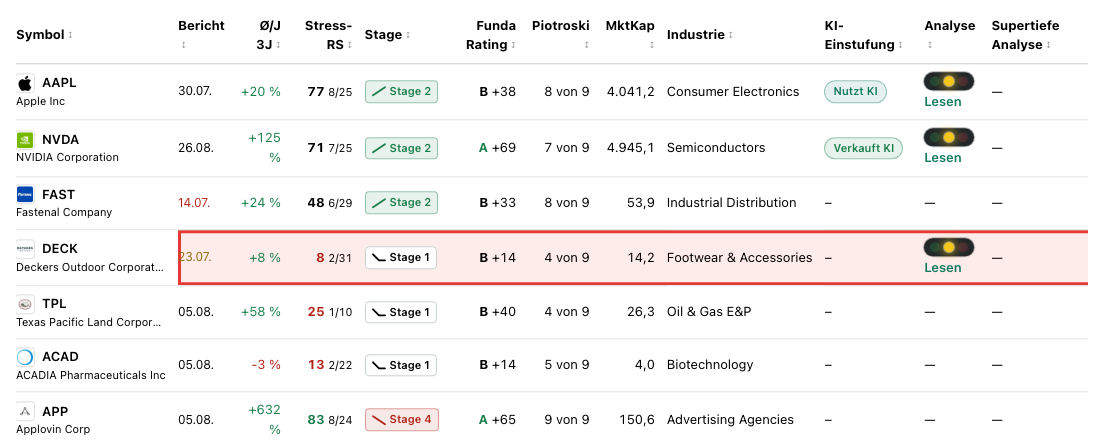

Every day we run about 3,500 stocks through our scanners. Deckers lights up in three scanners (data as of July 8, 2026) — and all three are value or quality scanners: the Magic Formula of value investor Joel Greenblatt (membership confirmed live on July 14, 2026), the point system of Susan Levermann with 4 points — exactly the buy threshold for large caps — and Buffett's owner-earnings yield, which alongside quality demands that free cash flow yield at least 5 percent of the purchase price. Greenblatt's idea in one sentence: buy good companies (high return on capital — how much profit per dollar of capital employed?) at fair prices (a reasonable price-to-earnings ratio). Our screener version approximates the return on capital as return on equity times equity ratio and demands at least 25 percent.

After our recent experiences with this formula, the cross-check is mandatory: at the memory-chip cyclical Micron it lit up right at the earnings peak, and at the river-barge operator Kirby the signal turned out to be a data error. So we redo the math with Deckers' real balance-sheet figures (10-K, balance sheet as of March 31, 2026): net income of $1,024.1 million on $2,499.6 million of equity yields a return on equity of about 41 percent. Equity of $2,499.6 million against total assets of $3,687.8 million yields an equity ratio of 67.8 percent. Multiplied: a return-on-capital approximation of about 27.8 percent — above the 25 percent threshold. The price-to-earnings ratio sits around 15. This time the math holds. Deckers really does earn extraordinary amounts of money on little tied-up capital — no wonder for a group that owns no factories and whose balance sheet is half cash.

And yet honesty includes the other half of the scanner fingerprint: not a single trend or momentum signal. The stock sits in Stage 1 (the basing phase after a downtrend in the Weinstein model), the relative strength of 34 says: it has run weaker than two thirds of the market. At the data cut-off the price sat a good 52 percent below the all-time high of early 2025 and 12 percent below its 200-day average. The Piotroski F-Score, a nine-point test of balance-sheet quality, stands at a meager 4 of 9 — above all because margins and revenue momentum recently faded. The EPS rating of 29 and the fundamental rating B with 14 of 100 points place the earnings momentum at the bottom — not the earnings level. The honest finding: the scanners say "cheap and highly profitable", the price board says "shunned". Exactly this gap is what the rest of the analysis has to explain.

