Virgin Galactic Stock: 675 Customers Are Waiting for Space — and the Company's Own Annual Report Doubts It Will Survive

Virgin Galactic has a spaceship factory in Arizona, a spaceport in New Mexico, a global brand and about 675 paid reservations — but nobody has flown since June 2024, and the stock shows up in our warning scanner "Thomas Inso Kandidat". We read the annual report (10-K) for 2025 and the quarterly report (10-Q) as of March 31, 2026: $1.5 million in revenue against a $278.9 million loss, a cash pile that has more than halved in five quarters, a debt restructuring from 2.5 to 9.8 percent interest — and, for the first time, official doubt about the company's survival. Everything hangs on one date in the fourth quarter of 2026. Not investment advice — just a countdown in which we count along every number straight from the original filings.

There is a calculation that almost writes itself when you look at crashed dream stocks: "It used to trade above a thousand dollars — now it costs $2.50. It can't fall much further." Psychologists call this the anchoring effect, crossed with lottery-ticket thinking: the old price feels like a promise, the new one like a bargain, and the possible loss of your stake feels small against the dream behind it. And hardly any stock delivers a bigger dream than Virgin Galactic (NYSE: SPCE): spaceflights for private citizens, a global brand, a charismatic founder named Sir Richard Branson. So let's make a deal: before you buy the lottery ticket, we read together what Virgin Galactic itself reported to the U.S. securities regulator, the SEC — in the annual report (10-K) for 2025 and the quarterly report (10-Q) as of March 31, 2026. An SEC filing is honest under penalty of law. And this one contains a sentence that has never before appeared in this company's filings: official doubt about its own survival. In the end, you decide for yourself.

What Virgin Galactic actually does

The product is quickly explained, because it is so unique: Virgin Galactic sells suborbital spaceflights — excursions to the edge of space, without orbiting the Earth. A twin-fuselage carrier aircraft hauls the spaceship to an altitude of about 45,000 feet and releases it there; then the rocket motor ignites, the ship climbs at more than three times the speed of sound, a few minutes of weightlessness and the view of the Earth's curvature wait at the top, and afterwards the ship glides back to the runway. From boarding to exit the experience lasts about 90 minutes, launching from Spaceport America in New Mexico — which, by the way, the state paid for, not the company. Customers are private citizens ("Future Astronauts"), researchers with experiments, and government agencies. Unlike the satellite operator Iridium or the Earth-observation firm BlackSky, which generate recurring revenue with space technology, the business model here is an experience product — closer to the luxury-travel market than to the space industry.

The catch: since the flight "Galactic 07" in June 2024, nobody has flown. Virgin Galactic deliberately stopped flights with the old ship VSS Unity to throw all its forces at the next ship generation: production ships with six passenger seats (50 percent more than Unity), built for hundreds of missions and two flights per week per ship, manufactured in the company's own Arizona factory, opened in July 2024. With the first two new ships, the company aims for up to 125 space missions per year; the upgraded carrier aircraft can meanwhile fly on consecutive days. The timetable per the quarterly report as of March 31, 2026: test flights starting in the third quarter of 2026, commercial restart in the fourth quarter of 2026 with a research flight, private astronauts six to eight weeks later. 694 people work for Virgin Galactic (end of 2025), headquarters are in Tustin, California, and the company has been publicly listed since October 2019. Remember the puzzle image: factory, spaceport, brand, customers and date are on the table — only the piece called "revenue" has been missing since mid-2024. The question is whether the money lasts until it is placed.

