Cytokinetics Stock: 20 Years of Losses, Negative Equity — and a Record Chart After the First Approval

Cytokinetics builds drugs that make the heart muscle deliberately stronger or weaker — and after two decades of research received its first approval in December 2025: MYQORZO, against a dangerous heart-muscle disease. The stock trades near its all-time high, weighing in at about $10.9 billion. And yet it shows up in our going-concern warning scanner. We read the annual report (10-K) for 2025 and the quarterly report (10-Q) as of March 31, 2026: a $3.7 billion accumulated deficit, equity of minus $826.6 million, a cash burn that keeps running — but also $1.1 billion in the till and not a word of going-concern doubt from the auditor. Not investment advice — just a clear-eyed look at what stands behind the celebration curve.

There is a reflex that reliably lures investors into the most expensive stocks: let's call it the winner's reflex. In front of you lies a price chart that points from bottom-left to top-right, up 149 percent in a year, near the all-time high — and a piece of news that finally sounds like a happy ending: after more than two decades of research, the company has had its first drug approved. Your gut says: "Everything is going right here, jump on." Hardly any company serves this reflex as beautifully right now as Cytokinetics (NASDAQ: CYTK), a biopharma from South San Francisco that turns the mechanics of the heart muscle into medicine. And yet the very same stock shows up in our warning scanner for going-concern doubt — among companies with serious balance-sheet worries. Two labels that seem to contradict each other: "record winner" and "nearing insolvency". So let's make a deal: before you let the green chart or the red warning label do your thinking for you, we read together what Cytokinetics itself reported to the U.S. securities regulator, the SEC — in the annual report (10-K) for 2025 and the quarterly report (10-Q) as of March 31, 2026. An SEC filing is honest under penalty of law. In the end, you decide for yourself.

What Cytokinetics actually does

Picture the heart muscle as an engine whose power has to be dosed exactly: too weak, and the blood is no longer pumped through the body; too strong and thickened, and the chamber becomes so narrow that hardly any blood gets through. It is precisely this mechanics of muscle contraction that Cytokinetics has worked on for more than 20 years — not the metabolism, not the electrics of the heart, but the pure force regulation of the muscle itself. The company builds small molecules that act like an accelerator or a brake for the heart-muscle fibers. The great hope is called aficamten, marketed as MYQORZO: a "brake" for patients with obstructive hypertrophic cardiomyopathy (oHCM) — a disease in which the heart muscle is pathologically thickened and narrows the blood outlet. MYQORZO relaxes the overactive muscle and is meant to improve exercise capacity and symptoms.

And this is the real turning point of this analysis: after two decades of pure research, Cytokinetics received its first approval ever in 2025 — the FDA in the United States and the authority in China cleared MYQORZO in December 2025, the EU followed in February 2026; the first patients were prescribed the drug from late January 2026. Behind it stands a whole family of candidates built on the same biology: ulacamten against a related form of heart failure (HFpEF) and omecamtiv mecarbil, which conversely is meant to strengthen a heart muscle that is too weak (HFrEF). Sounds like the transition from perpetual research lab to real pharmaceutical company? In part it is. But note here already the central tension of this analysis: a $10.9 billion company with its first approved drug and a record chart — that nonetheless sits in a near-insolvency filter, because two decades of research have left behind negative equity and a $3.7 billion accumulated deficit. It runs through every chapter. For a look at what such a turning point looks like at another biotech, see our analysis of Arcus Biosciences — there too the distress label deceives at first glance.

Where the stock shows up in our scanner

Every day we run about 3,500 stocks through our scanners. Cytokinetics triggers a downright contradictory mix (data as of July 8, 2026). On the warning side stands the "Going Concern (Distress-Proxy)" — a filter that looks for the classic signs of a shaky balance sheet: an Altman Z-Score in the danger zone, negative interest coverage, persistent losses. The Altman Z-Score, a classic early-warning gauge for insolvency built from several balance-sheet ratios, sits deep in the red at Cytokinetics (about minus 7); the Piotroski F-Score, a nine-point test of balance-sheet quality, stands at 3 of 9 — a fundamentally healthy company stands at 8 or 9. Five distress flags, fundamental rating D. On paper, a balance-sheet ruin.

