Bitdeer Stock: 3 Gigawatts, 2,033 Mined Bitcoin — and a Year That Cost $1.7 Billion in Cash

Bitdeer is building everything at once: its own mining chips, data centers on three continents, an AI cloud running NVIDIA hardware and a power portfolio of 3.0 gigawatts. The market pays about $4 billion for it — and at the same time our warning scanner reports: cash running out. We read the annual report for foreign private issuers (20-F) for 2025 and the latest interim reports (6-K): an operating cash outflow of $1,738.7 million in a single year, a profit that stems solely from revaluing the company's own convertible notes, and a founder who is at once lender, bitcoin lender and custodian of the corporate till. Not investment advice — just the look behind the steel door before the next crane rolls in.

Construction sites are soothing. Where cranes stand, chips roll off the line and a new megawatt figure gets announced every week, our brain thinks: value is being created here. Psychologists call this the activity bias — we mistake visible busyness for progress, because standing still feels like risk and motion feels like safety. Hardly any stock feeds this reflex as reliably in 2026 as Bitdeer (NASDAQ: BTDR): mining chips of its own design, the most efficient in company history; data centers on three continents; a power portfolio of 3.0 gigawatts — as much as two large nuclear reactor blocks; on top of that, the conversion of entire sites for artificial intelligence. The market rewards the construction site with about $4 billion of market value (data as of July 8, 2026). And at the same time our warning scanner "Insolvency Radar", sober and unimpressed, reports: cash running out. Both belong to the same company. So let's make a deal: we let the cranes stand still for a moment and read together what Bitdeer itself reported to the U.S. securities regulator, the SEC — in the annual report for foreign private issuers (20-F) for 2025 and in the interim reports (6-K) through the end of June 2026. An SEC filing is honest under penalty of law. In the end, you decide for yourself.

What Bitdeer actually does

Bitdeer is a child of the bitcoin industry in the literal sense: in 2021 the Chinese entrepreneur Jihan Wu — co-founder of Bitmain, the world's largest maker of bitcoin mining machines — spun off the mining division and turned it into Bitdeer, headquartered in Singapore; in April 2023 the stock came to the Nasdaq via a SPAC merger with Blue Safari. Today the business rests on three pillars. First: mining for its own account. Bitcoin mining is a global computing race — whoever manages more hashing attempts per second wins the block reward more often. Bitdeer runs its own data centers for this, most recently with 231,000 of its own mining machines and a hashrate of about 70 EH/s (May 2026) — the "E" stands for quintillions of hashing attempts per second. Second: selling shovels and renting out hotel rooms. Since acquiring the chip designer FreeChain (2024), Bitdeer develops its own special-purpose chips — ASICs, processors that master only a single task, but do it faster than anything else — and builds them into the SEALMINER series, which is also sold to third parties; in 2025 that was already the second-largest revenue source at 17.5 percent of revenue. Add hosting: outsiders park their mining machines in Bitdeer's halls, like in a parking garage with a flat rate for power. Third, the market story: artificial intelligence. Through its AI cloud, Bitdeer rents out computing time on NVIDIA supercomputers (DGX SuperPOD H100, H200, B200, GB200 NVL72) to companies training their own AI models, and is converting sites like Tydal in Norway into AI data centers meant to go to deep-pocketed anchor tenants — "colocation": Bitdeer supplies the hall, power and cooling, the tenant brings the servers.

The real treasure behind all three pillars is the same: power. 1,744 megawatts are already connected — from Rockdale in Texas (563 megawatts) via Ohio, Tennessee and Washington to Molde and Tydal in Norway, plus 600 megawatts of hydropower in the Kingdom of Bhutan and 50 megawatts in Ethiopia. Another 1,259.5 megawatts sit in the pipeline — together 3,003.5 megawatts (interim report 6-K of May 14, 2026). Note, right here, the central tension of this analysis: Up front, everything is growing — revenue, hashrate, megawatts. Out back, the capital market pays the bill, because the till itself lost more in 2025 than ever before. It runs through every chapter. How differently bitcoin miners tell the AI story is shown by our analyses of Riot Platforms (AI label, mining ingredient list) and Bit Digital (an ether hoard plus an AI cloud) — Bitdeer is the only one of them with chip development of its own.