The numbers over the years — honestly appraised

First, what genuinely impresses — and that is quite a lot. Deckers has delivered four record years in a row: revenue rose from $3.63 billion (fiscal year 2023) via $4.29 and $4.99 to $5.47 billion (fiscal year 2026). Net income climbed over the same period from $516.8 via $759.6 and $966.1 million to $1,024.1 million — above the billion for the first time. Earnings per share more than doubled: from $3.23 to $7.02 (all figures adjusted for the one-for-six stock split of September 2024), thanks also to buybacks that shrink the share count year after year. The gross margin — what remains of the selling price after pure product costs — stands at 57.7 percent: of every shoe dollar, almost 58 cents remain for marketing, stores and profit. The operating margin: 23.1 percent. And the balance sheet is the kind that bores auditors: $1.91 billion in cash, zero drawn bank loans (the $400 million credit line is untouched), inventories at $487 million even slightly below the prior year, goodwill of only $14 million — nothing here has been bought pretty. Operating cash flow: $1.18 billion, on modest capital expenditures of about $85 million. That is the substance behind the Greenblatt signal.

Where does the run come from? From both brands — but with fading momentum. HOKA grew 15.9 percent in fiscal year 2026 to $2.59 billion: strong, but the staircase leads downward — plus 27.9 percent (2024), plus 23.6 (2025), plus 15.9 (2026). UGG added 8.2 percent to $2.74 billion, after 13.1 percent the year before; in the decisive holiday quarter (October through December 2025) it was only plus 4.9 percent. Also striking is where the growth comes from: wholesale grew at 12.3 percent, twice as fast as the direct business (plus 6.3 percent) — even though the group's declared long-term goal is actually the opposite, since direct selling brings the higher margins. On a comparable basis the direct business grew only 4.6 percent. And the volume picture: 78.7 million units sold, plus 6.2 percent — the rest of the revenue gain came from price increases and product mix. The running interim report card, the quarterly report as of December 31, 2025, confirms both: a solid plus 7.1 percent in revenue and plus 11 percent in earnings per share for the quarter — but a gross margin that gave up half a percentage point because of tariffs.

What the filings say — the uncomfortable truths

Uncomfortable truth no. 1: two brands carry 97 percent — and their boss is named fashion

Deckers calls itself a brand portfolio, but the arithmetic is a cluster: HOKA and UGG stand for 97.3 percent of revenue, and the rest shrank 33.9 percent in fiscal year 2026 — Sanuk sold, Koolaburra and AHNU wound down, Teva in restructuring. What this concentrate means when taste turns is described by the annual report itself — soberly and without embellishment:

"The footwear, apparel, and accessories industry is subject to rapid changes in consumer preferences and fashion tastes, which makes it difficult to anticipate demand for our products and forecast our results of operations. Our success depends, in part, on brand loyalty, and there can be no assurance that consumers will continue to prefer our brands. […] New products may not achieve market acceptance, including due to pricing that consumers are unwilling to bear, or our brands may fall out of favor, which could impede our ability to maintain or grow sales, adversely affect brand perception, and negatively impact our results of operations."

— Deckers Outdoor, SEC annual report 10-K, fiscal year 2026, Item 1A "Risk Factors"

Why this is more than lawyerly caution is shown by the company's own history: in the mid-2000s UGG was already the fashion wave once — and afterwards, for years, the cautionary tale of one that had ebbed away. Today's UGG renaissance is real, but it is a fashion phenomenon with an expiry date of unknown length. And HOKA competes in a market where — per the report — contract manufacturing has lowered the barriers to entry and financially stronger competitors are deliberately attacking its very categories. A group that hangs practically entirely on two questions of taste deserves a valuation discount against a genuine portfolio — the only question is how large it has to be. Remember: with fashion stocks, the brand is the moat — and moats made of zeitgeist have ebb and flow.