And now the contradiction that makes this stock so instructive: the same company sits at the same time in about two dozen scanners of strength. The price trades above its 50- and 200-day lines, Weinstein phase analysis classes it in Stage 2 (an intact uptrend, not a topping formation), it sits near its 52-week high and only about 25 percent below the all-time high, the power trend is active, and it appears in the institutional accumulation scanner because large addresses are buying in. A going-concern warning signal next to a power trend — that is not common. This is exactly where the comparison with another case from the same warning scanner pays off: at Replimune the distress proxy matched the hard truth — there the auditor had actually written a going-concern qualification into the opinion. At Cytokinetics that is expressly not the case. The proxy is only a quantitative approximation, and here it shows, like any smoke detector, that it can go off where there is no fire at all — more on that shortly. How such warning lists are to be read in general — a smoke detector, not a demolition notice — we explained in the article "Insolvency Radar: the Top 10".

The numbers over the years — honestly appraised

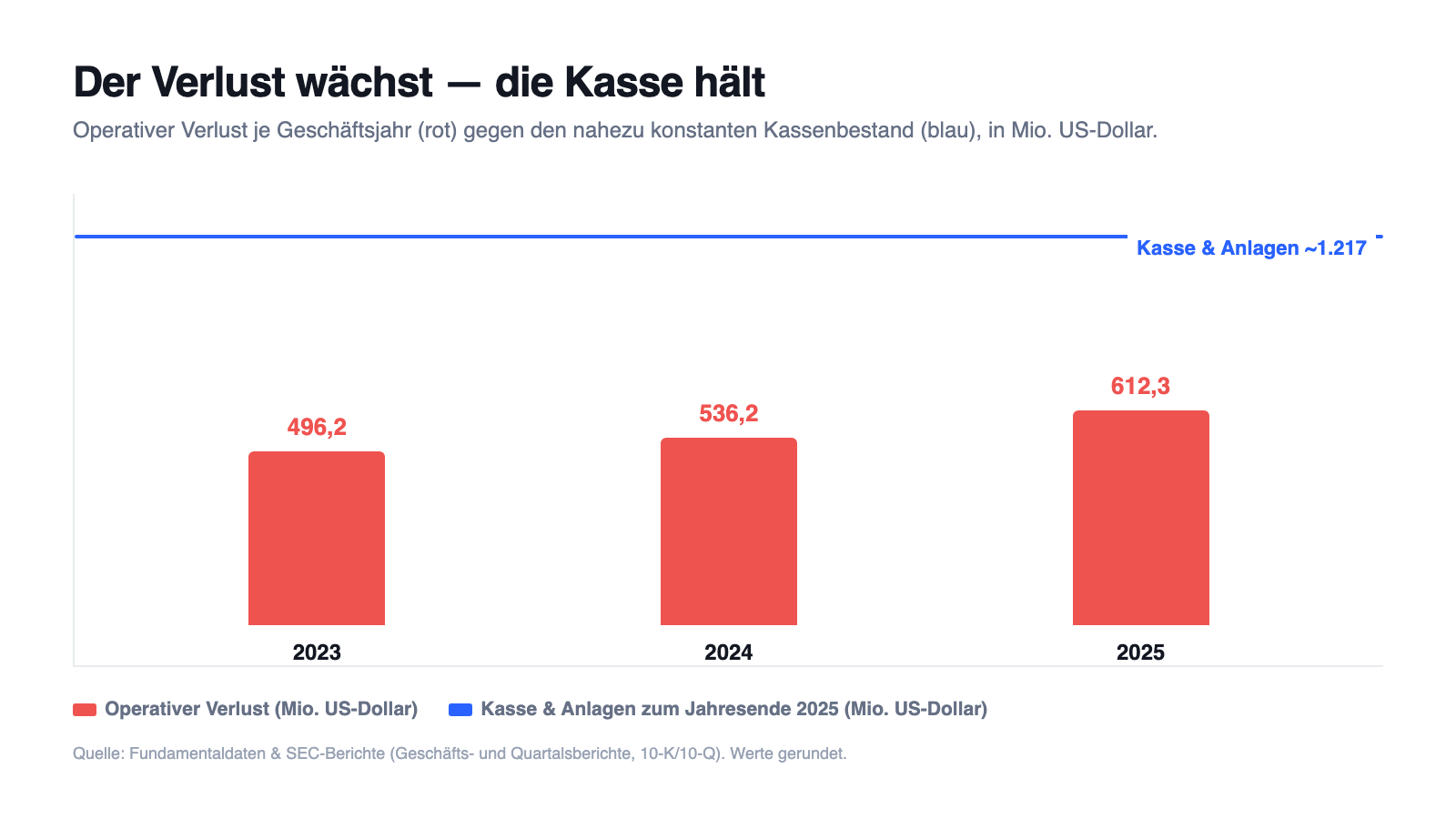

With a company like Cytokinetics you have to start honestly: until recently there is no revenue curve to admire that rests on products. For more than two decades the company lived off milestone and license payments from its pharma partners and off selling new shares and bonds — in 2025 total revenue came to $88.0 million ($79.4 million from licenses and milestones from Bayer and Sanofi, $8.7 million from collaborations), product revenue: zero. That is not a hidden weakness but the very nature of a development-stage biopharma: a large lab racing against time. And this research carries a rising price. The net loss climbed from $526.2 million (2023) via $589.5 million (2024) to $785.0 million (2025); the operating loss alone stood at $612.3 million in 2025, driven by $416.0 million in research and development and $284.3 million for administration and building the sales force. The real turning point sits right at the start of the 2026 figures: in the first quarter Cytokinetics booked product revenue for the first time in its history — $4.8 million from MYQORZO. A tender shoot, but a historic one.