Where the stock shows up in our scanner

Every day we run about 3,500 stocks through our scanners. With Bitdeer, a look at the mechanics pays off first, because the stock demonstrates how warning lists really work: BTDR landed on our research list as a hit of the warning scanner "Insolvency Radar: cash running out". As of the July 8, 2026 data cut-off the stock had just rotated out — on July 14, 2026 it was back in. Such lists are snapshots, and Bitdeer swings back and forth at the threshold: the radar calculates concretely whether the operating business has burned cash over four quarters and whether, at an unchanged burn rate, the till lasts less than four more quarters. Both are the case at Bitdeer — the quarters from mid-2025 to early 2026 add up to roughly $1.8 billion of operating outflow, a good $450 million per quarter, against $297.7 million of cash as of March 31, 2026. Arithmetically the steel door would be empty in less than a quarter if fresh money were not arriving continuously. Honesty requires the context: a substantial part of this outflow is inventory build-up and prepayments for SEALMINER mass production — more an investment in the product than a pure loss — and $245.0 million sat in bitcoin holdings and receivables alongside the cash. The Altman Z-Score, the classic early insolvency warning built from balance-sheet ratios, also stands at about 4.7 — outside the danger zone. The radar measures no scores, it measures the till — and at Bitdeer the till lives on replenishment. How to read such warning lists is explained in our article "Insolvency Radar: the Top 10".

The remaining hits paint the picture of a gambler's ticket with ambitions of substance: as of the July 8, 2026 data cut-off, BTDR fired in 7 scanners — among them "High ADR" with an average daily swing around 10.4 percent, "Above the 50- & 200-day lines", "Pros 80%" (institutional investors hold about 71 percent), Mike Webster's "Recession Proof" and "Swing Trading List" as well as Richard Moglen's "Top Performers 3/6 Month" with plus 89.5 percent in three months. The relative-strength rating stood at 89 — the stock ran better than 89 percent of all others — while it also traded about 41 percent below its 52-week high and lost almost 14 percent in the month before the cut-off. The Piotroski F-Score, a nine-point test of balance-sheet quality, stands at 3 of 9 — a thoroughly healthy company stands at 8 or 9. Translated: strong momentum, thin balance-sheet quality, brutal swings. Exactly the fingerprint of a stock whose story grows faster than its foundation.

