MSG Entertainment Stock: The World's Most Famous Arena Lives Off One Christmas Show — and the Dolans Have the Final Word

Madison Square Garden, Radio City Music Hall, the Rockettes: Madison Square Garden Entertainment owns stages everyone knows — and shows up in our value scanner built on Joel Greenblatt's Magic Formula, surrounded by a dozen momentum signals near the all-time high. We read the annual report (10-K) for fiscal year 2025 and the quarterly report (10-Q) as of March 31, 2026: 18 percent of revenue comes from a single show born in 1933, the holiday quarter earns more operating profit than the entire year, $609 million of debt carries entirely floating rates — and the Dolan family controls 64 percent of the votes with 3.6 percent of the Class A shares. Not investment advice — just a front-row seat when the house lights come up behind the stage.

There is a moment when a concertgoer wants to become a shareholder. You are standing in Madison Square Garden, 20,000 people are singing, the hall is shaking, everything is sold out — and somewhere between the encore and the ride home you think: "They own this place. I'm buying the stock." Let's call it the fan reflex: we buy stocks like fan jerseys — of things we love and whose greatness we have seen with our own eyes. The reflex likes to invoke Peter Lynch's "buy what you know" but drops its second half: and then do your homework. Hardly any stock invites the fan reflex like Madison Square Garden Entertainment (NYSE: MSGE): the world's most famous arena, Radio City Music Hall, the Rockettes — and, most recently, even a hit in our value scanner built on Joel Greenblatt's Magic Formula, while the price sits at its all-time high. So let's make a deal: before you put the jersey into your portfolio, we read together what the company itself reported to the U.S. securities regulator, the SEC — in the annual report (10-K, the yearly mandatory filing) for fiscal year 2025 and in the quarterly report (10-Q) as of March 31, 2026. An SEC filing is honest under penalty of law. And in it stands one sentence about a 93-year-old Christmas show that carries the whole investment thesis — or doesn't. In the end, you decide for yourself.

What MSG Entertainment actually does

Picture MSGE as the landlord and promoter of America's rarest stages. The group owns or controls five houses: The Garden (the fourth Madison Square Garden arena, a New York fixture since 1879, up to 21,000 seats), The Theater at Madison Square Garden, Radio City Music Hall ("The Showplace of the Nation", since 1932, leased through 2038), the Beacon Theatre (leased through 2036) and The Chicago Theatre (purchased in 2007). MSGE earns money in three ways. First, as a stage landlord: concert promoters pay a license fee per night — from Billy Joel's 150-show residency to UFC fight nights. Second, as the producer of a single show of its own, more on that in a moment. Third, as landlord to its own relatives: the basketball Knicks and hockey Rangers of the publicly listed sister company MSG Sports must, under 35-year agreements (through 2055), play all home games at The Garden and pay arena license fees for it — in fiscal year 2025, arena licenses and other rentals brought in $79.9 million, on top of shared suite, food-and-beverage and sponsorship revenues. The company employs about 1,200 full-time and 5,400 part-time staff (as of June 30, 2025), 71 percent of them unionized.

And the show of its own? The Christmas Spectacular Starring the Radio City Rockettes has run at Radio City Music Hall since 1933 — the Rockettes celebrated their centennial in 2025. In the fiscal year 2025 season, the 91st production sold about 1.1 million tickets across 200 performances; the following season had 215 performances. For context on the group structure: MSGE is the youngest child of a Dolan spin-off series — in April 2023, today's Sphere Entertainment (operator of the Las Vegas sphere) spun off the traditional venues business as a standalone company and distributed about 67 percent of the shares to its shareholders. By the way, a rarity in the stock-market year 2026: in six MSGE SEC filings, the words "artificial intelligence" appear not a single time — this business model consists of people physically walking into a hall. But note, right here, the central tension of this analysis: irreplaceable stages with real, steadily growing operating profit — but the profit hangs on a single holiday quarter, the balance sheet on floating-rate debt, the voting rights on one family, and after the rally the market pays about 75 times annual earnings. It runs through every chapter.

