Kirby Stock: America's Largest River Tanker Operator, a Genuine Record Run — and a Value Signal That Turns Out to Be a False Echo

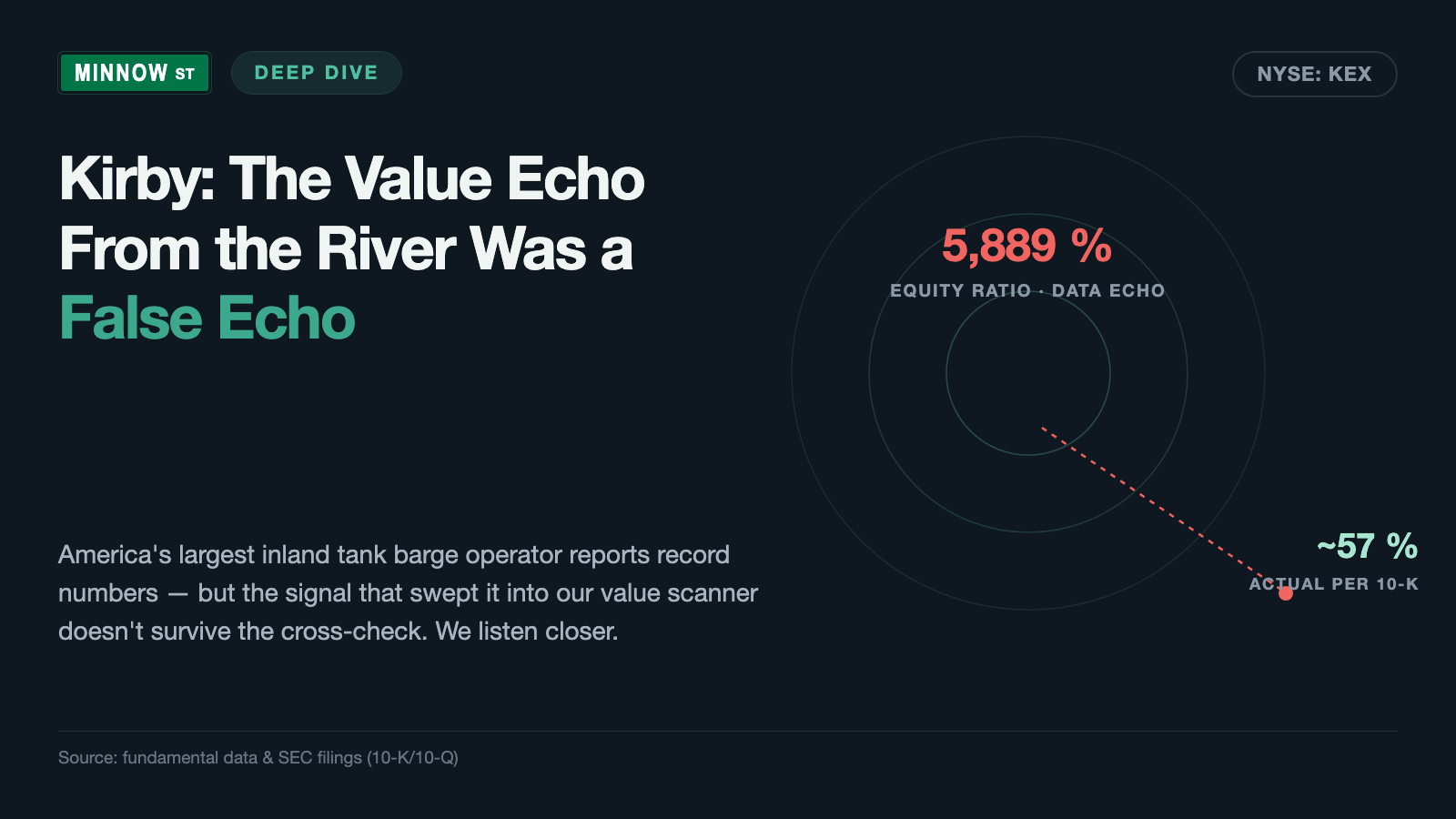

On the Mississippi, Kirby Corporation holds something like the house rules: 1,105 tank barges, roughly 28 percent of the U.S. inland tank barge fleet, protected by the Jones Act — and since 2022 earnings per share have nearly tripled ($2.03 to $6.33). Now the stock shows up in our value scanner built on Joel Greenblatt's Magic Formula. We ran the cross-check — in the annual report (10-K), in the quarterly reports (10-Q) and in the scanner's own raw data. The result: the record run is genuine, and so is the data center tailwind. The value seal, however, rests on an equity ratio of 5,889 percent in the data set — an outlier by a factor of 100. Not investment advice — just the cross-check at the original document before you follow the navigation system into the river.

Every water police unit knows the story, and every year it happens again somewhere: a driver steers his car down the boat ramp into the water — because the navigation system said the road continues here. Psychologists have a name for this: automation bias, the faith in the screen. What a device displays feels more thoroughly checked than what we see with our own eyes — yet the device has merely calculated, with whatever it was fed. On the stock market, this navigation system rides along everywhere: screeners, rankings, scanner signals. And this time it concerns — savor the irony — of all things a company whose vessels travel real rivers: Kirby Corporation (NYSE: KEX), the largest inland tank barge operator in the United States, showed up in our value scanner built on Joel Greenblatt's Magic Formula — good company, fair price, says the signal. So let's make a deal: before you follow the signal, we do the cross-check together — in the annual report (10-K, the yearly mandatory filing to the U.S. securities regulator, the SEC) and in the quarterly reports (10-Q). An SEC filing is honest under penalty of law. And this cross-check brings two things to light: a record run that is completely genuine — and a value seal that is not one. In the end, you decide for yourself.