The numbers over the years — honestly appraised

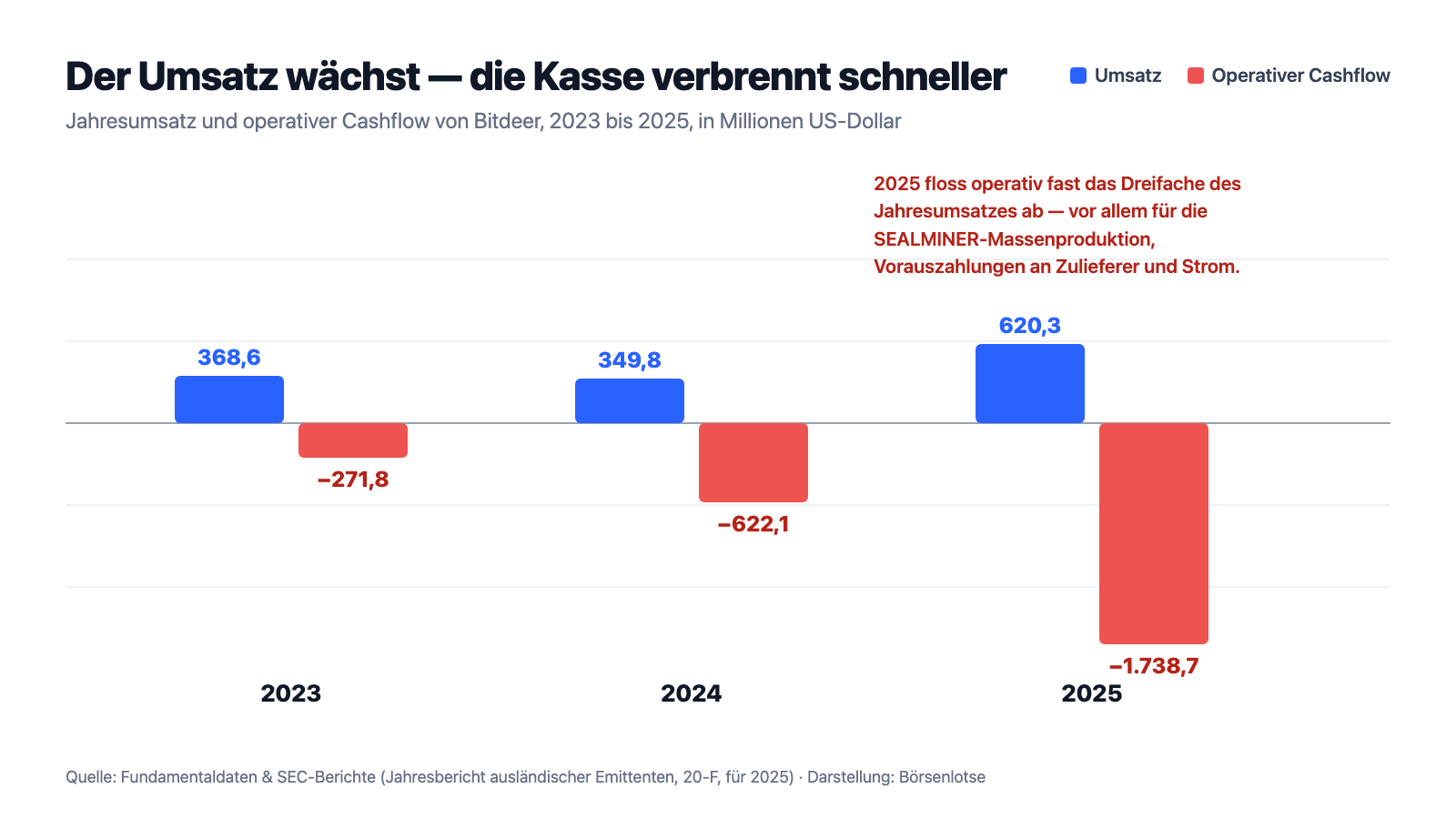

First, what genuinely impresses — and it is more than construction-site optics. Revenue jumped 77 percent in 2025 to $620.3 million (2024: $349.8 million; 2023: $368.6 million) and, in the first quarter of 2026, another 169 percent to $188.9 million versus the prior-year quarter. The engine behind it is genuine engineering: average self-mining hashrate increased sixfold within a year from 9.7 to 63.2 EH/s (Q1 2026), reaching 70.2 EH/s by May 2026 — bitcoin production rose 370 percent in May, to 921 coins. This is made possible by the SEALMINER from in-house development: the A4 generation, launched in the first quarter of 2026, pushes power hunger down to 16.4 joules per terahash — almost half the 29.0 of the year before; whoever pays only half as much for power per computing step also survives lean bitcoin prices longer. Adjusted EBITDA — operating profit before interest, taxes, depreciation and various valuation effects — swung to plus $14.4 million in the first quarter of 2026 (prior year: minus $45.6 million). And the AI cloud reported, in June 2026, about $69 million of annualized revenue at 90 percent GPU utilization. That is one half of the truth. The other stands in the cash ledger:

For the bill has grown, too: cost of revenue in the first quarter of 2026, at $228.0 million, sat above revenue — the gross margin came to minus 20.7 percent, mainly because of power and the depreciation on the freshly installed machine fleet. The bottom line was a quarterly loss of $159.5 million. And the foundation of this bill sways with the bitcoin price: the annual report itself records the slide from about $126,000 in October 2025 to about $67,000 as of March 31, 2026. A miner sells a product whose price can halve within months, while power and depreciation costs stay. Remember this sentence: at a miner, revenue is a bet, costs are a contract. Which brings us to the uncomfortable truths.

What the filings say — the uncomfortable truths

Uncomfortable truth no. 1: $1.7 billion of operating outflow in one year — the till lives on the capital market

The central number of this analysis sits in the risk chapter of the annual report, soberly and without a drumroll:

"We had negative cash flows from operating activities in the amount of US$271.8 million, US$622.1 million and US$1,738.7 million for the years ended December 31, 2023, 2024 and 2025, respectively. [...] There is no assurance that we will be able to sustain profitability, generate positive cash flow from operating activities or maintain our current level of financial performance in future periods."

