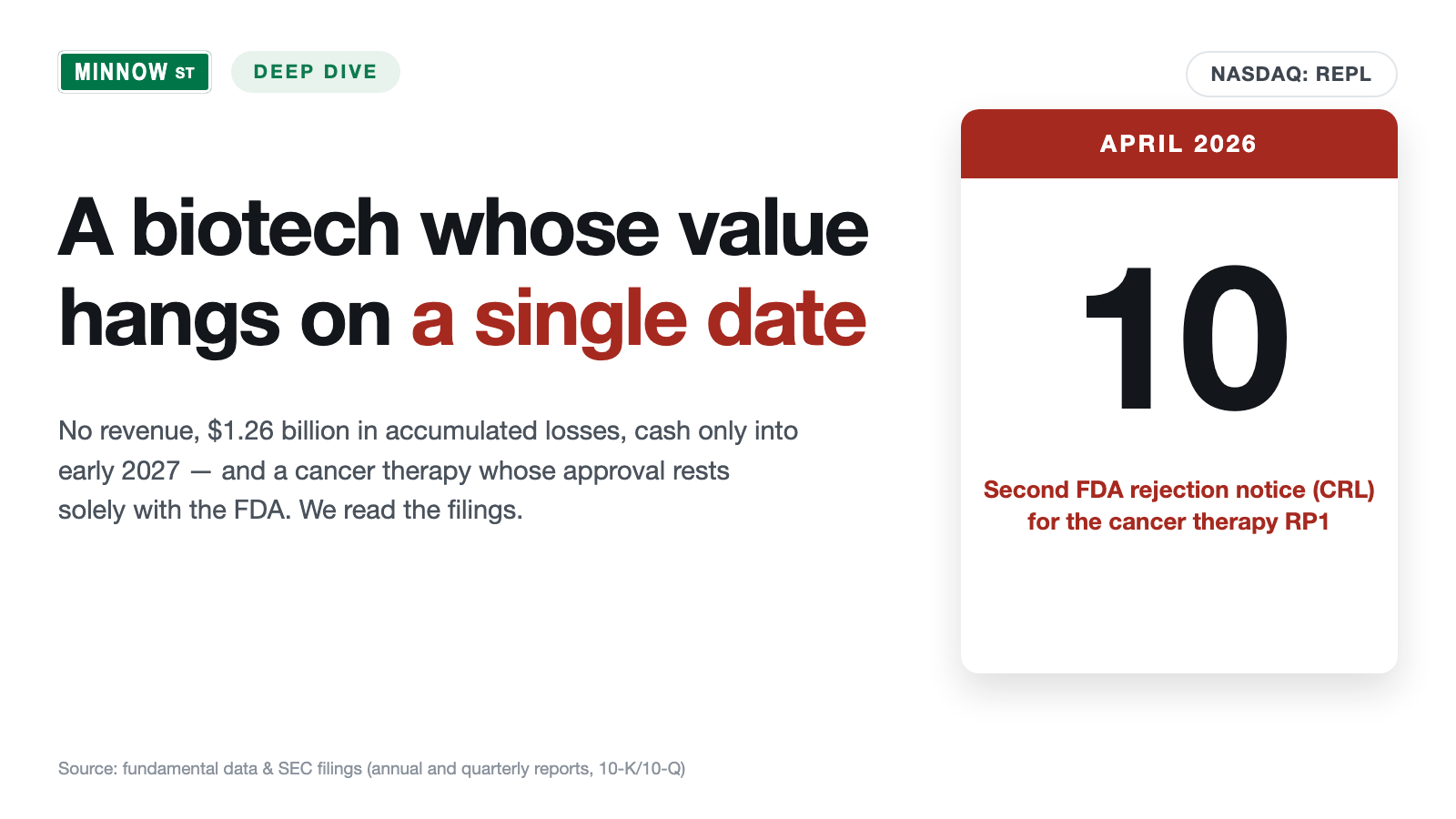

Replimune Stock: The Auditor Doubts the Company Will Survive — and the Market Bets on the Cancer Approval Anyway

Replimune builds viruses meant to blow tumors open from the inside — one of the most exciting ideas in cancer medicine. Only, the company earns not a single dollar from it so far. The stock shows up in our going-concern warning scanner, and its own annual report confirms exactly that: we read the 10-K for fiscal year 2026 and the quarterly report (10-Q) — $1.26 billion in accumulated losses, a till that per the auditor lasts only into early 2027, an explicit doubt about survival, and two FDA rejections for the cancer therapy RP1. Still the price jumped 153 percent in two months. Not investment advice — just a sober cash count before the big date.