Where the stock shows up in our scanner

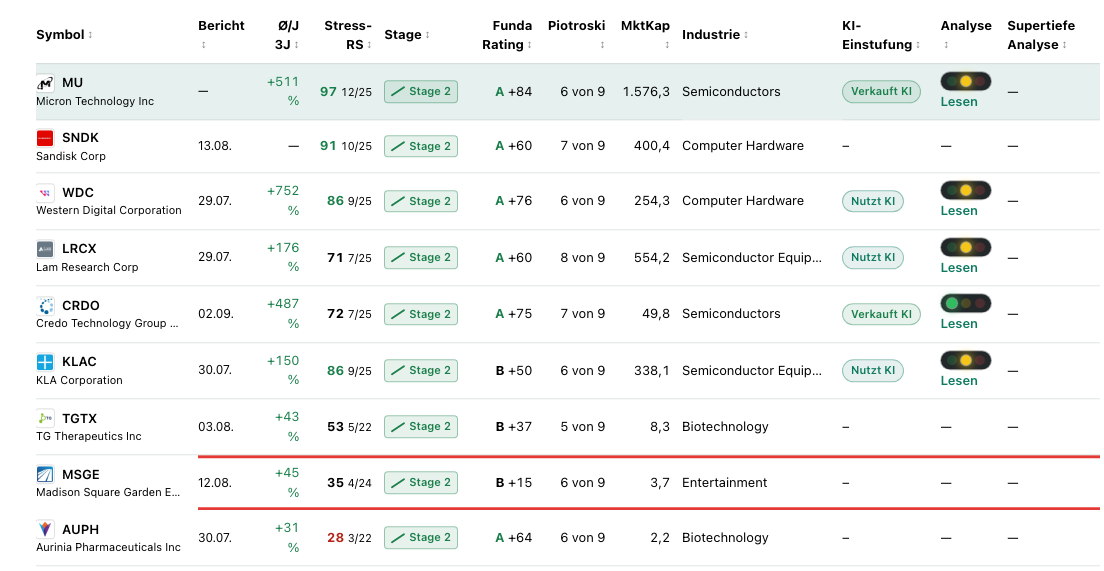

Every day we run about 3,500 stocks through our scanners. MSGE lights up in 19 scanners (data as of July 8, 2026) — one of the longest hit lists in the market, and not a single warning scanner among them. The most prominent hit is the Magic Formula of value investor Joel Greenblatt: buy good companies (high return on capital) at fair prices (high earnings yield). Our screener version checks the return on capital as return on equity times equity ratio — and this is exactly where you have to look before you believe the value label: MSGE's return on equity stands, per the fundamental data, at about 170 percent. Not because The Garden were a money-printing machine, but because the denominator has almost vanished: after the spin-off and share buybacks, equity stood at minus $13.3 million as of June 30, 2025 — on $1.67 billion of total assets. A return on a mini-equity is like a class test with a single question: the top grade says little. How the same formula lights up at a cyclical at its earnings peak is something we dissected only recently at Micron — at MSGE it is not the cycle that tricks the formula, it is the balance-sheet structure.

The other 18 hits tell a different, more honest story — they are almost all momentum signals: Weinstein Stage 2 (a stable uptrend), "near 52-week high", "ATH" (the stock trades exactly at its all-time high, 0 percent below), price above the 50- and 200-day lines, Power Trend, Pocket Pivot, Minervini trend criteria, tight weekly ranges, institutional accumulation, Dual Momentum. The relative strength of 86 says: only 14 percent of the market ran better recently — plus 48.6 percent in six months, plus 41.8 percent year to date (data as of July 8, 2026). The Piotroski F-Score, a nine-point test of balance-sheet quality, stands at a decent 6 of 9; the Altman Z-Score, a classic early-warning gauge for insolvency, at a relaxed 4.1 (danger begins below 1.8) — bankruptcy really is not the issue here. But two metrics fall out of the choir of cheers: the EPS rating of 18 (earnings momentum weaker than 82 percent of the market) and an interest coverage around 2 — operating income covers the interest bill only a good two times. The scanner fingerprint therefore does not read "overlooked value gem" but: a momentum star at its all-time high, onto which a balance-sheet artifact has additionally pinned a value label. All the more important what the filings say.

