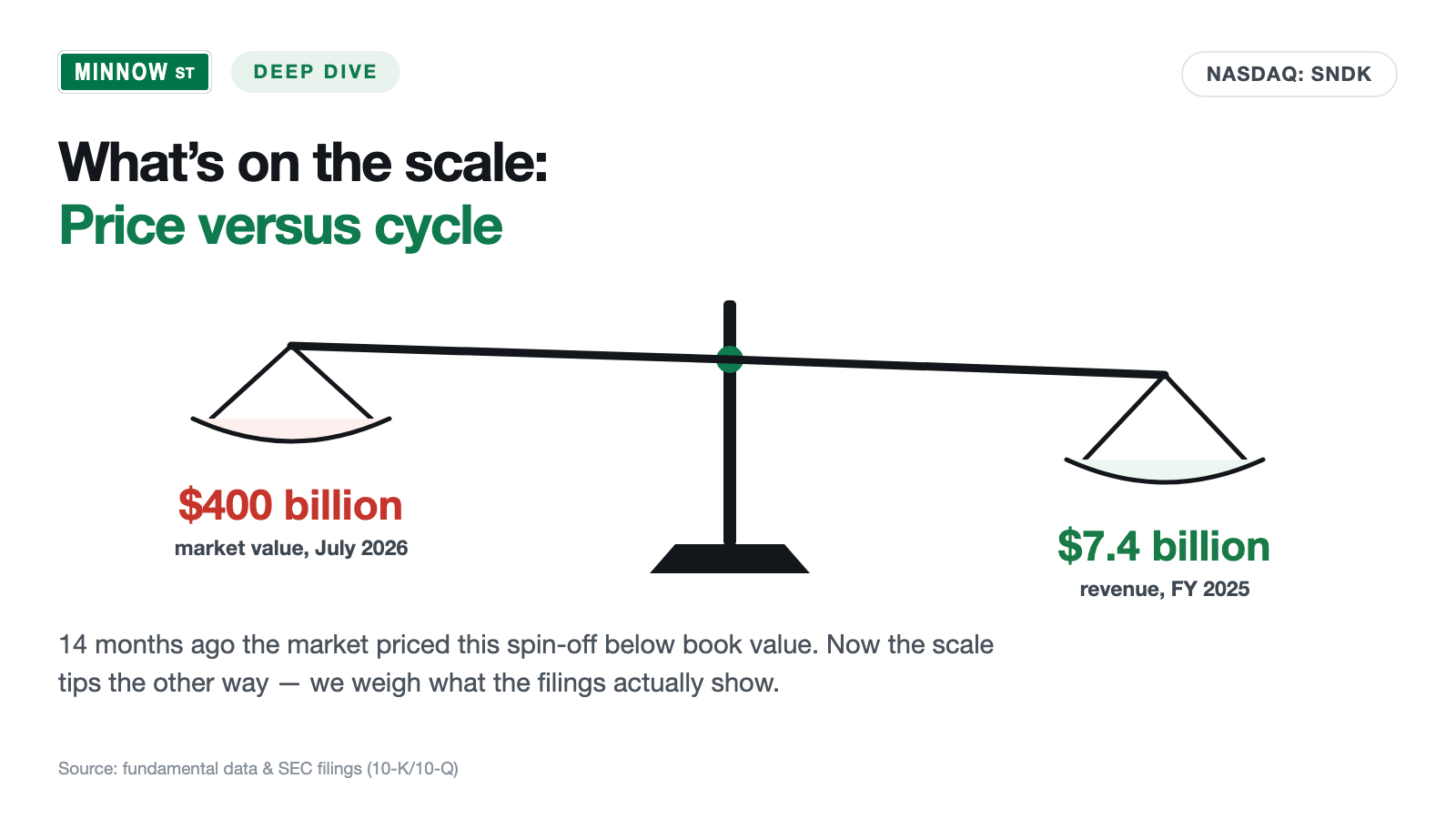

Sandisk Stock: The Spurned Spin-Off That Had to Write Off Its Own Goodwill — and Weighs $400 Billion 14 Months Later

When Western Digital spun its memory division Sandisk off to the stock exchange in February 2025, hardly anyone wanted it: the market pushed the company below its book value, Sandisk had to write off $1.8 billion of goodwill in the spin-off quarter, and the former parent quickly passed its stake along. 14 months later the same company sits at about $400 billion of market value and shows up in our value scanner built on Joel Greenblatt's Magic Formula. We read the annual report (10-K) and the quarterly reports (10-Q): a 251 percent revenue jump that comes almost entirely from the price per gigabyte, a $41.6 billion order backlog — and a joint-venture corset with Kioxia that works against Sandisk in a downturn. Not investment advice — just a cross-examination of the inner know-it-all who claims all of this was foreseeable.