There is a mental trap that strikes especially eagerly at biotech stocks: let's call it the lottery-ticket reflex. In front of you lies a ticket with an enormous jackpot — a company whose drug, if it gets approved, could multiply the share price. And because the jackpot shines so brightly, you see only the winning number, not the many blanks beside it. Hardly any company plays on this reflex right now as vividly as Replimune Group (NASDAQ: REPL): a biotech that builds living cancer drugs out of herpes viruses, whose stock has jumped 153 percent in just two months — and which nonetheless shows up in our warning scanner for going-concern doubt. So let's make a deal: before you let the shine of the ticket dazzle you, we read together what Replimune itself reported to the U.S. securities regulator, the SEC — in the annual report (10-K) for the fiscal year ended March 31, 2026 and in the quarterly report (10-Q). An SEC filing is honest under penalty of law. And in it stands a sentence from its own auditor that you should have read. In the end, you decide for yourself.

What Replimune actually does

Picture your immune system as a factory security team that normally spots intruders reliably — but cancer cells camouflage themselves well and simply get waved through. This is exactly where Replimune comes in, a clinical-stage biotech company from Woburn near Boston. Clinical-stage means: it researches and tests, it sells nothing yet. Its field is oncolytic immunotherapy — a clunky term for a vivid idea: trained viruses that blow tumors open from the inside and at the same time alert the security team. For this the company takes a disarmed strain of the herpes simplex virus (HSV-1), packs in additional blueprints for immune-activating proteins and injects this "living drug" directly into the tumor. Two effects are meant to come together: the virus kills the tumor cell directly — and the released fragments plus the built-in signaling substances call the immune system onto the scene, which is then supposed to attack distant metastases too. Replimune calls this technology family its RPx platform.

The great hope is called RP1 (drug name vusolimogene oderparepvec), with a second candidate RP2 behind it. The decisive trial, IGNYTE, tests RP1 against advanced melanoma (black skin cancer) — in combination with nivolumab, an established immune drug that the pharma giant Bristol Myers Squibb contributes to the trial free of charge. Sounds like an elegant bet on the future? Perhaps it is. But note here already the central tension of this analysis: one of the most exciting ideas in cancer medicine — carried by a company without a cent of revenue, whose cash has an expiry date and whose entire worth hangs on a single regulatory decision. It runs through every chapter. How differently such "single-product bets" can turn out is shown, for comparison, by our analysis of Outlook Therapeutics — there too, the FDA alone decides between triumph and ruin.

Where the stock shows up in our scanner

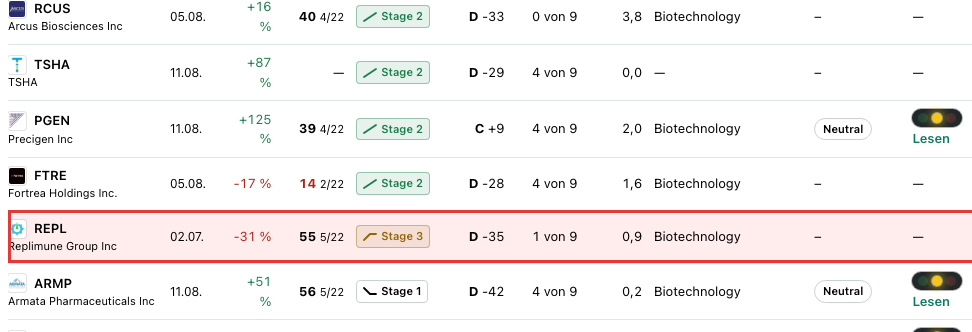

Every day we run about 3,500 stocks through our scanners. Replimune registers in a telling mix (data as of July 8, 2026). On the warning side stands the "Going Concern (Distress-Proxy)" — a filter that looks for the classic signs of a shaky balance sheet: an Altman Z-score in the danger zone, interest coverage below one, negative operating cash flow. The Altman Z-score, a classic early-warning gauge of insolvency built from several balance-sheet ratios, sits deep in the red for Replimune; the Piotroski F-Score, a nine-point test of balance-sheet quality, stands at 1 of 9 — a rock-solid company sits at 8 or 9. And the best part (in the sense of: the most remarkable): this scanner is explicitly only a quantitative approximation, not the real auditor's note. But at Replimune the suspicion matches the original — the auditor actually wrote the going-concern doubt into the opinion. Rarely do smoke detector and fire brigade agree so precisely. How such warning lists are to be read — a smoke detector, not a demolition order — we explained in the piece "Insolvency Radar: the Top 10".