— Bitdeer Technologies Group, SEC annual report 20-F for 2025, Item 3D "Risk Factors"

Operating cash flow is what actually left the account by year-end, before a single crane was ordered — and this account lost $1,738.7 million in 2025, almost three times annual revenue. The largest items: $786.9 million of inventory build-up (wafers, chips, finished SEALMINERs) and $408.2 million of prepayments to suppliers — Bitdeer pays for its chip production months in advance. That is strategically explainable, but it changes nothing about the mechanics: as of March 31, 2026, $297.7 million sat in the till (including restricted funds), plus $245.0 million in bitcoin holdings and receivables — against a most recent operating outflow of $346.9 million per quarter. That the door nevertheless does not slam shut is thanks to the capital market: $844.3 million flowed in from financing in 2024, in 2025 as much as $1,369.0 million, and another $352.6 million net in the first quarter of 2026 — among other things from a convertible-note package of $568.3 million in February 2026. In total, Bitdeer has issued $1.55 billion of convertible notes since November 2024 (coupons between 4.0 and 5.25 percent, due 2029 through 2032). A convertible note is a loan with a built-in right to swap into shares — in the end it is paid either with money the company still has to earn, or with your slice of the pie. Gross debt stood at about $1.9 billion as of March 31, 2026, the quarter's net interest expense at $29.5 million — compared with $5.3 million a year earlier.

Uncomfortable truth no. 2: the 2025 "profit" came from revaluing the company's own IOUs

Whoever looks at Bitdeer's data sheet in 2026 sees net income of $65.6 million for 2025 — after a $599.2 million loss the year before. Sounds like a turnaround. It is bookkeeping: in 2025 Bitdeer booked $444.9 million of income from the revaluation of derivatives — at the core, the conversion rights of its own convertible notes and the Tether warrants. The logic is as legal as it is counterintuitive: when the value of these conversion rights falls (say, because the share price falls or notes are redeemed), an income arises in the profit-and-loss statement — nobody earned any money on it. Bitdeer itself strips these effects out of its adjusted metrics, and then 2025 looks like this:

"We earned adjusted profit of US$15.2 million for the year ended December 31, 2023, and incurred adjusted losses of US$51.3 million and US$229.9 million for the years ended December 31, 2024 and 2025, respectively [...]."

— Bitdeer Technologies Group, SEC annual report 20-F for 2025, Item 5 "Operating and Financial Review"

On an adjusted basis, then, Bitdeer has never lost more than in 2025 — in the middle of its biggest growth year. The gap is also paid for with fresh shares: the weighted share count rose within one year from 190.2 to 233.4 million — plus 23 percent; your slice of the pie gets smaller while new slices are constantly being cut. And over the share count still hang the conversion rights from $1.55 billion of convertible notes plus ongoing share sales through the exchange (ATM program). The screener, by the way, shows no price-to-earnings ratio at all for BTDR — there simply is no sustainable profit to compute it on. One more detail for connoisseurs: since January 1, 2026, Bitdeer no longer reports under international IFRS rules but under U.S. GAAP — prior-year figures were restated accordingly. A change of rulebook in mid-conversion does not make time-series comparisons wrong, just more laborious.

Uncomfortable truth no. 3: the founder sits on both sides of the table — 69.5 percent of the votes, and the company's bitcoin sit at his other firm

Whoever buys the Bitdeer share becomes a junior partner of Jihan Wu — to a degree you should know about. Through the BVI vehicle Victory Courage (held in a family trust), Wu controls 44.4 million Class V super-voting shares with ten votes apiece: together 69.5 percent of the voting rights on roughly a fifth of the shares (as of April 21, 2026). The second-largest block belongs to the orbit of the stablecoin group Tether: its entities — attributed to Tether co-founder Giancarlo Devasini — hold 19.3 percent of the Class A shares, but thanks to the super-voting shares only 6 percent of the votes. Even the mightiest outside shareholder is a bystander here. The construction becomes truly remarkable at the question of where Bitdeer's crypto assets actually sit:

"BIT Group and its subsidiaries are entities over which Bitdeer’s controlling person has significant influence, as Mr. Jihan Wu, Bitdeer’s founder and Chairman of the board of directors, is the co-founder and chairman of the board of directors of BIT Group. During the years ended December 31, 2023, 2024 and 2025, substantially all of Bitdeer’s cryptocurrencies were held in custody by BIT Group and Bitdeer’s purchase and disposal of cryptocurrencies, at spot price on the date of transaction, was primarily from and to BIT Group."