In every investor lives a lodger who never pays rent and is always right: the inner know-it-all. He reliably speaks up when a chart like Sandisk's (Nasdaq: SNDK) scrolls across the screen — up 727 percent since the start of the year, roughly 58 times its 52-week low (data as of July 8, 2026) — and says his favorite sentence: "You could have seen that coming." Psychologists call this lodger hindsight bias: once the outcome is fixed, our memory rebuilds the past so that it marched straight toward it — every low retroactively becomes a signposted entry point. The treacherous part is the conclusion he draws: whoever believes yesterday was recognizable automatically trusts himself to recognize tomorrow, too — and buys. So let's make a deal: we cross-examine the know-it-all. As evidence we take the documents Sandisk files, honest under penalty of law, with the U.S. securities regulator, the SEC — the annual report (10-K, the yearly mandatory filing) and the quarterly reports (10-Q). The record is unambiguous: 14 months ago, nobody thought this stock was a bargain. Not the market, which pushed it below its book value. Not its own balance sheet, which for that reason had to write off $1.8 billion of goodwill. And not even the former parent Western Digital, which quickly passed its stake along. In the end, you decide for yourself what that means for today.

What Sandisk actually does

Sandisk makes NAND flash — the long-term memory of the digital world. NAND cells are the storage cells that remember even without power: they sit in the SSDs of data centers and laptops, in smartphones, memory cards and USB sticks. The company from Milpitas, California (about 11,000 employees in 33 countries, 73 percent of them in Asia-Pacific) sorts its business into three end markets: "Datacenter" (data centers, formerly called "Cloud"), "Edge" (devices such as PCs and smartphones, formerly "Client") and "Consumer" (cards, sticks, external drives — the SanDisk products from the electronics-store shelf). The memory wafers are not made in factories of its own but in Flash Ventures — a web of three joint companies with the Japanese partner Kioxia, in each of which Sandisk holds 49.9 percent, with seven fabs in Japan and an eighth ramping up. Remember this construct, we will come back to it — it is blessing and corset at once.

Two peculiarities you need to know before the numbers make sense. First, the origin: until February 21, 2025, Sandisk was a wholly owned subsidiary of Western Digital; then came the spin-off — WDC distributed 80.1 percent of the Sandisk shares to its own shareholders (one third of a Sandisk share per WDC share) and initially kept 19.9 percent. As a parting gesture Sandisk took on a $2 billion loan and wired $1.5 billion of it to its parent as a settlement payment — the child moved out with debts whose proceeds stayed at the parents' house. Second, the calendar: Sandisk reports in an offset fiscal year ending on the Friday closest to June 30. "Fiscal year 2026" means: June 28, 2025 through July 3, 2026; the third quarter of that fiscal year ended April 3, 2026. And with that, the central tension that runs through this analysis as its connecting thread: the same market has priced the same company, within 14 months, once below book value and once at 25 times book value — and what changed in that time is above all one single variable: the price per gigabyte.

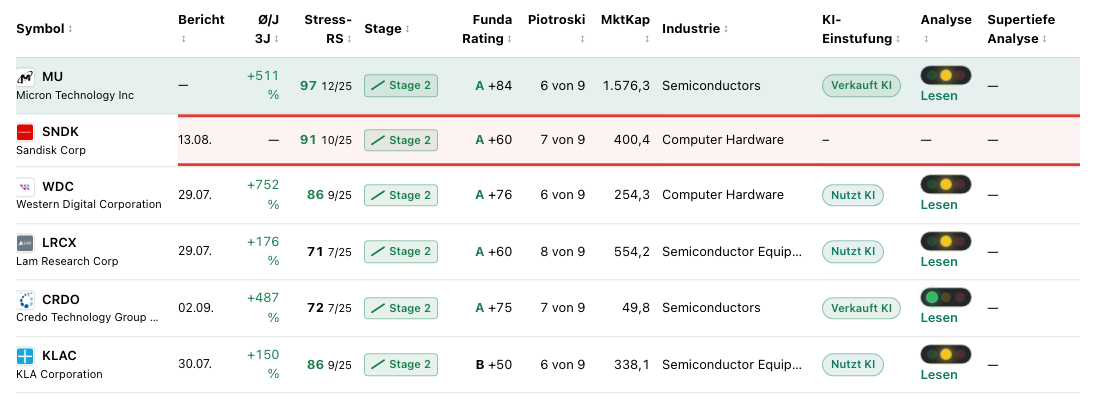

Where the stock shows up in our scanner

Every day we run about 3,500 stocks through our scanners. Sandisk shows up in the value scanner "Joel Greenblatt: Magic Formula" — right at the top, and the neighborhood is a family photo of the memory industry: as of the July 8, 2026 data cut-off Sandisk stood in second place, framed by Micron above and its own former parent Western Digital below; at the live check on July 14, 2026 it was third, behind both. As of the July 8 cut-off Sandisk additionally led our EBIT-margin ranking — the operating margin of the last four quarters sits around 70 percent. Greenblatt's formula, in plain words: buy good companies at a fair price, measured by exactly two numbers — return on capital (how much operating profit per dollar of working capital employed?) and earnings yield (how much operating profit per dollar of enterprise value?). A freshly exploded memory maker naturally shines in both disciplines.

We dissected it at length in the Micron analysis and repeat only the core here: with cyclicals, the Magic Formula preferentially fires at the earnings peak, because it treats the most recently reported profits as a permanent state. A memory maker at record prices always looks "cheap" in this arithmetic — until the cycle turns. The remaining metrics are strong in their own right: a Piotroski F-Score of 7 of 9 (a nine-point test of balance-sheet quality — 7 is good), an Altman Z-Score around 13 (a classic early warning of insolvency; danger begins below 1.8 — miles away here), fundamental rating A, relative strength 99: hardly any stock in the market has run better over the last twelve months. But that is exactly the point: this is not an overlooked value gem the scanner has dug up. This is one of the hottest stocks in the market, waved through by a value filter because of its record profits — the second time within a week, after Micron. The inner know-it-all and the formula make related mistakes: he considers the past to have been predictable, it considers the present to be permanent.