Add up all the losses since the company's founding, and the books show an accumulated deficit of about $3.7 billion (March 31, 2026). It was financed through share issues, convertible notes and unusual deals with the investor Royalty Pharma. That is the second side of the biotech coin you should keep in mind: two decades of progress were paid for with other people's money — and that money secured its share of the future. Which brings us to the uncomfortable truths — and to the resolution of the scanner contradiction.

What the filings say — the uncomfortable truths

Uncomfortable truth no. 1: 20 years, not a single profitable year — and equity below zero

Here sits the root of the distress label. Cytokinetics has been publicly listed since 2004 and in all that time has never posted an annual profit. The company says so itself in the quarterly report, soberly:

"We have incurred an accumulated deficit of approximately $3.7 billion since inception and there can be no assurance that we will attain profitability. […] We anticipate that we will have operating losses and net cash outflows in future periods."

— Cytokinetics, SEC quarterly report 10-Q as of March 31, 2026, Note 1 "Organization and Liquidity"

This loss history has an accounting consequence that triggers the distress proxy: equity is negative. As of March 31, 2026 the balance sheet showed a "total stockholders' deficit" of minus $826.6 million (end of 2025: minus $659.6 million). In arithmetic terms: liabilities exceed assets — if you sold everything today at book value and paid off all debts, shareholders would be left with a minus. It is exactly such numbers — negative equity, negative interest coverage, perpetual losses — that fed the Altman Z-Score into the red. Remember this tension: the warning filter measures yesterday's accounting (two decades of losses), not tomorrow's solvency. At Cytokinetics the two are far apart — and that is the core of the case.

Uncomfortable truth no. 2: the cash burn keeps running — but the till is full, and the auditor stays silent

The engine keeps burning cash: in 2025, $510.0 million flowed out from operations alone, another $145.5 million in the first quarter of 2026. At a clinical biotech like Replimune that was exactly what triggered the auditor's going-concern doubt. Here, though, the report says the opposite — and that is the decisive honesty of this case:

"We believe that our existing cash, cash equivalents and investments will be sufficient to fund cash requirements for at least the next 12 months after the issuance of these consolidated financial statements."