— Bitdeer Technologies Group, SEC annual report 20-F for 2025, Item 7B "Related Party Transactions"

BIT Group — known until March 2026 as Matrixport, Wu's crypto-finance group — is for Bitdeer custodian, trading partner, lender and bitcoin lender in one: a secured credit line of up to $400 million at 8.35 percent interest, another of $200 million, plus, since February 2026, a bitcoin borrowing raised within weeks from 800 to 6,000 bitcoin. As of March 31, 2026, roughly $713 million of the debt came from this related party. That also explains a curiosity from the quarterly report: Bitdeer mined 2,033 bitcoin in the first quarter of 2026 but "held" only 31 at the reporting date — the rest was sold, lent out or pledged as loan collateral; the balance sheet correspondingly carries $209.9 million as bitcoin receivables. The annual report calls the bundle by its name: a concentrated counterparty risk. None of this is forbidden, all of it is disclosed. But if your neighbor told you his company was doing great — and you then learned that the cash, the loans and the emergency fund all sit with the same neighbor's second company: would you swallow for a moment?

Uncomfortable truth no. 4: the AI story stands for $4 billion of valuation — and for 2 percent of revenue

That leaves the story that turns a bitcoin miner into an "AI infrastructure platform". It has real building blocks: NVIDIA clusters up to the latest GB300 generation, about $69 million of annualized AI-cloud revenue at 90 percent utilization (June 2026), the planned conversion of Rockdale, Knoxville and Wenatchee — and in Tydal, by the company's account, Norway's largest AI data center is taking shape, for which a colocation lease was signed on June 29, 2026. Except: this lease is not yet effective — per the announcement it stands under conditions precedent outside Bitdeer's control, with no assurance that they will occur. And in the numbers, AI is so far a footnote:

"Our AI infrastructure and AI cloud business, generating revenue of US$6.8 million for the year ended December 31, 2025, remains at an early stage, and there is no assurance that we will be able to scale it to a level that meaningfully contributes to our overall profitability."

— Bitdeer Technologies Group, SEC annual report 20-F for 2025, Item 3D "Risk Factors"

As long as AI revenue stays small, Bitdeer remains at its core a bitcoin miner — with everything that entails. The protocol itself cuts the industry's pay every four years: at the next halving, expected in 2028, the block reward halves again from 3.125 to 1.5625 bitcoin — same work, half the wage; whoever then lacks the most efficient machines and the cheapest power mines below cost. Exactly this makes the pivot toward AI strategically consistent — it just is not yet earned, only paid for. And every megawatt that migrates to AI is missing from mining: the annual report itself warns that the reallocation could shrink Bitdeer's share of mining rewards. The market values the company at about $4 billion — roughly 5.5 times revenue and 5.7 times book value (data as of July 8, 2026). For comparison: that is the valuation class of successful software companies, paid for a business with a negative gross margin in the most recent quarter. The professionals see it rosy nonetheless — twelve analysts cover the stock, the consensus stands at "buy" — but their optimism applies to the construction site of 2027, not to the bill of 2025.

Valuation: $4 billion for the finished construction site of the day after tomorrow

Let's sum up the price question: about $4.0 billion of market value (data as of July 8, 2026) stands against $620.3 million of 2025 revenue — a price-to-sales ratio around 5.5 — with a negative gross margin in the most recent quarter, an adjusted annual loss of $229.9 million and no meaningful price-to-earnings ratio. Against that stand real assets: $1.2 billion of property and equipment, $613 million of inventory (mostly SEALMINERs and chips), $245 million of crypto assets, a 3-gigawatt power portfolio whose replacement would take years — and $1.9 billion of debt that wants to be served first. What you really acquire when you buy is a bet on the conversion: that megawatts become colocation leases (Tydal would be the proof, once the lease becomes effective), that SEALMINER efficiency survives the 2028 halving, and that the capital market keeps refilling patiently until then. The volatility prices that honestly: around 10 percent daily swing, plus 89.5 percent in three months, minus 14 percent in the month before, about 41 percent below the 52-week high (all values: data as of July 8, 2026). This is not an investor's certificate, this is a construction schedule with a ticker.