The numbers over the years — honestly appraised

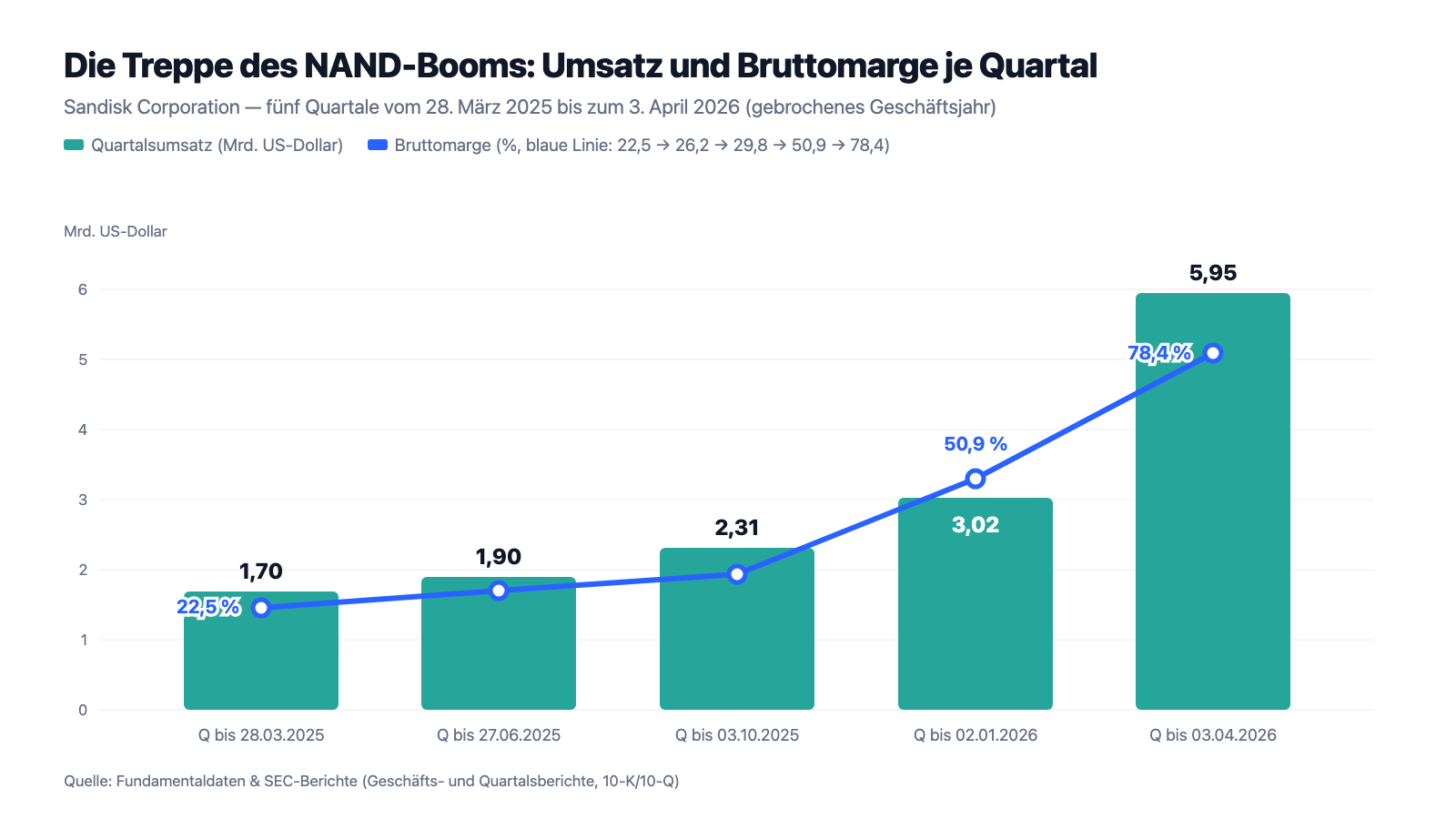

First, what genuinely impresses — and it is one of the steepest staircases we have ever seen in a quarterly report. Fiscal year 2026, quarter by quarter: $2.31 billion of revenue in the first quarter (through October 3, 2025), $3.03 billion in the second (through January 2, 2026), $5.95 billion in the third (through April 3, 2026) — up 97 percent within a single quarter, up 251 percent versus the prior-year quarter. Over the same span the gross margin climbed from 29.8 via 50.9 to 78.4 percent — a level this company had never before seen even from afar. After nine months the books show $11.3 billion of revenue (up 107 percent), $4.5 billion of net income and $4.5 billion of operating cash flow. And the balance sheet as of April 3, 2026 is unrecognizable within a year: the $2 billion farewell loan is fully repaid (on March 4, 2026, out of cash), zero financial debt stands against $3.7 billion of cash, equity grew from $9.2 to $13.8 billion, and at the end of April the board authorized a share buyback program of $6 billion. The driver is the AI wave: data centers are buying flash SSDs as if there were no tomorrow — datacenter revenue grew six-and-a-half-fold in the third quarter, to $1.47 billion.

