Arcus Biosciences: Why a Stock-Market Star With a Billion in the Bank Sits in the Insolvency Warning Scanner

Arcus builds drugs meant to teach the immune system to recognize cancer cells again — and the stock is a market darling: up 234 percent in a year, close to its 52-week high. Yet it blinks in our warning scanner "Going Concern (Distress-Proxy)". We read the annual report (10-K) for 2025 and the quarterly report (10-Q) as of March 31, 2026: not a cent of product revenue, $1.5 billion in accumulated losses — but also about $1.0 billion in cash, no doubt from the auditor about the company's survival, and in Gilead a billion-dollar partner that owns a quarter of the firm. Not investment advice — just an honest look in the till behind the red warning light.

There is a mental trap that wants to take the work off our hands — and deceives us in doing so: let's call it the label reflex. A red warning sign ("insolvency approaching!") makes us flinch; a green "+234 percent!" makes us give chase. Both times it is not the mind that decides, but the label. Hardly any stock demonstrates this reflex so beautifully right now as Arcus Biosciences (NYSE: RCUS): a cancer biotech whose stock has more than tripled in twelve months and trades close to its 52-week high — but which at the same time shows up in our warning scanner "Going Concern (Distress-Proxy)", among companies with serious balance-sheet worries. Green label, red label, the same stock. So let's make a deal: before you settle on either sign, we read together what Arcus itself reported to the U.S. securities regulator, the SEC — in the annual report (10-K) for 2025 and the quarterly report (10-Q) as of March 31, 2026. An SEC filing is honest under penalty of law. And there it says why the red warning light here means something different than at most distress candidates. In the end, you decide for yourself.

What Arcus actually does

Picture the immune system as a very good guard force that normally recognizes intruders reliably — but with which cancer cells camouflage themselves and simply get waved through. It is precisely this camouflage that Arcus Biosciences attacks, a clinical immuno-oncology company from Hayward near San Francisco. Clinical means: it researches and tests, it does not yet sell a single drug. Arcus builds several tools meant to make the tumors' camouflage visible to the guard force again — partly small, swallowable molecules, partly antibodies.

The most important candidate is called casdatifan, an oral inhibitor of the cell switch HIF-2-alpha, which plays a key role in renal cell cancer (technical term: ccRCC, clear-cell renal cell carcinoma). The decisive trial PEAK-1 tests casdatifan in combination with an established agent; the annual report puts the worldwide peak-sales opportunity at more than $2 billion — if everything works. Alongside it stand the antibody domvanalimab (it blocks the brake "TIGIT", the Phase 3 trial STAR-121 runs against lung cancer), the PD-1 antibody zimberelimab and the CD73 inhibitor quemliclustat against pancreatic cancer. A whole toolbox, then — of which none is yet approved.

And now the part that sets Arcus apart from most small biotechs: the partner. The pharma giant Gilead Sciences is deeply interwoven with Arcus — it holds about a quarter of the shares, sits on the board and finances almost all of the reported revenue through collaboration payments. Sounds like a safety net? In part it is. But note here already the central tension of this analysis: a well-financed market darling with a billion in cash and a strong partner — that nonetheless sits in an insolvency-approximation scanner because it (entirely as planned) earns no profit. It runs through every chapter. What a genuine balance-sheet emergency looks like in the same warning scanner is shown, for comparison, by our analysis of Replimune — there the auditor did in fact cast doubt on the company's survival. At Arcus, we can reveal this much, it did not.