Where the stock shows up in our scanner

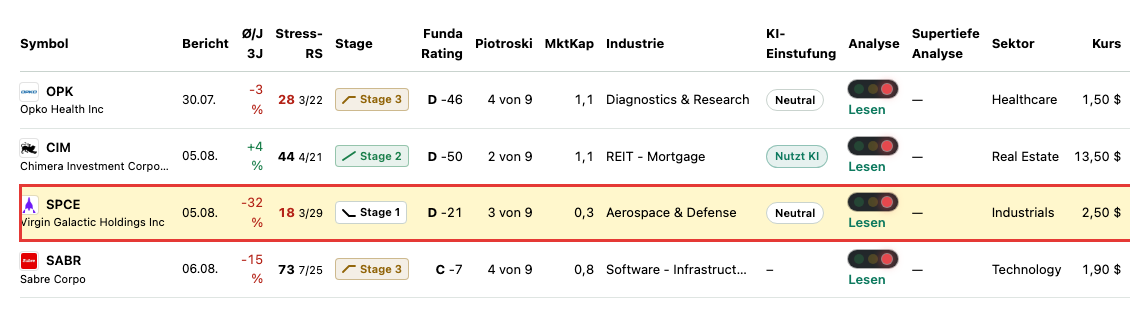

Every day we run about 3,500 stocks through our scanners. Virgin Galactic lights up in 5 scanners (data as of July 13, 2026) — and the list reads like a medical chart: "Thomas Inso Kandidat" (our warning scanner for bankruptcy risk: weak balance sheet, interest not covered by earnings, falling revenue), "Going Concern (Distress-Proxy)", "Altman-Z: Distress-Zone", plus "Unter 50- & 200-SMA" (price below both key moving averages) and "Kathy Donnelly: Liquid Movers Down". How to read such warning lists — a smoke detector, not a demolition order — is explained in our piece "Insolvency radar: the top 10". The readings behind them: the Altman Z-score, a classic insolvency early-warning built from several balance-sheet ratios, stands at minus 10.75 — the danger zone historically begins below 1.8; a negative value of this magnitude comes out when a firm burns very large amounts of money relative to its assets. The Piotroski F-Score, a nine-point test of balance-sheet quality, stands at 3 of 9 — a thoroughly healthy company scores 8 or 9. And interest coverage is deeply negative: operating income does not remotely suffice to earn even the interest.

One hit deserves special attention: our scanner "Going Concern (Distress-Proxy)" is deliberately built as an approximation — it combines an Altman Z-score in the distress zone, interest coverage below 1 and negative operating cash flow, because this combination often fires exactly where auditors have serious doubts about a company's survival. At Virgin Galactic, the approximation is no longer needed: the real going-concern warning has stood verbatim in the filings since the 10-K for 2025 — more on that in a moment. That names the central tension of this analysis: a unique product with real, paying demand and a concrete restart date — against a cash pile that melts faster than the date approaches, and a capital structure that pays dearly for this waiting period. It runs through everything that follows.

The numbers over the years — honestly appraised

First, what has real substance — because there is some. In 2023/24, Virgin Galactic proved that the product works and gets paid for: seven commercial flights between June 2023 and June 2024, paying private customers and research contracts. The demand is documented: as of December 31, 2025, there were reservations from about 675 "Future Astronauts", representing about $188 million in spaceflight revenue upon completion of the flights — and the sale of a new ticket tranche was opened at a base price of $750,000 per seat, after $600,000 in 2023 and $450,000 in 2021. The company itself puts it this way in the annual report:

"We have recently reopened ticket sales for a tranche of spaceflight reservations at a higher base price per seat. As of December 31, 2025, we have reservations for spaceflights for approximately 675 future astronauts, which represent approximately $188 million in expected future spaceflight revenue upon completion of the spaceflights."

— Virgin Galactic, SEC annual report 10-K 2025, Item 7 "MD&A — Customer Demand"

