KLA Stock: The Quiet Quasi-Monopoly of Chip Inspection — and a Price That Presupposes Perfection

KLA builds the inspection and measurement technology without which no modern chip fab can run: a 60.9 percent gross margin, record revenue of $12.2 billion in fiscal year 2025, the sixteenth consecutive dividend increase. We read the annual and quarterly reports — and the other numbers are in there too: a third of revenue from China under tightening export controls, two customers accounting for 30 percent of revenue, and a valuation around 70 times earnings after the stock nearly doubled. Not investment advice — just the question of what perfection is allowed to cost.

There is a thinking trap that catches good investors above all — not the gamblers, the thorough ones. It goes like this: "This is the best company in the industry. Quasi-monopoly, dream margins, a dividend rising for years. With a company like that, you can't go wrong." The sentence feels like prudence. In truth it is a free pass your own head writes for itself: the moment a company wears the label quality, the brain stops asking about the price. Psychologists call this the halo effect — the shine of one attribute outshines all the others. So let's make a deal: we look at KLA Corporation (NASDAQ: KLAC) together — a company that genuinely ranks among the best the stock market has to offer. And then we read what KLA itself reported, under penalty of law, to the U.S. securities regulator, the SEC: in the annual report (10-K) for fiscal year 2025 and in the quarterly reports (10-Q) through March 31, 2026. Because both halves of the truth are in there: the margins of a quasi-monopoly. And the sentences about China, customer concentration and cyclicality that the shine outshines. In the end, you decide for yourself.

What KLA actually does

A modern chip fab is probably the most sensitive production site in the world: on a silicon disc (the "wafer"), hundreds of process steps create structures smaller than a virus. A single undetected speck of dust, a deviation of a few nanometers — and a batch worth millions is scrap. This is exactly where KLA earns its money: the company does not build the furnaces and lithography machines that make chips — it builds the eyes of the fab. Inspection systems that find defects, and measurement systems (the technical term: metrology) that check whether every layer sits right. The field is called "process control", and the annual report describes the role like this:

"We are a leading supplier of process control and yield management solutions and services for the semiconductor and related electronics industries. Our broad portfolio of inspection and metrology products, and related service, software and other offerings, support R&D and manufacturing of ICs, wafers and reticles."

— KLA Corporation, SEC annual report 10-K for fiscal year 2025, Item 7 (MD&A)