— Cytokinetics, SEC annual report 10-K 2025, Item 7 MD&A "Liquidity and Capital Resources"

The bare arithmetic behind it: as of March 31, 2026, about $1.1 billion in cash and investments sat in the till (end of 2025: $1.2 billion). That covers the current annual burn with a comfortable margin — and unlike a compound without market access, here a revenue stream is just beginning to flow. The auditor signed off on the accounts without reservation; the words "substantial doubt", which stood in black and white in Replimune's opinion, are entirely absent at Cytokinetics. This is the resolution of the scanner contradiction: the going-concern proxy is a mechanical approximation that fires on losses and negative equity — here it is a false alarm in the literal sense, a smoke detector reacting to the steam of a hot shower, not to fire. That does not make the balance sheet pretty: a company that burns half a billion a year remains dependent on the capital market. But "dependent on fresh money" and "on the brink of bankruptcy" are two different things — and this analysis does not confuse them.

Uncomfortable truth no. 3: the financing is sold future — $1.3 billion of debt plus assigned revenue

How does a perpetually loss-making research house keep refilling the till over two decades without endlessly diluting its old shareholders? Cytokinetics chose an unusual path — and you should know its price. The report quantifies the debt burden like this:

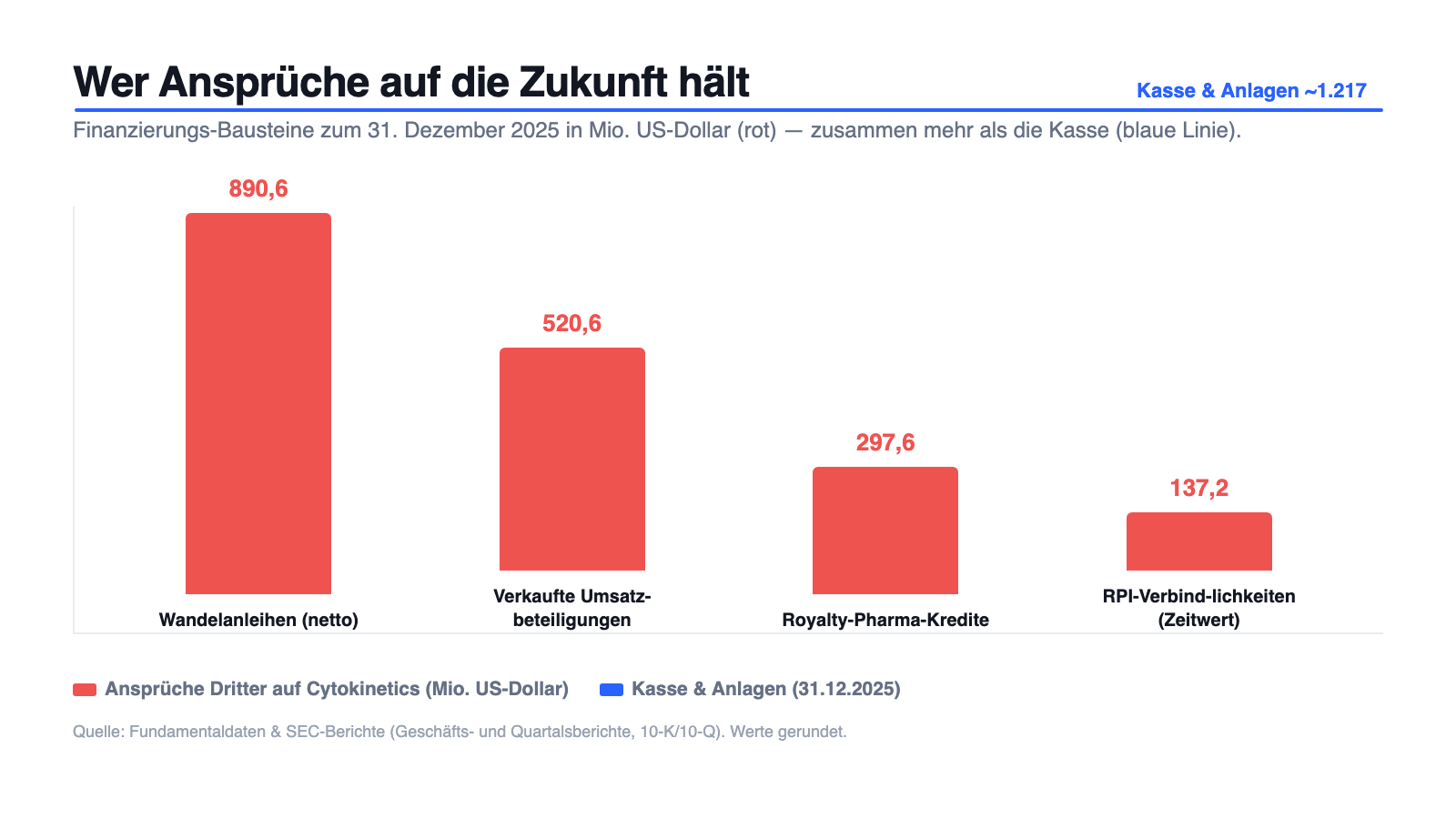

"As of December 31, 2025 and 2024 we had $1.3 billion and $0.8 billion of debt recorded on the balance sheet comprised of the Term loans […], Liabilities related to RPI Transactions measured at fair value, and the Convertible Notes […]. Additionally we have liabilities related to revenue participation right purchase agreements of $520.6 million and $462.2 million at December 31, 2025 and 2024."

— Cytokinetics, SEC annual report 10-K 2025, Item 1A "Risk Factors" (Indebtedness)

Translated: alongside classic convertible notes (among them the 2031 notes at 1.75 percent with a conversion price around $68), Cytokinetics has taken money from the specialist investor Royalty Pharma — and in return assigned part of its future drug revenue. Concretely, Royalty Pharma secures 4.5 percent of worldwide aficamten revenue up to $5 billion. That is clever because it does not directly dilute shareholders like a capital increase. But it is also sold future: of every MYQORZO dollar that the record prices are betting on, part flows off to an investor before it reaches the company.