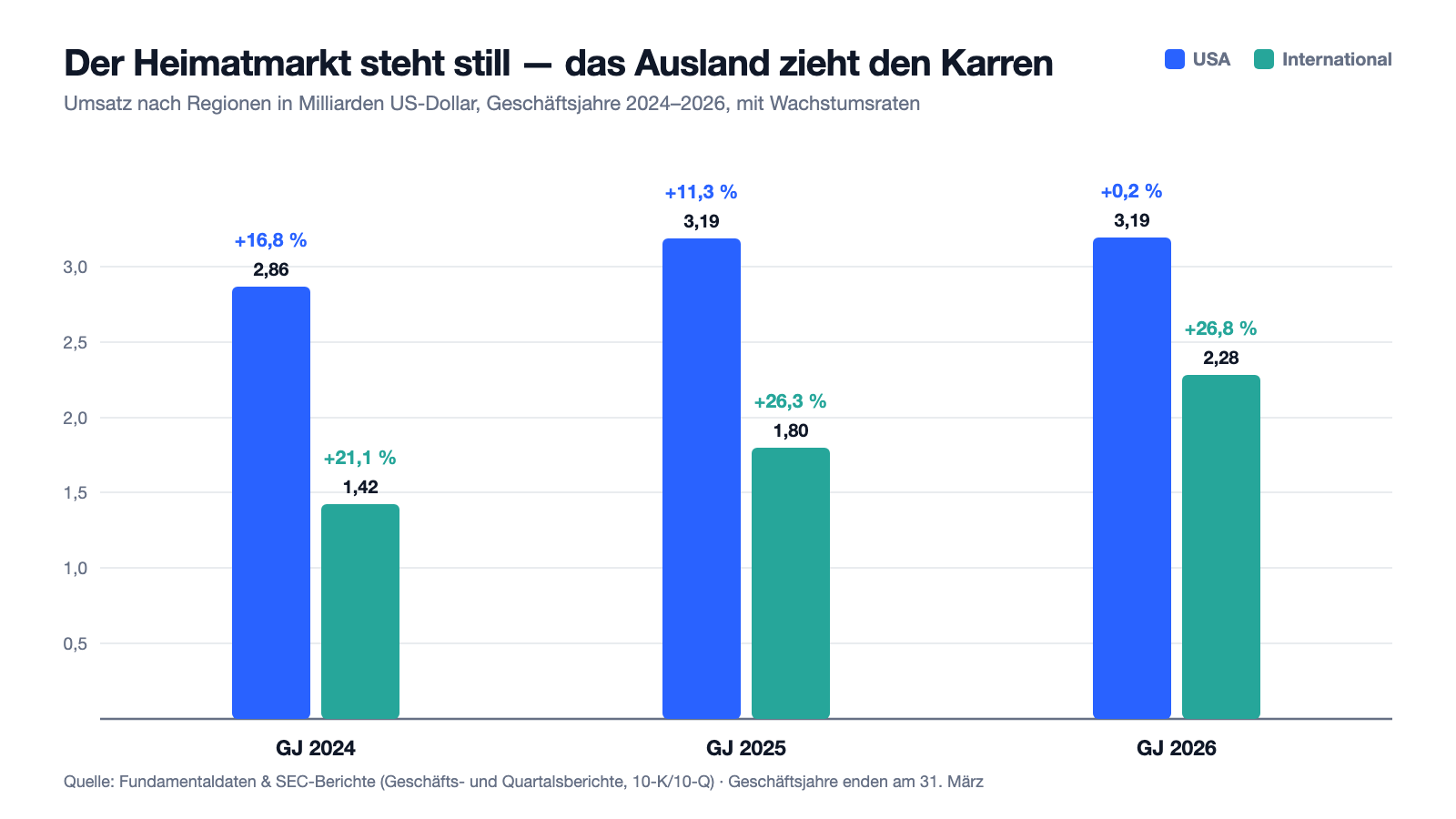

Uncomfortable truth no. 2: the home market has braked to zero — all the growth comes from outside

The most striking number of fiscal year 2026 hides in an inconspicuous enumeration in the management report:

"Domestic net sales increased 0.2% to $3,191,518. International net sales increased 26.8% to $2,280,778."

— Deckers Outdoor, SEC annual report 10-K, fiscal year 2026, Item 7 MD&A "Financial Highlights"

The filing counts in thousands of dollars — so about $3.19 billion domestic and $2.28 billion international. In plain terms: in the United States — still 58 percent of the business — Deckers gained practically not one dollar of revenue in the past fiscal year. Just two years earlier the home market grew 16.8 percent, then 11.3 — now 0.2. All of the group's growth came from abroad, where HOKA and UGG are expanding and a weaker dollar helped on top (currency-adjusted, the group grew 9.0 instead of 9.8 percent). You can tell this story two ways: optimistically — the international expansion is working, and abroad still has years of catch-up potential. Or cautiously — in the most mature market, where both brands have been present longest, saturation has been reached, and HOKA's growth staircase (27.9 via 23.6 to 15.9 percent) shows what it looks like when a growth brand grows up. Both readings stand in the same report. Only one thing is certain: abroad now has to deliver every year what the home market no longer yields — and exchange rates, tariffs and local competition all have a say there.