And now the contradiction that makes this stock so special: on the other side stands a momentum frenzy. The price trades above the 50- and the 200-day line, it has risen about 29 percent in one month and 153 percent in two months, it sits 642 percent above its 52-week low — and at the same time still 79 percent below its all-time high. Exactly this altitude rush is flagged by two further scanners as a warning, not an invitation: Weinstein Stage 3 classifies the stock as a topping formation (an uptrend losing steam), and the scanner "Overheated (Webby RSI)" reports a price that has moved too far from its own average line. Translated: the market has bet on something — more on that shortly — but the rally itself already bears the signs of exhaustion. A price firework next to a going-concern note is no proof of a bargain, but a price tag for a bet.

The numbers over the years — honestly appraised

With a clinical-stage biotech you have to be honest: there is no revenue curve to admire, because there is no revenue. Replimune has earned not a single dollar from a product since its inception — that is not a weakness to be hidden, but the nature of the thing: the company is a large research lab working against the clock. What there is to appreciate, then, is the progress of the program — and that has its price. The net loss (in the report "net loss") has grown ever larger as the trials advanced: from $66.6 million (fiscal year to March 2024) via $247.3 million (to March 2025) to $313.9 million (to March 2026). In three years the loss has thus more than quadrupled. The biggest chunk is research itself: $221.2 million in research and development spending in the last fiscal year, plus $98.7 million for administration and commercial preparation.

Adding up all losses since the company's existence, an accumulated deficit of $1,262.5 million stands in the books (March 31, 2026) — more than the company's entire market weight. This was financed almost exclusively through the sale of new shares: since the IPO in July 2018, Replimune has raised about $1,132.9 million net through capital increases. That is the second side of the biotech coin you should remember: every advance is paid for with fresh shares — and your slice of the cake shrinks when new slices are cut off all the time. Which brings us to the uncomfortable truths.

What the filings say — the uncomfortable truths

Uncomfortable truth no. 1: the company's own auditor doubts its survival

There is hardly a harder signal in an annual report than this. An auditor normally confirms soberly that the numbers are correct. In rare cases, though, it adds a warning — the going-concern note, meaning: doubt about the company's continuation. That is exactly what happened at Replimune. The company writes itself:

"Based on its current operating plan, the Company expects to continue to generate operating losses for the foreseeable future and that its existing cash, cash equivalents and short-term investments will be sufficient to fund its operating expenses and capital expenditure requirements only into the first calendar quarter of 2027, which is less than one year from the date these consolidated financial statements are issued. […] These conditions raise substantial doubt about the Company's ability to continue as a going concern."

— Replimune Group, SEC annual report 10-K 2026, Note 1 "Going Concern"