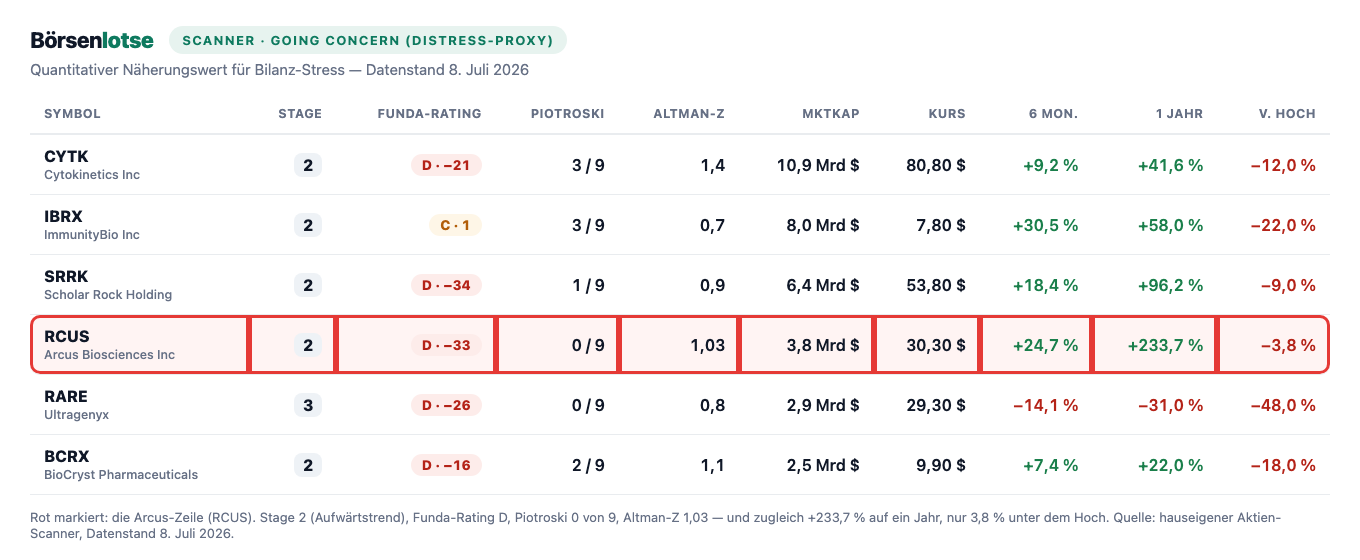

Where the stock shows up in our scanner

Every day we run about 3,500 stocks through our scanners. Arcus triggers a downright contradictory mix (data as of July 8, 2026). On the warning side stands the "Going Concern (Distress-Proxy)" — a filter that looks for the classic signs of a shaky balance sheet: interest coverage below one, negative operating cash flow, weak balance-sheet metrics. The fundamental rating stands at D, the Piotroski F-Score — a nine-point test of balance-sheet quality — at 0 of 9 (a fundamentally healthy company stands at 8 or 9), and the Altman Z-Score, a classic early warning of insolvency, sits at about 1.03 — the historical danger zone begins below 1.1. At first glance: a restructuring case.

And now the contradiction that makes this stock so instructive: on the other side, Arcus sits in a whole series of strength scanners. The price trades above its 50- and 200-day lines, the stock is in Stage 2 of Weinstein phase analysis (an intact uptrend), it is an RS leader with a relative-strength rating of 93, shows up in "near the 52-week high" (only 3.8 percent below the peak) and appears in "Pros 80%" because about 72 percent of the shares are held by institutions. Over twelve months the price has gained about 234 percent. Precisely this juxtaposition is the point: the distress proxy is, as the name says, an approximation — it measures quantitatively that a company yields no profit and burns cash. For a clinical biotech both are the normal state, not an alarm. How such warning lists are to be read — a smoke detector, not a demolition notice — we explained in the article "Insolvency Radar: the Top 10". Remember: a smoke detector that goes off while you cook reports smoke — not necessarily a fire.

