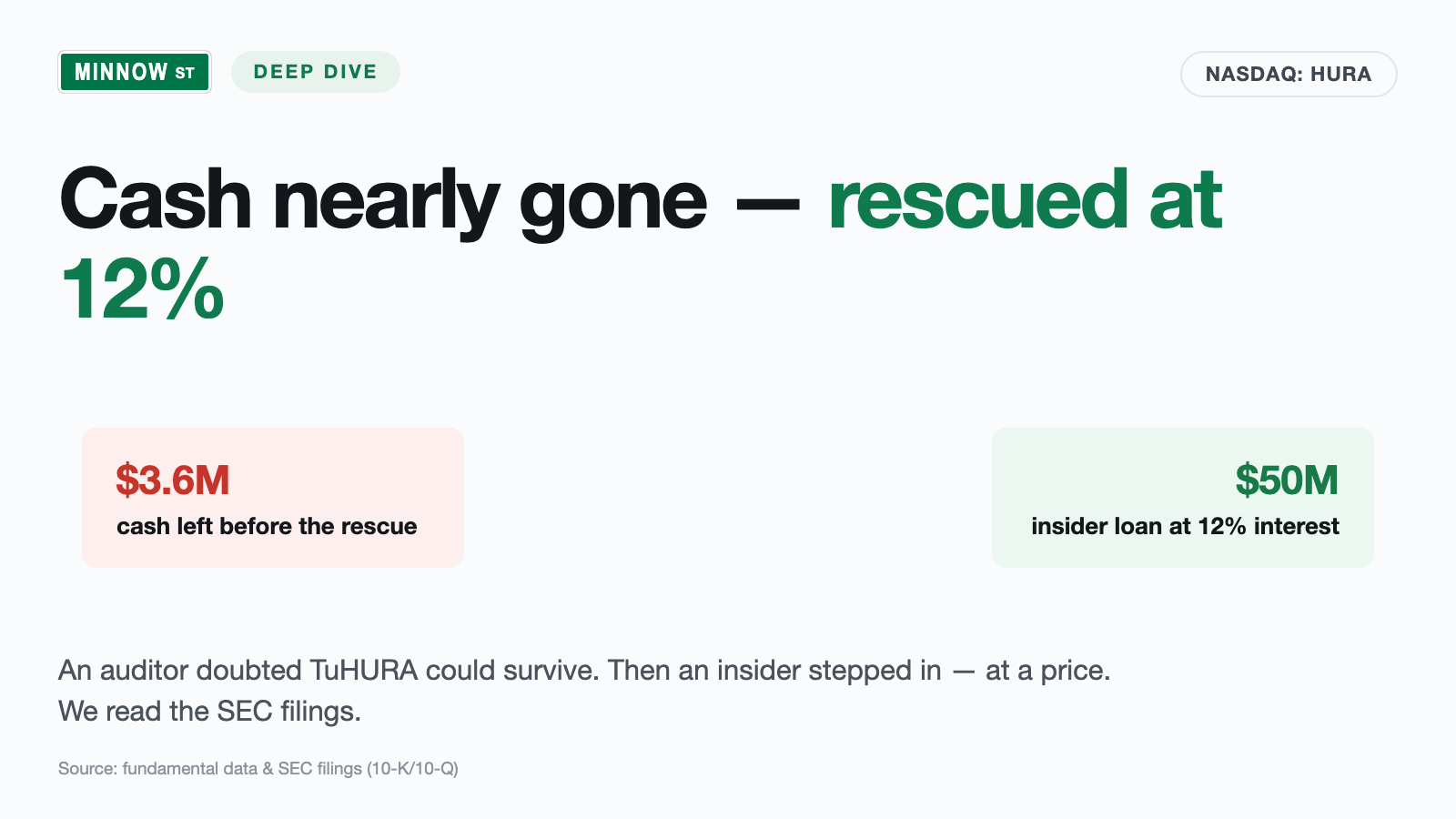

TuHURA Stock: The Auditor Doubts the Company Can Survive — Then an Insider Lends 50 Million at 12 Percent

TuHURA Biosciences is building a cancer immunotherapy that makes tumors look to the immune system like bacteria — a fascinating idea now being tested in Phase 3 against rare Merkel cell skin cancer. Only, at the turn of the year the company had just $3.6 million left in the till, and the auditor wrote a going-concern qualification into its opinion. We read the annual report (10-K) for 2025 and the quarterly report (10-Q) as of March 31, 2026: not a cent of revenue, $141 million in accumulated losses — and a rescue in April 2026 that comes from a company attributable to the major shareholder, at 12 percent interest, secured against everything, including a perpetual royalty on the lead drug. Not investment advice — just a cash count before you bet on the all-clear.