Uncomfortable truth no. 3: almost every shoe comes from Vietnam or Indonesia — and tariff policy is a lucky bag with court cases attached

Deckers manufactures nothing itself: independent producers make the goods, in fiscal year 2026 "predominantly from Vietnam and Indonesia" — less than 5 percent from China or any other single country. This concentration met a U.S. tariff policy changing by the week in 2025 — with real consequences: the gross margin gave up 20 basis points despite price increases and cost-sharing with suppliers, "driven by tariffs", as the report comments on the segment accounts. And then comes the passage that makes this reporting season special:

"We are exposed to risks from evolving trade policies, including higher tariffs and restrictions affecting goods imported from certain regions where we have a concentration of sourcing and manufacturing. Recent judicial, regulatory, and administrative developments regarding tariffs imposed under the International Emergency Economic Powers Act and other authorities have increased uncertainty related to both our future duty costs and potential recovery of previously paid duties. […] As of March 31, 2026, we have not recognized any amounts related to potential tariff refunds or other recoveries."

— Deckers Outdoor, SEC annual report 10-K, fiscal year 2026, Item 7 MD&A "Trends and Uncertainties"

The background, in the risk chapter of the same report: the U.S. Supreme Court has declared invalid certain tariffs based on the emergency statute IEEPA, and the customs authority has announced a refund process — but whether, when and how much Deckers gets back is open, and nothing is booked. That is honest accounting and at the same time a symbol of how plannable this cost block is: a group that imports practically all of its goods is currently calculating with tariffs whose legal basis is being litigated in court and which tomorrow may be higher, lower or called something else. The report warns accordingly that the margin protection of the past year — price increases, cost-sharing, sourcing management — may not be repeatable in fiscal year 2027. For a business model whose 57.7 percent gross margin is the crown jewel, that is no footnote.

Uncomfortable truth no. 4: the raw material of half the company runs through two tanneries

Looking into the supply chain, the cluster gets even tighter. The sheepskin that makes up a substantial part of the UGG products — the brand with $2.74 billion in revenue, roughly half the group — takes a remarkably narrow path:

"We purchase raw materials and components that are subject to supplier and geographic concentration, most significantly sheepskin, which is used in a substantial portion of our UGG brand products. Sheepskin is in high demand and sourced primarily from Australia and processed largely by two tanneries in China capable of meeting our quality, volume, and animal welfare standards. This geographic and supplier concentration exposes us to supply disruption risk."

— Deckers Outdoor, SEC annual report 10-K, fiscal year 2026, Item 1A "Risk Factors"

Customer concentration would be the classic worry — Deckers doesn't have it, not a single buyer accounts for 10 percent of revenue. But here it is raw-material concentration: if one of the two tanneries failed — technically, politically, or because a trade conflict escalates — half the group would face a sourcing problem for which, per the report, replacements are not freely available. Add a quieter time bomb in the same chapter: growing resistance to animal-derived materials and possible sales bans in individual markets — "Because sheepskin is integral to the UGG brand", Deckers writes, changed consumer preferences or regulations around sheepskin could materially impair the business. Translated: the material that makes UGG unmistakable is at the same time its regulatory and societal risk. A company can replace many suppliers — its identity it cannot.