The numbers over the years — honestly appraised

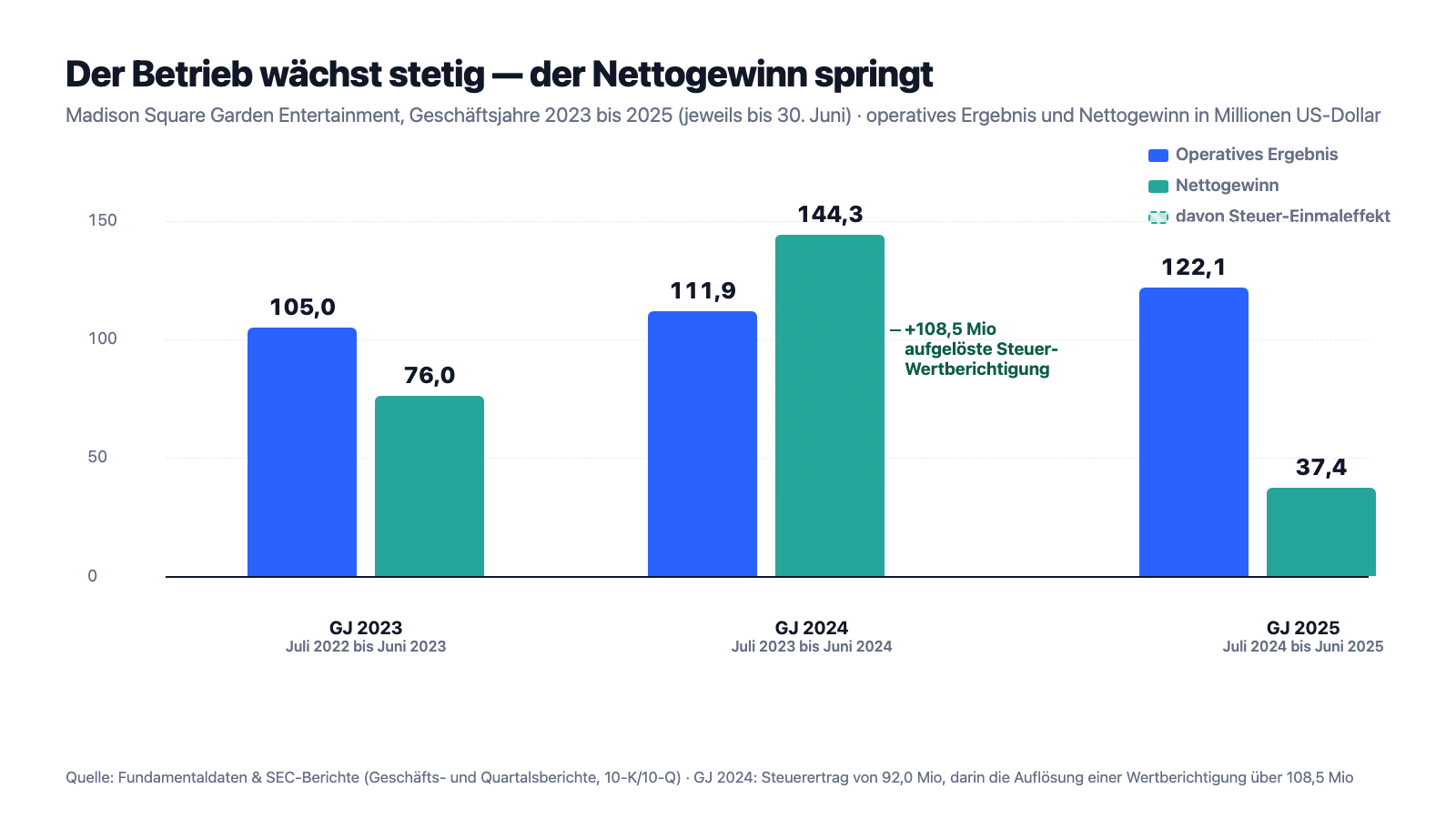

First, what has real substance. Revenue is stable around the billion mark: $851.5 million (FY 2023), $959.3 million (FY 2024), $942.7 million (FY 2025) — important: MSGE's fiscal year runs from July through June, "fiscal year 2025" ended on June 30, 2025. And in the first nine months of fiscal year 2026 (July 2025 through March 2026) business picked up: $864.5 million in revenue, plus 10 percent versus the prior-year period, carried by a record holiday season (15 additional performances, higher ticket prices, fuller halls) and more concerts at The Garden. Operating income grows with the calm of clockwork: $105.0 million (FY 2023), $111.9 million (FY 2024), $122.1 million (FY 2025); adjusted operating income (AOI) most recently rose to $222.5 million. Operating cash flow in fiscal year 2025 was $115.3 million, capital expenditures a modest $22.2 million — iconic, long-built houses need no chip fabs. And the debt shrinks on schedule: from $609.4 million (June 30, 2025) to $586.5 million in principal as of March 31, 2026. So much for the clockwork. Now look at net income — and instead of clockwork you see a bouncing ball:

$76.0 million, $144.3 million, $37.4 million — whoever reads only the net incomes of fiscal years 2023 through 2025 takes MSGE for a lottery ticket. The resolution follows below among the uncomfortable truths. Before that, a look at the current fiscal year, because it is genuinely pleasing: after nine months (through March 31, 2026) the books show $150.2 million in operating income (prior-year period: $147.8 million) and $76.2 million in net income (plus 18 percent) — despite a $13.8 million impairment on an abandoned office floor and $10.9 million in restructuring costs. Cash swelled from $43.5 million to $323.7 million, operating cash flow over the nine months was a hefty $368.1 million. But be careful with that cash balance, a good part of it is other people's money: the liability side shows $287.2 million in deferred revenue (above all pre-sold tickets and suite licenses) and $340.1 million in payables — ticket money MSGE collects in trust for promoters, and the fourth quarter (April through June) is structurally a loss and outflow quarter. Which brings us to the heartbeat of this business.