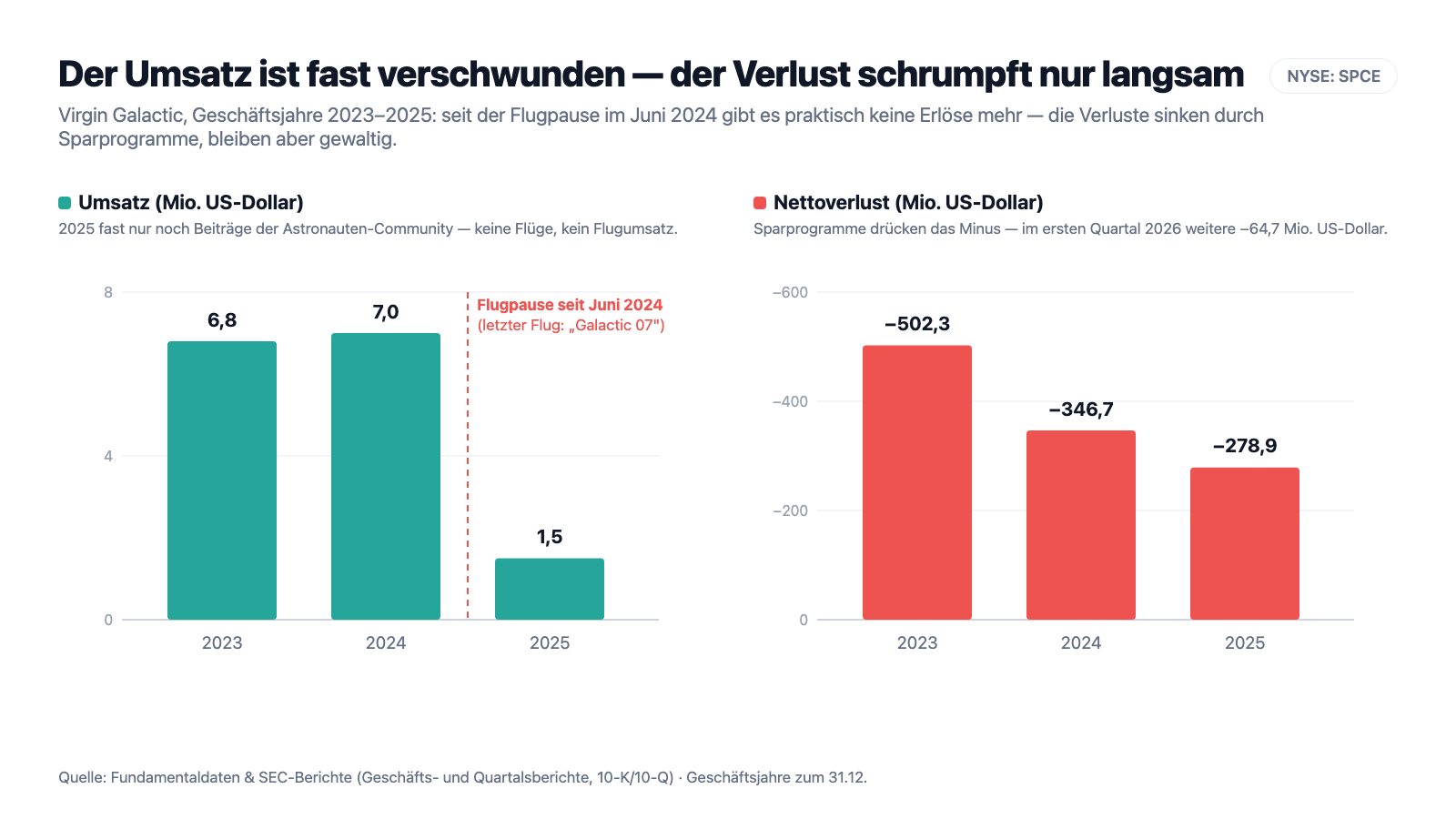

The cost discipline deserves recognition too: research and development spending fell 47 percent in 2025 to $80.5 million (the expensive design work is finished, the tooling paid for), operating and administrative costs also declined, and the cash outflow from operations went from $352.7 million (2024) to $240.1 million (2025) — in the first quarter of 2026 it was $53.5 million, after $75.9 million in the prior-year quarter. Only: all of that is consumption reduction, not income. The chart shows the whole truth:

Revenue fell from $6.8 million (2023) via $7.0 million (2024) to $1.5 million (2025) — that is not a typo: a company with 694 employees and an NYSE listing took in less in 2025 than many a car dealership branch, essentially membership fees from the astronaut community. In the first quarter of 2026 it was $0.2 million. Against that stand net losses of −$502.3, −$346.7 and −$278.9 million (2023 through 2025), plus −$64.7 million in the first quarter of 2026. Yes, the curve points in the right direction — the loss has almost halved since 2023. But a company that loses one hundred times its revenue per year does not live off its customers; it lives off its cash. And that brings us to the uncomfortable truths.

What the filings say — the uncomfortable truths

Uncomfortable truth no. 1: the report itself doubts the company's survival — and its own math doesn't work without outside help

The phrase "going concern" is auditor language for the basic assumption behind every balance sheet: that the company lives on. When an annual report itself calls this assumption into doubt, that is the sharpest warning level financial reporting knows — not an insolvency verdict, but an officially documented "it could get tight". Exactly this sentence stands — for the first time — in the risk chapter of the 10-K for 2025:

"We believe that we may not have sufficient cash and marketable securities to maintain our planned operations for the next twelve months following the issuance date of the consolidated financial statements and have concluded that there are conditions present in the aggregate that raise substantial doubt about our ability to continue as a going concern."