Valuation: $14 billion for the two-brand cash box

In early July 2026 the Deckers stock cost about $103; that makes a market value of about $14.2 billion (all valuation figures: data as of July 8, 2026). Measured against the profit of the last four quarters, that is a price-to-earnings ratio of about 15 — for a company with a 41 percent return on equity, a 57.7 percent gross margin and net cash, that is cheap both historically and against the market; the broad U.S. market cost a multiple of that at the same time. Subtract the $1.9 billion of cash from the market value and you pay only about twelve times annual earnings for the operating business. The price-to-book ratio of about 5.7 looks high next to that, but it is mostly buyback math: Deckers consistently pays out its equity to shareholders — in fiscal year 2026, $1.08 billion flowed into its own shares (10.5 million of them at an average of $102.43), more than the year's profit, which is why equity fell slightly despite the record profit. Price-to-sales ratio: about 2.6. Price to free cash flow: about 12. The analysts (24 professionals, consensus "buy") expect $7.49 in earnings per share for fiscal year 2027 and $8.33 for 2028 — that would be P/Es of about 14 and 12. Add the shareholder policy: no dividend since the 1993 IPO, but the buyback authorization was topped up on May 20, 2026 by $3.5 billion to about $4.84 billion — enough, at current prices, to retire arithmetically a third of all shares. One bitter drop belongs to honesty: in fiscal year 2025 Deckers bought back at an average of $149.21 — near the high, 45 percent above the July 2026 price. Fairly summed up: the valuation does not price in a continuation of records, it prices in stagnation — that is the market's opportunity and its warning at once.

Opportunities and risks at a glance

What speaks for Deckers:

- Two strong brands with genuine pricing power: 57.7 percent gross margin, 23.1 percent operating margin, earnings per share more than doubled since fiscal year 2023 from $3.23 to $7.02 (10-K, fiscal year 2026).

- Fortress balance sheet: $1.91 billion in cash, no drawn bank loans, inventories below the prior year, goodwill of only $14 million — plus $1.18 billion in operating cash flow on about $85 million of capital expenditures (March 31, 2026).

- The value signal survives the cross-check: return-on-capital approximation about 27.8 percent (threshold 25), P/E about 15, price to free cash flow about 12; a confluence of Greenblatt, Levermann (4 points) and Buffett's owner-earnings yield (data as of July 8, 2026).

- International growth of plus 26.8 percent in fiscal year 2026 — in many foreign markets HOKA and UGG are only at the beginning of their distribution (10-K, fiscal year 2026).

- Massive capital returns: a buyback authorization of about $4.84 billion (May 2026) — roughly a third of the market value; plus the silent option on tariff refunds after the Supreme Court ruling, carried at zero in the books.

What speaks against it:

- Extreme brand concentration: HOKA and UGG carry 97.3 percent of revenue; the remaining portfolio shrank 33.9 percent — if fashion taste turns at just one of the two brands, it hits half the group (10-K, fiscal year 2026).

- The home market stagnates: U.S. revenue plus 0.2 percent, HOKA growth slowing from 27.9 via 23.6 to 15.9 percent, UGG grew only 4.9 percent in the holiday quarter (10-K; 10-Q as of December 31, 2025).

- Tariff and sourcing risk: manufacturing predominantly in Vietnam and Indonesia, tariffs already pressed the gross margin by 20 basis points, the legal situation is in motion after the IEEPA ruling, and per the report the margin protection may not be repeatable in fiscal year 2027 (10-K, fiscal year 2026).

- Raw-material cluster: the UGG sheepskin is processed largely by two tanneries in China; on top, growing societal and regulatory pressure on animal-derived materials (10-K, Item 1A).

- Broken market technicals: Stage 1, relative strength 34, a good 52 percent below the all-time high, Piotroski 4 of 9 — and the buyback history shows that even management bought most expensively near the high (average $149.21 in fiscal year 2025; data as of July 8, 2026).

A human conclusion

Back to the red price tag. The anchoring effect has two faces, and both are traps. The first one you know: "from 200 to 100 — a bargain!", and what gets bought is the discount instead of the shoe. The second is subtler: "whatever has fallen this far must be broken" — and what gets shunned is the crash instead of the company. The fitting at the original document protects against both. At Deckers it shows a company that is distinctly better than its price sheet: two global brands, a record profit above the billion, a balance sheet without debt and with $1.9 billion in the till, a value signal that — unlike recently at Kirby — survives the recalculation, and a board standing ready to buy back a third of the company. And it shows what the market has priced in: a home market at zero, a locomotive whose growth staircase leads downward, tariffs as a lucky bag, and a group that hangs on two verdicts of fashion and two tanneries. The red tag only tells you what the stock used to cost. Whether it is worth today's price will be decided by whether HOKA keeps running internationally and UGG remains a brand instead of becoming a wave again. Whoever buys after this fitting buys, with open eyes, a cheap two-brand cluster — not simply "52 percent off". What you make of it is your decision. And that is exactly as it should be.