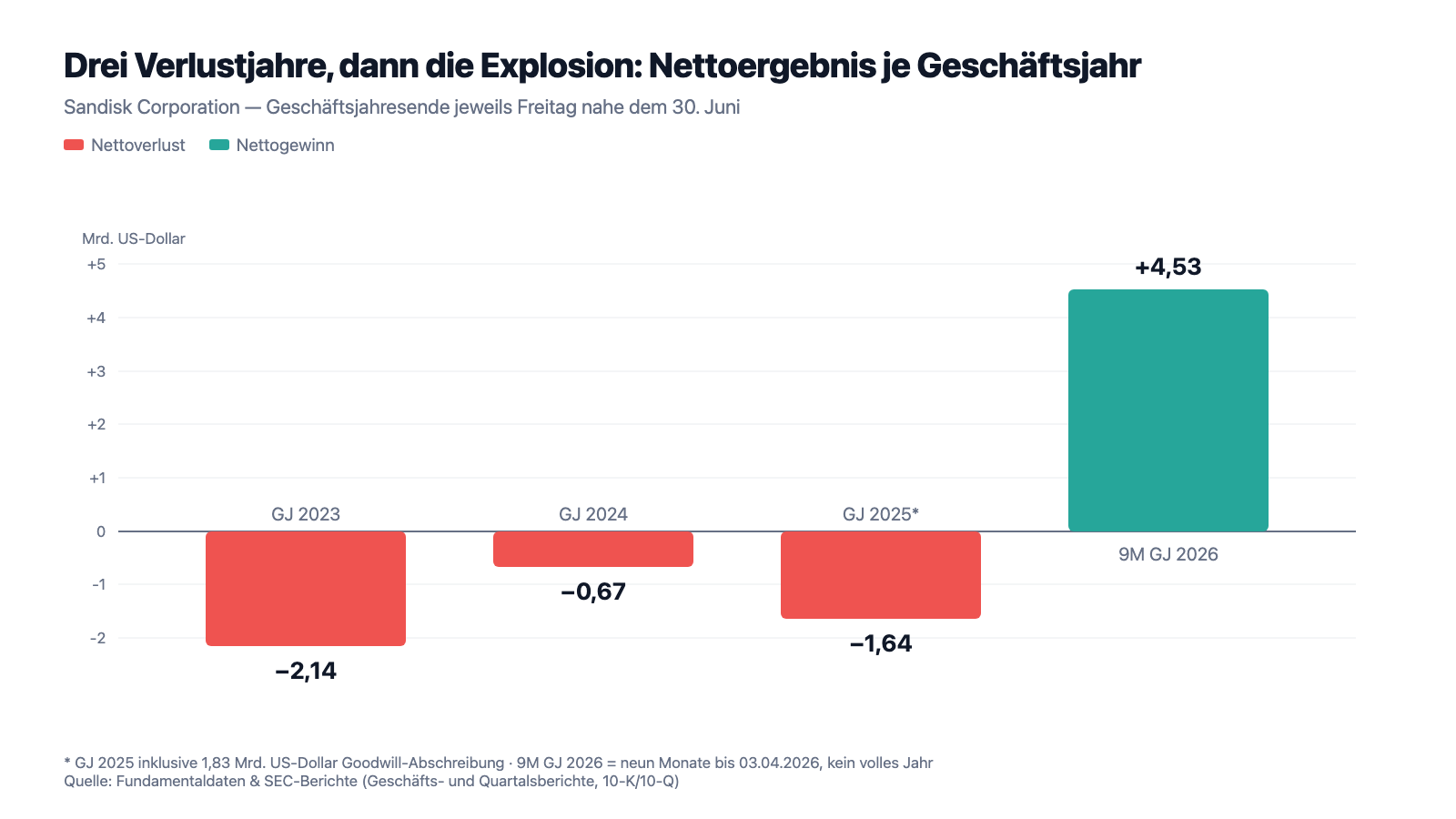

And now the same company, only a few years earlier — because a company's history does not begin at the 52-week low. Fiscal year 2023 (through June 30, 2023): $6.1 billion of revenue, a gross margin of 7.1 percent, a net loss of $2.1 billion — the memory market was stuck in the overcapacity crisis, and the then WDC division additionally wrote down inventories and paid underutilization charges for idle fabs. Fiscal year 2024: minus $672 million. Fiscal year 2025: revenue of $7.4 billion (up 10 percent — 6 points of it volume, 4 points price), a net loss of $1.6 billion, shaped by the goodwill write-off we will get to in a moment; even adjusted, only a wafer-thin operating profit remained. Three fiscal years, three losses, minus $4.5 billion combined — and then, in the fourth year, the explosion. Exactly this sequence is what the next picture shows, and it is the reason we read the filings especially carefully:

What the filings say — the uncomfortable truths

Uncomfortable truth no. 1: revenue up 251 percent — on practically unchanged volume

The quarterly report dissects the revenue jump itself, in the very first sentence of its revenue analysis — and you should have read this dissection before the inner know-it-all shouts "obvious case":

"Net revenue increased 251% in the three months ended April 3, 2026 from the comparable period in the prior year, primarily due to a 248% increase in average selling prices (“ASP”) per gigabyte. The exabytes sold remained flat from the comparable period in the prior year."