— Virgin Galactic, SEC annual report 10-K 2025, Item 1A "Risk Factors"

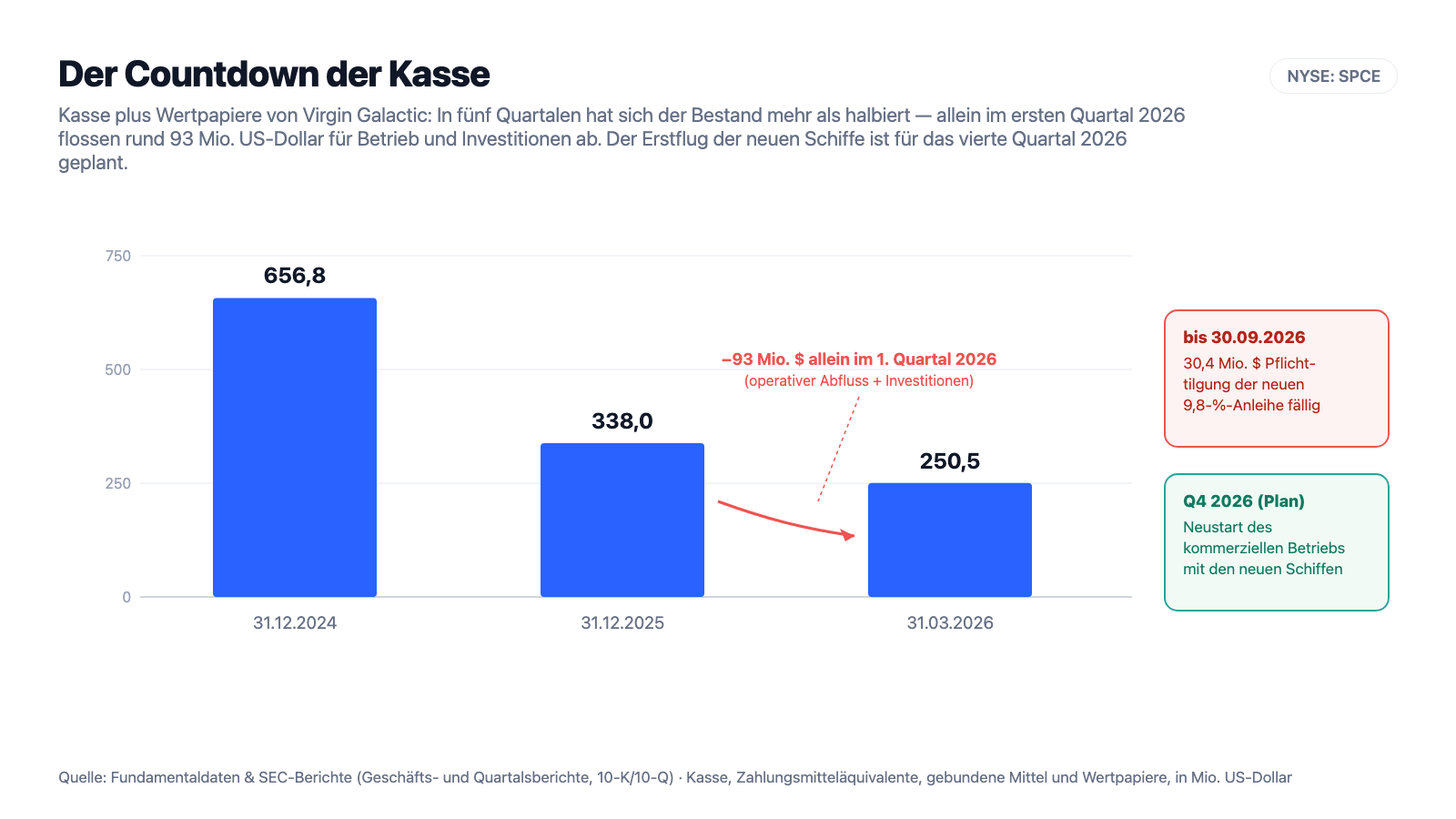

What matters is how this calculation comes about — because it is stricter than it sounds. The accounting rule ASC 205-40 demands: only funds that are certain may be counted. Management may not count anything outside its control — future ticket income, capital raises, new loans, deferred redemptions. What stands in this strict calculation: $250.5 million of cash plus securities as of March 31, 2026 (of which $30.6 million is restricted customer money — deposits from Future Astronauts that may only be used after a signed carriage agreement). What goes out: in the first quarter of 2026 alone, roughly $93 million for operations and investments, plus a mandatory redemption of $30.4 million on the new notes by September 30, 2026. The chart shows the countdown:

Honesty requires saying: management has a plan, and it is no castle in the air — restart in the fourth quarter of 2026, final payments from the waiting customers ahead of their flights, the sale of some early flights at premium prices, and if need be more shares through the running sales program. But the quarterly report as of March 31, 2026, itself says what these plans are worth in the sense of the accounting rule:

"The plans discussed above are subject to market conditions and, while management intends to apply its best efforts to the execution of these plans, they are not fully within the Company's control and therefore cannot be deemed to be probable in accordance with ASC 205-40, and as a result, management has concluded that its plans do not alleviate substantial doubt about the Company's ability to continue as a going concern for twelve months after the date that the condensed consolidated financial statements are issued."

