Taysha Stock: The Insolvency Scanner Sounds the Alarm — Yet the Cash Lasts into 2028

Taysha builds a "living medicine" from a virus that is meant to stop one of the cruelest childhood diseases — Rett syndrome. The stock turns up in our insolvency warning scanner, and at first that fits: not a cent of revenue, $753.7 million in accumulated deficit, a loss that keeps growing. But whoever reads the annual report (10-K) for 2025 and the quarterly report (10-Q) as of March 31, 2026 pauses: $276.6 million in cash, runway per the company into 2028, no going-concern qualification from the auditor. The warning label is a smoke detector, not a fire — the real bet lies elsewhere. Not investment advice — just a cash count behind the red warning sign.

There is a mental trap that costs you more on the stock market than almost any other: let's call it the label reflex. We see a sign — a red "Warning!" or a green "Future!" — and let the sign decide for us instead of looking behind it. Hardly any stock demonstrates this reflex as beautifully right now as Taysha Gene Therapies (NASDAQ: TSHA): a gene-therapy company from Dallas that works on one of the cruelest childhood diseases — and whose stock sits in our insolvency warning scanner. The red label screams "danger". And at first glance it seems to be right: not a cent of revenue, a loss that grows every year, $753.7 million in piled-up losses. But then you read on — and find $276.6 million in the bank and an auditor who explicitly raises no doubt about the company's survival. So let's make a deal: before you believe the label — in whichever direction — we read together what Taysha itself reported to the U.S. securities regulator, the SEC: in the annual report (10-K) for 2025 and in the quarterly report (10-Q) as of March 31, 2026. An SEC filing is honest under penalty of law. And there stands what this stock is really about — not survival until tomorrow, but a single bet. In the end, you decide for yourself.

What Taysha actually does

Picture the genome of a cell as a thick recipe book. In Rett syndrome — a severe neurological disorder that strikes almost only girls — a single, decisive page is missing: the MECP2 gene. Without it, children develop normally at first, then lose speech and hand use, suffer seizures, and need lifelong care. This is where Taysha comes in, a clinical gene-therapy company from Dallas. Clinical means: it researches and tests, it sells nothing yet. The idea is as elegant as it is bold: take a disarmed virus (a so-called AAV9 vector — practically an empty delivery van from which the disease-causing cargo has been removed and the missing gene page packed in instead) and deliver this "living medicine" straight into the cerebrospinal fluid. The virus smuggles the missing blueprint into the nerve cells — one injection, so the hope goes, instead of lifelong treatment. Taysha calls this lead candidate TSHA-102.

And now the point you should remember for the rest of this analysis: TSHA-102 is Taysha's only drug candidate in clinical development. There is an early pipeline (such as TSHA-113 against certain forms of dementia), but that is a distant prospect. The entire value of the company today hangs on this one molecule and a single agency — the U.S. approval authority, the FDA. Sounds like an elegant bet on the future? Perhaps it is. But note here already the central tension of this analysis: a company that stands surprisingly solid financially — and whose stock is nonetheless a pure yes/no bet on a single medicine. It runs through every chapter. How differently such "single-product bets" can turn out is shown, for comparison, by our analysis of Replimune — also a cancer biotech in the same warning scanner, but there with a genuine auditor's doubt about survival.

Where the stock shows up in our scanner

Every day we run about 3,500 stocks through our scanners. Taysha lights up in a telling mixture (data as of July 13, 2026). On the warning side stands the "Going Concern (Distress-Proxy)" — a filter that hunts for the classic signs of a shaky balance sheet: an Altman Z-Score in the danger zone (an insolvency early warning built from several balance-sheet ratios; at Taysha it sits near zero, clearly below the critical mark), no revenue, negative operating cash flow. The Piotroski F-Score, a nine-point test of balance-sheet quality, stands at 4 of 9 — a thoroughly healthy company stands at 8 or 9. The fundamental rating is D. All red, all as expected.