This is no acute maturity drama like at a classic zombie corporation — the large convertible notes run to 2027 and 2031, the royalty loans over ten years. But it is the reason the negative equity from truth no. 1 is not a pure accounting accident: Cytokinetics has pre-financed its future, and part of the earnings meant to justify today's price has already been promised to yesterday's financiers.

Uncomfortable truth no. 4: approval is not commercial success — and the incumbent is named Bristol Myers Squibb

The chart celebrates the approval as if the goal were reached. But an approval is the entry ticket to the market, not victory in it — and this market already has an established competitor sitting in it. The report says so unmistakably:

"MYQORZO competes with Camzyos® (mavacamten), a cardiac myosin inhibitor marketed by Bristol Myers Squibb, as a therapy for oHCM, along with generic therapies, specifically beta blockers and calcium channel blockers, which are currently considered first-line standard of care."

— Cytokinetics, SEC annual report 10-K 2025, Item 1 "Business — Competition for MYQORZO"

Two things you should keep apart here. First, the opportunity: per the report, the oHCM market is served by about 10,000 cardiologists in the United States — a concentrated specialist field that a company with a lean, specialized sales force can target deliberately. Cytokinetics does not have to build a mass pharmacy but to convince a few thousand doctors. Second, the risk: Bristol Myers Squibb is in the market before Cytokinetics with Camzyos, knows the doctors, has reimbursement sorted out — and beta blockers and calcium channel blockers are dirt cheap as first-line therapy. All the lovely revenue the valuation is betting on must therefore first be wrested from an established brand rival and from penny generics. On top come further contenders (among them Edgewise, Lexicon, Tenaya) working on competing compounds. Growth that still has to be conquered against an incumbent is never as certain as an approval date makes it look.