The numbers over the years — honestly appraised

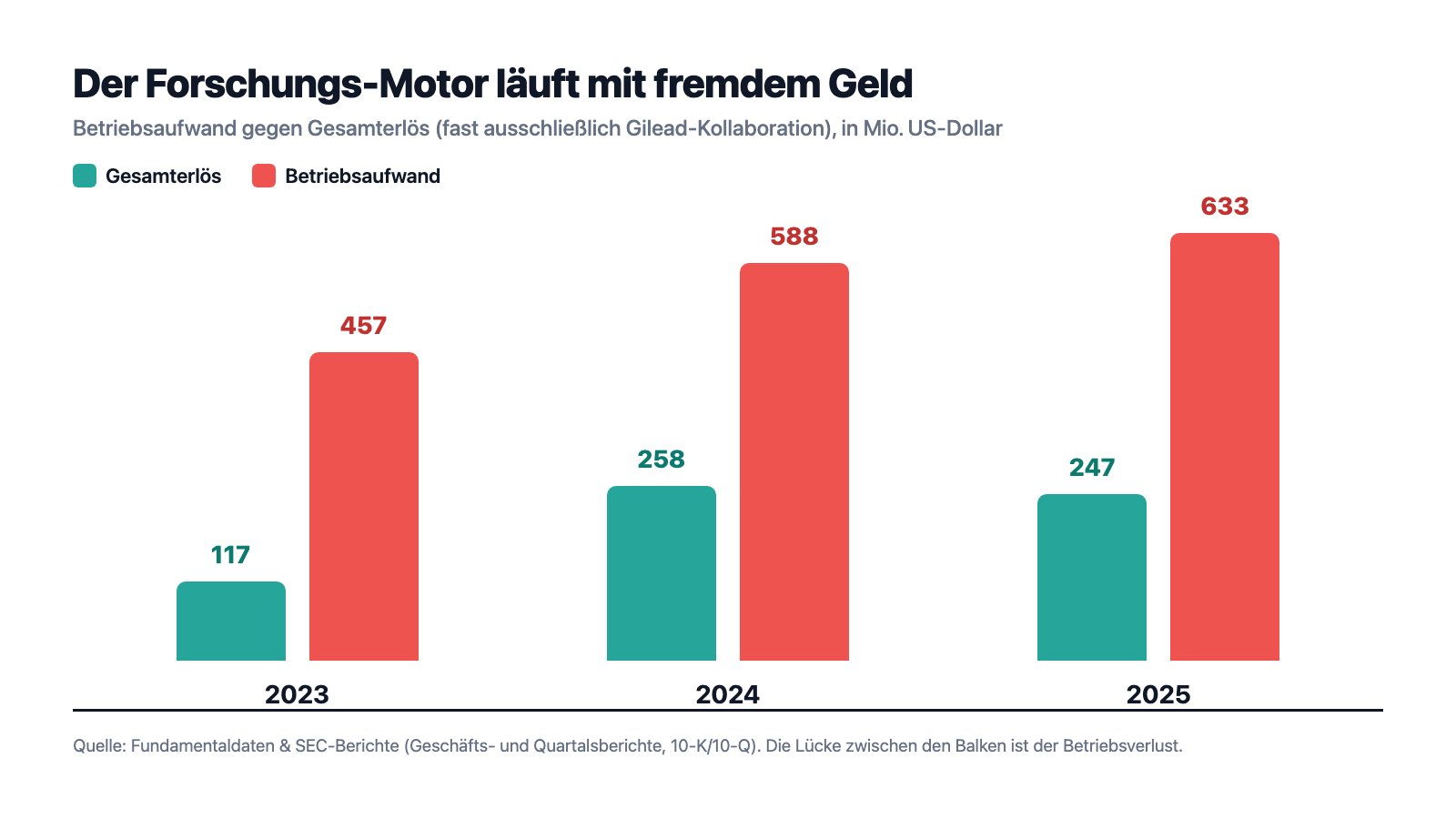

With a clinical biotech you have to be honest: there is no product-revenue curve to admire, because there is no product revenue. What Arcus reports as "revenue" is almost entirely collaboration payments — above all from Gilead, plus the Japanese partner Taiho. These proceeds therefore fluctuate with contract milestones, not with demand: $117 million (2023), $258 million (2024), $247 million (2025); of which from collaborations $80, $207 and $214 million. Against them stand the costs of research, and those know only one direction: research and development spending rose from $340 via $448 to $523 million, administration cost $110 million most recently. The gap between them is the operating loss — and fresh money has to fill it.