What the filings say — the uncomfortable truths

Uncomfortable truth no. 1: 18 percent of revenue hangs on a single show — and one quarter carries the whole year

The Christmas Spectacular is a world-class cash cow: 91 years of tradition, about 1.1 million tickets sold per season, rising prices, rising occupancy. Which is exactly why the risk chapter of the annual report contains a sentence the fan reflex never reads:

"The financial results of our business are dependent on the Christmas Spectacular production, for which the 2024 production represented 18% of our revenues in Fiscal Year 2025. […] The popularity of the Christmas Spectacular has in the past declined, for example, as a result of the COVID-19 pandemic, and if it were to decline in the future (including, for example, due to an economic downturn or another pandemic or other public health emergency), our revenues from ticket sales and concession and merchandise sales would decline, possibly materially as they did during the COVID-19 pandemic, and we might not be able to replace the lost revenue with revenues from other sources."

— Madison Square Garden Entertainment, SEC annual report 10-K, fiscal year 2025, Item 1A "Risk Factors"

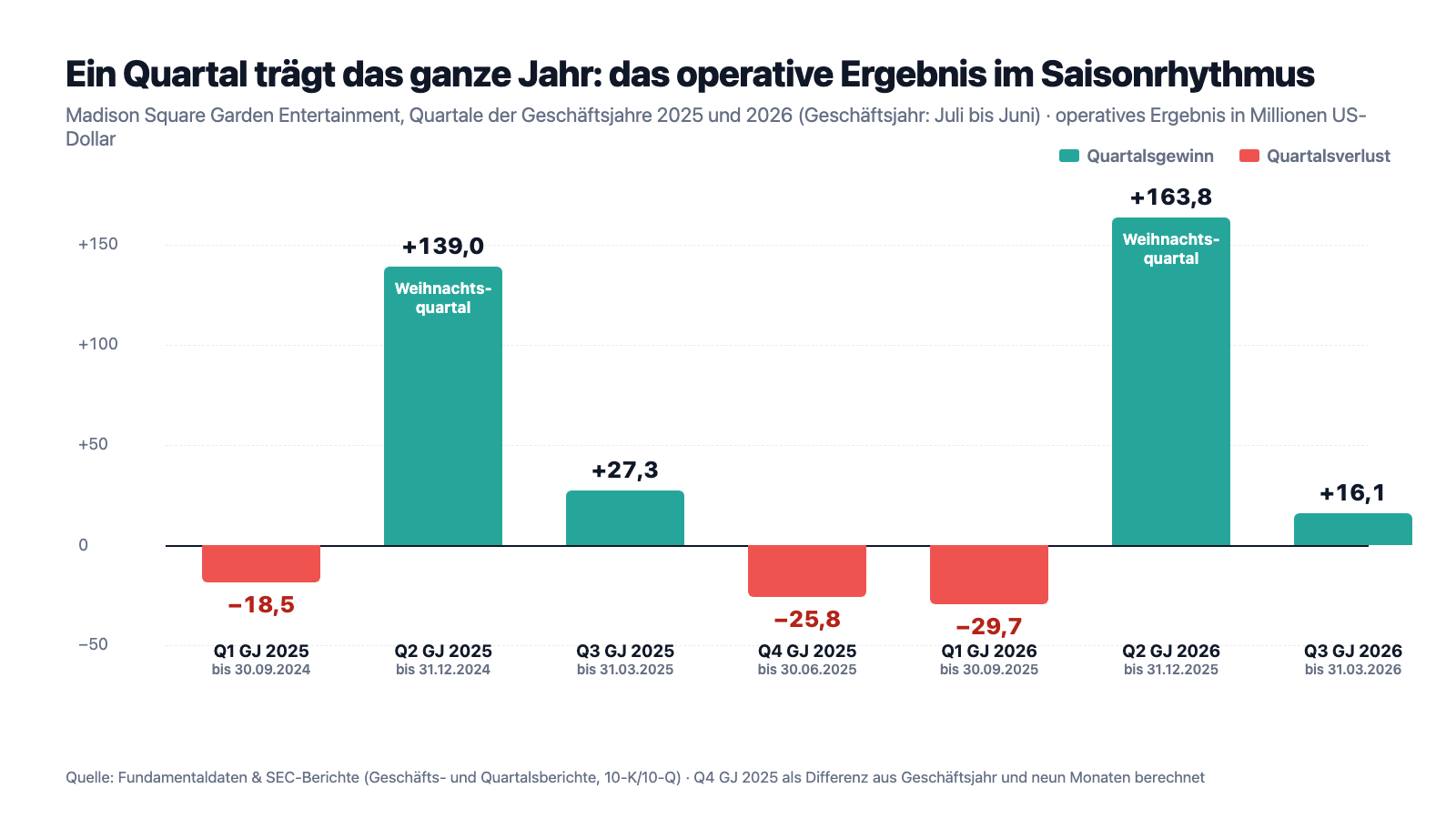

How much the show carries the year is visible in the quarterly rhythm — burn this picture into your memory:

In fiscal year 2025 the holiday quarter earned $139.0 million in operating income — more than the full year's $122.1 million, because the summer and closing quarters together lost $44.3 million. In the current fiscal year 2026 the same pattern, only steeper: minus $29.7 million in the fall, plus $163.8 million at Christmas, plus $16.1 million in the spring. MSGE is not a year-round business with a Christmas bonus — it is a Christmas business with an eleven-month run-up. Add to that: the concert business, the second pillar, is fickle and showed in 2025 how quickly the mix turns — concert revenues fell by $67.2 million in fiscal year 2025 because The Garden simply rented out more nights instead of promoting shows itself (less risk, but also less revenue per night). Whoever buys MSGE buys, at its core, two clusters: a Christmas show in a rented hall — the rights to the show and the Rockettes belong to MSGE independently of the lease, Radio City Music Hall itself is leased through 2038 — and an arena calendar in exactly one city.

Uncomfortable truth no. 2: $609 million of debt, entirely floating rate — and an equity that the buybacks have pushed below zero

Now to the balance sheet. The annual report says it without hedging:

"The Company is highly leveraged with a significant amount of debt and may continue to incur additional debt in the future. As of June 30, 2025, our total indebtedness was $609 million, $30 million of which matures before the end of Fiscal Year 2026."