There is a reflex that reliably leads investors astray, precisely with troubled companies: call it the all-clear reflex. A company is visibly in distress, everyone holds their breath — and then comes news that sounds like rescue: a financing, a loan, a partner. Relieved, the crowd exhales, the price jumps, and "this could go bankrupt" turns, emotionally, into "the danger is over." Hardly any case plays this reflex as instructively right now as TuHURA Biosciences (NASDAQ: HURA): a cancer biotech with $3.6 million in the till, an auditor who doubts it can survive — and a stock that has nonetheless risen 178 percent in six months. So let's make a deal: before you mistake the rescue for the end of the danger, we read together what TuHURA itself reported to the U.S. securities regulator, the SEC — in the annual report (10-K) for 2025 and the quarterly report (10-Q) as of March 31, 2026. An SEC filing is honest under penalty of law. And there it stands: who finances the rescue, and at what price. In the end, you decide for yourself.

What TuHURA actually does

Picture the immune system as a plant-security force that reliably spots intruders — but around which cancer cells camouflage well and are simply waved through. This is exactly where TuHURA comes in, a clinical-stage immuno-oncology company from Tampa, Florida. "Clinical" means: it researches and tests, it sells nothing yet. Its toolbox is the ImmuneFx platform — a construction kit of cell and gene therapies meant to make the immune system recognize and attack tumor cells. The trick of the lead agent IFx-2.0 is as vivid as it is bold: doctors inject a small amount of a set of building instructions (pDNA) directly into the tumor; these instructions make the tumor cell carry a bacterial protein on its surface — the tumor suddenly looks to the immune system like a bacterium and gets attacked. IFx-2.0 is being tested as an adjunctive therapy to the established immune drug pembrolizumab (trade name Keytruda), specifically against Merkel cell carcinoma, a rare, aggressive skin cancer.

Since 2025 there is a second candidate on top, TBS-2025, which TuHURA obtained through the acquisition of the company Kineta: a bispecific antibody approach meant to shut down the immunosuppressive cells in the tumor environment. Sounds like an elegant bet on the future? Perhaps it is. But note here already the central tension of this analysis: a fascinating cancer idea with a tangible approval path — carried by a company without a cent of revenue, whose cash was at times nearly empty and which could obtain fresh money only at distress rates from one of its own major shareholders. It runs through every chapter. How similarly and yet differently such "one-product bets" can end is shown by comparison in our analysis of Replimune — there, too, the FDA alone decides in the end.