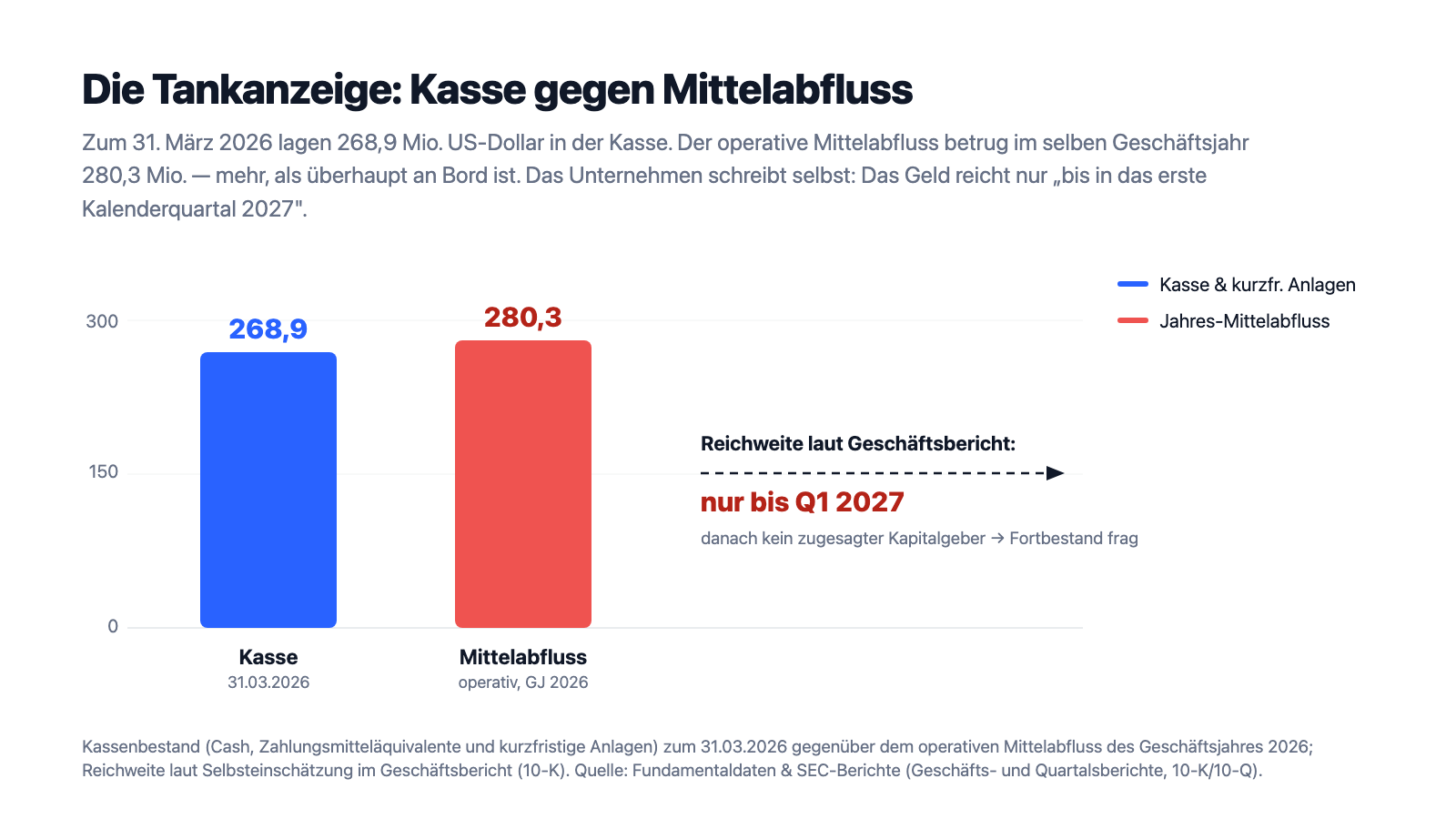

The bare arithmetic behind it is quickly told: as of March 31, 2026, $268.9 million in cash and short-term investments sat in the till. In the same fiscal year, though, $280.3 million flowed out of operations alone — more than is on board at all. A fuel gauge that drops into the red the moment you glance at the next stretch of road:

To be fair: a going-concern note is not a bankruptcy filing. It means: "Without fresh money in the next twelve months, things get tight." And Replimune has a real lever to raise money — including issuing more shares. But that is precisely the point: the way out of the cash squeeze is dilution, and the capital market's willingness to give fresh money to a biotech with two FDA rejections in turn hangs on exactly the decision around which everything revolves.

Uncomfortable truth no. 2: no revenue — the entire worth is a bet on a single approval

It is the sentence that frames everything at a clinical-stage biotech, and Replimune places it right at the start of its risk chapter:

"We have no products approved for commercial sale and have not generated any revenue from product sales to date, and we continue to incur significant research and development and other expenses related to our ongoing operations. […] The size of our future net losses will depend, in part, on our future expenses and our ability to generate revenue, if any."

— Replimune Group, SEC annual report 10-K 2026, Item 1A "Risk Factors"

For the valuation this has a radical consequence: the metrics you measure normal companies with run into the void here. There is no price-to-earnings ratio (no profit), a price-to-sales ratio is meaningless (no revenue). What you buy when you buy this stock is not an ongoing business but a warrant on an approval: if it comes, RP1 can address a billion-dollar market and today's price looks tiny in hindsight. If it doesn't come, what remains is a company with an empty till, billions in accumulated losses and a drug without market access. And whoever prices in the future alone should take away this reminder: a ticket without revenue is worth as much as the market currently believes in the jackpot — and that belief can halve or double in a single day.