— Madison Square Garden Entertainment, SEC annual report 10-K, fiscal year 2025, Item 1A "Risk Factors"

The details: a secured term loan of $609 million (refinanced in June 2025, due June 27, 2030, amortizing at 5 percent per year) plus a $150 million credit line. The catch sits in the same chapter: the entire debt carries floating rates — SOFR (the U.S. reference rate) plus 1.75 to 2.50 percentage points. If market rates rise, the interest bill rises with them immediately; exactly that happened from 2023 to 2024, when interest expense climbed from about $52 to $58 million despite amortization. In fiscal year 2025, interest expense of $50.5 million ate about 41 percent of operating income — an interest coverage of a good 2, where thoroughly healthy companies stand at 5 or higher. Honesty requires adding: measured against adjusted operating income of $222.5 million, the leverage is moderate (roughly 2.6 times, within the covenant maximum of 3.5 times), there is no going-concern note, and nothing big comes due before 2030 beyond the regular amortization. But now the equity: minus $13.3 million as of June 30, 2025. How can that be, with $153.0 million of accumulated retained earnings? Answer: since March 2023 the group has bought back its own shares for about $205 million (a $250 million buyback program; $44.8 million remained as of March 31, 2026) — the buybacks sit as a negative item of $205.2 million on the balance sheet and pushed equity below zero. Buybacks on a thin cash balance ($43.5 million as of June 30, 2025) and floating-rate debt are a question of style you can argue about: they lever earnings per share — and every future weakness just the same. As of March 31, 2026, equity stood at plus $48.0 million again thanks to the strong holiday season; on $1.96 billion of total assets that remains an equity ratio of 2.5 percent. What a balance sheet looks like when the same mechanics tip over is shown in our Sabre analysis — there, "highly leveraged" long ago became "the interest eats everything". MSGE is not there, not even close. But you should know the direction of the incentives.

Uncomfortable truth no. 3: the dream profit of 2024 was a tax artifact — the honest profit is smaller than the series looks

Back to the bouncing ball. Why does the same company earn $76 million, then $144, then $37? The resolution sits in the tax footnote of the annual report — dry, but decisive (amounts in thousands of dollars):

"Income tax benefit for Fiscal Year 2024 of $92,009 differs from income tax expense derived from applying the statutory federal rate of 21% to the pretax income primarily due to (i) income tax benefit due to a decrease in the valuation allowance of $108,506 and (ii) income tax benefit of $4,487 related to return to provision adjustments, partially offset by (iii) state income tax expense of $9,039."