And now comes the catch that no label reveals: this scanner is expressly only a quantitative approximation — a smoke detector, not an auditor's opinion. And at Taysha the smoke detector goes off for a reason that is built in at a biotech lab: the Altman Z-Score punishes almost automatically any company that makes no revenue and piles up losses — it was invented decades ago for classic industrial corporations, not for research firms whose business model is to burn money before they earn any. Unlike the similarly placed Replimune, where the auditor actually wrote the going-concern doubt into the opinion, at Taysha the original contradicts the smoke detector. How such warning lists are to be read — a smoke detector, not a demolition notice — we explained in the article "Insolvency Radar: the Top 10". That alongside it the technical scanners report strong momentum (plus 178.7 percent over twelve months, price above the average lines, Weinstein Stage 2) only makes it more intriguing: the market is betting on something — more on that shortly.

The numbers over the years — honestly appraised

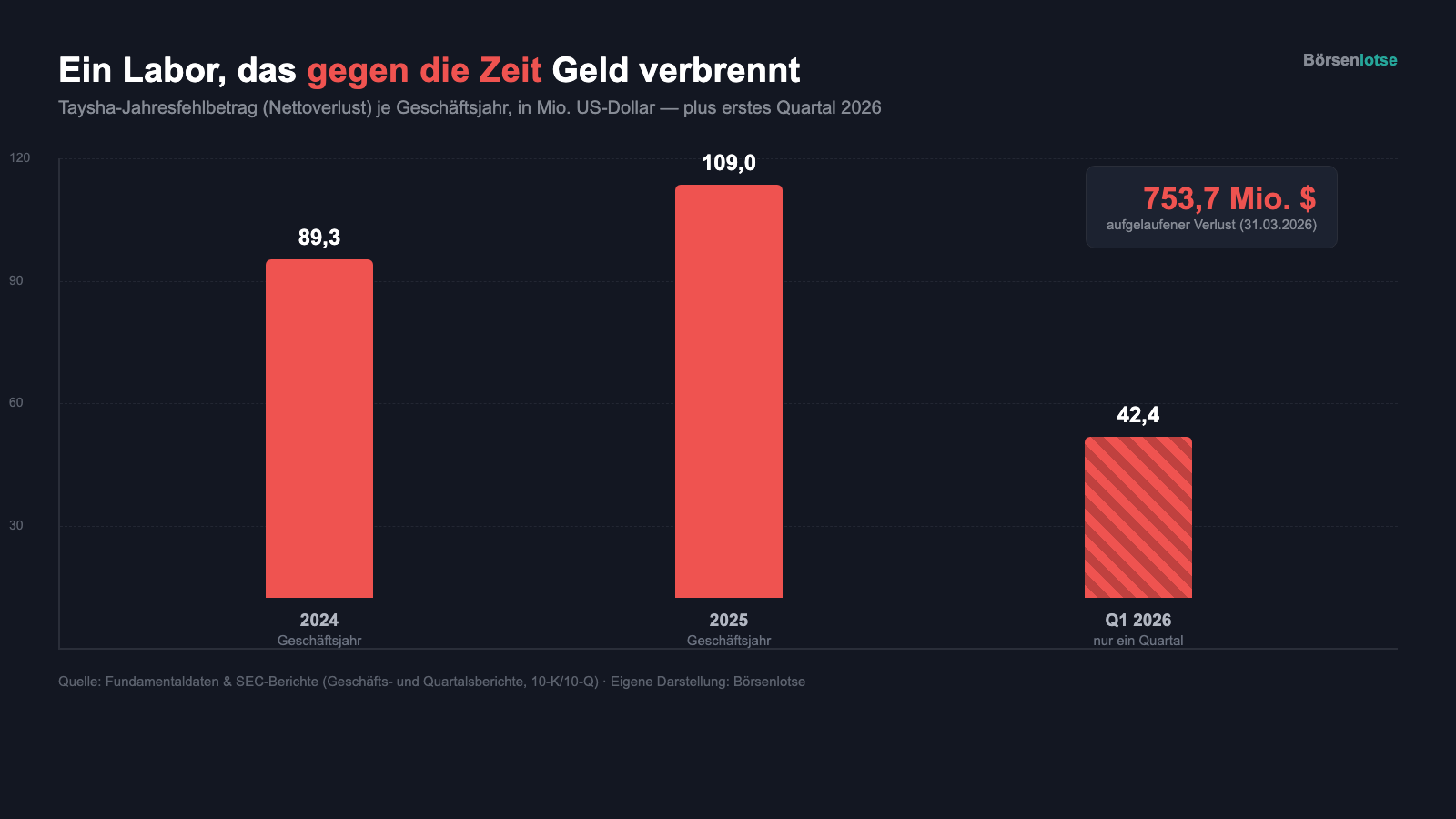

At a clinical biotech you have to be honest: there is no revenue curve to admire, because there is no revenue. Taysha has not earned a single dollar from a product since its founding — that is not a weakness to hide, but the nature of the thing: the company is a large research lab working against the clock. What there is to appreciate (and to scrutinize) is the price of this progress. The net loss has grown as the trials advanced: from $89.3 million (2024) to $109.0 million (2025), and in the first quarter of 2026 it already stood at $42.4 million. The largest chunk is research itself: $86.4 million in research and development expenses in 2025 (after $66.0 million in 2024), plus $33.9 million for administration.

Add up all the losses since the company began, and there stands an accumulated deficit of $753.7 million in the books (March 31, 2026). And now comes the part the red label leaves out: unlike a truly staggering company, Taysha sits on a full tank. As of December 31, 2025, $319.8 million lay in the cash box, and as of March 31, 2026 still $276.6 million. Because 2025 was an exceptional financing year: on balance, $274.6 million in fresh capital flowed in, and the cash balance rose over the year by $180.9 million. That is exactly the second side of the biotech coin you should remember: a research lab does not survive from cash flow, but from the capital market — and as long as the market plays along, "no revenue" is no death sentence. But this fresh money has a price, and it brings us to the uncomfortable truths.

What the filings say — the uncomfortable truths