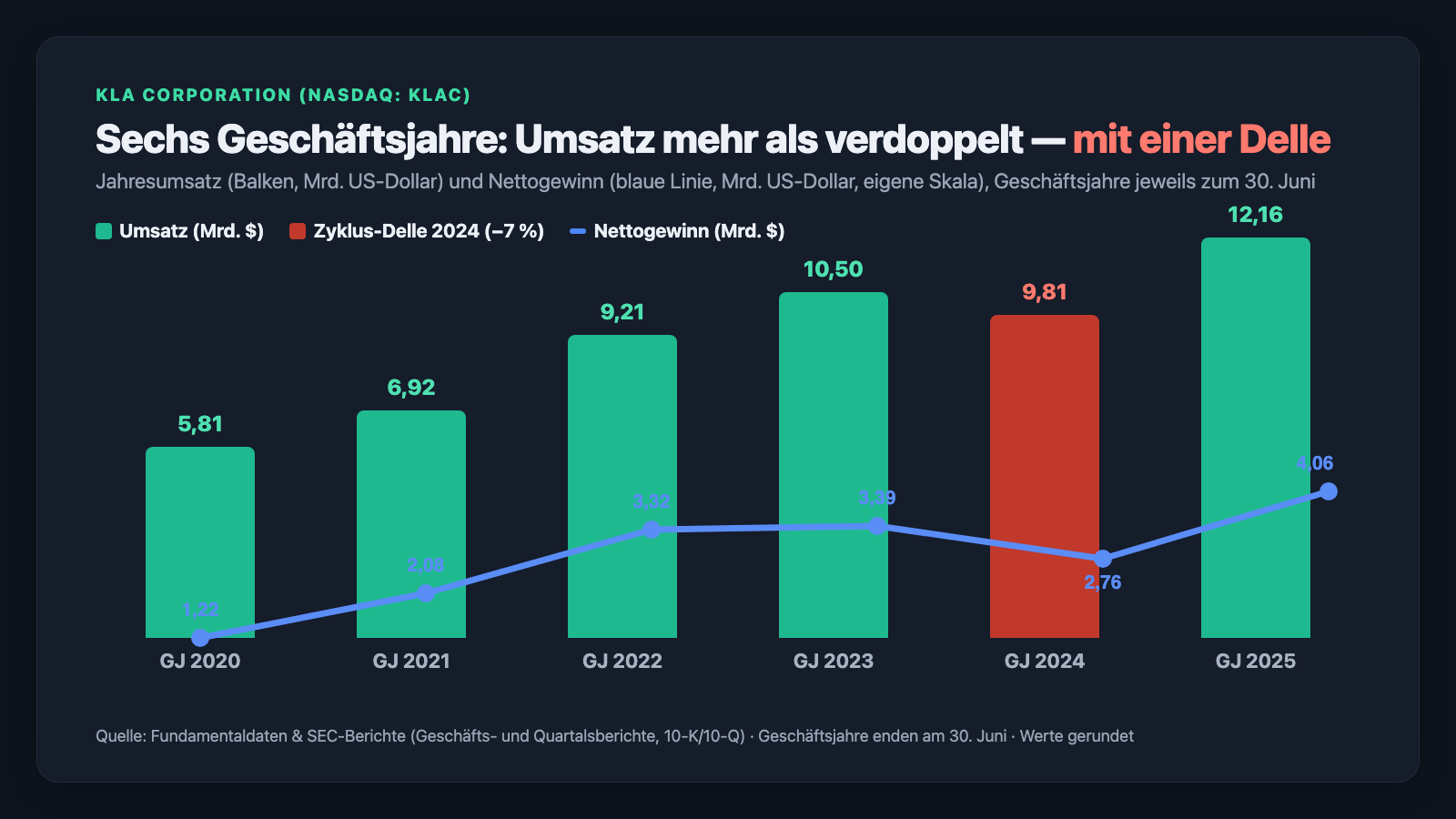

"Leading supplier" is almost an understatement. In the process-control niche, KLA is the top dog by such a margin that industry insiders speak of a quasi-monopoly — and the numbers speak the same language: a 60.9 percent gross margin and a good 41 percent operating margin in fiscal year 2025. Only a company that is nearly irreplaceable can charge margins like that. The firm itself is a child of the chip industry's early days: it was formed in 1997 as KLA-Tencor from the merger of KLA Instruments and Tencor Instruments, in business since 1975 and 1976 respectively. Headquarters: Milpitas, California; about 15,000 employees (as of June 30, 2025); three segments, of which the largest — Semiconductor Process Control — delivers the lion's share. One detail you must keep in mind for every number in this analysis: KLA's fiscal year ends not on December 31 but on June 30. "Fiscal year 2025" here therefore means July 2024 through June 2025. And a second detail for reading the chart: in June 2026, KLA split its stock 10-for-1 (current report, 8-K dated June 12, 2026) — one share became ten, and nothing about the company's value changed. Remember that for later; it comes back when we get to psychology.

Where the stock shows up in our scanner

Every day we run about 3,500 stocks through our scanners. KLA lights up in 2 scanners (data as of July 9, 2026) — and both are seals of quality, not warning lamps: the EBIT margin ranking, home to the most profitable companies in the market, and Joel Greenblatt: Magic Formula, which combines return on capital and earnings yield. Translated: our scanner confirms the quality thesis — KLA earns exceptionally much money per dollar of revenue (EBIT margin around 41 percent) and per dollar of capital employed. The return on equity works out to about 95 percent — though a footnote belongs here: it is that high because KLA deliberately keeps its equity small through years of share buybacks; more on that later. The market technicals were gleaming too: a relative strength of 96 — the stock ran better than 96 percent of the market —, the price sat only about 11 percent below its all-time high, but had also nearly doubled within six months (+88 percent) and nearly tripled within twelve (data as of July 9, 2026). And that is exactly where the tension begins that runs through this analysis: a nearly perfect business — at a price that already presupposes perfection. For a comparison of how the same AI fever looks one floor down, it is worth reading our Amkor analysis (a chip packager with a halved profit) and the Credo analysis (the cable the AI hangs on).

The numbers over the years — first what impresses, honestly appraised

Let's start with what genuinely impresses — and at KLA that is a lot. In fiscal year 2025 (July 2024 through June 2025), KLA generated $12.16 billion in revenue, a plus of 24 percent, and earned $4.06 billion in net income on it — every third revenue dollar became net profit. Operating cash flow came to $4.08 billion. And the run continued: in the first nine months of fiscal year 2026 (July 2025 through March 2026), revenue rose to $9.92 billion (+10 percent), net income to $3.47 billion (+21 percent). The January-through-March 2026 quarter was, at $3.42 billion in revenue, the strongest in company history, with a gross margin around 61 percent. The driver is exactly what you suspect: the report names the AI infrastructure wave, the race to 2-nanometer chips — the finer the structures, the more control every layer needs — and, most recently, a jump in memory investments: Korea revenue rose 80 percent in the January–March 2026 quarter.