— Madison Square Garden Entertainment, SEC annual report 10-K, fiscal year 2025, Item 7 MD&A "Income taxes"

Translated into everyday language: MSGE was sitting on old tax loss carryforwards whose usability the accountants had prudently written down. In fiscal year 2024 they concluded the carryforwards were usable after all — and reversed the write-down: a $108.5 million book gain without a single dollar of customer money flowing. Without this effect, fiscal year 2024 would have shown roughly $36 million in net income — almost exactly the level of fiscal year 2025 with its $37.4 million (which additionally absorbed an $11.2 million office impairment and $6.1 million in refinancing costs). The honest reading of the three years is therefore not "profit collapses from 144 to 37" but: the operation earns a steadily rising $105 to $122 million before interest and taxes — and after $50 million of interest and normal taxes, only $35 to $40 million of that remains at the bottom line. That number, not the 2024 outlier, is the yardstick for any valuation math. Remember: a one-off tax effect is like a tailwind gust in a hundred-meter dash — the time does not count for the record.

Uncomfortable truth no. 4: 3.6 percent of the Class A shares, 64 percent of the votes — the Dolans control the stage, the teams and the network

Whoever buys MSGE shares becomes a family's junior partner. The annual report describes the construction precisely:

"As of June 30, 2025, certain members of the Dolan family, including certain trusts for the benefit of members of the Dolan family (collectively, the 'Dolan Family Group') collectively owns all of our Class B common stock, approximately 3.6% of our outstanding Class A common stock […] and approximately 64.0% of the total voting power of all our outstanding common stock […] in matters other than the election of directors. […] The Dolan Family Group also controls Sphere Entertainment, MSG Sports and AMC Networks."

— Madison Square Garden Entertainment, SEC annual report 10-K, fiscal year 2025, Item 1A "Risk Factors"

The mechanics: every Class B share carries ten votes, all B shares belong to the family, and a stockholders agreement bundles them into a block. Within the family committee, CEO James L. Dolan holds two votes instead of one — he alone can block any takeover of the company there. MSGE is officially a "controlled company" on the NYSE and uses the exemptions: no majority-independent board, no independent nominating committee. In concrete terms: a takeover premium, the kind that lets shareholders of normal companies dream, exists here only if the family wants it. And the conflict of interest is built in, because the same family controls the most important tenant (MSG Sports with the Knicks and Rangers, agreements through 2055 including the teams' 67.5 percent share of suite revenues), the former parent (Sphere Entertainment, which shares office space and services with MSGE) and AMC Networks. Whether an arena license fee is "at market" is, in the end, negotiated by Dolans with Dolans. In fairness: it is precisely this family that has held and cared for the icons over decades instead of selling them — family control here is protection from short-term shareholder pressure and a lid on the share price at the same time. Both stand in the same chapter.

Uncomfortable truth no. 5: a tax privilege from 1982 is worth more than the annual profit — and politics is rattling it

Finally, the footnote hardly any investor knows. The Madison Square Garden complex has paid no property tax for over forty years:

"Our Madison Square Garden Complex benefits from a more limited real estate tax exemption pursuant to an agreement with the City of New York, subject to certain conditions, and legislation enacted by the State of New York in 1982. For Fiscal Year 2025, the tax exemption was $43.0 million. From time to time, there have been calls to repeal or amend the tax exemption."

— Madison Square Garden Entertainment, SEC annual report 10-K, fiscal year 2025, Item 1A "Risk Factors"

Do the quick math: the exemption was worth $43.0 million in fiscal year 2025 — net income in the same year was $37.4 million. The tax privilege is larger than the entire annual profit. True, under the arena license agreements the teams would formally have to bear any property tax; but if the exemption falls, the license fee MSGE receives from the Knicks and Rangers drops in return — the report calls the possible shortfall "significant". And the political pressure is documented: in 2023, New York representatives and the city's Independent Budget Office demanded the exemption be reviewed. What it would take is an act of the state legislature in Albany. That is not an acute risk — but it is a building block of profit that belongs not to the business model but to politics.