Uncomfortable truth no. 1: not a cent of revenue — and a loss larger than half the company

As understandable as the business model is, the balance-sheet reality is just as merciless. Taysha writes it itself, right at the start of the risk chapter — it hardly gets more sober:

"We have no products approved for commercialization and have never generated any revenue from product sales. […] Since our inception, we have incurred significant net losses. […] Our net losses were $109.0 million and $89.3 million for the years ended December 31, 2025 and 2024, respectively. As of December 31, 2025, we had an accumulated deficit of $711.3 million."

— Taysha Gene Therapies, SEC annual report 10-K, fiscal year 2025, Item 1A "Risk Factors"

Put this number in perspective: the accumulated deficit of $753.7 million (as of March 31, 2026) is in the same order of magnitude as the entire market value of the company. Translated: the price does not value the past — that is a deep hole — but exclusively the future of a single medicine. Whoever holds Taysha shares buys no substance and no profit, but a probability. And that is decided, see uncomfortable truth no. 2, at a single point.

Uncomfortable truth no. 2: everything hangs on a single drug — and a single agency

Diversification is the investor's best friend. Taysha is its opposite. The company says so itself, in a sentence that leaves nothing to be desired in clarity:

"We are substantially dependent on the success of our lead product candidate, TSHA-102, which is currently our sole product candidate in clinical development."

— Taysha Gene Therapies, SEC annual report 10-K, fiscal year 2025, Item 1A "Risk Factors"

What sounds troubling for the stock is medically encouraging: TSHA-102 carries strong FDA designations — Breakthrough Therapy (September 2025, an acceleration status for especially promising therapies), plus RMAT, Fast Track, Orphan Drug and the rare-pediatric-disease designation. Taysha has aligned the design of the pivotal REVEAL trial with the agency: 15 patients, each her own control, with a six-month interim analysis that could already form the basis for the approval filing (BLA). And the early data are strong — a response rate of 83 percent (5 of 6 patients on high dose, data cut May 2025), no serious treatment-related adverse events among the first twelve patients (data cut March 2026). But do not confuse "encouraging" with "certain": a gene therapy is a binary event. If the FDA says yes, the value can multiply. If it says no — or demands, as happened in the Replimune case, a further trial — the only pillar on which everything rests gives way. There is no second drug to catch the fall. Remember this tension: the balance sheet is more solid than the label — but the business is a coin toss with a high stake.