Sources

All original documents used in this analysis — to read for yourself:

- Deckers Outdoor Corporation — SEC annual report 10-K for fiscal year 2026 (ended March 31, 2026; filed May 22, 2026)

- Deckers Outdoor Corporation — SEC annual report 10-K for fiscal year 2025 (ended March 31, 2025; filed May 23, 2025)

- Deckers Outdoor Corporation — SEC quarterly report 10-Q as of December 31, 2025 (filed February 3, 2026)

- Deckers Outdoor Corporation — SEC quarterly report 10-Q as of September 30, 2025 (filed October 31, 2025)

- Deckers Outdoor Corporation — SEC quarterly report 10-Q as of June 30, 2025 (filed July 31, 2025)

- Deckers Outdoor Corporation — SEC quarterly report 10-Q as of December 31, 2024 (filed February 3, 2025)

- Deckers' complete SEC filing history: EDGAR overview (sec.gov)

- Fundamental data (metrics, valuation, raw scanner values; data as of July 8, 2026), reconciled with the SEC filings.

- Screener and rating data: in-house stock scanner (data as of July 8, 2026; scanner membership checked live on July 14, 2026).

Transparency & disclaimer: This analysis is a journalistic contextualization of publicly available information and is not investment advice, not a financial analysis in the regulatory sense, and not a solicitation to buy or sell securities. Stock investments carry substantial risks up to total loss. All information without guarantee; the data cut-off is noted in the text in each case. The author holds no position in Deckers stock at the time of publication.

Our Bottom Line at a Glance

- Brand strength & profitability positive

- HOKA and UGG are global brands with genuine pricing power: 57.7 percent gross margin, 23.1 percent operating margin, 41 percent return on equity — earnings per share have more than doubled since fiscal year 2023, from $3.23 to $7.02 (10-K, fiscal year 2026).

- Balance sheet & capital returns positive

- $1.91 billion in cash, no drawn bank loans, goodwill of only $14 million; buybacks of $1.08 billion in fiscal year 2026 and an authorization topped up to about $4.84 billion (May 2026) — roughly a third of the market value. No dividend since the IPO.

- Scanner signal & valuation positive

- The Greenblatt hit survives the cross-check (return-on-capital approximation about 27.8 percent against a threshold of 25; P/E about 15), flanked by Levermann (4 points) and Buffett's owner-earnings yield. Net of the cash, the operating business costs about twelve times annual earnings (data as of July 8, 2026).

- Growth quality & home market negative

- U.S. revenue grew only 0.2 percent in fiscal year 2026 — all growth came from abroad (+26.8 percent). HOKA's growth staircase leads downward (27.9 → 23.6 → 15.9 percent), UGG grew only 4.9 percent in the holiday quarter; Stage 1 and a relative strength of 34 show the market has priced that in.

- Concentration & tariff risks negative

- Two brands carry 97.3 percent of revenue in an industry with a declared fashion risk; manufacturing concentrates on Vietnam and Indonesia, the UGG sheepskin on two tanneries in China. Tariffs have already pressed the gross margin, and per the 10-K the margin protection may not be repeatable in fiscal year 2027.

Deckers is the rare case in which the value signal survives the recalculation: a debt-free two-brand group with a record profit above the billion, a 41 percent return on equity and a P/E around 15 — net of cash, about twelve times earnings. But the discount has nameable reasons: the U.S. market stagnates at plus 0.2 percent, HOKA's growth staircase leads downward, UGG remains a question of fashion, and tariffs as well as sourcing clusters (Vietnam/Indonesia, two tanneries) make the crown-jewel gross margin vulnerable. The market is pricing in stagnation; any stabilization of the home market would be a positive surprise — any fashion turn at UGG or HOKA an expensive one. Not investment advice.

What Our Rating Means

- If you don't own the stock

- As long as the question raised in the bottom line stays open, we see no basis for an entry.

- If you hold it in your portfolio

- Our findings offer no acute reason to sell — the checkpoints named remain decisive.