Opportunities and risks at a glance

What speaks for Bitdeer:

- Vertical integration that is rare in the industry: its own ASIC development (SEALMINER A4 at 16.4 J/TH — nearly halved power consumption per computing step within a year), its own data centers, its own power portfolio of 3,003.5 megawatts on three continents (6-K of May 14, 2026).

- Documented growth: revenue up 77 percent in 2025 to $620.3 million, Q1 2026 up 169 percent; self-mining hashrate increased sixfold to 63.2 EH/s on a quarterly average, bitcoin production up 370 percent (May 2026); adjusted EBITDA back to positive in Q1 2026 at plus $14.4 million.

- The AI option is real, not merely claimed: about $69 million of annualized AI-cloud revenue at 90 percent GPU utilization, NVIDIA clusters up to GB300 NVL72, a signed (not yet effective) colocation lease for Tydal — Norway's future largest AI data center by the company's account.

- Power as a scarce good: 570 megawatts at Clarington and 300 megawatts at Niles under contract in Ohio alone — in a market where AI giants compete for every megawatt, a 3-gigawatt portfolio is a genuine bargaining chip.

- Institutional confidence: about 71 percent of the shares with professionals, twelve analysts with a positive consensus, relative-strength rating 89 (data as of July 8, 2026).

What speaks against it:

- Cash consumption without precedent: operating outflow of $1,738.7 million in 2025 (after $622.1 and $271.8 million in the prior years), minus $346.9 million in Q1 2026 alone — against $297.7 million of cash as of March 31, 2026; the Insolvency Radar fires on exactly this.

- Earnings quality: the 2025 net income ($65.6 million) rests on $444.9 million of book gains from revaluing derivatives; adjusted, a record loss of $229.9 million, Q1 2026 gross margin minus 20.7 percent.

- Dilution and debt: $1.55 billion of convertible notes since November 2024, weighted share count up 23 percent in one year, gross debt around $1.9 billion, interest expense up sixfold.

- Governance cluster: founder Jihan Wu holds 69.5 percent of the votes through ten-vote super shares; "substantially all" crypto holdings, plus loans over two facilities and a 6,000-bitcoin borrowing, run through the founder-affiliated BIT Group — described by the annual report itself as a concentrated counterparty risk; Tether entities hold 19.3 percent of the Class A shares with only 6 percent of the voting weight.

- Bitcoin dependence remains: about 78 percent of Q1 2026 revenue from self-mining, the bitcoin price down per the annual report from $126,000 (October 2025) to $67,000 (March 31, 2026), the 2028 halving cuts the block reward in half again; the AI cloud delivered just $6.8 million of revenue in 2025 (about 1 percent), and the Tydal lease is not yet effective.

A human conclusion

Back to the activity bias from the beginning. It does not lie completely: at Bitdeer, real building is going on, and what is taking shape is no paper promise — the chips get more efficient, the hashrate increases sixfold, the megawatts are under contract, the NVIDIA clusters run at 90 percent utilization. Whoever bought the stock in the spring got 89 percent in three months for their faith in the construction site — and in the weeks after, experienced what 10 percent daily swings feel like. But this is exactly where the case helps you catch your own reflex: busyness is not proof. A construction site is a cost block until the first tenant pays. The numbers that count are not written on the cranes but in the cash ledger: $1,738.7 million of operating outflow in one year, adjusted the largest loss in company history, a till that would be empty within a quarter without convertible notes, share sales and loans from the founder's empire — and an AI story that so far carries 2 percent of revenue. None of this has to end badly: if the Tydal lease becomes effective and colocation delivers plannable rents, the narrative turns — then boring rental income finances the rest of the construction site, and the radar falls silent on its own. Until then, the craftsman's order of operations applies: first the lease, then the topping-out wreath. Check the cash ledger before you believe the cranes. What you make of it is your decision. And that is exactly as it should be.