Where the stock shows up in our scanner

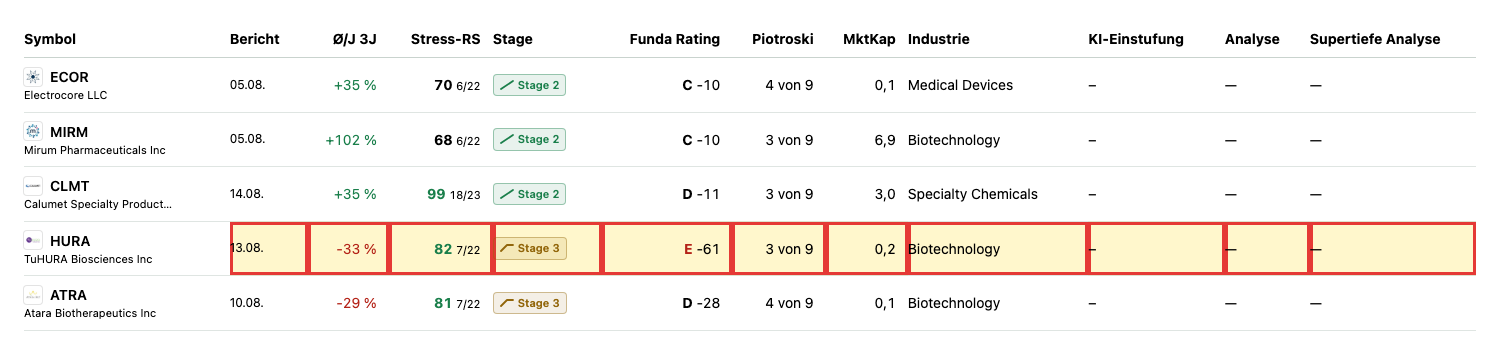

Every day we run about 3,500 stocks through our scanners. TuHURA lights up in an instructive mix (data as of July 8, 2026). On the warning side stands a whole distress trio right away: the "Insolvency Radar: cash running low" — the list this analysis came from — the "Going Concern (Distress Proxy)" and the "Altman-Z Distress Zone". The Altman-Z score, a classic insolvency early-warning measure built from several balance-sheet ratios, sits for TuHURA deep in the red (the danger zone historically begins below 1.1). The Piotroski F-Score, a nine-point test of balance-sheet quality, stands at 3 of 9 — a rock-solid company sits at 8 or 9 — and the in-house fundamental rating awards the grade E. And here is the remarkable part: with TuHURA the quantitative suspicion coincides with the original — the auditor actually wrote the going-concern doubt into the 2025 opinion. How such warning lists should be read — smoke detectors, not demolition orders — we explained in the piece "Insolvency Radar: the Top 10".

And now the contradiction that makes this stock so special: on the other side stands a momentum surge. The price has risen about 178 percent in six months and sits 532 percent above its 52-week low — which is why TuHURA appears at the same time in the scanner "Qullamaggie: Top Gainers 6M" and in the filter for high daily volatility. It is precisely this altitude high that the scanner Weinstein Stage 3 flags as a warning, not an invitation: a top formation, an uptrend losing steam. One detail sets TuHURA apart from many other price rockets: only about 15 percent of the shares sit with institutions, but about 35 percent with insiders — this is not a broad professional bet but a thinly traded micro-cap story in which single pieces of news carry the price far. A price fireworks display next to three insolvency-warning scanners is no proof of a bargain, but a price tag on a bet.