On top of that comes a buffer that hardly any cyclical has: a growing share of revenue is recurring. Service revenue — maintenance, spare parts, software for the installed fleet of systems — came to $2.31 billion in the nine months through March 2026, a good 23 percent of total revenue, up 16 percent year over year. Machines can be canceled; running fabs must be maintained. So much for the picture that creates the halo. Now we turn the page — because an SEC filing is honest under penalty of law, and KLA writes four things in there that you should know before you sign the quality free pass.

What the filings say — the uncomfortable truths

Uncomfortable truth no. 1: every third revenue dollar came from China — and KLA itself reckons with losing revenue

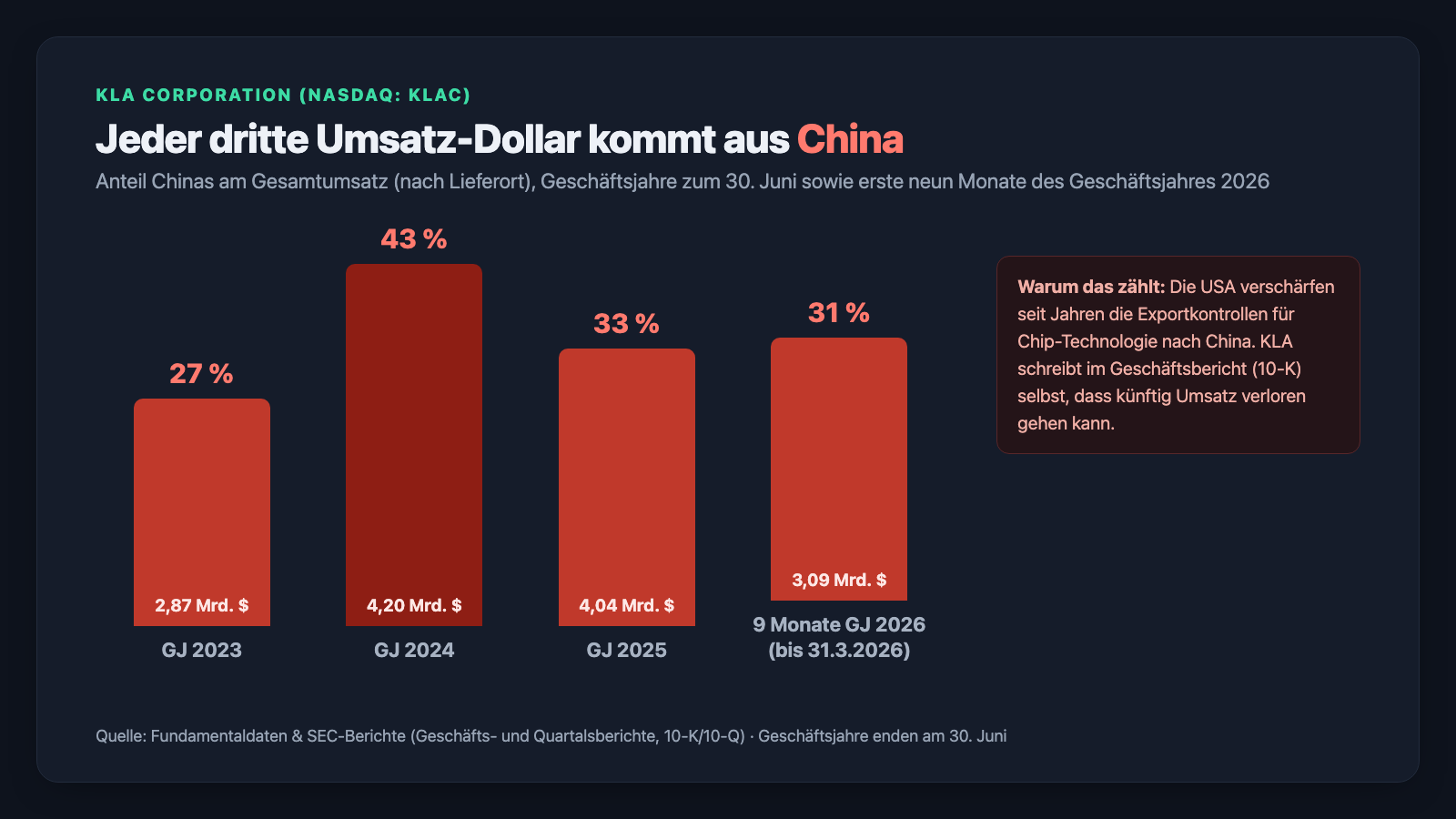

China's chip industry is arming up massively, with KLA technology among its tools. In fiscal year 2024, 43 percent of KLA's revenue came from China; in fiscal year 2025 it was still 33 percent ($4.04 billion), and in the nine months through March 31, 2026 about 31 percent. At the same time, the United States has been tightening export controls on chip technology bound for China for years — and the annual report says with rare clarity what that can mean:

"We may lose revenue in future periods related to anticipated sales to customers in China unless we are able to replace their orders with other customer orders for which either an export license has been obtained or is not required. Our revenue from sales of products and provision of services to customers in China was 33%, 43% and 27% for fiscal years 2025, 2024 and 2023, respectively."

— KLA Corporation, SEC annual report 10-K for fiscal year 2025, Item 1A "Risk Factors"

Two things make the passage more explosive than it sounds. First, the subordinate clause in the same chapter: the U.S. restrictions could make it easier for China's own inspection vendors to win market share — Beijing subsidizes self-sufficiency with billions. A quasi-monopoly is only a quasi-monopoly as long as nobody is forced to build alternatives. Second, the reverse direction that arrived in 2025: in April 2025, China imposed export controls on rare earths — raw materials that, per the annual report, sit inside components of KLA products. The trade war thus potentially cuts both ways. To be fair: so far the risk has stayed manageable — the China share normalized from 43 to 31–33 percent while total revenue rose to record levels, because Taiwan, Korea and the United States filled the gap. But a third of revenue tied to a region whose access depends on regulations written in Washington remains the single biggest bet in KLA's books.

Uncomfortable truth no. 2: two customers, thirty percent of revenue — and orders come with no purchase obligation

Customer concentration means: if your neighbor told you his shop was doing splendidly, but two buyers provided almost a third of the receipts — would you swallow for a second? At KLA, the quarterly report puts it like this:

"In the three months ended March 31, 2026, two customers accounted for approximately 19% and 11% of total revenues each. […] In the nine months ended March 31, 2026, one customer accounted for approximately 17% of total revenues."

— KLA Corporation, SEC quarterly report 10-Q as of March 31, 2026, Note 16 "Segment Reporting and Geographic Information"

The annual report names names, too: in each of fiscal years 2023 through 2025, more than ten percent of annual revenue sat with Taiwan Semiconductor Manufacturing Company (TSMC), and in 2023 additionally with Samsung Electronics. Now, TSMC is roughly the most solvent major customer you could wish for — the concentration risk here is not a question of creditworthiness but of investment moods. Because KLA states expressly in its risk factors that in this concentrated environment customers can change, delay or cancel orders, that the systems are configured to customer specifications (so cancellations end up expensive) — and elsewhere, that the backlog does not permit a reliable conclusion about the timing of future revenues. There is no long-term purchase obligation securing KLA's record revenues; there are the investment plans of a handful of chip giants. If TSMC or Samsung push their build-out back by two quarters, it shows up in KLA's numbers immediately. That is not a weakness of the business model — it is its nature. But it sits badly with a valuation that prices in friction-free growth.

Uncomfortable truth no. 3: the business is cyclical — the last dent was two years ago, not twenty

In the intoxication of AI records, it is easy to forget what kind of business this is. KLA itself does not forget:

"Still, our business has historically been cyclical with respect to the capital equipment procurement practices of semiconductor, semiconductor-related and electronic device manufacturers, and it is impacted by the investment patterns of such manufacturers in different global markets."

— KLA Corporation, SEC annual report 10-K for fiscal year 2025, Item 1 "Business"

And its own history supplies the proof: in fiscal year 2024 — July 2023 through June 2024, in the middle of the chip downturn after the pandemic boom — KLA's revenue fell 7 percent to $9.81 billion, and net income slumped 18 percent to $2.76 billion. The red bar in our chart above is not distant history; it is two fiscal years old. A number from the fiscal 2025 footnotes fits the same picture: the stock of contractually committed, not yet billed work (the technical term: remaining performance obligations — in effect the order book) fell from $10.0 billion at the end of September 2024 to $7.9 billion as of June 30, 2025 — so the record revenues were partly served out of the order cushion. None of this is an alarm signal; cycles belong to this business the way ebb and flow belong to a harbor. Only: whoever buys at 70 times earnings is implicitly betting that the tide never goes out again. The filing says: it always did, eventually.