— Sandisk Corporation, SEC quarterly report 10-Q as of April 3, 2026, Item 2 MD&A "Net Revenue"

Look at the breakdown of the end markets and you see how one-sided this boom is: in the "Edge" business (PCs, smartphones — at $3.66 billion the quarter's largest revenue block) prices rose 343 percent while the volume sold fell 10 percent. In the consumer business prices rose 139 percent — on 40 percent less volume. Only the data-center business grew both ways, through price (up 186 percent) and volume (up 160 percent); but so far it accounts for only a quarter of revenue. A boom that sits almost entirely in the price hangs on the one variable a maker of commodity goods controls least — NAND from Sandisk does the same thing as NAND from Samsung, SK hynix, Kioxia or Micron. What it feels like when it tips over is described with remarkable candor in the risk section of the company's own annual report: the memory market has experienced "periods of excess capacity leading to liquidation of excess inventories, inventory write-downs, underutilization charges, significant reductions in average selling prices" — and can experience them again (10-K fiscal year 2025, Item 1A). This is not theory: as recently as fiscal year 2025 Sandisk paid $75 million in underutilization charges for idle capacity and wrote off $24 million of inventories — in the crisis year 2023, still under WDC's roof, it was 296 plus 108 million. A price that multiplies three-and-a-half-fold in twelve months is not a new law of nature. It is the other half of the same roller coaster.

Uncomfortable truth no. 2: the $41.6 billion backlog — at Sandisk, too, "this time it's different" now comes in contract form

Now the counter-thesis, and it is strong. In the third quarter of fiscal year 2026 Sandisk signed multi-year supply agreements with major customers — including prepayments that sit on the balance sheet as contract liabilities ($511 million as of April 3, 2026, after $25 million in June 2025). The real punch is in a footnote of the revenue note:

"As of April 3, 2026, the transaction price allocated to remaining performance obligations was $41.6 billion, of which $41.2 billion has not yet been billed and $0.4 billion has been recorded as contract liabilities. Approximately 15% of the remaining performance obligations from these contracts with customers are expected to be recognized as revenue over the next twelve months."

— Sandisk Corporation, SEC quarterly report 10-Q as of April 3, 2026, Note 4 "Revenue"

Be fair to both sides here as well. In favor: $41.6 billion is 5.7 times the complete 2025 annual revenue — a backlog that has never existed in this form in flash history. Customers who make prepayments and commit for years evidently fear the shortage more than the price; we know the pattern from Micron's 10-Q with its take-or-pay contracts. Against it speak three things. First, the duration: if only about 15 percent becomes revenue over the next twelve months, the rest spreads across many years — that is a tailwind, but no guarantee for today's margin, and the report is silent on the prices and adjustment clauses at which delivery will happen. Second, the timing: these contracts were signed at the most expensive price level in the industry's history — and the memory industry has a long tradition of long-term contracts from the cycle peak being renegotiated in the downturn. Third, the symmetry: a backlog also binds Sandisk itself — to delivery volumes for which the capacity has yet to be built, together with a partner who is about to become important. A mountain of signed contracts is better than none. But it is a promise about the future, given at the most euphoric moment in the industry's history.

Uncomfortable truth no. 3: the Kioxia corset — half the fixed costs are mandatory, even if Sandisk orders nothing

Sandisk owns no wafer fabs of its own. Practically the entire flash supply comes from the Flash Ventures joint companies with Kioxia in Japan — and the annual report describes very precisely what that means in a downturn:

"The terms of our agreements with Kioxia with respect to Flash Ventures require that substantially all of our flash-based memory be obtained from Flash Ventures [...] For example, we are contractually obligated to pay for 50% of the fixed costs of Flash Ventures regardless of whether we order any flash-based memory, and our orders placed with Flash Ventures on a rolling basis are binding."

— Sandisk Corporation, SEC annual report 10-K, fiscal year 2025, Item 1A "Risk Factors" (Flash Ventures)

Let's translate the construct into an everyday image: Sandisk has rented a commercial kitchen together with its competitor Kioxia — for decades, with termination clauses that feel more like a marriage. When the restaurant is running, the shared kitchen is a cost advantage. When the dining room stays empty, Sandisk still pays half the kitchen rent. That is the irony of this balance sheet: while Micron had take-or-pay contracts signed by its customers, Sandisk has always carried a built-in take-or-pay toward its own supplier — in a downturn, it pays first. On top come obligations that do not sit on the balance sheet: Sandisk guarantees half of Flash Ventures' factory lease agreements — about $993 million off balance sheet as of April 3, 2026 — and the report puts the maximum loss scenario from the whole construct (loans, equity stake, guarantees, prepayments) at just under $3 billion. And one more clause belongs here: per the risk chapter, the JV agreements could significantly impede a takeover of Sandisk — whoever speculates on a takeover premium is speculating against the fine print. None of this is a problem in the boom, on the contrary: the fabs run full, the shared costs lever the profit. But it means: Sandisk's cost structure is built for cycle peaks — flexible upward, rigid downward.