What Kirby actually does

Picture America's rivers as the largest conveyor belt of U.S. industry. On the Mississippi River System and the Gulf Intracoastal Waterway — together more than 12,000 miles of navigable waterways — floats what refineries and chemical plants ship to one another: benzene, styrene, methanol, naphtha, black oil, diesel, liquid fertilizer. It is transported not in ships with their own engines but in tank barges — unpowered steel boxes that a towboat lashes together into tows of up to 25 barges. Kirby operates 1,105 inland tank barges with 24.5 million barrels of capacity and, on average, 266 towboats (as of December 31, 2025) — roughly 28 percent of the entire U.S. inland tank barge fleet of about 4,004 barges. The rest of the market is fragmented: Kirby is, by its own statement in the annual report, "the nation's largest domestic tank barge operator". Add to that 28 coastal tank barges with 2.9 million barrels for service along the U.S. coasts. The whole thing has grown over decades through acquisitions: from 71 tank barges in 1988 to 1,105 today — in 2023 through 2025 alone, Kirby bought 52 used barges and several tugs from competitors, most recently 14 barges plus four towboats for $97.3 million in March 2025. The company's roots reach back to 1921, headquarters are in Houston, Texas, and about 5,200 people work on board and ashore.

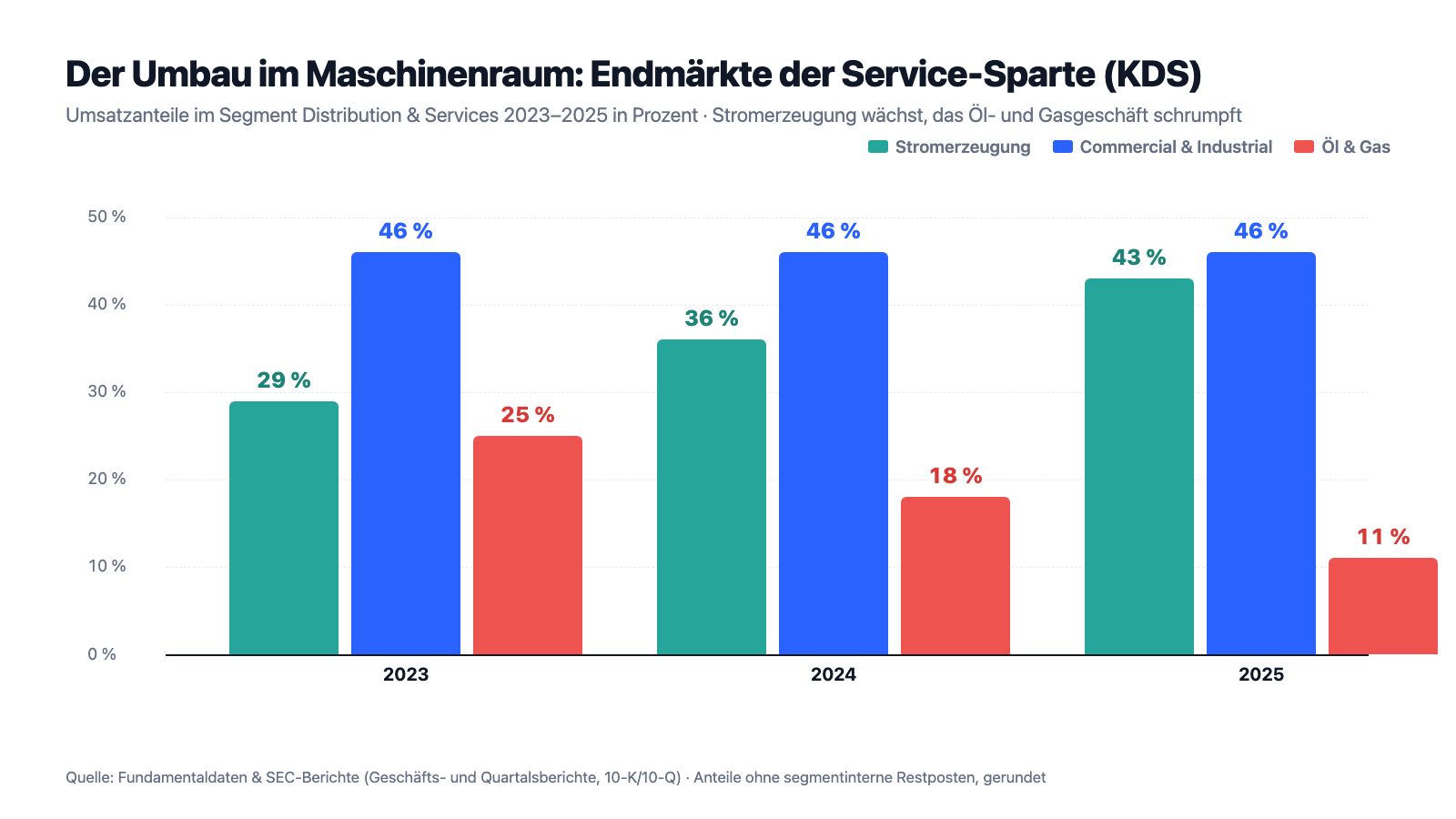

What makes this market special is its doorman: the Jones Act. This U.S. federal law of 1920 is something like the house rules of American waters — freight between two U.S. ports may only be carried by vessels that are built in the United States, registered in the United States, and manned, owned and operated by U.S. citizens. Foreign shipping companies with cheaper vessels and crews stay outside; the moat is written into the statute book. And then there is the second, often overlooked leg: Distribution & Services (KDS), a full 42 percent of revenue in 2025. This segment services and sells engines, transmissions and spare parts (among other things as the exclusive distributor of MTU and Allison products in several states), builds equipment for oilfield service companies — and, increasingly important: power generation systems, from backup generator sets to complete behind-the-meter power packages for data centers. Remember the central tension of this analysis, it runs through every chapter: a rock-solid, legally protected market leader in record form with a genuine data center tailwind — but the value seal that washed it into our scanner does not survive the cross-check, and the freight-rate cycle is showing its first cracks.