Uncomfortable truth no. 4: billions for shareholders, debt at equity level — and insiders selling at the record price

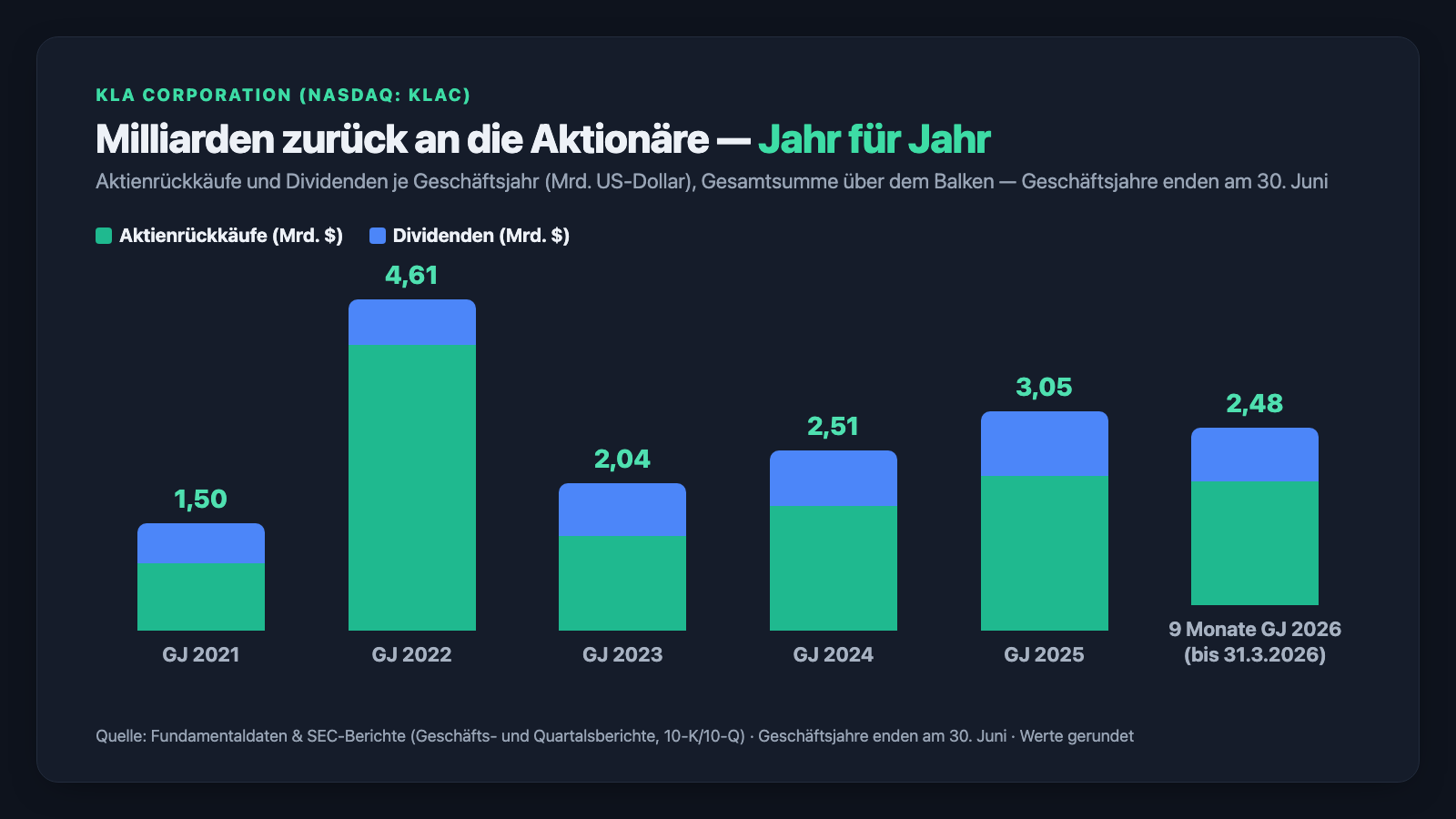

KLA's capital returns are impressively consistent: in fiscal year 2025 the company bought back $2.15 billion of its own shares and paid $905 million in dividends; the quarterly dividend rose to $1.90 per share (pre-split) — per the annual report the sixteenth consecutive dividend increase. In the January–March 2026 quarter, the board added another $7 billion of fresh buyback authorization on top; as of March 31, 2026, $10.31 billion stood authorized and ready. The share count has been falling for years — of what the company earns, a great deal really does reach the shareholders.