Uncomfortable truth no. 4: the balance sheet remembers — a goodwill write-off at the start, growing clusters in the boom

Finally, the truth that convicts the inner know-it-all of outright false testimony. When Sandisk came to the exchange in February 2025, buyers did not find the price attractive — there simply were too few buyers. The share fell so low that the market value slipped below book value, and that forced the freshly spun-off company into a remarkable step in that very quarter:

"Subsequent to the completion of the separation, we identified potential impairment indicators related to the trading price of our common stock and a resulting market capitalization that was below its December 27, 2024 net book value. In accordance with Accounting Standards Codification No. 350, Intangibles - Goodwill and Other, we performed a quantitative test, which indicated that the carrying value of our reporting unit exceeded its estimated fair value resulting in the recognition of a $1.8 billion impairment charge as of, and for the nine months ended, March 28, 2025."

— Sandisk Corporation, SEC annual report 10-K, fiscal year 2025, Item 1A "Risk Factors" (section "Future material impairments …")

Goodwill, translated: the premium over substance value that a buyer once paid and that has sat in the balance sheet as a line item of hope ever since — when the hope shrinks, it must be written off. Hold the two pictures side by side: in March 2025 the market said this company was worth less than its book value. In July 2026 the same market pays 25 times book value. At least one of the two valuations was grotesquely wrong — and nothing guarantees it was only the first. The former parent, by the way, read the situation no better: as early as June 2025 — before the price explosion — Western Digital swapped 14.6 percent of Sandisk away against its own debt; the costs of the placements, per the report, were paid by Sandisk. And today's balance sheet carries new, boom-typical clusters: of the $17.1 billion in total assets, $5.0 billion is still goodwill — just under 30 percent —, trade receivables more than doubled in nine months from $1.1 to $2.7 billion (booked, not yet paid revenue), the ten largest customers accounted for 46 percent of revenue in the third quarter (prior-year quarter: 41 percent), for the first time since the spin-off a single customer crossed the 10 percent mark, and 72 percent of quarterly revenue came from Asia. None of this is a scandal. But taken together it means: the higher the boom carries, the more concentrated customers, region and receivables become.

Valuation: $400 billion for the commodity of the digital economy

In early July 2026 the Sandisk stock cost about $2,335; at about 148 million shares that corresponds to a market value of about $400 billion (all valuation figures: data as of July 8, 2026). For perspective: that is more than the former parent Western Digital is worth — the daughter has overtaken the parents' house. Measured against the profits of the last four quarters, the price-to-earnings ratio comes out around 80; simply annualize the explosive third quarter and it shrinks well below 30, and the estimates of the twelve analysts (consensus on average "buy") push it further toward the low double digits for the coming fiscal year. You recognize the pattern from the Micron analysis: the further you extend the recent past, the cheaper the stock becomes. The inner know-it-all eagerly does the math along. The counter-check comes from the substance metrics: a price-to-sales ratio around 30, price-to-book around 25 — for a company whose product is commodity ware, whose gross margin sat at 22.5 percent four quarters ago and which wrote nothing but losses in the three fiscal years before. Calculated on fiscal year 2025 revenue, the P/S would sit above 50. What lies on the other side of the scale: zero financial debt, $3.7 billion of cash, $4.5 billion of nine-month operating cash flow, the $41.6 billion backlog and a $6 billion buyback program. That is considerably more substance than the spin-off mockers credited this company with in the spring of 2025. But the price presupposes that the 78 percent gross margin is not an outlier but a plateau — for a product whose price per gigabyte, per the company's own risk chapter, regularly races in the other direction too. How the market prices perfection and what remains of it when one detail wobbles is something we recently dissected at the chip inspector KLA.

Opportunities and risks at a glance

What speaks for Sandisk:

- A genuine scarcity tailwind: AI data centers are driving NAND demand; datacenter revenue grew six-and-a-half-fold (plus 645 percent) in the quarter through April 3, 2026 — through price and volume (10-Q as of April 3, 2026).

- A historic earnings explosion: $5.95 billion of quarterly revenue (plus 251 percent), a 78.4 percent gross margin, $3.6 billion of net income in the quarter; $4.5 billion of operating cash flow in nine months.

- A lightning-renovated balance sheet: the $2 billion spin-off loan was fully repaid on March 4, 2026 — zero financial debt, $3.7 billion of cash, $13.8 billion of equity, an Altman Z around 13, plus a $6 billion share buyback program (April 2026).

- A contractual backbone for the first time: $41.6 billion of remaining performance obligations from long-term contracts plus $511 million of customer prepayments — more than five times the 2025 annual revenue (10-Q as of April 3, 2026, Note 4).

- A strong scanner signature: top trio in the Greenblatt value scanner (second place on July 8, third at the live check on July 14, 2026), Piotroski 7 of 9, fundamental rating A, an EBIT margin of the last four quarters around 70 percent, relative strength 99; twelve analysts on average at "buy" (data as of July 8, 2026).

What speaks against it:

- An almost pure price boom: selling prices per gigabyte up 248 percent on flat volume (consumer: minus 40 percent volume) — and a risk chapter of its own that describes overcapacity phases with price crashes, inventory write-downs and underutilization charges as a recurring industry pattern (10-Q as of April 3, 2026; 10-K fiscal year 2025).