Where the stock shows up in our scanner — and what the cross-check says

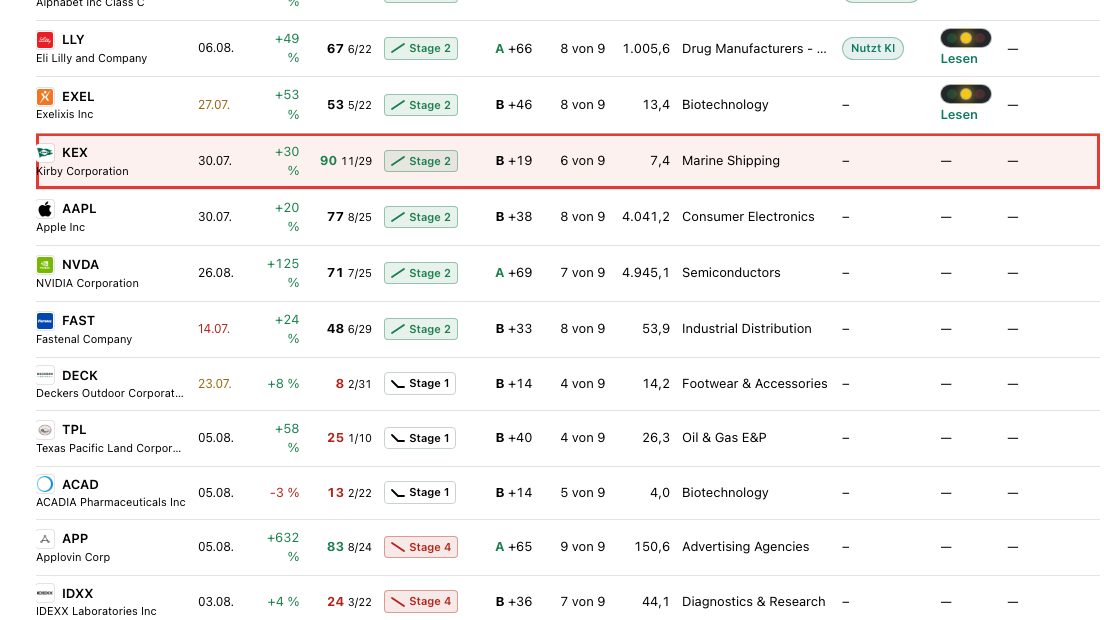

Every day we run about 3,500 stocks through our scanners. Kirby lights up in 7 scanners (data as of July 8, 2026), and not a single warning scanner is among them. The eye-catcher is the Magic Formula of value investor Joel Greenblatt — we confirmed the membership live once more on July 14, 2026. Greenblatt's idea in one sentence: buy good companies (high return on capital — how much profit per dollar of capital employed?) at fair prices (a reasonable price-to-earnings ratio). Our screener version approximates the return on capital as return on equity times equity ratio and demands at least 25 percent.

And now the cross-check that gives this analysis its connecting thread. Let's redo Greenblatt's criterion with Kirby's real balance-sheet figures (10-K 2025, balance sheet as of December 31, 2025): equity of $3.38 billion against total assets of $6.01 billion yields an equity ratio of about 57 percent — rock-solid. The return on equity: $354.6 million in profit on $3.38 billion of equity, so about 10.5 percent. Multiplied, that yields a return-on-capital approximation of about 6 percent — miles below the formula's 25 percent threshold. So why is Kirby in the scanner? Take a look at the metrics box on our Kirby stock page: there the equity ratio reads 5,889.4 percent — a value no balance sheet in the world can produce. In the fundamental data, Kirby's equity ratio is stored — as the only value in the hit list — too high by a factor of 100: a unit outlier, 58.9 instead of 0.589. The navigation system calculated with wrong coordinates. We show you this so openly because it is the most important lesson of this analysis: a scanner is only ever as honest as its data. How the same formula can be tricked by genuine numbers, by the way, is something we recently dissected twice — at the cyclical Micron it lit up right at the earnings peak, at MSG Entertainment a mini-equity inflated the return. Kirby is the third case in the series: here not even the number is right.