— Virgin Galactic, SEC quarterly report 10-Q as of March 31, 2026, Note 2 "Going Concern"

Remember: a going-concern warning is not a death sentence — but it shifts the burden of proof. It is no longer the skeptics who must explain why things could go wrong; the company must deliver so that they go right.

Uncomfortable truth no. 2: the December restructuring — from 2.5 percent unsecured to 9.8 percent with a lien on almost everything

How expensive the waiting period has become is shown most clearly by the capital transaction of December 2025. Virgin Galactic bought back $354.6 million of its old convertible notes — issued in 2022, at 2.5 percent interest, unsecured, due in February 2027. They were replaced, at the core, by $212.5 million of new notes at 9.8 percent interest, due at the end of 2028 — and the new creditors had themselves given considerably more than just the nearly quadrupled interest rate:

"The 2028 Notes were issued at a price of 100% of their face value and bear interest at a rate of 9.80% per year, payable quarterly in arrears […] The 2028 Notes are secured on a first-priority basis by liens on substantially all of the assets of the Company and its domestic subsidiaries […]"

— Virgin Galactic, SEC annual report 10-K 2025, Note 9 "Long-Term Debt"

The package in detail: buyers of the new notes additionally received warrants on 31.7 million shares (subscription rights at $6.696 each, exercisable from June 2026 through the end of 2030) with a fair value of $62.5 million; in parallel, new shares and pre-funded warrants were placed for $45.6 million. The notes demand $30.4 million of mandatory redemption by September 30, 2026, and from the end of 2027 $10.1 million per quarter; asset sales and capital raises trigger additional mandatory repurchases. And the accounting calls the child by its name: the company had to book the transaction under the accounting rule ASC 470-60 as a "troubled debt restructuring" — the restructuring of a debtor in difficulty. Of the old convertible notes, $70.4 million remain outstanding, due in February 2027; their conversion price of a calculated $255.77 per share is pure theory at a price around $2.50 — nothing gets converted there, the money must be repaid in cash. Added up, $282.9 million of note debt sits on the books (December 31, 2025), of which $47.8 million is due within a year. Whoever, in December 2025, got fresh money only against a lien on practically everything, nearly quadrupled interest and equity kickers does not negotiate from a position of strength the next time.

Uncomfortable truth no. 3: the dilution machine is running — share count from 33 to 81 million in fifteen months

Dilution means: your slice of the cake gets smaller because new slices keep being cut. At Virgin Galactic this is not a side effect but, for years, the main source of financing. The share count rose from 33.0 million (end of 2024) via 73.3 million (end of 2025) to 81.4 million as of March 31, 2026 — plus 147 percent in fifteen months. This runs through a so-called at-the-market program: a standing authorization to sell new shares directly into the market on an ongoing basis (frame: up to $300 million, agreed in November 2024). In 2025 this brought in a net $118.1 million; in the first quarter of 2026 alone, another 4.0 million shares were sold at an average of about $2.76. Add the 31.7 million warrants from the restructuring — if they were all exercised, almost 40 percent of the current share count would come on top (at least: against cash payment of $6.696 each). How brutal this spiral has been for long-time shareholders is shown by two numbers from the report itself: the loss per share was still $13.89 in 2024, then $5.44 in 2025 — not because the company was doing so much better, but because the number of shares across which the loss is spread more than doubled. And all of that after a 1-for-20 reverse split in June 2024, which turned every 20 old shares into one new one — the usual emergency measure when the price would otherwise quote in the cent range. Split-adjusted, the stock sits about 99.8 percent below its record high from the 2021 hype era (data as of July 13, 2026). Remember: growth paid for with fresh shares is never entirely free — here, so far, it mostly pays for the waiting period.

Uncomfortable truth no. 4: the brand belongs to Branson — and in 2025 it cost more than the company's revenue

"Virgin" sounds like property but is rent: the name belongs to Virgin Enterprises Limited, a company from the business empire of Sir Richard Branson, and is licensed until October 2044. The related-party note of the annual report puts a figure on what that costs:

"The Company licenses its brand name from certain entities affiliated with Virgin Enterprises Limited ('VEL'), a company incorporated in England. […] During the years ended December 31, 2025 and 2024, the Company incurred royalty expenses of $2.5 million and $1.5 million, respectively."