Sources

All original documents used in this analysis — to read for yourself. Note: Bitdeer is registered as a "foreign private issuer" and therefore files the annual report for foreign private issuers (20-F) and interim reports (6-K) instead of the U.S. forms 10-K/10-Q:

- Bitdeer Technologies Group — SEC annual report 20-F for 2025 (filed April 30, 2026)

- Bitdeer Technologies Group — SEC annual report 20-F for 2024 (filed April 21, 2025)

- Bitdeer Technologies Group — SEC interim report 6-K of May 14, 2026: first-quarter 2026 results (Exhibit 99.1)

- Bitdeer Technologies Group — SEC interim report 6-K of June 18, 2026: May 2026 production and operations update (Exhibit 99.1)

- Bitdeer Technologies Group — SEC interim report 6-K of June 29, 2026: colocation lease for Tydal, Norway (Exhibit 99.1)

- Bitdeer's complete SEC filing history: EDGAR overview (sec.gov)

- Fundamental data (metrics, quarterly series, valuation; data as of July 8, 2026), reconciled with the SEC filings.

- Screener and rating data: in-house stock scanner (metrics as of July 8, 2026; Insolvency Radar membership verified on July 14, 2026).

Transparency & disclaimer: This analysis is a journalistic contextualization of publicly available information and is not investment advice, not a financial analysis in the regulatory sense, and not a solicitation to buy or sell securities. It expressly contains no judgment on whether an insolvency will occur. Stock and crypto investments carry substantial risks up to total loss. All information without guarantee; the data cut-off is noted in the text in each case. The author holds no position in Bitdeer stock at the time of publication.

Our Bottom Line at a Glance

- Business model & vertical integration positive

- The only large miner with its own ASIC development (SEALMINER A4: 16.4 J/TH, nearly halved power consumption within a year), its own data centers and a 3,003.5-megawatt power portfolio on three continents; rig sales were already the second-largest revenue source in 2025 (annual report 20-F for 2025, 6-K of May 14, 2026).

- Growth & operational execution positive

- Revenue up 77 percent in 2025 to $620.3 million, up 169 percent in Q1 2026; self-mining hashrate increased sixfold, bitcoin production up 370 percent (May 2026), adjusted EBITDA back to positive in Q1 2026 (+$14.4 million).

- Cash & financing negative

- Operating cash outflow of $1,738.7 million in 2025 and $346.9 million in Q1 2026 against $297.7 million of cash (March 31, 2026); the gap is closed by $1.55 billion of convertible notes, ATM share sales and loans from the founder-affiliated BIT Group — the Insolvency Radar fires on exactly this.

- Earnings quality & dilution negative

- The 2025 net income ($65.6 million) stems from $444.9 million of derivative book gains; adjusted, a record loss of $229.9 million, Q1 2026 gross margin minus 20.7 percent, weighted share count up 23 percent in one year, interest burden up sixfold.

- Governance & entanglement negative

- Jihan Wu controls 69.5 percent of the votes through ten-vote super shares; "substantially all" crypto holdings, two credit facilities and a 6,000-bitcoin borrowing run through his BIT Group (formerly Matrixport) — per the annual report a concentrated counterparty risk; Tether entities hold 19.3 percent of the Class A shares with almost no voting weight.

- AI story & momentum neutral

- About $69 million of annualized AI-cloud revenue at 90 percent utilization and the (not yet effective) Tydal lease are real progress — but in 2025 AI contributed just $6.8 million of revenue (~1 percent); add an RS rating of 89, plus 89.5 percent in three months, around 10 percent daily swing and 41 percent distance to the 52-week high (data as of July 8, 2026).

Bitdeer is probably the most ambitious construction site in the mining industry: its own chips, 3 gigawatts of power, an AI cloud running NVIDIA hardware — and documented growth on every level. None of it is paid for yet: in 2025, $1,738.7 million flowed out of operations, the adjusted loss is the largest in company history, and the till lives on convertible notes, share sales and loans from the empire of a founder who controls 69.5 percent of the votes and is at the same time custodian of the company's bitcoin. The market is already paying about $4 billion for the finished platform — delivered so far is the construction site. Not investment advice.

What Our Rating Means

- If you don't own the stock

- In our view, the documented risks clearly outweigh — we see no basis for an entry.