Below the line, red stood every year accordingly: a net loss of $307 million (2023), $283 million (2024) and $353 million (2025); in the first quarter of 2026 another $128 million was added (prior-year quarter: $112 million). Add up all the losses since the company's existence and an accumulated deficit of $1.5 billion stands in the books (December 31, 2025), which grew to $1.6 billion by March 31, 2026. That is the one side — and the distress proxy is right with this number. But it is only half the story. Remember the sentence that carries us through the next chapters: a loss becomes dangerous only when there is no money left to pay for it. Which brings us to the uncomfortable truths — and to the question of how full the till really is.

What the filings say — the uncomfortable truths

Uncomfortable truth no. 1: not a cent of product revenue — and the loss keeps growing

Let's start with the number that triggers the warning scanner. Arcus says it in its own risk disclosures as unmistakably as one can:

"We have a history of operating losses, have never generated any revenue from product sales and anticipate that we will continue to incur significant losses for the foreseeable future."

— Arcus Biosciences, SEC annual report 10-K 2025, Item 1A "Risk Factors"

That is the bare truth behind the D rating and the Piotroski 0 of 9: no revenue from the actual business, a loss that grows with every trial, no interest coverage (there is simply no operating profit from which anything could be covered). For a quantitative filter that is a crystal-clear warning signal — and for a clinical biotech it is at the same time simply the job description. The difference between "dangerous" and "normal" is decided not by this number, but by the next one.

Uncomfortable truth no. 2: the warning scanner is a false alarm here — the cash carries into 2028

Now comes the part a purely arithmetic distress filter cannot see. A genuine restructuring case has three hallmarks: an empty till, an auditor who doubts the company's survival (the notorious "going-concern qualification"), and no plan for how the next bill gets paid. Arcus has — none of the three. The company writes itself:

"As of December 31, 2025, we had $1.0 billion of cash, cash equivalents and marketable securities, which we believe will be sufficient to provide funding until at least the second half of 2028."

— Arcus Biosciences, SEC annual report 10-K 2025, Item 1A "Risk Factors"