Uncomfortable truth no. 3: survival is paid for with fresh shares — and your slice shrinks

We have seen that Taysha is financially well cushioned. Now the flip side: where does this cushion come from? Not from sales — there are none — but almost entirely from issuing new shares. In 2025 alone the company raised $274.6 million: $215.6 million through a large share placement in May 2025, $50.0 million through a loan from Trinity Capital and $48.4 million by simply selling 10.23 million shares bit by bit over the exchange in November and December 2025 (a so-called ATM program, "at the market"). The company names the consequence in the risk chapter without mincing words:

"Raising additional capital may cause dilution to our stockholders, restrict our operations or require us to relinquish rights to our technologies or product candidates."

— Taysha Gene Therapies, SEC annual report 10-K, fiscal year 2025, Item 1A "Risk Factors"

Translated, dilution means: your slice of the pie gets smaller when new slices are constantly cut off. The share count now stands at about 287 million — plus pre-funded warrants that can turn into real shares practically at any time for a fraction of a cent. As long as TSHA-102 is not approved, Taysha will keep needing fresh money, and the most likely route there is the one the company already took in 2025: even more shares. The cash lasts, per the report, "into 2028" — but an approval process, a possible second trial and building a commercial operation cost more than is in the tank today. Growth paid for with fresh shares is never entirely free.

Valuation: a bet, not a value

At Taysha the usual tools fail, and that is itself a statement. There is no price-to-earnings ratio — the earnings are missing. There is no price-to-sales ratio — the revenue is missing. What remains is the soberest of all questions: what is the probability that TSHA-102 gets approved and sells, times the possible market, discounted to today — and does that fit the market value? No one can seriously present you this calculation to two decimal places; it hangs on an FDA decision that even experts can only assign probabilities to. For orientation, three numbers suffice: the accumulated deficit ($753.7 million) is in the order of magnitude of the market value, the cash ($276.6 million) covers a good two to three more years of losses, and the analysts who cover the stock at all (about ten) are on average optimistic — which, for a binary event, says little about the hit probability and much about the size of the prize if it works. More important than any metric is the insight: you are not valuing a company, you are valuing a coin toss with unequal sides. The price rally of plus 178.7 percent over twelve months (data as of July 13, 2026) is the anticipated hope for "heads" — nothing more.

Opportunities and risks at a glance

What speaks for Taysha:

- Solidly financed for a clinical biotech: $276.6 million in cash (March 31, 2026), runway per the company's own report "into 2028", and — unlike comparable warning-scanner hits — no going-concern qualification from the auditor.

- Strong medical designations: Breakthrough Therapy (September 2025), RMAT, Fast Track, Orphan Drug and rare-pediatric-disease status for TSHA-102 — accelerators the FDA grants only to serious candidates.

- Encouraging early data: 83 percent response rate (5 of 6 patients, high dose, data cut May 2025), no serious treatment-related adverse events among the first twelve patients (March 2026), an aligned design of the pivotal REVEAL trial with a possible six-month interim analysis.

- Enormous unmet need: for Rett syndrome there is no causal therapy — a one-time gene therapy would have, if approved, an extraordinary value and pricing potential.

- The momentum suggests the market takes the bet seriously: plus 178.7 percent over twelve months, price above the average lines, about 96 percent of the shares in institutional hands (data as of July 13, 2026).

What speaks against it:

- Not a cent of revenue since inception, a rising net loss ($89.3 → $109.0 million in 2024/2025; first quarter of 2026 already $42.4 million), accumulated deficit $753.7 million — in the order of magnitude of the entire market value.

- Cluster risk in its purest form: TSHA-102 is, per the company's own report, the "sole product candidate in clinical development" — the entire value hangs on one molecule and one FDA decision, without a second pillar as a safety net.

- Dilution as a permanent state: $274.6 million in fresh capital in 2025 alone, of which $264.0 million through new shares; about 287 million shares plus pre-funded warrants — and the need does not end with the cash lasting into 2028.

- Binary approval risk: a gene therapy with a small, single-arm pivotal trial (15 patients, each her own control) can at any time be judged insufficient by the FDA or require a further, expensive trial — as happened in the comparison case Replimune.