The numbers over the years — honestly appraised

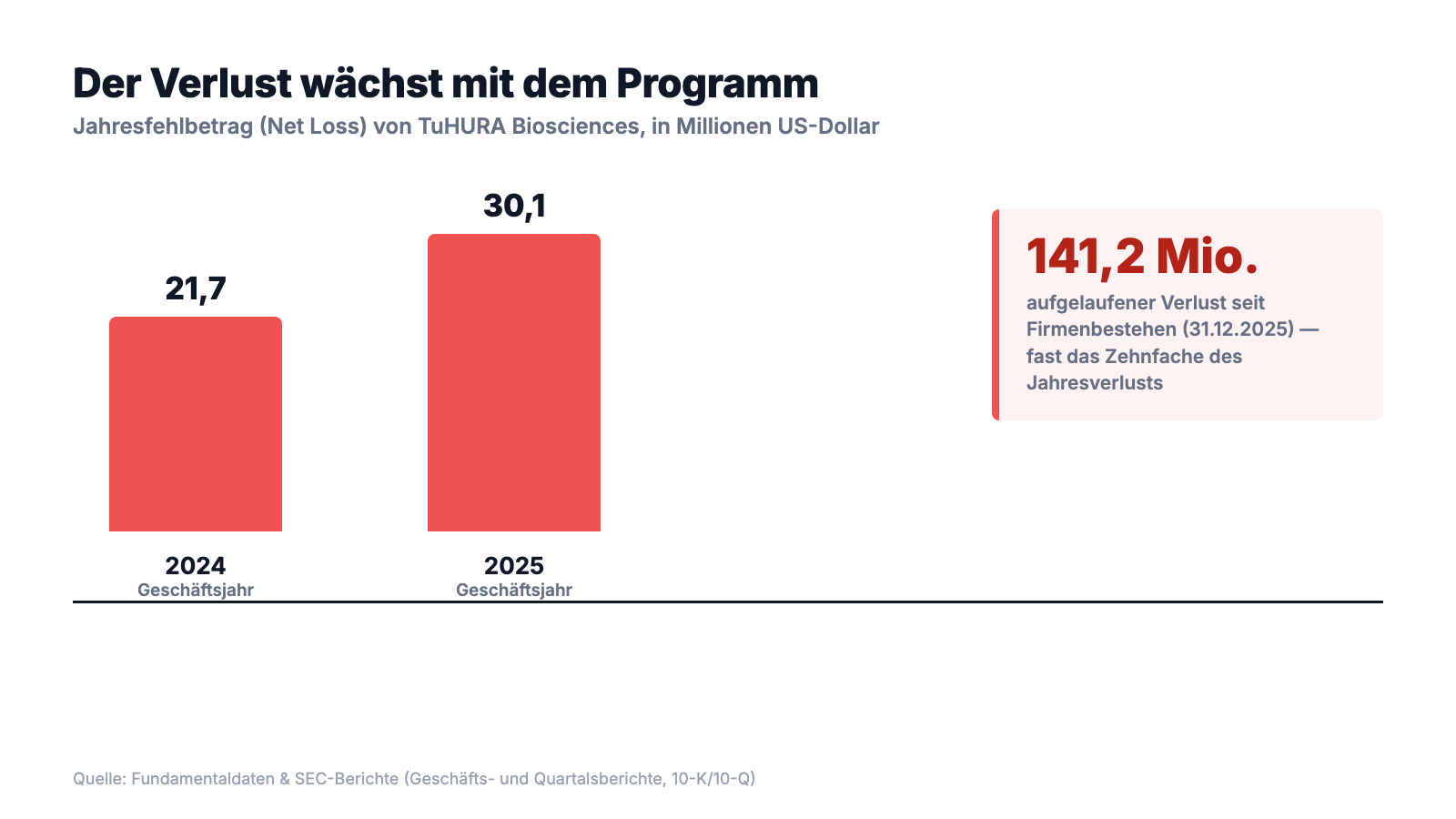

With a clinical biotech one has to be honest: there is no revenue curve to admire, because there is no revenue. TuHURA has never earned a dollar with a product — that is no hidden weakness but the essence of the thing: the company is a research lab working against the clock. What there is to appreciate is the progress of the program — and that has its price. The net loss rose from $21.7 million (2024) to $30.1 million (2025); the biggest chunk is research itself ($20.5 million), plus $7.6 million of administration and $3.7 million of acquisition costs for the Kineta deal. Per share, 2025 showed a loss of $0.63.

Add up all the losses since inception, and an accumulated deficit of $141.2 million sits on the books (December 31, 2025). This was financed almost entirely through the sale of new shares and convertible notes: since inception TuHURA has raised about $99.7 million net through capital measures. It shows in the share count, which has practically exploded — from 12.2 million (end of 2024) via 59.3 million (end of 2025) to 63.6 million (March 31, 2026). Remember this second side of the biotech coin: every bit of progress is paid for with fresh shares — and your slice of the cake gets smaller when new slices keep being cut. Unlike at some over-indebted industrial group, by the way, TuHURA's equity is positive (about $20.9 million at year-end) — the problem is not a mountain of debt but simply the emptying till. Which brings us to the uncomfortable truths.

What the filings say — the uncomfortable truths

Uncomfortable truth no. 1: the company's own auditor doubts it can survive

There is hardly a harder signal in an annual report than this one. An auditor normally confirms, soberly, that the numbers are correct. In rare cases, though, it adds a warning — the going-concern qualification: doubt about the company's ability to continue. That is exactly what happened at TuHURA for fiscal year 2025. The company writes itself:

"In our financial statements for the years ended December 31, 2025 and 2024, we concluded that our recurring losses from operations and need for additional financing to fund future operations raise substantial doubt about our ability to continue as a going concern. Similarly, our independent registered public accounting firm included an explanatory paragraph in its report on our financial statements for the year ended December 31, 2025 with respect to this uncertainty."

— TuHURA Biosciences, SEC annual report 10-K 2025, Item 1A "Risk Factors" (Going Concern)

A going-concern qualification is not a bankruptcy filing — it means: "Without fresh money in the next twelve months, it gets tight." But it is the most honest alarm signal an audited set of accounts knows, and here it comes not from a computational model but from the pen of those who saw the books most closely. How tight "tight" really was is shown by a look into the till.