- A short, red history: fiscal years 2023 through 2025 brought a combined $4.5 billion of losses; as recently as fiscal year 2025, $75 million of underutilization charges accrued. As a standalone company Sandisk has not yet lived through a single complete downturn.

- The Kioxia corset: a purchase obligation for practically the entire flash supply, 50 percent of the fixed costs due even without orders, $993 million of off-balance-sheet lease guarantees, just under $3 billion in the maximum loss scenario — and JV clauses that make a takeover of Sandisk harder (10-K fiscal year 2025; 10-Q as of April 3, 2026).

- The valuation prices in a plateau: about $400 billion of market value, P/S around 30, P/B around 25, up 727 percent since the start of the year, roughly 58 times the 52-week low (data as of July 8, 2026) — small doubts about the margin thesis produce large price swings.

- Growing clusters: top-10 customers at 46 percent of quarterly revenue, for the first time a single customer above 10 percent, receivables more than doubled in nine months from $1.1 to $2.7 billion, 72 percent of revenue from Asia, $5 billion of goodwill on the balance sheet (10-Q as of April 3, 2026).

A human conclusion

Back to the inner know-it-all and his favorite sentence: "You could have seen that coming." The cross-examination is over, and the record speaks against him. Demonstrably, nobody recognized the spring 2025 low as an opportunity: the market valued the company below book value. The company itself drew the accounting consequence and wrote off $1.8 billion of goodwill. The former parent swapped its stake away against its own debt months before the explosion — professionals with the best inside view anyone can have into this business. If not even they saw yesterday coming, then the claim that tomorrow is now clearly recognizable is exactly that: a claim. Whether the 78 percent margin is a plateau or the top of the roller coaster, nobody knows today — not the Greenblatt scanner, which dutifully files record profits as value, not the twelve analysts, not we ourselves, and least of all the know-it-all; in two years he will simply tell you the story differently again. What the filings can give you are the two scales: here a debt-free manufacturer with a $41.6 billion backlog in the middle of a genuine shortage — there a commodity producer with three loss years in a row, a fixed-cost corset and a price of 25 times a book value that the market would not even fully pay 14 months ago. Which scale weighs more for you is your decision — in full knowledge that it is a decision under uncertainty, not one that was obvious in hindsight. And that is exactly as it should be.

Sources

All original documents used in this analysis — to read for yourself:

- Sandisk Corporation — SEC annual report 10-K for fiscal year 2025, ended June 27, 2025 (filed August 21, 2025)

- Sandisk Corporation — SEC quarterly report 10-Q as of April 3, 2026 (filed May 1, 2026)

- Sandisk Corporation — SEC quarterly report 10-Q as of January 2, 2026 (filed January 30, 2026)

- Sandisk Corporation — SEC quarterly report 10-Q as of October 3, 2025 (filed November 7, 2025)

- Sandisk Corporation — SEC quarterly report 10-Q as of March 28, 2025 (filed May 12, 2025)

- Sandisk's complete SEC filing history: EDGAR overview (sec.gov)

- Fundamental data (metrics, quarterly series, valuation; data as of July 8, 2026), reconciled with the SEC filings.

- Screener and rating data: in-house stock scanner (data as of July 8, 2026; scanner membership checked live on July 14, 2026).

Transparency & disclaimer: This analysis is a journalistic contextualization of publicly available information and is not investment advice, not a financial analysis in the regulatory sense, and not a solicitation to buy or sell securities. Stock investments carry substantial risks up to total loss. All information without guarantee; the data cut-off is noted in the text in each case. The author holds no position in Sandisk stock at the time of publication.

Our Bottom Line at a Glance

- Market position & product neutral

- One of only a few NAND makers in the world, with secured manufacturing access through the Kioxia joint venture — but the product is commodity ware without an HBM counterpart of its own, and the booming data-center market accounts for only a quarter of revenue so far (Q3 FY 2026: $1.47 of $5.95 billion).

- Earnings power & balance sheet positive

- $5.95 billion of revenue and $3.6 billion of net income in the quarter through April 3, 2026 (a 78.4 percent gross margin), $4.5 billion of operating cash flow in nine months; zero financial debt, $3.7 billion of cash, a $6 billion buyback program, an Altman Z around 13.

- Cyclicality & price dependence negative

- The boom is almost entirely a price boom (+248 percent per gigabyte on flat volume; consumer volume −40 percent). Fiscal years 2023 through 2025 brought three losses in a row (a combined −$4.5 billion), and the company's own risk chapter describes overcapacity phases with price crashes as a recurring industry pattern.

- Valuation & expectations negative

- About $400 billion of market value, P/S around 30, P/B around 25, up 727 percent since the start of the year, roughly 58 times the 52-week low (data as of July 8, 2026): the price treats the best margin in the company's history as a plateau — the same company traded below book value 14 months ago.

- Contracts & dependencies neutral

- $41.6 billion of order backlog from long-term contracts plus $511 million of customer prepayments are a genuine first — but only about 15 percent of it becomes revenue within twelve months, the Kioxia corset obligates Sandisk to 50 percent of the fixed costs even without orders (plus $993 million of off-balance-sheet guarantees), and customer concentration is rising (top 10: 46 percent, for the first time a single customer above 10 percent).