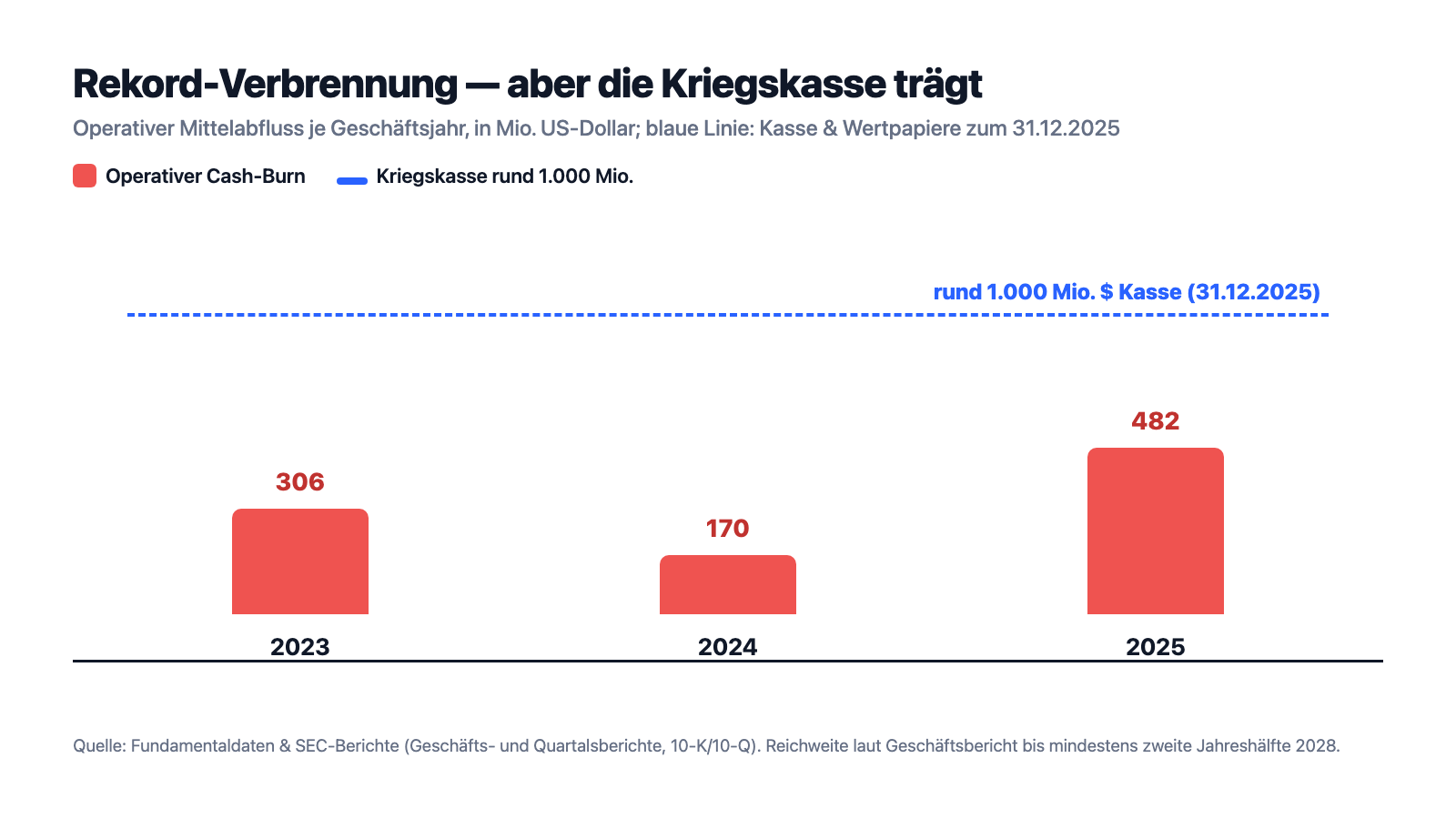

About $1.0 billion lay in the war chest at year-end 2025 ($992 million a year earlier); as of March 31, 2026 it was still $876 million. And yes, the burn is rising: operating cash outflow climbed from $306 million (2023) via $170 million (2024) to $482 million in 2025 — a record, driven by the expensive Phase 3 trials. But look at how this record burn relates to the cash:

That is the core of this analysis: the "Going Concern (Distress-Proxy)" is called precisely that — a proxy, an approximation. It reliably detects that a company burns cash and earns no profit. But it cannot tell whether an empty till lies behind it (then it is serious) or a billion in reserve and a billion-dollar partner (then it is the ordinary operation of a research lab). To stay honest: even a full till is finite. "Second half of 2028" is no promise of eternity, and every new trial costs — Arcus, like every biotech, will at some point have to raise fresh money again. But that is something fundamentally different from acute bankruptcy risk. The red warning light here is a smoke detector in the test kitchen, not a fire alarm.

Uncomfortable truth no. 3: a quarter belongs to Gilead — backbone and cluster risk in one

If the cash is not the real risk, then what is? The most honest answer stands in the chapter on ownership structure — and it is named Gilead Sciences. The pharma group is not only a partner, but a major shareholder with special rights:

"Gilead owns approximately 25.1% of our outstanding common stock, and we have appointed its three designees to our board of directors pursuant to the terms of the Investor Rights Agreement. As a result, these stockholders, acting together, have significant influence over all matters that require approval by our stockholders, including the election of directors and approval of significant corporate transactions."

— Arcus Biosciences, SEC annual report 10-K 2025, Item 1A "Risk Factors"

That is the double edge you should have understood. The opportunity: Gilead is a deep-pocketed, experienced partner that, through collaboration and option payments, supplies almost all revenue — $214 of $247 million in 2025 came from collaborations — and helps carry the expensive late-stage trials. Without this partner the till would be nowhere near as comfortable. The risk: a single partner that is at the same time a major shareholder and sits on the board is a cluster risk — if your neighbor told you his business was going great, but a single customer accounted for half his revenue and also sat on his advisory board, you would swallow hard for a moment. Gilead's interests and those of minority holders run in parallel as long as both want the same thing. What happens when they don't stands in the next truth.