— Virgin Galactic, SEC annual report 10-K 2025, Note 17 "Related Party Transactions"

Go ahead and read those two numbers twice: $2.5 million of brand rent against $1.5 million of total revenue. The fee is constructed as a minimum amount and rises further after the first paid passenger flight — over a four-year ramp into the low seven figures per year, inflation-indexed thereafter. The contract also has teeth: VEL may terminate if Virgin Galactic goes too long without commercial flights carrying paying passengers (safety pauses excepted) — after a termination, 90 days would remain to remove logos and change the company name. And the entanglement does not end with the brand: Branson's investment vehicle Virgin Investments Limited has secured veto rights by shareholder agreement — among other things over larger asset sales and acquisitions from $10 million upward, dividends, the size of the board of directors and the incurrence of certain debt; a further threshold applies to mergers and charter amendments. These rights hang on the number of originally held shares, not on today's stake. All disclosed, none of it forbidden — but you should know: the brand, the name and part of the strategic decisions of this company belong to a contract partner who earns even when the stock does not. From the same hype era, incidentally, stem shareholder lawsuits with case names like "… v. Branson et al." — the securities class action was settled in 2025 for $8.5 million, of which the insurers are to carry $6.25 million.

Valuation: a $275 million market value on $1.5 million of revenue — what exactly are you paying for?

Time for the price question. In mid-July 2026 the Virgin Galactic stock cost about $2.50, putting the market value at about $275 million (data as of July 13, 2026). Computing a price-to-sales ratio here is almost satire — it sits beyond 200, because the denominator has practically vanished. A price-to-earnings ratio does not exist for lack of earnings. More honest is this calculation: add $282.9 million of note debt to the market value, subtract $250.5 million of cash and securities — that makes an enterprise value of a good $300 million. For that you get: a spaceship factory including tooling, a flight-proven carrier aircraft, the technology of two decades of development, a global brand (rented), about 675 waiting customers with a $188 million order backlog — and the hope that $750,000 tickets at 125 flights per year will someday become a profitable business. That is not an absurd hope, but it is one that can only be proven after the restart. Until then the stock is an option certificate on a date: extremely volatile (on average the price moves double digits per day — 11 to 19 percent daily range depending on the measurement window), down about 6.5 percent in 2026 through mid-July, and only a scant 16 percent of the shares sit with institutional investors. For the scale of the fall: whoever bought at the split-adjusted record high of the 2021 hype era has lost about 99.8 percent — the anchor "it used to be much more expensive" has already blocked many people's view of the real question: does the cash last until the first full flight season?

Opportunities and risks at a glance

What speaks for Virgin Galactic:

- A unique, proven product: seven commercial flights between June 2023 and June 2024, working technology (carrier aircraft + reusable spaceship), two decades of development lead — and per the annual report the most important competitor, Blue Origin, has itself paused its suborbital tourist flights for at least two years.

- Documented, paying demand: about 675 reservations with roughly $188 million in expected spaceflight revenue (December 31, 2025), a new ticket tranche at $750,000 per seat — prices rose from $450,000 to $750,000 between 2021 and 2025.

- A concrete, recently confirmed timetable: the Arizona factory finished, tooling paid for, test flights from the third and commercial restart in the fourth quarter of 2026; the new ships offer 6 seats and are designed for two flights per week — target rate 125 missions per year with two ships.

- Visible cost discipline: research and development costs down 47 percent (2025), operating cash outflow cut from $352.7 to $240.1 million, further down to $53.5 million in the first quarter of 2026 — the investment peak, per the report, lies behind the company.

- Option value beyond tourism: research and government flights, plus the evaluated use of the carrier-aircraft design as a high-altitude endurance flyer (HALE) for government purposes.

What speaks against it:

- A going-concern warning in the 10-K and 10-Q: under the strict math of ASC 205-40, cash and securities ($250.5 million as of March 31, 2026) may not last twelve months; the counter-plans are explicitly deemed "not probable" in the sense of the rule.

- Practically no revenue since mid-2024 (2025: $1.5 million against a $278.9 million loss; Q1 2026: $0.2 million against a $64.7 million loss) — every delay of the restart extends the revenue-less period at running costs of roughly $93 million per quarter (including investments).