Uncomfortable truth no. 3: two FDA rejections — and the whole case hangs on one date

With that we are at the heart of the matter. The reason the stock first crashed and then exploded has a name: Complete Response Letter (CRL) — the rejection notice from the U.S. drug regulator FDA, with which it turns down a marketing application in its current form. Replimune received not one of these, but two. The timeline reads like a screenplay of constant twists — and it stands like this in the annual report:

"On April 10, 2026, the FDA issued a second CRL for the RP1 BLA for the treatment of advanced melanoma. The second CRL reiterated points made in the first CRL that were presumably addressed by the FDA accepting the BLA for resubmission… On June 26, 2026 we announced the FDA accepted the BLA resubmission as a Class 1 resubmission with an action date of August 2, 2026. The FDA also stated that they would convene an advisory committee meeting in late July 2026."

— Replimune Group, SEC annual report 10-K 2026, Item 1A "Risk Factors"

Take a moment to sort this out, because it explains the entire share price. July 2025: first CRL, the stock crashes. October 2025: the FDA accepts a resubmission, action date April 10, 2026. April 10, 2026: instead of approval a second CRL — the crash deepens. May/June 2026: the company reports it has agreed with the FDA on a path forward, the agency will treat the application "as a priority" — and on June 26 accepts the resubmission with the new action date of August 2, 2026. That is the spark that lit the 153 percent rally: the market revived its hope. But read the fine print along with it: the second notice even contradicted, per the company, a position the FDA itself had taken in the autumn of 2025. With a binary approval bet, not only the outcome is open — but at times even the rules of the game. For you, soberly, that means: on or around August 2, 2026 the value of this stock can change abruptly, in both directions. That is not a forecast but the description of an event risk.

Uncomfortable truth no. 4: the survival austerity program — 55 percent fewer staff

How serious the situation is you recognize not from words but from deeds. As of March 31, 2026, Replimune had 465 employees. A few weeks later management reached for the harshest cost brake a research company knows:

"In April 2026, we implemented a plan for a restructuring, which included a reduction of our workforce by approximately 55%. Without a near-term accelerated approval of our BLA for RP1 plus nivolumab for the treatment of advanced melanoma, we may be required to initiate a further reduction in our workforce."

— Replimune Group, SEC annual report 10-K 2026, "Human capital" / Risk Factors

More than every second job — and the open threat of a further reduction should the approval fail to come. That is the flip side of the cash squeeze from truth no. 1: to stretch the runway, Replimune is shrinking itself to the bare minimum. For the till that is sensible. For the substance of a research company it is a bloodletting — the people who push the next drug candidates forward are largely gone. A company that simultaneously fights for its twelve-month liquidity and lays off more than half its staff tells you, more clearly than any metric, how much currently hangs on that one regulatory decision.

Valuation: about $0.92 billion market value — for a ticket without revenue

In early July 2026 the Replimune stock cost about $11; that makes a market value of about $0.92 billion (data as of July 8, 2026). The usual valuation measures deliberately fail here: no price-to-earnings ratio (no profit), no meaningful price-to-sales ratio (no revenue). The most honest framing is a juxtaposition: against the market value of $0.92 billion stand an accumulated deficit of $1.26 billion and a cash balance of $0.27 billion that, per the auditor, does not even last a year. Put differently: you are paying not for what is, but solely for what could be. This is exactly why the price moves so extremely — plus 153 percent in two months, minus 79 percent against the all-time high, plus 642 percent above the 52-week low (all figures: data as of July 8, 2026). Remarkable is that about 97 percent of the shares are in the hands of institutions: this is no pure retail game, but a bet in which professional money is seated too — which tends to amplify the swing in both directions rather than dampen it. With such warrant-like securities the rule is: small news, large price swings.

Opportunities and risks at a glance

What speaks for Replimune:

- One of the most exciting ideas in cancer medicine: oncolytic immunotherapy on its own RPx platform (HSV-1), with RP1 as lead drug in the IGNYTE trial against advanced melanoma — combined with nivolumab, which Bristol Myers Squibb contributes free of charge (annual report 10-K 2026).

- A tangible, near-term trigger: after two rejection notices, the FDA accepted the resubmission on June 26, 2026 with an action date of August 2, 2026 and intends to treat the application "as a priority" — an approval would open RP1 access to a billion-dollar market.

- The capital structure is not crushed by bank debt: the going-concern doubt stems from the cash burn, not from maturing loans — fresh equity (for instance via the ongoing share-issuance program) is a real, if dilutive, way out.