Valuation: $10.9 billion market value — for a promise that is only just becoming revenue

In early July 2026 the Cytokinetics stock cost about $81; at about 123 million shares that makes a market value of about $10.9 billion (data as of July 8, 2026). The usual valuation measures deliberately work poorly here: there is no price-to-earnings ratio (no profit), and a price-to-sales ratio would be absurdly high because product revenue is only just beginning at a few million per quarter. So what you buy when you buy this stock is not an ongoing business but a bet on commercialization: that MYQORZO becomes a hundreds-of-millions or billion-dollar product in the coming years, that ulacamten and omecamtiv follow — and that all of it grows faster than the half billion the company burns every year, minus the 4.5 percent that go to Royalty Pharma. The analyst consensus (about 21 houses) is on average confident, with a clear buy leaning — but that is the "professionals' view" of a future scenario, not a certainty. With a stock near its all-time high, plenty of success is already priced in; the drop height arises where expectations already stand high. That is exactly why the stock moves so vigorously: about 149 percent up over twelve months, but with a daily swing range of around four percent (all figures: data as of July 8, 2026).

Opportunities and risks at a glance

What speaks for Cytokinetics:

- First approval after more than 20 years: MYQORZO (aficamten) has been approved against oHCM since December 2025 (United States, China) and February 2026 (EU) and has been on sale since the first quarter of 2026 — in the first quarter of 2026 the first product revenue in company history flowed in at $4.8 million (annual report 10-K 2025, quarterly report 10-Q Q1 2026).

- Solid cash and no going-concern doubt: about $1.1 billion in cash and investments (31.03.2026), an unqualified audit opinion, funds sufficient per the company "for at least the next 12 months" — unlike many stocks in the same warning scanner.

- Focused platform with a pipeline behind it: aficamten also in a trial against the non-obstructive form (nHCM, ACACIA-HCM), plus ulacamten (HFpEF) and omecamtiv mecarbil (HFrEF) — all on the same, deeply understood muscle mechanics.

- Concentrated target market: oHCM is served, per the report, by about 10,000 U.S. cardiologists — a specialist field a lean sales force can work deliberately.

- Tailwind from market and professionals: Weinstein Stage 2, power trend, institutional accumulation, about 149 percent price gain over twelve months and an on-average buy-leaning analyst consensus (about 21 houses).

What speaks against it:

- Two decades without a single profitable year: about $3.7 billion in accumulated deficit, equity of minus $826.6 million (31.03.2026) — that is what the distress label hangs on, and the approval changes nothing about it at first.

- The cash burn keeps running: $785.0 million net loss and $510.0 million operating cash outflow in 2025, another $145.5 million in Q1 2026 alone — the company remains dependent on the capital market.

- Sold future: about $1.3 billion of debt plus $520.6 million in assigned revenue participations; Royalty Pharma collects 4.5 percent of every dollar of worldwide aficamten revenue up to $5 billion.

- Commercial fight against an incumbent: in the oHCM market MYQORZO meets the established Camzyos (mavacamten) from Bristol Myers Squibb and cheap generics (beta blockers, calcium channel blockers) as first-line standard.

- High expectations are priced in: price near the all-time high, market value $10.9 billion with product revenue only just beginning; early-warning systems: Altman Z minus 7.25, Piotroski 3 of 9, five distress flags, fundamental rating D (data as of July 8, 2026).