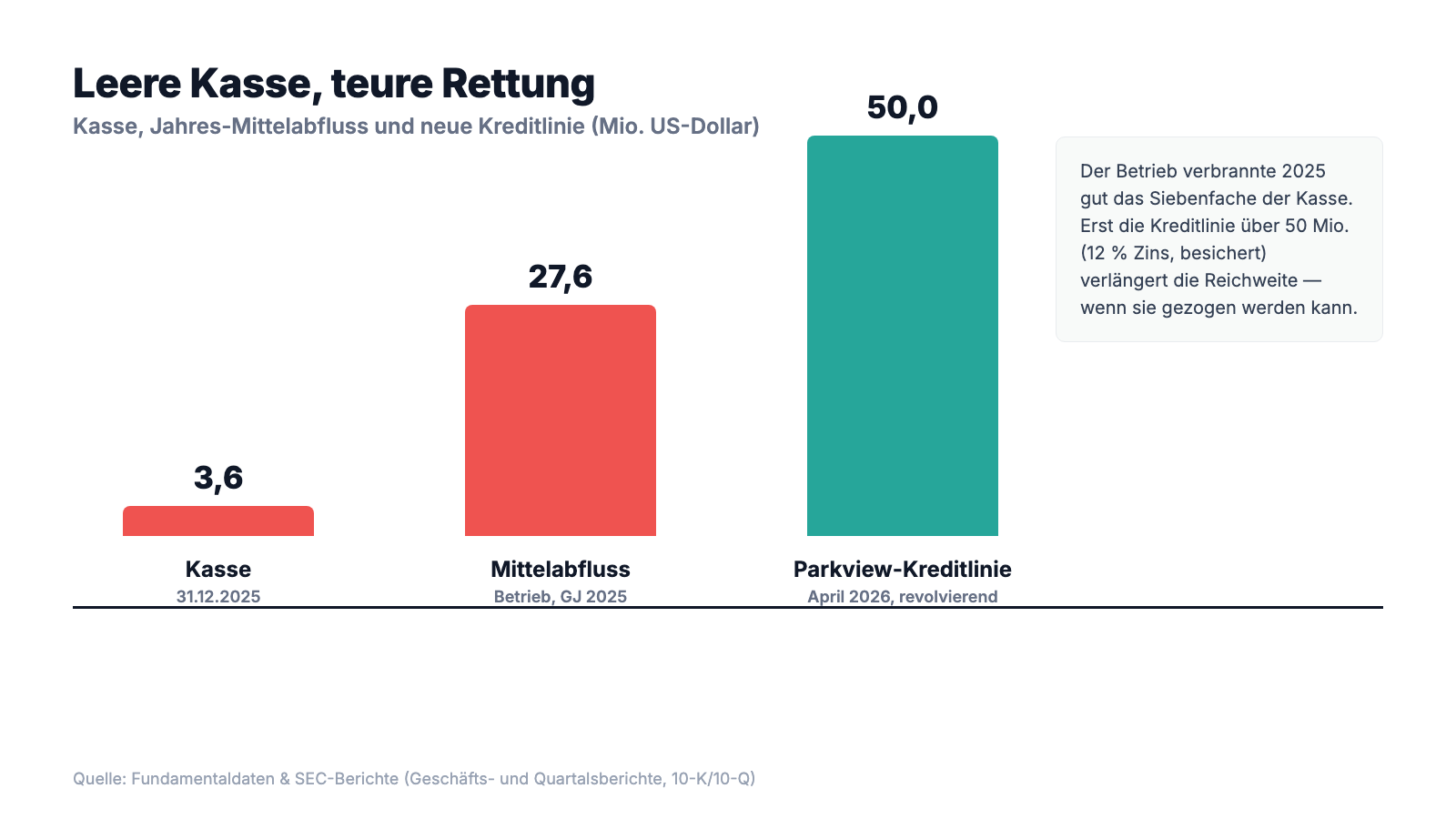

Uncomfortable truth no. 2: the till was nearly empty — $3.6 million against $27.6 million of annual burn

The bare arithmetic reads dramatically. As of December 31, 2025, TuHURA's till held only $3.6 million — while ongoing operations in the same year had burned $27.6 million of cash. That is a tank not on reserve but nearly dry. The company itself puts the runway in the annual report — and the time horizon is remarkably short:

"As of December 31, 2025, we had cash and cash equivalents of $3.6 million. Based on our current operating plan, we believe that our existing cash, cash equivalents and short-term investments, together with the $7.0 million received in the first quarter from the December 2025 registered direct offering, should be sufficient to fund our operations through early third quarter of 2026."

— TuHURA Biosciences, SEC annual report 10-K 2025, Item 7 MD&A "Liquidity and Capital Resources"

It is exactly here that the all-clear reflex from the beginning kicks in — because shortly after the balance-sheet date the rescue arrived. And it is a big deal.

Uncomfortable truth no. 3: the rescue came from an insider — at 12 percent, with a lien on everything

In April 2026 the tide seemed to turn: TuHURA secured a revolving credit facility of $50 million. With it, the most recent quarterly-report update suddenly re-states the runway — "through the end of 2028" — and, genuinely remarkable, the quarterly document cites no going-concern qualification any more. Sounds like the classic all-clear. But look at who is doing the rescuing and at what price:

"On April 21, 2026, the Company entered into a Loan Agreement with Parkview Holdings One LLC (“Parkview”), an affiliate of K&V Investment LLC (“K&V Investment One”) (a holder of more than 5% of the Company's fully diluted capital stock and an entity owned by Vijay Patel), pursuant to which Parkview agreed to extend a $50 million revolving credit facility to the Company maturing on April 21, 2031. Borrowings under the facility bear interest at 12% per annum (plus an additional 6% during any event of default), payable monthly in arrears, and are secured by substantially all assets of the Company and its subsidiaries."