What remains once you subtract the false echo? A thoroughly respectable but different picture: the remaining six hits are trend and momentum signals — Weinstein Stage 2 (a stable uptrend), "strength on stress days" (on weak market days the stock held up better than 90 percent of the market), institutional accumulation, "pros 80%" (a high reported institutional share), plus a swing-trading list and a breakout signal. The relative strength of 68 says: solidly run, no high-flyer — up 20 percent in twelve months, up 26 percent year to date, but 12 percent below the high (data as of July 8, 2026). The Piotroski F-Score, a nine-point test of balance-sheet quality, stands at a decent 6 of 9. The fundamental rating of B with 19 of 100 points and an EPS rating of 60, by contrast, place the fundamental momentum only mid-field. The honest scanner fingerprint: a solid trend runner with an intact balance sheet — not a value bargain. All the more important what the filings say.

The numbers over the years — honestly appraised

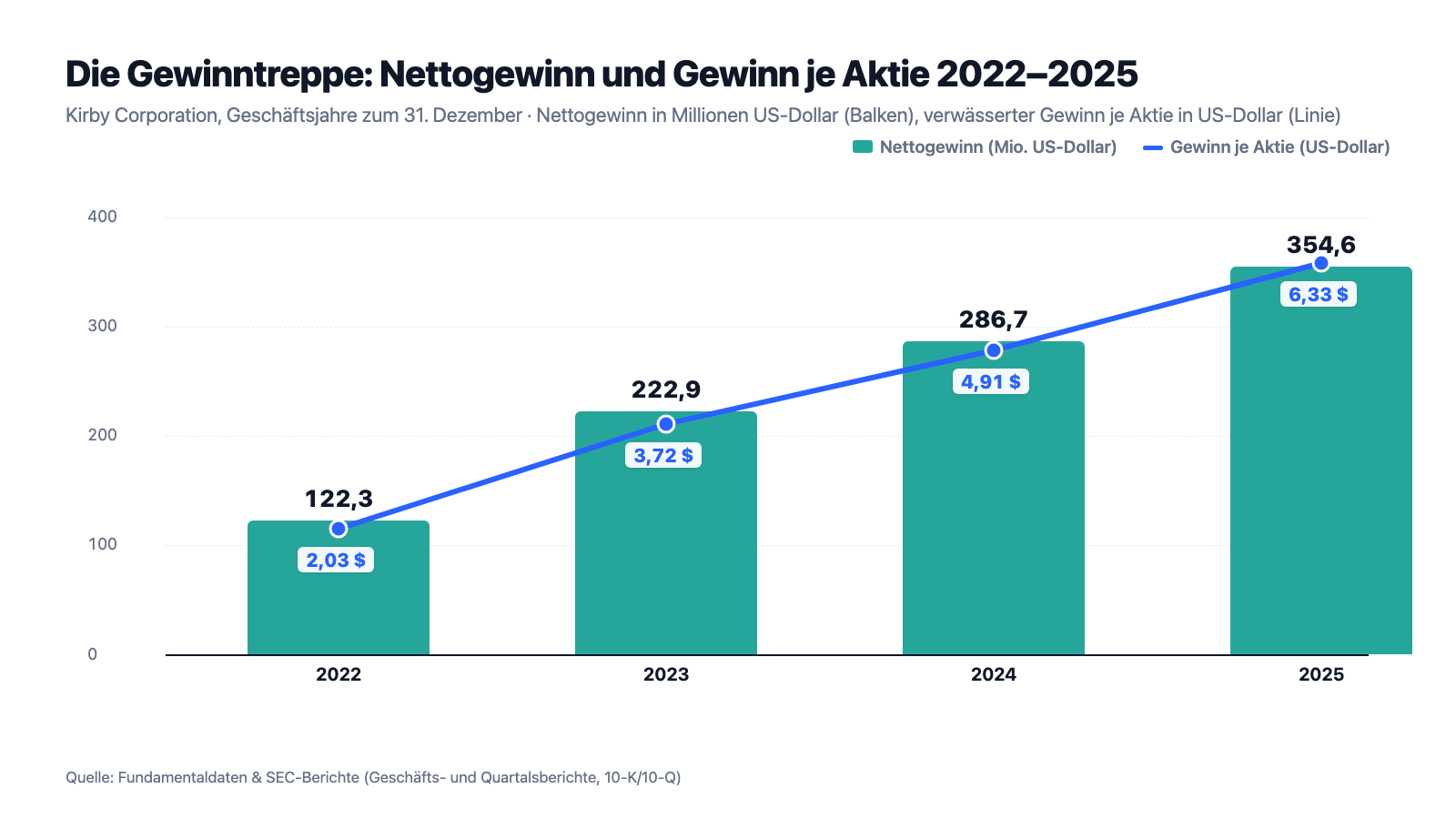

First, what genuinely impresses — and that is quite a lot. Kirby has delivered four years in a row: revenue rose from $2.78 billion (2022) via $3.09 (2023) and $3.27 (2024) to $3.36 billion (2025) — a record. Net income climbed over the same span from $122.3 via $222.9 and $286.7 to $354.6 million, earnings per share from $2.03 to $6.33 — nearly tripled. The trick with the lever: part of that is buyback math. Kirby has paid no dividend since 1989, but bought back $354.2 million of its own shares in 2025 alone — nearly the entire annual profit — and has shrunk the share count by a good tenth since the end of 2022. Operating cash flow: $670.2 million in 2025 (after $756.5 million in 2024), of which $264.5 million went into capital expenditures — $226.6 million of that into maintenance of the fleet alone; the ship eats before it earns, more on that later. The balance sheet as of December 31, 2025: $922.4 million of debt against $3.38 billion of equity (debt at 21.4 percent of total capitalization), and interest is covered about eleven times by operating income. And the current year keeps delivering: in the first quarter of 2026, revenue rose 7 percent to $844.1 million, earnings per share 13 percent to $1.50.

Where does the run come from? From two engine rooms. First, the marine transportation segment (KMT, 58 percent of revenue): its operating margin climbed from 13.9 percent (2023) via 19.0 to 19.3 percent (2025) — carried by a tight market. The U.S. inland tank barge fleet has stagnated at around 4,000 barges since 2019; industry-wide, 66 new barges were placed into service in 2025 and 65 were retired — zero growth. On the coast it is even tighter: there, per the annual report, not a single newbuild is on order, and Kirby pushed through price increases of 19 to 21 percent on contract renewals in the first quarter of 2026; the coastal fleet was 92 percent committed under term contracts and effectively fully utilized. Second, the transformation in the service segment (KDS, 42 percent): there the power generation business — backup power, peak shaving, behind-the-meter systems for data centers — is growing rapidly: plus 20 percent (2024), plus 26 percent (2025); its share of segment revenue rose from 29 percent (2023) via 36 to 43 percent (2025). The annual report explicitly names "several large project awards from data center customers" as the driver. At the same time, the same segment's conventional oil and gas business shrank from about a quarter (2023) to just 11 percent (2025). Exactly this transformation is what the next picture shows:

What the filings say — the uncomfortable truths

Uncomfortable truth no. 1: the freight-rate cycle is already showing cracks — in the middle of a record year

A tank barge is a commodity on the water: the price is set not by Kirby but by the ratio of cargo to available freight capacity. Two thirds of inland revenues run under term contracts (terms of twelve months and up), the rest in the spot market — the river's taxi stand, where every trip is negotiated anew. And exactly there the wind turned while the annual figures were still reporting records. The annual report logs it soberly:

"Inland tank barge utilization levels in 2025 were flat as compared to 2024, ranging from the low to mid-90% range during both the 2025 first and second quarters, and mid-80% range during the 2025 third quarter, and the mid to high 80% range during the 2025 fourth quarter."

— Kirby Corporation, SEC annual report 10-K 2025, Item 7 MD&A "Marine Transportation"

In plain terms: in the second half of 2025, noticeably more barges sat at the bank without cargo than in the first. The quarterly report as of March 31, 2026 continues the series: utilization in the low 90s range (prior year: low to mid-90s range), inland spot rates 4 to 6 percent below the prior year, term contracts up only 0 to 2 percent — and the marine segment's operating margin eased slightly in the quarter (18.0 after 18.2 percent). That is not a slump, but it is the direction that counts: the spot market is the fever thermometer of this business, and it no longer points uphill. Industry history counsels humility: when oil prices fell after 2015 and freight capacity came free, the number of barges in crude oil service halved within a few years — Kirby's own report documents the decline from about 550 to 170 to 180 barges. A tight market can become a normal market very quickly.

Uncomfortable truth no. 2: the fleet averages 17.8 years of age — and replacement costs more than ever

Kirby's most important machine is made of steel, and it rusts. The 1,105 inland tank barges average 17.8 years of age; industry-wide, about 600 of the good 4,000 barges are more than 30 years old. In the short term that supports prices (old iron leaves the market), but in the long term it poses the most expensive question of all: what does it cost to replace this fleet? The annual report's answer should be known to anyone buying the stock as an "asset play":

"Significant increases in the construction cost of tank barges and towing vessels may limit the Company's ability to earn an adequate return on its investment in new tank barges and towing vessels. […] Although steel prices have remained stable in 2024 and 2025, they still remain near historical highs."

— Kirby Corporation, SEC annual report 10-K 2025, Item 1A "Risk Factors"

The numbers for it are in the cash flow statement: of $264.5 million in capital expenditures in 2025, $226.6 million was pure maintenance — money that merely keeps the fleet where it is, before a single dollar of growth is financed. Kirby's way out is clever but finite: instead of building new at high prices, the company buys used barges from smaller competitors (52 of them from 2023 through 2025) and even operates its own towboat shipyard with San Jac. But the older the industry fleet gets, the closer the day when new tonnage must be built at peak prices — or capacity shrinks. The latter would be good for rates, the former bad for returns on capital. That is exactly why the honest return-on-capital figure of about 6 percent from our scanner cross-check is not a footnote but the core: this business earns solidly — but it earns on heavy, expensive, rusting steel.