A human conclusion

Back to the winner's reflex from the start. It has a kernel of truth: at Cytokinetics something big really did happen — the first approval after more than two decades, the transition from pure lab to company with a product. But this is exactly where the thinking error sits that this case can show you: neither the red warning label nor the green chart thinks for you. The red "going concern" label is a mechanical smoke detector that goes off here on two decades of losses and negative equity — not on a fire; the till is full, the auditor is silent, that is the honest resolution. Conversely, the celebration curve tempts you to treat the hard part as done. But it is not: the cash burn runs on, part of the future is sold to Royalty Pharma, and the real competition for every MYQORZO dollar against Bristol Myers Squibb is only just beginning. Cytokinetics is thus neither a bankruptcy candidate nor a sure thing but a bet with clear conditions: it pays off if commercialization grows faster than the half-billion annual burn — and it goes wrong if the market arrives more slowly than the chart promises, because then high expectations meet a company that still has to refuel with capital. Both stand in the same report, only a few pages apart. Anyone who buys in here should do so because they have understood the bet — not because the chart is so nicely green or the warning label looks so nicely dramatic. What you make of it is your decision. And that is exactly as it should be.

Sources

All original documents used in this analysis — to read for yourself:

- Cytokinetics, Incorporated — SEC annual report 10-K for 2025 (filed February 26, 2026)

- Cytokinetics, Incorporated — SEC annual report 10-K for 2024 (filed February 27, 2025)

- Cytokinetics, Incorporated — SEC quarterly report 10-Q as of March 31, 2026 (filed May 5, 2026)

- Cytokinetics, Incorporated — SEC quarterly report 10-Q as of September 30, 2025 (filed November 5, 2025)

- Cytokinetics, Incorporated — SEC quarterly report 10-Q as of June 30, 2025 (filed August 7, 2025)

- Cytokinetics, Incorporated — SEC quarterly report 10-Q as of March 31, 2025 (filed May 6, 2025)

- Cytokinetics' complete SEC filing history: EDGAR overview (sec.gov)

- Fundamental data (metrics, quarterly series, valuation; data as of July 8, 2026), reconciled with the SEC filings.

- Screener and rating data: in-house stock scanner (data as of July 8, 2026).

Transparency & disclaimer: This analysis is a journalistic contextualization of publicly available information and is not investment advice, not a financial analysis in the regulatory sense, and not a solicitation to buy or sell securities. It expressly contains no judgment on whether an insolvency will occur or whether a drug will be commercially successful. Stock investments carry substantial risks up to total loss — especially so with biopharma stocks. All information without guarantee; the data cut-off is noted in the text in each case. The author holds no position in Cytokinetics stock at the time of publication.

Our Bottom Line at a Glance

- Product & pipeline positive

- After more than 20 years of research, the first approval: MYQORZO (aficamten) against oHCM (US/China 12/2025, EU 02/2026), first product revenue in the first quarter of 2026 ($4.8 million). Behind it a focused platform on the same muscle mechanics (ulacamten, omecamtiv mecarbil) and a concentrated target market of about 10,000 U.S. cardiologists.

- Going concern & liquidity neutral

- About $1.1 billion in cash (31.03.2026), an unqualified audit opinion, no going-concern qualification — markedly more solid than many stocks in the same warning scanner. At the same time the company keeps burning ($510.0 million operating cash outflow in 2025, $145.5 million in Q1 2026) and remains dependent on fresh capital.

- Balance sheet & loss history negative

- Two decades without a profitable year: about $3.7 billion in accumulated deficit, equity of minus $826.6 million (31.03.2026), a net loss of $785.0 million (2025). That is exactly what Altman Z minus 7.25, Piotroski 3 of 9 and the distress label hang on — yesterday's accounting, not tomorrow's solvency.

- Financing & dilution negative

- About $1.3 billion of debt from convertible notes and Royalty Pharma loans plus $520.6 million in sold revenue participations; Royalty Pharma collects 4.5 percent of every dollar of worldwide aficamten revenue up to $5 billion. Part of the earnings meant to justify the price is already given away.

- Market, competition & momentum neutral

- Price near the all-time high, Weinstein Stage 2, power trend, institutional accumulation, about 149 percent up over twelve months and a buy-leaning analyst consensus (about 21 houses). Against it stands real competition: MYQORZO faces the established Camzyos (mavacamten) from Bristol Myers Squibb and cheap generics — approval is the starting line, not the finish line.