— TuHURA Biosciences, SEC quarterly report 10-Q as of March 31, 2026, Note 14 "Subsequent Events"

The fine print makes the rescue even more expensive: on top of the double-digit interest come an annual commitment fee of 1.5 percent, the obligation to use 75 percent of net profits from drug sales for repayment — and a perpetual royalty: Parkview receives a low-to-mid single-digit license fee on the net revenue of future IFx-2.0 products, up to $450 million of revenue per year, continuing until the expiry of the last IFx-2.0 patent. Pause here for a moment, because this is the core of the all-clear reflex: yes, the acute cash distress is defused, and the going-concern qualification has vanished from the quarterly report. But the runway "through the end of 2028" presupposes that TuHURA can actually draw the facility — the report lists exactly that as a risk of its own — it is paid for at distress rates, it pledges the entire assets, and it hands a major shareholder a permanent slice of the greatest success case. A rescue that secures survival and at the same time makes it more expensive is not an all-clear — it is a new clock that ticks.

Uncomfortable truth no. 4: no revenue — the entire value hangs on a single approval

In the end, everything at TuHURA runs toward one question: will IFx-2.0 be approved? The company has negotiated an unusually clear regulatory path for the lead agent — and describes it itself:

"We have entered into a Special Protocol Assessment agreement with the FDA for a single Phase 3 randomized placebo and injection-controlled trial for IFx-2.0, our lead innate immune agonist, as an adjunctive therapy to pembrolizumab (Keytruda) in the first line treatment of patients with advanced or metastatic Merkel cell carcinoma, who are checkpoint inhibitor-naïve utilizing the FDA's accelerated approval pathway."

— TuHURA Biosciences, SEC annual report 10-K 2025, Item 1 "Business"

For the valuation this has a radical consequence: the metrics with which one measures normal companies run into a void here. There is no price-to-earnings ratio (no earnings), a price-to-sales ratio is meaningless (no sales). What you buy when you buy this stock is not a running business but an option warrant on an approval: if it comes, IFx-2.0 can address a real, if niche, market and today's price will look small in hindsight. If it does not come, what remains is a company with an empty till, a secured insider debt and a drug without market access. The report itself expressly dampens the hope: a Special Protocol agreement "does not increase the likelihood of an approval." Remember the sentence: a ticket without revenue is worth as much as the market currently believes in the jackpot — and that belief can halve or double on a single trial result.

Valuation: about $0.17 billion in market value — for a bet without revenue

In early July 2026 the TuHURA stock cost about $2.60; at about 63.6 million shares that makes a market value of about $0.17 billion (data as of July 8, 2026). The usual valuation measures deliberately do not apply: no price-to-earnings ratio (no earnings), no meaningful price-to-sales ratio (no revenue). The most honest framing is a comparison: against the $0.17 billion of market value stand an accumulated deficit of $141.2 million, a cash balance last at $6.3 million (March 31, 2026) and a secured credit facility of $50 million whose interest sits at 12 percent. Put differently: you are paying not for what is, but exclusively for what could be. That is exactly why the price moves so extremely — plus 178 percent in six months, plus 532 percent above the 52-week low, and yet almost the entire former value of the predecessor shell destroyed (all figures: data as of July 8, 2026). That only about 15 percent of the shares sit with institutions and about 35 percent with insiders makes the matter no calmer: a thinly traded paper with a binary outcome swings far in both directions.

Opportunities and risks at a glance

What speaks for TuHURA:

- A fascinating cancer idea with a clear regulatory path: IFx-2.0 makes tumors look to the immune system like bacteria; for the lead candidate there is a Phase 3 trial agreed with the FDA (Special Protocol Assessment) in Merkel cell carcinoma via the accelerated approval pathway, Phase 3 since June 2025 (annual report 10-K 2025).

- The acute cash distress is defused for now: with the $50 million credit facility the company puts its runway at "through the end of 2028"; the most recent quarterly report (10-Q as of March 31, 2026) no longer cites a going-concern qualification.

- No crushing mountain of outside debt and positive equity (about $20.9 million as of December 31, 2025) — the problem was liquidity, not over-indebtedness.

- A second leg to stand on: through the Kineta acquisition, another drug candidate, TBS-2025, came into the house, meant to prevent resistance to checkpoint inhibitors — a reserve ticket, should IFx-2.0 stumble.

What speaks against it:

- The auditor gave the 2025 annual report a going-concern qualification; cash stood at only $3.6 million as of December 31, 2025, operating cash outflow at $27.6 million, the runway per the 10-K only "through early third quarter of 2026."

- The rescue is expensive and from inside: an entity attributable to major shareholder Vijay Patel lends at 12 percent (plus 6 percent on default), secured by virtually all assets, including a 75-percent profit sweep and a perpetual royalty on IFx-2.0 — and the runway "through the end of 2028" presupposes the facility can be drawn at all.