Sandisk is the proof that the same market can price the same company, within 14 months, once below book value and once at 25 times book value: first the spurned spin-off with a $1.8 billion goodwill write-off, now a debt-free record earner with a $41.6 billion backlog in the middle of the NAND shortage. The Greenblatt scanner did the math correctly — but it is calculating with a boom that sits almost entirely in the price per gigabyte, on flat volume, with three loss years in the recent history and a fixed-cost corset toward Kioxia that works against Sandisk in a downturn. Whether a 78 percent gross margin is a plateau or the top of the roller coaster will be decided by the memory cycle — not by the hindsight bias's "you could have known". Not investment advice.

What Our Rating Means

- If you don't own the stock

- As long as the question raised in the bottom line stays open, we see no basis for an entry.

- If you hold it in your portfolio

- Our findings offer no acute reason to sell — the checkpoints named remain decisive.

A journalistic assessment by our editorial team at the time of the deep dive, based on public sources — not investment advice and not a solicitation to buy or sell. Your personal circumstances (investment goals, risk capacity, taxes) cannot be taken into account. What our categories mean, how verdicts are formed, and what conflicts of interest exist →

Worth Noting

- Sandisk reports in an offset fiscal year (ending: the Friday closest to June 30); "FY 2026" denotes the period from June 28, 2025 through July 3, 2026, and the nine-month figures end April 3, 2026. All periods are explicitly dated in the text.

- The $4.5 billion of FY 2026 net income is a nine-month figure, not a full-year figure; the comparison with the prior full years in the net-result chart is labeled accordingly.

- Price and valuation figures are dated July 8, 2026 (about $2,335 per share, about $400 billion of market value); analyses are evergreen, daily prices are not a buy argument.

- The FY 2025 loss (−$1.6 billion) includes the goodwill write-off of $1.8 billion; even without it, only a slim pre-tax profit remained. The scanner membership (Greenblatt, third place) was verified live on July 14, 2026; as of the July 8 data cut-off Sandisk additionally led the EBIT-margin ranking.

Frequently Asked Questions

Sandisk (Nasdaq: SNDK) of Milpitas, California, makes NAND flash memory — the chips in SSDs for data centers and PCs, in smartphones, memory cards and USB sticks. The end markets are called Datacenter, Edge and Consumer. The memory wafers are made in the Flash Ventures joint venture with Kioxia in Japan. In fiscal year 2025 (ended June 27, 2025) Sandisk generated $7.4 billion in revenue, then $5.95 billion in the quarter through April 3, 2026 alone.

Until February 2025 Sandisk was a wholly owned subsidiary of Western Digital. On February 21, 2025 WDC spun off the flash business: shareholders received one third of a Sandisk share per WDC share; SNDK has traded on the Nasdaq since February 24, 2025. WDC initially kept 19.9 percent and gave the stake up almost entirely by early 2026 — as a parting gesture Sandisk also paid its parent $1.5 billion out of a loan taken on specifically for that purpose.

Joel Greenblatt's Magic Formula looks for companies with a high return on capital and a high earnings yield. Sandisk's record quarter (a 78.4 percent gross margin, an EBIT margin of the last four quarters around 70 percent) meets both criteria — in the top trio with Micron and Western Digital (second place on July 8, third at the live check on July 14, 2026). The formula's known weakness: with cyclicals it preferentially fires at the earnings peak, because it treats current record profits as a permanent state.

After the spin-off the share price fell so low that the market value sat below net book value — an accounting impairment indicator. The mandatory test showed that the company's carrying value exceeded its estimated fair value; Sandisk therefore wrote off $1.8 billion of goodwill in the quarter through March 28, 2025. As of April 3, 2026 about $5 billion of goodwill still sits on the balance sheet — just under 30 percent of total assets.

In the quarter through April 3, 2026 Sandisk signed multi-year supply contracts with major customers, partly with prepayments ($511 million of contract liabilities). The remaining performance obligations from them add up to $41.6 billion — more than five times the 2025 annual revenue. Only about 15 percent of that is expected to become revenue over the next twelve months; on prices and adjustment clauses the report gives no details.

Very: Sandisk holds 49.9 percent of three Flash Ventures joint companies with Kioxia, from which it must obtain substantially all of its flash memory. Sandisk contractually carries 50 percent of the fixed costs — even if it orders nothing —, guarantees about $993 million of factory lease agreements off balance sheet and puts the maximum loss scenario from the construct at just under $3 billion. The JV clauses can also make a takeover of Sandisk harder.

That depends on the yardstick: calculated on the last four quarters, the price-to-earnings ratio sits around 80 and would fall sharply if the record profits persisted. A price-to-sales ratio around 30 and price-to-book around 25, by contrast, price in that the best margin in the company's history becomes the permanent state (data as of July 8, 2026) — for a commodity product whose prices, per the company's own risk chapter, regularly crash as well. A low P/E at the cycle peak is no proof of a bargain.

Sandisk reports in an offset fiscal year that ends on the Friday closest to June 30. "Fiscal year 2026" runs from June 28, 2025 through July 3, 2026; the third quarter ended April 3, 2026, and fiscal year 2025 ended June 27, 2025. When comparing with the calendar-year figures of other chip companies you have to keep this shift in mind — which is why all periods in this analysis are explicitly dated.

Found an error?

Did you spot a factual error, an outdated number, or a typo in this deep dive? Let us know briefly — your report goes straight to the editorial team.