- The insolvency warning scanner flags Taysha for a real reason — Altman Z near zero, Piotroski 4 of 9, fundamental rating D (data as of July 13, 2026); the metrics are structurally strict for a revenue-less lab, but the loss burn is real.

A human conclusion

Back to the label reflex from the beginning. The red warning sign on Taysha's stock is not wrong — but it answers the wrong question. It screams "insolvency risk", and whoever reads only the sign sells in horror or scents a bargain in the "undervalued distressed stock". Both are mistaken, because both confuse the sign with the thing. The truth behind the label is more uncomfortable and more honest at once: Taysha stands more solid financially than the smoke detector suggests — and is nonetheless one of the riskiest bets you can take on the stock market. Not because the money runs out tomorrow (it does not), but because here everything hangs on a single yes or no. If the FDA says yes to TSHA-102, the value could multiply, and the children with Rett syndrome would get the first causal treatment in their history. If it says no, the only pillar falls, and the full cash box merely lengthens the road down. Both stand in the same report. Whoever gets in here should do so because they have understood this bet — not because a sign frightened them or a price jump lured them. Always read behind the label. What you then make of it is your decision. And that is exactly as it should be.

Sources

All original documents used in this analysis — to read for yourself:

- Taysha Gene Therapies, Inc. — SEC annual report 10-K for 2025 (filed March 19, 2026)

- Taysha Gene Therapies, Inc. — SEC annual report 10-K for 2024 (filed February 26, 2025)

- Taysha Gene Therapies, Inc. — SEC quarterly report 10-Q as of March 31, 2026 (filed May 6, 2026)

- Taysha Gene Therapies, Inc. — SEC quarterly report 10-Q as of September 30, 2025 (filed November 4, 2025)

- Taysha Gene Therapies, Inc. — SEC quarterly report 10-Q as of June 30, 2025 (filed August 12, 2025)

- Taysha Gene Therapies, Inc. — SEC quarterly report 10-Q as of March 31, 2025 (filed May 15, 2025)

- Taysha's complete SEC filing history: EDGAR overview (sec.gov)

- Fundamental data (metrics, valuation; data as of July 13, 2026), reconciled with the SEC filings.

- Screener and rating data: in-house stock scanner (data as of July 13, 2026).

Transparency & disclaimer: This analysis is a journalistic contextualization of publicly available information and is not investment advice, not a financial analysis in the regulatory sense, and not a solicitation to buy or sell securities. It expressly contains no judgment as to whether an insolvency occurs or whether TSHA-102 gets approved. Stock investments carry substantial risks up to total loss — especially at a clinical biotech with a single product candidate. All information without guarantee; the data cut-off is noted in the text in each case. The author holds no position in Taysha stock at the time of publication.

Our Bottom Line at a Glance

- Financial position & liquidity positive

- Surprisingly solid for a clinical biotech: $276.6 million in cash (March 31, 2026), runway per the report "into 2028", and in 2025 the cash balance even rose by $180.9 million. Unlike comparable warning-scanner hits, there is NO going-concern qualification from the auditor.

- Science & approval path neutral

- TSHA-102 carries strong FDA designations (Breakthrough Therapy, RMAT, Fast Track, Orphan Drug) and showed an early response rate of 83 percent (5 of 6 patients, high dose, May 2025 data cut). The design of the pivotal REVEAL trial is aligned with the FDA. But the trial is small and single-arm — the outcome remains open.

- Cluster risk (a single drug) negative

- TSHA-102 is, per the company's own report, the "sole product candidate in clinical development". The entire company value hangs on one molecule and a single FDA decision — without a second pillar as a safety net. A no, or the demand for a further trial (as in the Replimune case), would let the only load-bearing pillar give way.

- Dilution & financing negative

- Without revenue, Taysha finances itself almost entirely through new shares: $274.6 million fresh in 2025 alone (of which $264.0 million through shares), about 287 million shares plus pre-funded warrants. The capital need does not end with the cash lasting into 2028 — an approval process and building commercial operations are likely to cost further shares.