- Not a cent of product revenue; net loss up from $21.7 to $30.1 million, accumulated deficit $141.2 million; the share count multiplied within a year from 12.2 to 63.6 million — ongoing, heavy dilution.

- Binary approval risk: the entire value hangs on IFx-2.0; the FDA agreement "does not increase the likelihood of an approval." Plus warning signals: three insolvency scanners, Altman-Z deep in the red, Piotroski 3 of 9, fundamental rating E, a survived but recurring Nasdaq one-dollar threshold (data as of July 8, 2026).

A human conclusion

Back to the all-clear reflex from the beginning. It has a true core: TuHURA's idea is real, the approval path is unusually clear, and the $50 million credit facility has indeed averted the acute bankruptcy danger — the going-concern qualification has vanished from the most recent quarterly report, and that is no small thing. But this is exactly where the thinking error sits that this case can show you: a rescue is not the end of the danger, but its move to another line of the balance sheet. "Is the till about to run dry?" has become "can the expensive, secured insider facility be drawn, and does the bet on IFx-2.0 pay off before interest, profit sweep and royalty eat up the substance?" That does not make TuHURA a "bad" or "good" company, but a bet with clear conditions: whoever gets in here buys neither substance nor earnings, but the probability of a single yes or no — and pays for the waiting with a clock that ticks at 12 percent a year. If the yes comes, the slim market value can lever far upward; if the no comes, it hits a company that has already pledged its entire assets. Both are possible, neither is certain. Whoever takes this bet should do it because they have understood its conditions — not because a rescue announcement felt like an all-clear. What you make of it is your decision. And that is exactly as it should be.

Sources

All original documents used in this analysis — to read for yourself:

- TuHURA Biosciences, Inc. — SEC annual report 10-K for 2025 (filed March 31, 2026)

- TuHURA Biosciences, Inc. — SEC annual report 10-K for 2024 (filed March 31, 2025)

- TuHURA Biosciences, Inc. — SEC quarterly report 10-Q as of March 31, 2026 (filed May 15, 2026)

- TuHURA Biosciences, Inc. — SEC quarterly report 10-Q as of September 30, 2025 (filed November 14, 2025)

- TuHURA Biosciences, Inc. — SEC quarterly report 10-Q as of June 30, 2025 (filed August 14, 2025)

- TuHURA Biosciences, Inc. — SEC quarterly report 10-Q as of March 31, 2025 (filed May 15, 2025)

- TuHURA's complete SEC filing history: EDGAR overview (sec.gov)

- Fundamental data (metrics, quarterly series, valuation; data as of July 8, 2026), reconciled with the SEC filings.

- Screener and rating data: in-house stock scanner (data as of July 8, 2026).

Transparency & disclaimer: This analysis is a journalistic contextualization of publicly available information and is not investment advice, not a financial analysis in the regulatory sense, and not a solicitation to buy or sell securities. It expressly contains no judgment on whether an insolvency will occur or whether an approval will be granted. Stock investments carry substantial risks up to total loss — with clinical biotech names to a particular degree. All information without guarantee; the data cut-off is noted in the text in each case. The author holds no position in TuHURA stock at the time of publication.

Our Bottom Line at a Glance

- Technology & program positive

- The ImmuneFx idea is fascinating: IFx-2.0 makes tumors look to the immune system like bacteria. For the lead candidate there is an unusually clear regulatory path — a Phase 3 trial agreed with the FDA (Special Protocol Assessment) in Merkel cell carcinoma via the accelerated approval pathway, Phase 3 since June 2025 (annual report 10-K 2025).

- Going concern & liquidity negative

- The auditor gave the 10-K 2025 a going-concern qualification; cash stood at only $3.6 million as of December 31, 2025, against $27.6 million of annual cash outflow. The $50 million credit facility of April 2026 defuses the acute distress (runway per the 10-Q "through the end of 2028"), but presupposes the facility can be drawn.

- Rescue & governance negative

- The credit facility comes from an insider (Parkview/K&V, an entity owned by major shareholder Vijay Patel, stake over 5%): 12% interest (plus 6% on default), secured by virtually all assets, including a 75-percent profit sweep and a perpetual royalty on future IFx-2.0 revenue. A rescue that secures survival and at the same time makes it more expensive.

- Loss & dilution negative

- No product revenue since inception; net loss up from $21.7 to $30.1 million, accumulated deficit $141.2 million. The share count multiplied within a year from 12.2 to 63.6 million — ongoing, heavy dilution, most recently intensified by the Kineta acquisition.