Uncomfortable truth no. 4: if Gilead says no to a program, Arcus stands alone

The dependence has a concrete mechanism, and the annual report names it openly. Gilead holds option rights to the Arcus programs — the right to take over a program at a later date and co-finance it, or not. That sounds like flexibility, but it has an uncomfortable flip side for Arcus:

"Given the breadth of the collaboration with Gilead, our ability to form new collaborations in the future will be limited. If Gilead declines to exercise its option to a program, we may need to enter into new collaborations for such programs with companies that have more resources and experience than us."

— Arcus Biosciences, SEC annual report 10-K 2025, Item 1A "Risk Factors"

Translated, that means: the close tie to Gilead makes Arcus less freely available to other major partners — and if Gilead waves off a program, that is doubly expensive. First, the giant's money and experience are then missing; second, it is a signal the market will read ("why doesn't Gilead want this?"). Add the second side of the biotech coin that every investor should know: the loss is financed through the sale of new shares and through Gilead's stake purchases — and every new piece makes your own smaller. That is the silent arithmetic behind every "but the growth is financed": it is financed, yes — with your share too. And above it all hovers the real biotech risk that no metric captures: the value of Arcus hangs on clinical trial results that no one can predict. A disappointing Phase 3 result can cost more in price within hours than any balance-sheet metric in years.

Valuation: $3.8 billion market value for a bet on the trial results

In early July 2026 the Arcus stock cost about $30; at about 126 million shares that makes roughly $3.8 billion in market value (data as of July 8, 2026). Classic valuation metrics run into the void here: a price-to-earnings ratio does not exist for lack of a profit, and a price-to-sales ratio of about 16 (measured against the fluctuating collaboration proceeds) says little, because this "revenue" is not product demand. What the market actually prices here is something else: the probability that casdatifan, domvanalimab & co. clear approval — that more-than-$2-billion peak-sales opportunity for the kidney-cancer program alone, multiplied by a success chance that sharper minds than a metrics grid argue over. Still: the balance sheet, unlike the D rating suggests, carries almost no debt (debt-to-equity about 0.2), equity is clearly positive, and about 72 percent of the shares are held by institutions. This is no substanceless gambling paper — it is an early bet on clinical data, wrapped in a solidly financed shell. With such stocks the rule holds: trial results move the price in jumps, in both directions — the 234 percent of the past year can repeat in one direction as in the other.

Opportunities and risks at a glance

What speaks for Arcus:

- Solidly financed for a clinical biotech: about $1.0 billion in cash and securities (December 31, 2025), runway per the annual report into at least the second half of 2028, no going-concern qualification, little debt (debt-to-equity about 0.2), positive equity.

- Strong partner with real money: Gilead Sciences holds about 25.1 percent, supplies almost all revenue through collaboration and option payments ($214 of $247 million in 2025) and shares the costs of the expensive late-stage trials.

- Broad, addressable pipeline: lead compound casdatifan (HIF-2-alpha) with a peak-sales opportunity named in the annual report of more than $2 billion in renal cell cancer alone; plus domvanalimab (TIGIT, Phase 3 in lung cancer), zimberelimab and quemliclustat.

- The pros' market is on board: about 72 percent institutional ownership, RS rating 93, an intact uptrend (Stage 2), plus 234 percent over twelve months — a clear momentum vote.

- The distress-scanner hit is mostly an arithmetic approximation for missing profit, not for acute insolvency — that distinguishes Arcus from genuine restructuring cases.

What speaks against it:

- Not a cent of product revenue since founding; net loss $353 million (2025), accumulated deficit $1.5 billion (by Q1 2026: $1.6 billion), operating cash outflow risen to a record $482 million — the till is full, but finite, and further capital raises are foreseeable.

- Cluster risk Gilead: a single partner supplies almost all revenue, holds a quarter of the shares and three board seats; if Gilead passes on a program, money and experience are missing — and the market reads that as a warning signal.

- Binary clinical risk: the value hangs on trial results (including PEAK-1, STAR-121) that no one can predict with certainty; a disappointing Phase 3 result can move the price within hours many times more than any balance-sheet metric.