The flip side is on the balance sheet: as of March 31, 2026, $5.89 billion of long-term debt stood against equity of $5.83 billion — the years of buybacks have deliberately kept equity thin (hence the optically spectacular return on equity of about 95 percent and a price-to-book ratio around 58, which you therefore should not take at face value). Against that stand $4.96 billion in cash and securities; with more than $4 billion of operating cash flow per year, all of this is sustainable — as long as the tide holds. And two dated observations from the summer of 2026 that you should know: in June 2026 came the 10-for-1 stock split — a purely cosmetic move that makes a stock "look cheaper" and historically often arrives when a company wants to grow its retail-investor fan base. And shortly afterwards, insiders reported sales (insider filings, Form 4): CEO Richard Wallace sold shares worth about $10 million on June 11, 2026, and CFO Bren Higgins about $7.4 million worth on July 2, 2026. Such sales are routine at U.S. corporations and often planned long in advance — but they fit the picture: the people who know the company best are taking money off the table at the record price. For a sense of proportion: CEO Wallace earned about $25.1 million in fiscal year 2025, per the proxy statement (DEF 14A).

And AI? A winner of the wave — without selling AI itself

Because in 2026 every chip stock glows in the AI light, we checked the filings systematically for it. The finding is twofold. First: AI is the most important demand driver — KLA calls it, in the quarterly report, a technology inflection point driving innovation and demand at the leading edge, and sees its own portfolio as uniquely positioned to support the AI build-out (original: "AI is a technology inflection point driving innovation and demand at the leading edge, and we believe our portfolio of products is uniquely positioned to support leading-edge demand and the ongoing AI buildout", quarterly report 10-Q as of March 31, 2026). Second: KLA also uses AI itself — the annual report describes AI capabilities being built increasingly into technology development, operations and the company's own products and services; modern defect detection is barely conceivable without learning algorithms. What KLA, per the filings, is not: an AI seller. The revenue source remains inspection and metrology systems plus service — AI makes them better and more sought-after, but is not itself sold. In our company-by-company AI classification, we therefore list KLA as "Uses AI". For you this means: the AI story in this stock is real, but indirect — it hangs on TSMC, Samsung and company continuing to fill fabs with equipment. If the AI investment cycle snaps, it hits the equipment maker with a delay, but with certainty.

Valuation: you are paying for perfection — and getting no discount for the risks

Now to the question of price, and we stay with orders of magnitude instead of daily prices (data as of July 9, 2026): the market valued KLA at a good $330 billion — about 70 times net income and 26 times revenue of the trailing four quarters. For perspective: the same company with the same quasi-monopoly margins could be had for a fraction of these multiples across long stretches of recent years; the doubling of the price within six months made the valuation grow faster than any fundamental — earnings of the last nine months rose 21 percent, not 90. The dividend yield has melted to about 0.3 percent — not because the dividend is small, but because the price ran away from it. The "professionals' view" changes little: 30 analysts covered the stock most recently, the consensus stood at "buy" (average rating 1.4) with expected earnings growth around 36 percent for the coming fiscal year — Wall Street believes in the AI wave, and it prices it in fully. Do the math yourself: for a P/E of 70 to come back down to a down-to-earth 25 to 30 without the price falling, KLA would have to more than double its earnings — and along the way suffer not a single cyclical dip, no China shock, no investment pause by its two major customers. That is what "perfection priced in" means in concrete terms. The next reality check is already on the calendar: KLA's fiscal year ends at mid-2026, followed by the new annual report (10-K) with the outlook for 2027.

Opportunities and risks at a glance

What speaks for KLA:

- A quasi-monopoly in process control with pricing power: a 60.9 percent gross margin and about 41 percent operating margin in fiscal year 2025 — confirmed by our scanner hits in the EBIT margin ranking and the Magic Formula (data as of July 9, 2026).

- Record numbers with an AI tailwind: revenue +24 percent to $12.16 billion (fiscal year 2025), another +10 percent in the nine months through March 2026, Korea revenue +80 percent in the latest quarter on memory investments.

- Recurring revenue as a buffer: $2.31 billion of service revenue in nine months (about 23 percent of revenue, +16 percent) — the installed fleet has to be maintained even when new orders pause.

- Reliable capital returns: the sixteenth consecutive dividend increase, $2.15 billion of buybacks in fiscal year 2025, $10.31 billion of authorized buyback volume outstanding (March 31, 2026), more than $4 billion of operating cash flow per year.

- The smaller the chip structures (the 2-nanometer race, advanced packaging), the higher the control requirement per wafer — the structural trend runs in KLA's favor.

What speaks against it:

- A China cluster under political reservation: 33 percent of fiscal 2025 revenue (43 percent in 2024) from a region for which the United States keeps tightening export rules; KLA itself warns of revenue losses and strengthened Chinese competition; since April 2025, China's rare-earth export controls add a sourcing risk on top.