- Expensive, secured debt: $282.9 million of notes, of which the new 9.8 percent notes are secured on a first-priority basis by practically all assets, booked as a "troubled debt restructuring"; $30.4 million of mandatory redemption by September 30, 2026, $70.4 million of convertible notes due in cash in February 2027.

- Ongoing dilution: share count plus 147 percent in fifteen months (33.0 to 81.4 million), an at-the-market program of up to $300 million, warrants on a further 31.7 million shares; a 1-for-20 reverse split in 2024, the price about 99.8 percent below the record high.

- Dependencies and early-warning signals: the brand only rented (termination right after too long a flight pause; brand fee in 2025 higher than revenue), veto rights of the Branson vehicle VIL, plus five scanner hits with an Altman Z-score of −10.75, Piotroski 3 of 9 and deeply negative interest coverage (data as of July 13, 2026).

A human conclusion

Back to the lottery-ticket thought from the opening. "It can't fall much further" — yes, it can: the floor is not the price, it is the cash. A stock quoting 99.8 percent below its high can lose half again, and again, as long as new shares dilute the old ones — and exactly that has been the mechanism by which this company pays for its waiting period for years. The old price above a thousand dollars is not a promise; it is the memory of a valuation that was never covered by revenue. And yet it would be dishonest to dismiss this company as an empty shell: the product exists, it has flown, it has been paid for, 675 people stand on the list with reservations, the factory stands, the date is set. Virgin Galactic is no swindle — it is a bet with an open outcome and a ticking clock: do the new ships make it into paid service in the fourth quarter of 2026 before the cash needs outside help once more — and if not, at what price does that help come? The annual report itself does not answer the question; it only poses it — with the sharpest warning label financial reporting knows. If you want to buy this ticket anyway, then not because it looks cheap, but because you have understood the bet and stake only money whose total loss you can absorb. What you make of it is your decision. And that is exactly as it should be.

Sources

All original documents used in this analysis — to read for yourself:

- Virgin Galactic Holdings, Inc. — SEC annual report 10-K for 2025 (filed March 30, 2026)

- Virgin Galactic Holdings, Inc. — SEC annual report 10-K for 2024 (filed February 26, 2025)

- Virgin Galactic Holdings, Inc. — SEC quarterly report 10-Q as of March 31, 2026 (filed May 14, 2026)

- Virgin Galactic Holdings, Inc. — SEC quarterly report 10-Q as of September 30, 2025 (filed November 13, 2025)

- Virgin Galactic Holdings, Inc. — SEC quarterly report 10-Q as of June 30, 2025 (filed August 6, 2025)

- Virgin Galactic Holdings, Inc. — SEC quarterly report 10-Q as of March 31, 2025 (filed May 15, 2025)

- Virgin Galactic's complete SEC filing history: EDGAR overview (sec.gov)

- Fundamental data (metrics, quarterly series, valuation; data as of July 13, 2026), reconciled with the SEC filings.

- Screener and rating data: in-house stock scanner (data as of July 13, 2026).

Transparency & disclaimer: This analysis is a journalistic contextualization of publicly available information and is not investment advice, not a financial analysis in the regulatory sense, and not a solicitation to buy or sell securities. It expressly contains no judgment on whether an insolvency will occur; a going-concern warning is a warning, not a verdict. Stock investments carry substantial risks up to total loss. All information without guarantee; the data cut-off is noted in the text in each case. The author holds no position in Virgin Galactic stock at the time of publication.

Our Bottom Line at a Glance

- Product & demand positive

- A unique, flight-proven product (seven commercial flights in 2023/24) with documented paying demand: about 675 reservations, roughly $188 million in expected spaceflight revenue, new tickets at a $750,000 base price (annual report 10-K for 2025). The Arizona factory is finished, the timetable most recently confirmed.

- Cost discipline & progress neutral

- Research and development costs cut 47 percent in 2025, operating cash outflow reduced from $352.7 to $240.1 million (Q1 2026: $53.5 million); the investment peak, per the report, lies behind the company. But: all of it is consumption reduction — income only arrives after the restart in the fourth quarter of 2026.

- Revenue & earnings negative

- Practically no revenue since the flight pause in June 2024 (2025: $1.5 million; Q1 2026: $0.2 million) against net losses of $278.9 million (2025) and $64.7 million (Q1 2026). The loss is falling for the second year in a row — but a company that loses one hundred times its revenue lives off its cash, not its business.