- Dilution: the loss is financed through new shares — every new piece shrinks the stake of existing shareholders.

- Weak metrics picture: fundamental rating D, Piotroski 0 of 9, Altman Z around 1.03, negative interest coverage (data as of July 8, 2026) — no basis for value-oriented investors, but for a pure trial bet the normal state.

A human conclusion

Back to the label reflex from the beginning. Arcus is the perfect teaching case for why no single label does the work for you. The red sign ("distress proxy!") is right in its number and deceives in its meaning: yes, the company burns cash and earns no profit — but it has a billion in the till, no going-concern qualification and a billion-dollar partner that holds a quarter. The green sign ("+234 percent!") is likewise right and likewise deceives: yes, the momentum is strong and the pros are on board — but it is a bet on trial results, not a certainty, and a single disappointing data point can reverse the rally. The real story stands between the two signs, in the annual report: a well-financed research lab whose future hangs on the clinic and on a single large partner. Whoever buys in here buys neither a balance sheet nor a price chart — they buy the probability that casdatifan and its siblings reach the finish line, and the willingness to sit in the same boat as Gilead. That can pay off, and it can get expensive. Both stand honestly in the same report. What you make of it is your decision. And that is exactly as it should be.

Sources

All original documents used in this analysis — to read for yourself:

- Arcus Biosciences — SEC annual report 10-K for 2025 (filed February 25, 2026)

- Arcus Biosciences — SEC annual report 10-K for 2024 (filed February 25, 2025)

- Arcus Biosciences — SEC quarterly report 10-Q as of March 31, 2026 (filed May 5, 2026)

- Arcus Biosciences — SEC quarterly report 10-Q as of September 30, 2025 (filed October 28, 2025)

- Arcus Biosciences — SEC quarterly report 10-Q as of June 30, 2025 (filed August 6, 2025)

- Arcus Biosciences — SEC quarterly report 10-Q as of March 31, 2025 (filed May 6, 2025)

- Arcus' complete SEC filing history: EDGAR overview (sec.gov)

- Fundamental data (metrics, quarterly series, valuation; data as of July 8, 2026), reconciled with the SEC filings.

- Screener and rating data: in-house stock scanner (data as of July 8, 2026).

Transparency & disclaimer: This analysis is a journalistic contextualization of publicly available information and is not investment advice, not a financial analysis in the regulatory sense, and not a solicitation to buy or sell securities. It expressly contains no judgment on whether an insolvency will occur. Stock investments carry substantial risks up to total loss. All information without guarantee; the data cut-off is noted in the text in each case. The author holds no position in Arcus stock at the time of publication.

Our Bottom Line at a Glance

- Financing & liquidity positive

- About $1.0 billion in cash and securities (December 31, 2025), runway per the annual report into at least the second half of 2028, no going-concern qualification, low debt (debt-to-equity about 0.2), positive equity. For a clinical biotech, a comfortable starting position.

- Earnings & cash burn negative

- No product revenue, net loss $353 million (2025), accumulated deficit $1.5 billion, operating cash outflow risen to a record $482 million. Fundamental rating D, Piotroski 0 of 9, Altman Z around 1.03 — precisely what triggers the distress proxy.

- Partner Gilead neutral

- Gilead Sciences holds about 25.1 percent, appoints three board members and supplies almost all revenue through collaboration and option payments ($214 of $247 million in 2025). Backbone and cluster risk in one: if Gilead passes on a program, money and experience are missing — and the market reads that as a warning signal.

- Pipeline & clinical risk neutral

- Broad pipeline with lead compound casdatifan (HIF-2-alpha, renal cell cancer, peak-sales opportunity per the 10-K of more than $2 billion), domvanalimab (TIGIT, Phase 3 lung cancer), zimberelimab and quemliclustat. The value hangs on binary trial results (including PEAK-1, STAR-121) that no one can predict with certainty.

- Market & momentum positive

- Intact uptrend (Stage 2), RS rating 93, only 3.8 percent below the 52-week high, plus 234 percent over twelve months, about 72 percent institutional ownership (data as of July 8, 2026). A clear momentum vote — that likewise hangs on the next trial data.