- Scanner finding & market neutral

- The warning scanner "Going Concern (Distress-Proxy)" flags Taysha for real (Altman Z near zero, Piotroski 4 of 9, rating D) — but the metric is structurally strict for a revenue-less lab. At the same time a strong price rally is under way (plus 178.7 percent over twelve months, data as of July 13, 2026) and about 96 percent of the shares are held by institutions: the market takes the bet seriously but has not decided it.

Taysha is the opposite of what the red warning sign suggests: more solid financially than the insolvency scanner implies ($276.6 million in cash, runway into 2028, no going-concern qualification) — and nonetheless one of the riskiest bets on the market. Because the entire value hangs on a single drug, TSHA-102 against Rett syndrome, and on a single FDA decision. No revenue, a growing loss, constant dilution — set against strong medical designations and encouraging early data. A binary event. Not investment advice.

What Our Rating Means

- If you don't own the stock

- In our view, the documented risks clearly outweigh — we see no basis for an entry.

- If you hold it in your portfolio

- In our view, the findings carry enough weight to warrant a critical look at your own position.

A journalistic assessment by our editorial team at the time of the deep dive, based on public sources — not investment advice and not a solicitation to buy or sell. Your personal circumstances (investment goals, risk capacity, taxes) cannot be taken into account. What our categories mean, how verdicts are formed, and what conflicts of interest exist →

Worth Noting

- Taysha reports on a calendar-year basis (fiscal year ends December 31). Program and trial updates appear partly mid-year via press release — when in doubt, reconcile against the filing periods.

- The financing chart sums the three 2025 capital sources per the 10-K (May 2025 placement $215.6 million, Trinity loan $50.0 million Tranche A, ATM sale $48.4 million); the reported net financing inflow for 2025 was $274.6 million.

- Price and scanner figures are dated July 13, 2026 (plus 178.7 percent over twelve months; about 287 million shares); analyses are evergreen, daily prices are not a buy argument.

Frequently Asked Questions

Taysha (NASDAQ: TSHA) of Dallas, Texas, is a clinical gene-therapy company. From a disarmed virus (AAV9) it develops "living medicines" that deliver missing genes directly into the nervous system. Its lead drug is TSHA-102 against Rett syndrome, a severe neurological disorder that strikes almost only girls. Nothing is sold yet — the company researches and tests.

Because the scanner is a quantitative approximation: it reacts to missing revenue, negative operating cash flow and an Altman Z-Score near zero. This metric punishes revenue-less firms almost automatically. The auditor, however, issued NO going-concern qualification, and as of March 31, 2026 there was $276.6 million in the cash box — a runway, per the report, into 2028.

As of March 31, 2026, Taysha had $276.6 million in cash and cash equivalents (after $319.8 million at the end of 2025). The company states in its report that this money will cover expenses "into 2028". At an operating cash outflow of about $93 million in 2025 that is plausible — but an approval process and building commercial operations are likely to require further capital.

TSHA-102 is Taysha's only drug candidate in clinical development — a gene therapy against Rett syndrome. An AAV9 viral vector delivers a functional copy of the missing MECP2 gene directly into the cerebrospinal fluid. In the early REVEAL trial the response rate was 83 percent (5 of 6 patients, high dose, data cut May 2025). TSHA-102 carries the FDA designations Breakthrough Therapy, RMAT and Fast Track.

Because its entire value hangs on a single medicine and a single agency. TSHA-102 is, per the report, the "sole product candidate in clinical development". If the FDA says yes, the value can multiply; if it says no or demands a further trial, the only pillar gives way. There is no second drug as a safety net — a binary event.

Yes. Since there is no revenue, Taysha finances itself almost entirely through new shares. In 2025 alone the company raised $274.6 million — $215.6 million through a placement in May, $48.4 million through ongoing at-the-market share sales (ATM) and $50.0 million through a loan. The share count stands at about 287 million, plus pre-funded warrants. Dilution is a permanent state.

This analysis expressly issues no insolvency verdict. The facts: there is no going-concern qualification from the auditor, the cash lasts per the report into 2028, and in 2025 the cash balance even rose by $180.9 million. The real risk is not solvency through 2028, but the binary bet on the FDA approval of TSHA-102 and the ongoing dilution.

Found an error?

Did you spot a factual error, an outdated number, or a typo in this deep dive? Let us know briefly — your report goes straight to the editorial team.