Cytokinetics is the rare counterpart to a bankruptcy drama: a $10.9 billion company whose going-concern warning signal stems from two decades of losses and negative equity — not from an acute shortage of money. The till holds about $1.1 billion, the auditor signed off without reservation, and with MYQORZO the first product revenue is just flowing. Against that stand an ongoing annual burn of about half a billion, revenue participations sold to Royalty Pharma, and the commercial fight against Bristol Myers Squibb's Camzyos. Not investment advice.

What Our Rating Means

- If you don't own the stock

- As long as the question raised in the bottom line stays open, we see no basis for an entry.

- If you hold it in your portfolio

- Our findings offer no acute reason to sell — the checkpoints named remain decisive.

A journalistic assessment by our editorial team at the time of the deep dive, based on public sources — not investment advice and not a solicitation to buy or sell. Your personal circumstances (investment goals, risk capacity, taxes) cannot be taken into account. What our categories mean, how verdicts are formed, and what conflicts of interest exist →

Worth Noting

- The scanner's going-concern proxy is a quantitative approximation from balance-sheet ratios; at Cytokinetics it is expressly NOT backed by an auditor's qualification (unlike, for instance, Replimune). The assignment to the warning scanner was confirmed locally and live on July 14, 2026.

- All earnings and balance-sheet figures come from the audited annual report 10-K for 2025 and the quarterly report 10-Q as of March 31, 2026; the 2025 net loss includes a one-off item of $121.2 million from the early exchange of convertible notes.

- Price and valuation figures are dated to July 8, 2026 (about $81, about 123 million shares); analyses are evergreen, daily prices are not a buy argument.

Frequently Asked Questions

Cytokinetics (NASDAQ: CYTK) of South San Francisco is a biopharma company that acts on the mechanics of heart-muscle contraction. Its first approved drug, MYQORZO (aficamten), relaxes the overactive heart muscle in obstructive hypertrophic cardiomyopathy (oHCM). Further candidates (ulacamten, omecamtiv mecarbil) target related forms of heart failure.

Because the filter reacts mechanically to balance-sheet ratios: about $3.7 billion in accumulated deficit, negative equity (minus $826.6 million) and negative interest coverage. Unlike some other stocks in the same scanner, however, there is NO going-concern qualification from the auditor behind it — the till holds about $1.1 billion. Here the proxy is a false alarm, not genuine going-concern doubt.

As of March 31, 2026, about $1.1 billion in cash and investments sat in the till (end of 2025: $1.2 billion). Against that stands an operating cash outflow of $510.0 million in 2025 and $145.5 million in the first quarter of 2026. The company writes that the funds are sufficient "for at least the next 12 months"; a going-concern qualification is absent.

Yes. The FDA and the Chinese authority approved MYQORZO in December 2025 against obstructive hypertrophic cardiomyopathy (oHCM), and the EU followed in February 2026. The first prescriptions started in late January 2026, and in the first quarter of 2026 Cytokinetics booked its first product revenue ever at $4.8 million.

Royalty Pharma has financed Cytokinetics over the years — with loans and, crucially, by buying revenue participations. Against payments of up to $150 million, the investor secured the right to 4.5 percent of worldwide aficamten revenue up to $5 billion. So part of every MYQORZO dollar flows off to Royalty Pharma.

No. In the SEC filings analyzed there is no AI product and no material use of AI in the business model — artificial intelligence is mentioned only in passing as a cybersecurity risk. In our company-specific AI classification, Cytokinetics is therefore rated "Neutral": the business revolves around heart-muscle mechanics, not AI.

This analysis expressly issues no insolvency verdict — and the facts speak against it: no going-concern qualification, an unqualified audit opinion, about $1.1 billion in cash and product revenue that is just beginning. At the same time the company keeps burning about half a billion a year and remains dependent on the capital market. The distress label reflects the loss history, not an acute risk of bankruptcy.

Found an error?

Did you spot a factual error, an outdated number, or a typo in this deep dive? Let us know briefly — your report goes straight to the editorial team.