Arcus is the teaching case for why a warning-scanner hit is not the same as a restructuring case. The "Going Concern (Distress-Proxy)" triggers because the company earns no profit and burns cash — for a clinical biotech without product revenue the normal state. Behind it, however, stand about $1.0 billion in cash, no going-concern qualification, little debt and, in Gilead, a billion-dollar partner that holds a quarter. The real risk lies not in the balance sheet, but in the clinic and in the dependence on this one partner. Not investment advice.

What Our Rating Means

- If you don't own the stock

- In our view, the documented risks clearly outweigh — we see no basis for an entry.

- If you hold it in your portfolio

- In our view, the findings carry enough weight to warrant a critical look at your own position.

A journalistic assessment by our editorial team at the time of the deep dive, based on public sources — not investment advice and not a solicitation to buy or sell. Your personal circumstances (investment goals, risk capacity, taxes) cannot be taken into account. What our categories mean, how verdicts are formed, and what conflicts of interest exist →

Worth Noting

- The "revenue" of Arcus consists almost entirely of collaboration and option payments (above all from Gilead, plus the partner Taiho) and therefore fluctuates with contract milestones, not with product demand — Arcus has no approved product.

- The scanner hit "Going Concern (Distress-Proxy)" is by definition a quantitative approximation and not an auditor qualification; the auditor did not cast doubt on the survival of Arcus.

- Price, valuation and scanner figures are dated to July 8, 2026 (about $30, about $3.8 billion in market value); analyses are evergreen, daily prices are not a buy argument.

Frequently Asked Questions

Arcus Biosciences (NYSE: RCUS) of Hayward, California, is a clinical immuno-oncology company: it develops cancer drugs that activate the immune system against tumors. The lead compound is the oral HIF-2-alpha inhibitor casdatifan against renal cell cancer, plus the TIGIT antibody domvanalimab, the PD-1 antibody zimberelimab and the CD73 inhibitor quemliclustat. No product is approved yet.

Because the scanner is a purely arithmetic approximation: it triggers when a company earns no profit, burns cash and has no interest coverage. For a clinical biotech without product revenue that is the normal state, not acute insolvency risk. Unlike a genuine restructuring case, Arcus carries no going-concern qualification from its auditor and about $1.0 billion in cash.

This analysis expressly issues no insolvency verdict. The facts: as of December 31, 2025 Arcus held about $1.0 billion in cash and securities, per the annual report enough at least into the second half of 2028; the auditor issued no going-concern qualification, and debt is low with a debt-to-equity ratio around 0.2. The real risk lies in clinical trial results and the dependence on Gilead, not in acute insolvency.

Gilead is partner and major shareholder at once: the pharma giant holds about 25.1 percent of Arcus shares, appoints three board members and has secured opt-in rights to the programs. Through collaboration and option payments, almost all reported revenue comes from Gilead ($214 of $247 million in 2025). That is financing backbone and cluster risk in one — if Gilead passes on a program, Arcus must go it alone or find new partners.

Arcus posted a net loss of $353 million in 2025 (2024: $283 million, 2023: $307 million); the accumulated deficit since inception is $1.5 billion. Operating cash outflow rose to $482 million in 2025. This is financed from the existing cash, collaboration and option payments from Gilead, and the issuance of new shares — which dilutes existing holdings.

Casdatifan is Arcus's most important drug candidate: an oral, swallowable inhibitor of the cell switch HIF-2-alpha, which plays a key role in clear-cell renal cell carcinoma (ccRCC). The Phase 3 trial PEAK-1 tests it in combination therapy; the annual report puts the worldwide peak-sales opportunity at more than $2 billion — provided approval succeeds.

The stock gained about 234 percent over twelve months and trades near its 52-week high (data as of July 8, 2026). This is driven not by profits but by the expectation of successful clinical trials and the prospect of approvals. Such biotech prices move in jumps along trial data — upward as well as downward.

Found an error?

Did you spot a factual error, an outdated number, or a typo in this deep dive? Let us know briefly — your report goes straight to the editorial team.