Uncomfortable truth no. 3: the moat belongs not to Kirby but to Congress — and it regularly gets exemption holes

Kirby's strongest competitive advantage sits in no patent and no balance sheet, but in a law from 1920. What the legislature has given, it can change — and the annual report names the risk itself:

"The Company's business could be adversely affected if the Jones Act or international trade agreements or laws were to be modified or waived as to permit foreign flagged vessels to operate in the United States as these vessels are not subject to the same United States government imposed regulations, laws, and restrictions."

— Kirby Corporation, SEC annual report 10-K 2025, Item 1A "Risk Factors"

Kirby itself considers outright repeal unlikely — but the exemptions are real and are used more often than you would think: the Department of Homeland Security can suspend the Jones Act by waiver and has done so — after the 2017 hurricanes, twice during the Colonial Pipeline shutdown in May 2021, twice after Hurricane Fiona in 2022, and most recently again in April 2025, once more because of the Colonial Pipeline. Each of these waivers lets foreign tankers into Kirby's territory for days or weeks. On top of that comes a second dependence on the state that hardly any investor has on the radar: Kirby's "road network" — more than 240 locks and dams — belongs to the federal government, and more than half of the locks are over 50 years old. More frequent maintenance outages, delays and extra costs included; 35 percent of the expansion is financed through a tax of 29 cents per gallon of marine diesel that Congress can raise at any time. A moat whose water level is set by politics: that is the flip side of the finest protective wall in U.S. shipping.

Uncomfortable truth no. 4: an oil legacy sits in the second leg — and the energy transition has already hit it once

The data center story of the service segment is real — but the same segment has just demonstrated how quickly an end market can tip. At the end of 2024, Kirby had to write down $56.3 million on inventories. The reason, logged in the annual report:

"During the fourth quarter of 2024, the Company recognized a $56.3 million non-cash impairment charge in the KDS segment primarily associated with conventional diesel fracturing equipment inventory. Based on the current market conditions and its view on the industry outlook, including decreased customer demand for conventional diesel fracturing equipment driven by an industry-wide shift to electric fracturing equipment, the Company determined that certain inventory had limited commercial opportunity, and the cost of these inventories exceeded its net realizable value."

— Kirby Corporation, SEC annual report 10-K 2025, Note 7 "Impairments"

An inventory write-down means, in plain terms: shelves full of technology nobody wants at cost anymore. The segment's oil and gas business shrank 28 percent in 2024 and another 32 percent in 2025; in the first quarter of 2026 the segment margin also slipped to 6.7 percent (prior year: 7.3), because the on-road service business is limping (a "trucking recession", the report calls it) and large projects only bring in money on delivery. And one more thing belongs to an honest framing of the data center imagination: Kirby is an equipment supplier and service provider here, not a platform — it sells engines, generator sets and maintenance into a boom market where Caterpillar, Cummins and other heavyweights also stand, and the report itself warns of extended lead times from the manufacturers whose products Kirby distributes. A growing, good business — but one with a single-digit to low-double-digit margin, not a software gold mine. Whoever buys the stock because of "AI data centers" should know they are buying a machinery dealer whose bigger brother drives tank barges.

Valuation: $7.4 billion for the river market leader

In early July 2026 the Kirby stock cost about $139; at 53.6 million shares outstanding, that makes a market value of about $7.4 billion (all valuation figures: data as of July 8, 2026). Measured against the earnings of the last four quarters, that is a price-to-earnings ratio of about 21 — and here the context the scanner could not deliver is worth having: for a company with about 10.5 percent return on equity and about 6 percent return on total capital, 21 times earnings is not a bargain but an advance of trust in the continuation of the record run. Analyst estimates (five professionals, consensus on average "buy") see $7.01 in earnings per share for 2026 and $8.28 for 2027 — that would be a P/E of about 20 and 17, respectively. The price-to-book ratio stands at about 2.2: the market pays double the book equity — though for a fleet whose replacement at steel prices near historical highs would also cost more than the book values suggest. Price-to-sales about 2.2, price-to-free-cash-flow about 15. Add the shareholder policy: no dividend since 1989, but consistent buybacks instead (2025: $354.2 million; in early 2026 the authorization was topped up by further shares). Summed up fairly: the valuation is neither euphoria nor a clearance offer — it is the price of quality and market position, paid at the point in the cycle where utilization is just beginning to crumble.

Opportunities and risks at a glance

What speaks for Kirby:

- Market leadership with a statutory moat: 1,105 inland tank barges, roughly 28 percent of the U.S. fleet, Jones Act protection against foreign competition; the industry fleet has stagnated since 2019, and not a single coastal newbuild is on order (10-K 2025).

- Record earnings: revenue of $3.36 billion, net income of $354.6 million, earnings per share nearly tripled since 2022; a 19.3 percent operating marine margin; the first quarter of 2026 with revenue up 7 percent and earnings per share up 13 percent.

- Data center tailwind in the second leg: power generation grew 20 and 26 percent in 2024/2025 to 43 percent of segment revenue, with large project awards from data center customers and full order books for 2026 (10-K 2025; 10-Q as of March 31, 2026).

- A solid balance sheet and shareholder-friendly capital allocation: debt at 21.4 percent of total capitalization, interest coverage about eleven times, $670 million in operating cash flow, buybacks of $354.2 million (2025) — the share count has been falling for years.

- Six genuine trend/momentum signals in the in-house scanner (Stage 2, strength on stress days 90, institutional accumulation and others), Piotroski 6 of 9 (data as of July 8, 2026).