- Liquidity & going concern negative

- A going-concern warning in the 10-K and 10-Q for the first time: $250.5 million of cash and securities (March 31, 2026) against roughly $93 million of outflow per quarter plus $30.4 million of mandatory redemption by September 30, 2026; the counter-plans are explicitly deemed "not probable" under ASC 205-40. The December 2025 restructuring (2.5 to 9.8 percent, first-priority security, "troubled debt restructuring") shows the price at which fresh money was last available.

- Capital structure & dependencies negative

- Share count plus 147 percent in fifteen months (33.0 to 81.4 million), an at-the-market program of up to $300 million, warrants on 31.7 million shares; $70.4 million of convertible notes due in cash in February 2027. The brand only rented from Branson's Virgin Enterprises (2025: a $2.5 million fee — more than revenue; termination right after a long flight pause), veto rights of the Branson vehicle VIL.

Virgin Galactic is no empty shell: the product flew and was paid for, 675 customers are waiting with a $188 million order backlog, the factory stands, the restart is scheduled for the fourth quarter of 2026. But the waiting period costs roughly $93 million per quarter against $250.5 million of cash and securities, the annual report itself doubts the company's survival for the first time, the debt restructuring brought 9.8 percent interest and a lien on almost everything, and the waiting period has been paid for with ever more new shares for years. Not investment advice.

What Our Rating Means

- If you don't own the stock

- In our view, the documented risks clearly outweigh — we see no basis for an entry.

- If you hold it in your portfolio

- In our view, the findings carry enough weight to warrant a critical look at your own position.

A journalistic assessment by our editorial team at the time of the deep dive, based on public sources — not investment advice and not a solicitation to buy or sell. Your personal circumstances (investment goals, risk capacity, taxes) cannot be taken into account. What our categories mean, how verdicts are formed, and what conflicts of interest exist →

Worth Noting

- A going-concern warning is a standardized warning under ASC 205-40 (a calculation without future revenue and capital measures) — it is not an insolvency verdict, and this analysis expressly renders none.

- The order backlog of roughly $188 million across 675 reservations averages out to roughly $279,000 per person — many reservations stem from earlier, considerably cheaper pricing rounds; new tickets cost a $750,000 base price (2021: $450,000; 2023: $600,000).

- Price and valuation figures are dated to mid-July 2026 (about $2.50, market value ~$275 million); analyses are evergreen, daily prices are not a buy argument.

Frequently Asked Questions

Virgin Galactic (NYSE: SPCE) of Tustin, California, sells suborbital spaceflights: a carrier aircraft brings the spaceship to an altitude of about 45,000 feet, then it climbs under rocket power to the edge of space — an experience of about 90 minutes with a few minutes of weightlessness. Customers are private citizens, researchers and government agencies; flights launch from Spaceport America in New Mexico.

Since the flight "Galactic 07" in June 2024 all flights are deliberately paused: the company is putting all resources into building the next ship generation with six seats. In 2025 only $1.5 million of revenue came together as a result — essentially fees from the astronaut community. The commercial restart is planned, per the quarterly report, for the fourth quarter of 2026.

The annual report (10-K) for 2025 states for the first time that substantial doubt exists about the ability to continue as a going concern: under the strict accounting rule ASC 205-40 — which may not count future revenue and capital measures — cash and securities ($250.5 million as of March 31, 2026) may not last twelve months. That is an official warning, not an insolvency verdict.

Per the quarterly report (10-Q) as of March 31, 2026, test flights of the new ships are to begin in the third quarter of 2026; the commercial restart is planned for the fourth quarter of 2026 with a research flight, and private astronauts follow six to eight weeks later. The new ships offer six seats and are meant to fly twice a week in regular service — dates the company has to keep.

Substantially: the share count rose from 33.0 million (end of 2024) to 81.4 million (March 31, 2026), because new shares are continuously sold through an at-the-market program (frame: $300 million). On top come warrants on 31.7 million shares from the December 2025 debt restructuring. As early as June 2024 there was a 1-for-20 reverse split; split-adjusted, the stock trades about 99.8 percent below its 2021 high.

The brand is only rented: the licensor is Virgin Enterprises Limited from the business empire of Sir Richard Branson; in 2025 the license cost $2.5 million — more than the entire annual revenue. The contract runs until 2044 but may be terminated if no paying passengers fly for too long. A ticket in the newest tranche costs a base price of $750,000 (2021: $450,000; 2023: $600,000).

Found an error?

Did you spot a factual error, an outdated number, or a typo in this deep dive? Let us know briefly — your report goes straight to the editorial team.