- Market & momentum neutral

- Plus 178 percent in six months and plus 532 percent above the 52-week low, carried by approval and rescue hope; technical scanners read the rally as a top formation (Weinstein Stage 3). Only about 15 percent institutional and about 35 percent insider ownership — a thinly traded micro-cap paper with a binary outcome.

TuHURA is not a case of substance versus story, but a pure bet with clear conditions: a fascinating cancer technology with a clear Phase 3 path on one side — on the other an auditor who doubted the company could survive for 2025, not a cent of revenue, $141 million in accumulated losses and a rescue that comes from a major shareholder: $50 million at 12 percent, secured against everything, including a perpetual royalty on the lead drug. The acute bankruptcy danger is defused — the price for it is a new, expensive clock that ticks. Not investment advice.

What Our Rating Means

- If you don't own the stock

- In our view, the documented risks clearly outweigh — we see no basis for an entry.

- If you hold it in your portfolio

- In our view, the findings carry enough weight to warrant a critical look at your own position.

A journalistic assessment by our editorial team at the time of the deep dive, based on public sources — not investment advice and not a solicitation to buy or sell. Your personal circumstances (investment goals, risk capacity, taxes) cannot be taken into account. What our categories mean, how verdicts are formed, and what conflicts of interest exist →

Worth Noting

- TuHURA emerged in October 2024 from the reverse merger with Kintara Therapeutics (1-for-35 reverse stock split, name change from KTRA to HURA); price and share history before October 2024 belong to the predecessor shell. The 2013 IPO year listed in databases refers to this shell.

- The disappearance of the going-concern qualification in the 10-Q as of March 31, 2026 rests on the $50 million credit facility agreed only after the 10-K (April 2026); its runway "through the end of 2028" presupposes, per the report, that the facility can be drawn.

- Price, valuation and scanner figures dated to July 8, 2026 (about $2.60); analyses are evergreen, daily prices are not a buy argument.

Frequently Asked Questions

TuHURA (NASDAQ: HURA) of Tampa, Florida, is a clinical-stage immuno-oncology company. Its ImmuneFx platform builds, from cell and gene therapies, agents that sic the immune system on tumors. The lead candidate is IFx-2.0: a set of building instructions injected into the tumor tissue makes the tumor cell carry a bacterial protein, so that the tumor looks to the immune system like a bacterium. The company sells no product yet and earns no revenue.

Because the classic distress signals apply: no revenue, high cash burn, Altman-Z deep in the red, Piotroski 3 of 9. What is decisive is that the suspicion is confirmed by the original: the auditor gave the 2025 annual report a going-concern qualification — "substantial doubt" about the company's ability to continue, because cash stood at only $3.6 million as of December 31, 2025.

As of December 31, 2025, $3.6 million sat in the till; as of March 31, 2026 it was $6.3 million. In fiscal year 2025 operations burned $27.6 million. Per the annual report the cash (including a capital increase) was sufficient only "through early third quarter of 2026" — only the $50 million credit facility agreed in April 2026 stretches the runway per the quarterly report to "through the end of 2028."

An insider: the revolving credit facility comes from Parkview Holdings One, an affiliate of K&V Investment and an entity owned by major shareholder Vijay Patel (stake over 5 percent). The terms are hard: 12 percent interest (plus 6 percent on default), secured by virtually all of the company's assets, plus a perpetual royalty on future IFx-2.0 revenue and a 75-percent profit sweep for repayment.

TuHURA is the listed vehicle of the former Kintara Therapeutics (ticker KTRA), a cancer company whose own programs failed. On October 18, 2024, Kintara carried out a 1-for-35 reverse stock split, merged with the private legacy TuHURA and renamed itself TuHURA Biosciences. The 2013 IPO year in many databases belongs to the predecessor shell.

No. In the SEC filings reviewed, the terms "artificial intelligence" and "machine learning" do not appear a single time. The business is purely biological (cell and gene therapies, pDNA-based immune agonists, antibody-drug conjugates). In our company-specific AI classification, TuHURA is therefore rated as "Neutral."

This analysis expressly issues no insolvency verdict. Facts: the auditor reported "substantial doubt" about the company's ability to continue for 2025, and the till was nearly empty. At the same time the $50 million credit facility of April 2026 has defused the acute distress, the most recent quarterly report no longer cites a going-concern qualification and puts the runway at "through the end of 2028." The outcome hangs on the drawability of that facility and on the IFx-2.0 approval.

Found an error?

Did you spot a factual error, an outdated number, or a typo in this deep dive? Let us know briefly — your report goes straight to the editorial team.