- The professional money is on board: about 97 percent of the shares are held by institutions; the stock jumped 153 percent in two months after the June news — the market considers a positive scenario possible.

What speaks against it:

- The auditor has issued a going-concern note: the cash ($268.9 million) lasts, per the company, only into the first calendar quarter of 2027, against an operating cash outflow of $280.3 million in fiscal year 2026 and with no committed further financing.

- Not a cent of product revenue since inception; accumulated deficit $1,262.5 million; the net loss more than quadrupled in three years from $66.6 to $313.9 million — the entire worth is a bet on an approval.

- Binary regulatory risk: two FDA rejection notices (July 2025, April 2026); the second even contradicted, per the company, an earlier FDA position. Around the August 2, 2026 date, abrupt price moves in both directions are possible.

- Survival austerity program with about 55 percent job cuts (April 2026) and the threat of further reductions; ongoing dilution via share issuances, plus 14 million pre-funded warrants overhanging the price. Early-warning systems: Altman Z deep in the red, Piotroski 1 of 9, fundamental rating D (data as of July 8, 2026).

A human conclusion

Back to the lottery-ticket reflex from the beginning. It has a true core: Replimune's idea is real, and the jackpot — an approved, effective virus therapy against cancer — would be enormous. But this is exactly where the fallacy sits that this case can show you: a glowing jackpot does not make the blanks any rarer. At Replimune both sides stand unusually clearly next to each other, only a few pages apart in the same report: the chance of an approval with a tangible date of August 2, 2026 — and an auditor who doubts survival in black and white, a till running empty, two regulatory rejections and a halved staff. That does not make Replimune a "bad" or a "good" company, but a bet with clear conditions: whoever enters here buys neither substance nor earnings, but the probability of a single yes or no. If the yes comes, the slim market value can lever far upward — the 153 percent in two months hinted at how fast that goes. If the no comes, it hits a company already working at its cash limit. Both are possible, neither is certain. Whoever takes this bet should do it because they have understood its conditions — not because the ticket shines so brightly. What you make of it is your decision. And that is exactly as it should be.

Sources

All original documents used in this analysis — to read for yourself:

- Replimune Group, Inc. — SEC annual report 10-K for the fiscal year ended March 31, 2026 (filed June 29, 2026)

- Replimune Group, Inc. — SEC annual report 10-K for the fiscal year ended March 31, 2025 (filed May 22, 2025)

- Replimune Group, Inc. — SEC quarterly report 10-Q as of December 31, 2025 (filed February 3, 2026)

- Replimune Group, Inc. — SEC quarterly report 10-Q as of September 30, 2025 (filed November 6, 2025)

- Replimune Group, Inc. — SEC quarterly report 10-Q as of June 30, 2025 (filed August 7, 2025)

- Replimune's complete SEC filing history: EDGAR overview (sec.gov)

- Fundamental data (metrics, quarterly series, valuation; data as of July 8, 2026), reconciled with the SEC filings.

- Screener and rating data: in-house stock scanner (data as of July 8, 2026).

Transparency & disclaimer: This analysis is a journalistic contextualization of publicly available information and is not investment advice, not a financial analysis in the regulatory sense, and not a solicitation to buy or sell securities. It expressly contains no judgment about whether an insolvency occurs or whether an approval is granted. Stock investments carry substantial risks up to total loss — with clinical-stage biotech stocks to a particular degree. All information without guarantee; the data cut-off is noted in the text in each case. The author holds no position in Replimune stock at the time of publication.

Our Bottom Line at a Glance

- Technology & program positive

- Oncolytic immunotherapy on its own RPx platform (HSV-1) is one of the most exciting ideas in cancer medicine; the lead drug RP1 is tested in the IGNYTE trial against advanced melanoma, combined with nivolumab, which Bristol Myers Squibb contributes free of charge (annual report 10-K 2026).

- Going concern & liquidity negative

- The auditor has issued a going-concern note: the cash ($268.9 million as of March 31, 2026) lasts, per the company, only into the first calendar quarter of 2027, against an operating cash outflow of $280.3 million in fiscal year 2026 and with no committed further financing.

- Loss & revenue negative

- No product revenue since inception; the net loss rose in three fiscal years from $66.6 to $313.9 million, the accumulated deficit stands at $1,262.5 million — more than the entire market weight. The stock's value is entirely a bet on a future approval.