What speaks against it:

- The value label is a false echo: the Magic Formula membership rests on an equity ratio stored too high by a factor of 100 in the fundamental data; in reality the return-on-capital approximation sits at about 6 percent — the formula demands 25 (own cross-check against 10-K balance-sheet figures).

- The cycle is crumbling at the edge: utilization fell into the 80s range in the second half of 2025, inland spot rates in the first quarter of 2026 were four to six percent below the prior year, and the marine margin eased slightly in the quarter (10-K 2025; 10-Q as of March 31, 2026).

- Capital intensity: a fleet averaging 17.8 years of age, $226.6 of $264.5 million in capital expenditures is pure maintenance, newbuild prices sit near historical highs — the replacement question gets more expensive every year (10-K 2025).

- Dependence on politics: Jones Act waivers were issued in 2017, 2021, 2022 and most recently in April 2025; more than half of the federally owned locks are older than 50 years — maintenance outages and higher user fees loom (10-K 2025).

- An oil legacy and margin pressure in the service business: the segment's oil and gas revenues shrank 28 and 32 percent in 2024/2025, a $56.3 million inventory write-down for the shift to electric fracking, and a segment margin of 6.7 percent in the first quarter of 2026 (10-K 2025; 10-Q as of March 31, 2026).

A human conclusion

Back to the boat ramp. The driver who follows the navigation system into the water is no fool — he has merely misunderstood the division of labor: the device calculates, but looking is his job. Exactly this division of labor applied in this analysis. Our scanner calculated, correctly and stubbornly, with a number that was off by a factor of 100 — and awarded a value seal that Kirby, honestly calculated, would never have received. That is our false echo, and we would rather show it to you than hide it. But the cross-check at the original document did not just disenchant the seal — it also revealed a company that is better than its wrong label: a 105-year-old, conservatively financed heirloom of U.S. industry, market leader behind a statutory moat, with earnings per share nearly tripled, iron buyback discipline and a second leg that is just being caught by the data center boom. And it laid open the two questions the price has to answer: whether the crumbling utilization is only a dent — and whether 21 times a record profit remains a fair price for a business with a 6 percent return on capital once the river runs at normal levels again. Whoever buys after this cross-check buys the river tanker with open eyes — not the bargain from the screen. What you make of it is your decision. And that is exactly as it should be.

Sources

All original documents used in this analysis — to read for yourself:

- Kirby Corporation — SEC annual report 10-K for fiscal year 2025 (filed February 17, 2026)

- Kirby Corporation — SEC annual report 10-K for fiscal year 2024 (filed February 18, 2025)

- Kirby Corporation — SEC quarterly report 10-Q as of March 31, 2026 (filed May 8, 2026)

- Kirby Corporation — SEC quarterly report 10-Q as of September 30, 2025 (filed November 10, 2025)

- Kirby Corporation — SEC quarterly report 10-Q as of June 30, 2025 (filed August 11, 2025)

- Kirby Corporation — SEC quarterly report 10-Q as of March 31, 2025 (filed May 12, 2025)

- Kirby's complete SEC filing history: EDGAR overview (sec.gov)

- Fundamental data (metrics, valuation, raw scanner values; data as of July 8, 2026), reconciled with the SEC filings — including the unit outlier in the equity ratio disclosed in the text.

- Screener and rating data: in-house stock scanner (data as of July 8, 2026; scanner membership checked live on July 14, 2026).

Transparency & disclaimer: This analysis is a journalistic contextualization of publicly available information and is not investment advice, not a financial analysis in the regulatory sense, and not a solicitation to buy or sell securities. Stock investments carry substantial risks up to total loss. All information without guarantee; the data cut-off is noted in the text in each case. The author holds no position in Kirby stock at the time of publication.

Our Bottom Line at a Glance

- Market position & moat positive

- Largest U.S. inland tank barge operator (1,105 barges, roughly 28 percent of the fleet), protected by the Jones Act; the industry fleet has stagnated since 2019, on the coast not a single newbuild is on order and Kirby pushed through price increases of 19 to 21 percent there in early 2026 (10-K 2025; 10-Q as of March 31, 2026).

- Earnings & balance sheet positive

- Earnings per share nearly tripled since 2022 ($2.03 to $6.33), a 19.3 percent operating marine margin, $670 million in operating cash flow, debt at only 21.4 percent of total capitalization, interest coverage about eleven times — plus consistent buybacks instead of a dividend (since 1989).

- Scanner signal & data quality negative

- The Magic Formula hit is a false echo: the equity ratio is stored in the fundamental data too high by a factor of 100 (5,889 instead of roughly 59 percent); in reality the return-on-capital approximation sits at about 6 percent — far below the formula's 25 percent threshold. The remaining six hits are trend/momentum signals, and the fundamental rating (B, 19 of 100) sits in the lower midfield.

- Cyclicality & capital intensity negative

- Utilization fell into the 80s range in the second half of 2025, inland spot rates in early 2026 were four to six percent below the prior year; the fleet averages 17.8 years of age, newbuild prices sit near historical highs, and $226.6 of $264.5 million in capital expenditures is pure maintenance (10-K 2025).