Valuation: $3.7 billion of market value for $37 million of honest profit

In early July 2026 the MSGE stock cost about $78.80; at about 47 million shares (Class A and B) that makes roughly $3.7 billion in market value — at the all-time high, after plus 48.6 percent in six months (data as of July 8, 2026). Put that in proportion: based on the last four quarters (net income around $49 million), that is a price-to-earnings ratio of about 75; based on the "honest" annual profit of $35 to $40 million it would be even higher. The enterprise value (market value plus $586.5 million of debt minus $323.7 million of cash, as of March 31, 2026) sits at roughly 32 times operating income of the last four quarters — for a business whose revenue shrank 2 percent in the last full fiscal year. The cash lens looks friendlier: measured against operating cash flow, the stock looks cheap at about 11 times — but that figure is pumped up by seasonal pre-sale money; based on fiscal year 2025 ($115.3 million operating cash flow, $22.2 million capital expenditures), a free-cash-flow yield of about 2.5 percent on the market value remains. There is a serious counter-argument you should know: iconic real estate like The Garden appears on the balance sheet at historical cost ($621 million of property and equipment) — the replacement or trophy value of such one-offs may lie far above that, and that is exactly what the buyers at the all-time high are betting on. Except: an asset treasure that a family with 64 percent of the votes never has to sell is rarely paid in full on the stock market. One more curiosity at the margin: our data show about 102 percent institutional ownership — not a typo but an artifact of the small free float: institutional positions are measured against the freely tradable Class A shares, and the family's B shares never trade. Translated: the free float is practically entirely in professional hands; hardly any retail investor is betting against the pros here anymore — or with them.

Opportunities and risks at a glance

What speaks for MSG Entertainment:

- Uncopyable assets: five iconic stages, among them the world's best-known arena, plus the rights to the Christmas Spectacular and the Rockettes (since 1933, about 1.1 million tickets across 200 shows in fiscal year 2025) — pricing power that cannot be rebuilt (annual report 10-K, fiscal year 2025).

- A steadily growing operation: operating income of $105.0 to $111.9 to $122.1 million (fiscal years 2023 through 2025), $222.5 million adjusted; nine months of fiscal year 2026 with plus 10 percent revenue and plus 18 percent net income — despite one-off burdens.

- Plannable base revenues: 35-year agreements with the Knicks and Rangers through 2055, multi-year suite and sponsorship contracts with price escalators, low capital needs ($22.2 million of capex in fiscal year 2025).

- Debt shrinks on schedule ($609.4 to $586.5 million within nine months), covenants met, no major maturity before June 2030, a relaxed Altman Z of 4.1 — no distress case.

- Momentum and strong hands: all-time high, relative strength 86, Stage 2, practically the entire free float held by institutions (data as of July 8, 2026).

What speaks against it:

- Extreme concentration: 18 percent of revenue from a single show, the holiday quarter earns more operating profit than the entire year, two of four quarters are structural loss quarters — and almost everything hangs on one city (10-K fiscal year 2025, Risk Factors).

- $609 million of debt at 100 percent floating rates (SOFR plus 1.75 to 2.50 points): the $50.5 million interest bill ate about 41 percent of operating income in fiscal year 2025; interest coverage only a good 2.

- Equity around zero (June 30, 2025: minus $13.3 million; March 31, 2026: plus $48.0 million) after about $205 million of share buybacks — earnings per share are levered, and so would be any weakness.

- A governance discount: the Dolan family with 64 percent of the votes on 3.6 percent of the Class A shares, a "controlled company" without a majority-independent board, permanent contracts with the family-controlled firms MSG Sports and Sphere — no takeover fantasy against the family's will.

- Valuation after the rally: a price-to-earnings ratio around 75 (last four quarters), enterprise value around 32 times operating income, a free-cash-flow yield of about 2.5 percent, an EPS rating of 18 — and a political risk named property-tax exemption ($43.0 million in fiscal year 2025, more than the annual profit).

A human conclusion

Back to the fan reflex from the beginning. Like most reflexes, it has a true core: The Garden is unique, the Rockettes are a money-printing machine with 93 years of operating experience, and this company will not disappear — the family that never has to give it up sees to that. But right there sits the thinking error: a great evening in the hall is no proof of a great price on the stock market. What you see as a fan — the sold-out hall, the show, the world fame — everyone else sees too; that is why the price sits at its all-time high and why the group costs about 75 times its annual profit. What you do not see as a fan stands in the mandatory filings: that almost the entire profit is earned in eight December weeks, that the interest bill hangs on a floating rate, that the buybacks pushed equity below zero, that a $43 million tax privilege depends on state politics — and that as a Class A shareholder you are, in every vote, the junior partner of a family that also controls the most important tenant next door. None of this is a scandal; all of it has stood transparently in the filings for years. It is just not what you feel on the way home from a concert. If you still want to put the jersey into your portfolio, then at least knowing what is printed on it — and what is not. What you make of it is your decision. And that is exactly as it should be.