A journalistic assessment by our editorial team at the time of the deep dive, based on public sources — not investment advice and not a solicitation to buy or sell. Your personal circumstances (investment goals, risk capacity, taxes) cannot be taken into account. What our categories mean, how verdicts are formed, and what conflicts of interest exist →

Worth Noting

- Unlike the Kirby case (a data error), the Greenblatt hit here survives the cross-check against the 10-K figures; the calculation is disclosed in the text. The scanner row is documented in the screenshot (data as of July 8, 2026, confirmed live on July 14, 2026).

- Deckers has an offset fiscal year (ending March 31): "fiscal year 2026" = April 2025 through March 2026. All balance-sheet and earnings figures come from the SEC filings (10-K, filed 22.05.2026; 10-Q as of 31.12.2025, filed 03.02.2026) and are dated in the text; valuation figures carry the data cut-off of July 8, 2026.

- Analyst estimates ($7.49 and $8.33 in earnings per share for fiscal years 2027/2028) are consensus forecasts of 24 professionals, not facts — with consumer brands, estimates have historically been revised heavily after fashion turns.

- Possible tariff refunds after the Supreme Court's IEEPA ruling are carried at zero in the books (as of 31.03.2026) — a potential but uncertain one-off effect; size and timing are open.

Frequently Asked Questions

Deckers (NYSE: DECK) of Goleta, California, designs and markets footwear, apparel and accessories — all manufacturing is done by independent producers, predominantly in Vietnam and Indonesia. The two carrying brands are the running-shoe brand HOKA ($2.59 billion in revenue) and the sheepskin brand UGG ($2.74 billion); together they stood for 97.3 percent of group revenue of $5.47 billion in fiscal year 2026.

Deckers uses an offset fiscal year that ends on March 31 each time — "fiscal year 2026" means April 2025 through March 2026. The advantage: the important holiday season (the third fiscal quarter) and the subsequent sell-off fall into the same reporting year. When comparing with the calendar-year figures of other companies, you have to keep this shift in mind.

Because both criteria of the simplified Magic Formula are met — and the cross-check against the 10-K figures holds: return on equity of about 41 percent times an equity ratio of 67.8 percent yields a return-on-capital approximation of about 27.8 percent (threshold: 25 percent), at a price-to-earnings ratio around 15. In addition, the value scanners after Levermann (4 points) and Buffett's owner-earnings yield light up (data as of July 8, 2026).

Almost entirely: 97.3 percent of revenue in fiscal year 2026 came from these two brands. The remaining portfolio shrank by 33.9 percent — Sanuk was sold in 2024, Koolaburra and AHNU were wound down, Teva is being repositioned. The annual report names the core risk itself: the industry is subject to rapid fashion shifts, and brands can fall out of favor.

From its all-time high in early 2025 the stock lost a good 52 percent through July 8, 2026. Behind it stand the slowdown of HOKA's growth (from 27.9 via 23.6 to 15.9 percent), a U.S. revenue that grew only 0.2 percent in fiscal year 2026, and tariff and economic worries around the manufacturing in Southeast Asia. Earnings per share kept rising over the same period — which is why the price-to-earnings ratio fell to about 15.

A double one: manufacturing sits predominantly in Vietnam and Indonesia, which is why U.S. tariffs pressed the gross margin by 20 basis points in fiscal year 2026 despite price increases. At the same time the Supreme Court has declared certain IEEPA tariffs invalid — but possible refunds of duties already paid are uncertain, and Deckers deliberately booked no amounts whatsoever for them as of March 31, 2026.

No — since its IPO in 1993, Deckers has never paid a cash dividend. Distribution runs exclusively through share buybacks: $1.08 billion in fiscal year 2026, and in May 2026 the authorization was topped up to about $4.84 billion — enough for arithmetically about a third of all shares at the July 2026 market value.

Measured against the quality, yes: a price-to-earnings ratio of about 15, price to free cash flow of about 12, plus $1.9 billion in net cash (data as of July 8, 2026) at a 41 percent return on equity. But the discount has reasons: a two-brand cluster, a stagnating U.S. market, fading HOKA growth and tariff uncertainty. The market is pricing in stagnation rather than a continuation of records — that is opportunity and warning at once.

Found an error?

Did you spot a factual error, an outdated number, or a typo in this deep dive? Let us know briefly — your report goes straight to the editorial team.