- Customer concentration without purchase obligations: two customers at about 19 and 11 percent of quarterly revenue (January–March 2026), TSMC above 10 percent for years — per the annual report, orders can be delayed or canceled, and the backlog does not allow a reliable revenue forecast.

- Cyclicality is documented, not theoretical: revenue −7 percent and net income −18 percent in fiscal year 2024; the order cushion (remaining performance obligations) fell within three quarters from $10.0 to $7.9 billion (September 2024 through June 2025).

- A valuation without a safety net: about 70 times earnings, 26 times revenue, a 0.3 percent dividend yield after the stock nearly doubled in six months (data as of July 9, 2026); long-term debt ($5.89 billion) at roughly the level of equity ($5.83 billion, March 31, 2026).

- Insiders sold at the record price: the CEO (about $10 million, June 11, 2026) and the CFO (about $7.4 million, July 2, 2026) per insider filings (Form 4) — routine, but no buy signal; add the 10-for-1 split of June 2026, a classic retail-investor magnet.

A human conclusion

Back to the free pass in your head. The halo has a point, after all: KLA is one of the best companies you can buy on a stock exchange — a quasi-monopoly at a choke point of the most important industry of our time, with margins others dream of, and a management that has reliably returned money to shareholders for sixteen years. Nothing in the filings calls that quality into question. But the halo effect consists precisely in the second question no longer being asked — and it is not "Is the company good?" but "What am I paying for it?". The answer stands above: 70 times an earnings stream that is demonstrably cyclical, with a third of revenue under political reservation and two major customers with no purchase obligation — after a doubling of the price during which the insiders sold and the company re-cut its stock into retail-friendly pieces. A great company and a dangerous stock can carry the same ticker at the same time; whether KLAC is currently both is decided solely by the price you pay. The calendar helps you: after June 30, 2026 comes the new annual report, and with it the answer to whether the AI cycle carries what the price is already celebrating. A quasi-monopoly does not run away — it just gets offered at a discount again from time to time, usually when nobody happens to be asking for it. What you make of it is your decision. And that is exactly as it should be.

Sources

All original documents used in this analysis — to read for yourself:

- KLA Corporation — SEC annual report 10-K for fiscal year 2025, ended June 30, 2025 (filed August 8, 2025)

- KLA Corporation — SEC quarterly report 10-Q as of March 31, 2026 (filed April 30, 2026)

- KLA Corporation — SEC quarterly report 10-Q as of December 31, 2025 (filed January 30, 2026)

- KLA Corporation — SEC quarterly report 10-Q as of September 30, 2025 (filed October 31, 2025)

- KLA Corporation — Proxy statement (DEF 14A) of September 23, 2025 — executive compensation

- KLA Corporation — Current report (8-K) of June 12, 2026 — 10-for-1 stock split

- KLA Corporation — insider filings (Form 4) of June 11 and July 2, 2026: EDGAR overview of Form 4 filings (sec.gov)

- KLA's complete SEC filing history: EDGAR overview (sec.gov)

- Fundamental data (valuation, momentum, analyst consensus; data as of July 9, 2026), reconciled with the SEC filings (annual and quarterly reports, 10-K/10-Q).

- Screener and rating data: in-house stock scanner (data as of July 9, 2026).

Transparency & disclaimer: This analysis is a journalistic contextualization of publicly available information and is not investment advice, not a financial analysis in the regulatory sense, and not a solicitation to buy or sell securities. Stock investments carry substantial risks up to total loss. All information without guarantee; the data cut-off is noted in the text in each case. The author holds no position in KLA stock at the time of publication.

Our Bottom Line at a Glance

- Market position & margins positive

- A quasi-monopoly in process control: a 60.9 percent gross margin and about 41 percent operating margin in fiscal year 2025 (ended June 30, 2025); scanner hits in the EBIT margin ranking and the Magic Formula (data as of July 9, 2026).

- Growth & AI demand positive

- Revenue +24 percent to $12.16 billion in fiscal year 2025, another +10 percent in the nine months through March 2026 with a record quarter ($3.42 billion); AI and memory investments drive it (Korea +80 percent in the latest quarter).

- Capital returns positive

- The sixteenth consecutive dividend increase, $2.15 billion of buybacks in fiscal year 2025, $10.31 billion of authorized buyback volume outstanding (March 31, 2026) on more than $4 billion of operating cash flow per year.