- If you hold it in your portfolio

- In our view, the findings carry enough weight to warrant a critical look at your own position.

A journalistic assessment by our editorial team at the time of the deep dive, based on public sources — not investment advice and not a solicitation to buy or sell. Your personal circumstances (investment goals, risk capacity, taxes) cannot be taken into account. What our categories mean, how verdicts are formed, and what conflicts of interest exist →

Worth Noting

- BTDR landed on our research list as a hit of the warning scanner "Insolvency Radar: cash running out"; as of the July 8, 2026 data cut-off the membership had lapsed, on July 14, 2026 the stock stood in the radar again — Bitdeer swings back and forth at the threshold of the criterion. Scanner memberships are snapshots and shift daily.

- Bitdeer is registered as a foreign private issuer and files Forms 20-F (annual report) and 6-K (interim reports) instead of 10-K/10-Q; since January 1, 2026, the company reports under U.S. GAAP instead of IFRS, and prior-year figures were restated.

- Price and valuation figures are dated July 8, 2026 (market value about $4.0 billion); analyses are evergreen, daily prices are not a buy argument.

Frequently Asked Questions

Bitdeer (NASDAQ: BTDR) of Singapore mines bitcoin in its own data centers, develops and sells its own SEALMINER mining machines, rents out slots to third-party miners (hosting) and is building an AI cloud with NVIDIA supercomputers. The power portfolio spans 3,003.5 megawatts across the United States, Norway, Bhutan, Ethiopia and Malaysia; 2025 revenue: $620.3 million.

The radar calculates concretely: the operating business burned roughly $1.8 billion over the last four quarters, while cash stood at $297.7 million as of March 31, 2026 — at an unchanged burn rate that lasts less than four quarters. A hit is not an insolvency verdict: a large part of the outflow is inventory build-up for SEALMINER production, and Bitdeer keeps refilling through convertible notes and share sales.

Founder Jihan Wu (Bitmain co-founder) controls 69.5 percent of the voting rights through 44.4 million Class V shares with ten votes each (as of April 21, 2026). Entities of the stablecoin group Tether — attributed to co-founder Giancarlo Devasini — hold 19.3 percent of the Class A shares but only 6 percent of the votes. Institutional investors hold about 71 percent of the free float.

Only on paper: the net income of $65.6 million stems from $444.9 million of book gains from the revaluation of derivatives — at the core, the conversion rights of its own convertible notes and warrants. Adjusted, Bitdeer reports a record loss of $229.9 million for 2025; operating cash flow came to minus $1,738.7 million.

SEALMINER is Bitdeer's self-developed series of mining machines built on its own ASIC chips (special-purpose processors for exactly one computing task). The A4 generation (launched in the first quarter of 2026) needs 16.4 joules per terahash — almost half the power of the fleet a year earlier. Sales to third parties were already the second-largest revenue source in 2025 at 17.5 percent of revenue.

Small but growing: under $0.1 million in 2023, $3.5 million in 2024, $6.8 million in 2025 — about 1 percent of group revenue; in the first quarter of 2026 it was $3.7 of $188.9 million. In June 2026 Bitdeer reported about $69 million of annualized AI-cloud revenue at 90 percent utilization, plus a signed but not yet effective colocation lease for Tydal, Norway.

BIT Group (until March 2026: Matrixport) is the crypto-finance group whose co-founder and chairman is likewise Jihan Wu. Per the annual report, BIT Group holds "substantially all" of Bitdeer's crypto holdings in custody, handles their purchase and sale, and provides loans including a bitcoin borrowing raised to 6,000 bitcoin — as of March 31, 2026, roughly $713 million of the debt came from this related party. Bitdeer itself calls this a concentrated counterparty risk.

The bitcoin protocol halves the mining reward roughly every four years — in 2028 presumably from 3.125 to 1.5625 bitcoin per block. For miners that means: same work, half the wage. Bitdeer counters with more efficient chips of its own (16.4 J/TH) and cheap power, and is building up the less weather-dependent colocation and AI-cloud business in parallel.

Found an error?

Did you spot a factual error, an outdated number, or a typo in this deep dive? Let us know briefly — your report goes straight to the editorial team.