- Power generation growth story neutral

- The power generation business grew 20 and 26 percent in 2024/2025 to 43 percent of the service segment, with large project awards from data center customers — but Kirby is an equipment supplier there with a single-digit segment margin (6.7 percent in the first quarter of 2026), the oil legacy is shrinking at double-digit rates, and in 2024 the shift to electric fracking already cost a $56.3 million inventory write-down.

Kirby is the opposite of a warning-signal case — but no value bargain either: a conservatively financed, legally protected market leader in record form whose Greenblatt label rests on a unit outlier in the fundamental data (honest return-on-capital approximation: about 6 instead of the required 25 percent). Freight utilization has been crumbling since the second half of 2025, the fleet is aging while newbuild prices sit near historical highs, and 21 times a record profit already honors the quality. The data center tailwind in the service business is real but carries single-digit margins. Not investment advice.

What Our Rating Means

- If you don't own the stock

- As long as the question raised in the bottom line stays open, we see no basis for an entry.

- If you hold it in your portfolio

- Our findings offer no acute reason to sell — the checkpoints named remain decisive.

A journalistic assessment by our editorial team at the time of the deep dive, based on public sources — not investment advice and not a solicitation to buy or sell. Your personal circumstances (investment goals, risk capacity, taxes) cannot be taken into account. What our categories mean, how verdicts are formed, and what conflicts of interest exist →

Worth Noting

- The Magic Formula membership rests on a data error (the equity ratio stored too high by a factor of 100 in the fundamental data); the article lays the cross-check open. The scanner row is documented in the screenshot (data as of July 8, 2026, confirmed live on July 14, 2026).

- All balance-sheet and earnings figures come from the SEC filings (10-K 2025, filed 17.02.2026; 10-Q as of 31.03.2026, filed 08.05.2026) and are dated in the text; valuation figures carry the data cut-off of July 8, 2026 — analyses are evergreen, daily prices are not a buy argument.

- Analyst estimates ($7.01 and $8.28 in earnings per share for 2026/2027) are consensus forecasts of five professionals, not facts — with cyclicals, estimates have historically been revised most heavily at turning points.

- Kirby reports utilization only as ranges (e.g. "low-90% range"); the wording in the text follows the language of the 10-K/10-Q.

Frequently Asked Questions

Kirby (NYSE: KEX) of Houston, Texas, is the largest inland tank barge operator in the United States: 1,105 tank barges with 24.5 million barrels of capacity transport petrochemicals, black oil, refined fuels and agricultural chemicals on the Mississippi River System and along the U.S. coasts (58 percent of 2025 revenue). The second segment, Distribution & Services, services and sells engines, spare parts and power generation systems — increasingly for data centers.

The Jones Act of 1920 reserves freight transport between U.S. ports for vessels that are built and registered in the United States and manned, owned and operated by U.S. citizens. Foreign shipping companies with cheaper vessels are locked out — a statutory moat for Kirby. The flip side: the protection depends on politics, and the Department of Homeland Security temporarily suspended the Jones Act in 2017, 2021, 2022 and most recently in April 2025.

Because of a data error we disclose in the article: in the fundamental data, Kirby's equity ratio is stored too high by a factor of 100 (5,889 instead of roughly 59 percent). As a result, the Magic Formula's return-on-capital approximation appears above the 25 percent threshold. In reality it sits at about 6 percent — honestly calculated, Kirby would not be a hit. The remaining six scanner hits are trend and momentum signals.

Distinctly: freight rates follow the ratio of cargo volumes to available freight capacity. In 2025, the utilization of Kirby's inland fleet fell from the low to mid-90 percent range into the mid-80s range, and inland spot rates in early 2026 were four to six percent below the prior year. After the oil price collapse from 2015 onward, the number of barges in crude oil service shrank, per the annual report, from about 550 to 170 to 180.

The service segment builds, installs and maintains power generation systems — backup, peak-shaving and behind-the-meter installations, including for data centers. This business grew 20 percent in 2024 and 26 percent in 2025 and now makes up 43 percent of segment revenue (2023: 29 percent). Kirby is an equipment supplier and service provider here, with a single-digit segment margin — not a technology platform business.

With a price-to-earnings ratio of about 21, price-to-book of about 2.2 and price-to-free-cash-flow of about 15 (data as of July 8, 2026), the stock is valued fair to demanding — measured against a return on equity of about 10.5 percent and a return on total capital of about 6 percent. The price honors market leadership and a record run; a value bargain in the sense of the Magic Formula it is not, despite the scanner signal.

No — Kirby has not paid a dividend since 1989 and has no fixed dividend policy either. Instead, the company consistently buys back its own shares: $354.2 million worth in 2025 alone (3.7 million shares at an average of $96.27). The share count has fallen by a good tenth since the end of 2022, which additionally lifts earnings per share.

The 1,105 inland tank barges average 17.8 years of age; industry-wide, about 600 of the good 4,000 barges are more than 30 years old. In the short term that supports freight rates, because old capacity leaves the market. In the long term the expensive replacement question looms: newbuild prices sit near historical highs because of steel costs, and already today $226.6 of $264.5 million in capital expenditures goes into pure maintenance (2025).

Found an error?

Did you spot a factual error, an outdated number, or a typo in this deep dive? Let us know briefly — your report goes straight to the editorial team.