- Regulatory (FDA) neutral

- Two rejection notices (CRL) in July 2025 and April 2026 — the second contradicted, per the company, an earlier FDA position. On June 26, 2026 the FDA accepted the resubmission with an action date of August 2, 2026 and an advisory committee in late July 2026: a binary event with an open outcome.

- Market & momentum neutral

- Plus 153 percent in two months and plus 642 percent above the 52-week low, carried by the approval hope; about 97 percent institutional ownership. At the same time technical scanners rate the rally as a topping formation (Weinstein Stage 3) and "overheated" — an altitude rush next to a going-concern note.

Replimune is not a case of substance versus story, but a pure bet with clear conditions: a fascinating cancer technology and a tangible FDA date of August 2, 2026 on one side — on the other an auditor who doubts survival in black and white, not a cent of revenue, $1.26 billion in accumulated losses, two regulatory rejections and a workforce cut of about 55 percent. The stock is a warrant on a single yes or no. Not investment advice.

What Our Rating Means

- If you don't own the stock

- In our view, the documented risks clearly outweigh — we see no basis for an entry.

- If you hold it in your portfolio

- In our view, the findings carry enough weight to warrant a critical look at your own position.

A journalistic assessment by our editorial team at the time of the deep dive, based on public sources — not investment advice and not a solicitation to buy or sell. Your personal circumstances (investment goals, risk capacity, taxes) cannot be taken into account. What our categories mean, how verdicts are formed, and what conflicts of interest exist →

Worth Noting

- Replimune's fiscal year ends on March 31; annual figures refer to the respective fiscal year (e.g. "2026" = April 1, 2025 through March 31, 2026). Program and trial milestones, by contrast, the company reports on a calendar-year basis.

- All earnings and balance-sheet figures come from the audited annual report 10-K for the fiscal year ended March 31, 2026 as well as the quarterly reports; the FDA date status (August 2, 2026) is the status stated in the 10-K.

- Price and valuation figures dated to July 8, 2026 (about $11); analyses are evergreen, daily prices are not a buy argument.

Frequently Asked Questions

Replimune (NASDAQ: REPL) of Woburn, Massachusetts, is a clinical-stage biotech company for oncolytic immunotherapy: it builds "living drugs" out of a disarmed herpes virus (HSV-1) that are meant to destroy tumors directly and activate the immune system (RPx platform). The lead drug is RP1 against advanced melanoma (black skin cancer). The company does not yet sell any product and generates no revenue.

Because the classic distress signals apply: no revenue, high cash burn, Altman Z deep in the red. The decisive point is that the suspicion is confirmed by the original: the auditor issued a going-concern note on the 2026 annual report — "substantial doubt" about survival, because the cash, per the company, lasts only into the first calendar quarter of 2027.

As of March 31, 2026, $268.9 million in cash and short-term investments sat in the till. In fiscal year 2026, $280.3 million flowed out of operations. The company writes itself that the funds last "only into the first calendar quarter of 2027" and that there is no committed further source of financing — so fresh money must be raised.

A Complete Response Letter is the rejection notice of the U.S. drug regulator FDA: it cannot approve the marketing application in its current form. Replimune received two of them for the RP1 melanoma approval — in July 2025 and on April 10, 2026. On June 26, 2026 the FDA accepted a resubmission with an action date of August 2, 2026 and an expert hearing in late July 2026.

Because the price hangs on a single event: the FDA approval of RP1. After the second rejection notice in April 2026, the company reported a "path forward" in June with a new action date of August 2, 2026 — whereupon the stock jumped about 153 percent in two months. It is a hope rally, not a reaction to improved fundamentals; technical scanners already rate it as "overheated".

No. In the evaluated SEC filings there is no AI product and no material use of AI in the business model — artificial intelligence is mentioned only in passing as a general regulatory topic (the EU AI Act). In our company-specific AI classification, Replimune is therefore rated "Neutral": the business revolves around virus therapy, not AI.

This analysis expressly makes no insolvency verdict. The facts: the auditor reports "substantial doubt" about survival, the cash lasts, per the company, only into early 2027, and in April 2026 the workforce was cut by about 55 percent. At the same time there is no crushing mountain of bank debt, and an FDA approval of RP1 could open access to fresh capital and a billion-dollar market. The outcome is open.

Found an error?

Did you spot a factual error, an outdated number, or a typo in this deep dive? Let us know briefly — your report goes straight to the editorial team.