- China & export controls negative

- 33 percent of fiscal 2025 revenue from China (2024: 43 percent) under continually tightened U.S. export rules; KLA itself warns in the annual report (10-K) of revenue losses and strengthened Chinese competition; since April 2025, China's rare-earth export controls add a supply-chain risk.

- Concentration & cyclicality negative

- Two customers accounted for about 19 and 11 percent of revenue in the January–March 2026 quarter (TSMC above 10 percent for years), orders carry no long-term purchase obligation; fiscal year 2024 documents the cyclicality: revenue −7 percent, net income −18 percent.

- Valuation & insiders negative

- About 70 times earnings and 26 times revenue after the stock nearly doubled in six months (data as of July 9, 2026); long-term debt at roughly equity level; CEO and CFO sales of a combined $17 million or so in June/July 2026 (insider filings, Form 4).

KLA is the rare combination of a quasi-monopoly, dream margins and reliable capital returns — operationally there is little to criticize. What you pay for it, however, is a price that presupposes friction-free perfection: 70 times the earnings of a demonstrably cyclical business with a third of its revenue from China under political reservation and two dominant major customers. Not investment advice.

What Our Rating Means

- If you don't own the stock

- At the current price level, we don't see a sufficient margin of safety for an entry.

- If you hold it in your portfolio

- Our findings offer no reason to sell.

A journalistic assessment by our editorial team at the time of the deep dive, based on public sources — not investment advice and not a solicitation to buy or sell. Your personal circumstances (investment goals, risk capacity, taxes) cannot be taken into account. What our categories mean, how verdicts are formed, and what conflicts of interest exist →

Worth Noting

- The fiscal year ends on June 30: "fiscal year 2025" = July 2024 through June 2025. All quarterly figures in the text carry an explicit period.

- The 10-for-1 stock split took effect on June 11, 2026 (current report, 8-K dated June 12, 2026) — per-share figures before and after the split are not directly comparable; valuation multiples (P/E, P/S) are unaffected by it.

- The return on equity of about 95 percent and the price-to-book ratio around 58 are distorted by the buyback-driven small equity base and only meaningful to a limited extent (data as of July 9, 2026).

- Insider sales (CEO June 11, 2026; CFO July 2, 2026) are frequently pre-planned routine at U.S. corporations (Form 4) — they prove no knowledge of coming price declines, but they fit the stretched valuation.

Frequently Asked Questions

KLA builds the "eyes of the chip fab": inspection systems that find defects on wafers and photomasks, and measurement systems (metrology) that check every manufacturing layer — plus service and software for the installed fleet. In the process-control niche, KLA is by far the leading supplier. The company was formed in 1997 from the merger of KLA Instruments and Tencor Instruments, is headquartered in Milpitas, California, and employed about 15,000 people as of June 30, 2025.

KLA — like several other U.S. tech companies — reports on an offset fiscal year that ends on June 30 each time. "Fiscal year 2025" therefore covers July 2024 through June 2025. When comparing with companies that report on a calendar-year basis, you have to keep this shift in mind; every figure in our analysis therefore names the period explicitly.

Considerably: in fiscal year 2025, 33 percent of revenue ($4.04 billion) came from China, and the year before it was as much as 43 percent; in the nine months through March 31, 2026 it was about 31 percent. The United States keeps tightening export controls on chip technology, and KLA itself writes in its annual report (10-K) that this may cost revenue in future periods and strengthen China's domestic competitors.

By classic yardsticks, yes: about 70 times net income and 26 times revenue of the trailing four quarters at a market value of a good $330 billion (data as of July 9, 2026) — after the stock nearly doubled within six months. The quality of the company is undisputed; the valuation, however, prices in friction-free growth, even though the business is historically cyclical per its own annual report (10-K) (fiscal 2024 revenue: −7 percent).

Yes, but indirectly: KLA sells no AI — it sells the control technology no AI-chip fab can do without. The quarterly report (10-Q as of March 31, 2026) calls AI a technology inflection point driving demand at the leading edge — visible, for instance, in Korea revenue (+80 percent in the January–March 2026 quarter on memory investments). At the same time, KLA builds AI capabilities into its own products; our AI classification: "Uses AI".

One share became ten, effective June 11, 2026 (current report, 8-K dated June 12, 2026); nothing changes about the value of the company or of your stake. Splits make a stock optically cheaper and handier for retail investors — historically they often come after strong price run-ups. Shortly after the split, the CEO and CFO sold shares worth a combined $17 million or so (insider filings, Form 4 of June 11 and July 2, 2026).

Found an error?

Did you spot a factual error, an outdated number, or a typo in this deep dive? Let us know briefly — your report goes straight to the editorial team.