Sources

All original documents used in this analysis — to read for yourself:

- Madison Square Garden Entertainment Corp. — SEC annual report 10-K for fiscal year 2025 (filed August 13, 2025)

- Madison Square Garden Entertainment Corp. — SEC annual report 10-K for fiscal year 2024 (filed August 16, 2024)

- Madison Square Garden Entertainment Corp. — SEC quarterly report 10-Q as of March 31, 2026 (filed May 7, 2026)

- Madison Square Garden Entertainment Corp. — SEC quarterly report 10-Q as of December 31, 2025 (filed February 6, 2026)

- Madison Square Garden Entertainment Corp. — SEC quarterly report 10-Q as of September 30, 2025 (filed November 6, 2025)

- Madison Square Garden Entertainment Corp. — SEC quarterly report 10-Q as of March 31, 2025 (filed May 6, 2025)

- MSG Entertainment's complete SEC filing history: EDGAR overview (sec.gov)

- Fundamental data (metrics, quarterly series, valuation; data as of July 8, 2026), reconciled with the SEC filings.

- Screener and rating data: in-house stock scanner (data as of July 8, 2026; Greenblatt membership verified live on July 14, 2026).

Transparency & disclaimer: This analysis is a journalistic contextualization of publicly available information and is not investment advice, not a financial analysis in the regulatory sense, and not a solicitation to buy or sell securities. Stock investments carry substantial risks up to total loss. All information without guarantee; the data cut-off is noted in the text in each case. The author holds no position in MSGE stock at the time of publication.

Our Bottom Line at a Glance

- Assets & market position positive

- Five uncopyable stages — among them the world's best-known arena — plus the rights to the Christmas Spectacular and the Rockettes (since 1933, about 1.1 million tickets per season) and 35-year agreements with the Knicks and Rangers through 2055. Pricing power and base revenues no competitor can rebuild (10-K, fiscal year 2025).

- Operating performance positive

- Operating income grows steadily: $105.0 to $111.9 to $122.1 million (fiscal years 2023 through 2025, adjusted $222.5 million); the first nine months of fiscal year 2026 delivered plus 10 percent revenue and plus 18 percent net income on low capital needs (capex fiscal year 2025: $22.2 million).

- Concentration & seasonality negative

- 18 percent of revenue from a single show, the holiday quarter earns more operating profit than the entire year ($139.0 against $122.1 million in fiscal year 2025), two of four quarters are structurally loss-making, almost everything hangs on New York — and the company's own risk report calls the revenue irreplaceable in a worst case.

- Balance sheet & capital allocation neutral

- $586.5 million of debt (March 31, 2026) is moderate against adjusted operating income (leverage roughly 2.6 times, covenants met, Altman Z 4.1) — but 100 percent floating rate (interest coverage only a good 2), and about $205 million of share buybacks have pushed equity to the zero line (June 30, 2025: −$13.3 million; March 31, 2026: +$48.0 million).

- Governance & valuation negative

- The Dolan family controls 64 percent of the votes with 3.6 percent of the Class A shares, simultaneously controls the anchor tenant (MSG Sports) and uses the NYSE exemptions for controlled companies; a takeover premium is impossible against the family's will. For that, the buyer at the all-time high pays about 75 times the net income of the last four quarters — plus a political risk named property-tax exemption ($43.0 million in fiscal year 2025, more than the annual profit).

MSG Entertainment is the opposite of a warning-scanner case: trophy assets, a steadily growing operation, plannable contracts through 2055 and no whiff of insolvency. But the value label from our Greenblatt scanner misleads — the spectacular return on capital is an artifact of the nearly vanished equity, while the buyer really pays about 75 times annual earnings for a business that makes its profit in eight December weeks, whose interest bill hangs on a floating rate, and in which Class A shareholders can decide nothing against the Dolan family. A great company and a sportily priced stock are two different things. Not investment advice.

What Our Rating Means

- If you don't own the stock

- As long as the question raised in the bottom line stays open, we see no basis for an entry.

- If you hold it in your portfolio

- Our findings offer no acute reason to sell — the checkpoints named remain decisive.

A journalistic assessment by our editorial team at the time of the deep dive, based on public sources — not investment advice and not a solicitation to buy or sell. Your personal circumstances (investment goals, risk capacity, taxes) cannot be taken into account. What our categories mean, how verdicts are formed, and what conflicts of interest exist →

Worth Noting

- MSGE reports in an offset fiscal year ending June 30; "fiscal year 2025" means July 2024 through June 2025. All periods are explicitly dated in the text.

- The fourth quarter of fiscal year 2025 is calculated as the difference between full-year and nine-month figures (revenue $154.1 million, operating income −$25.8 million).

- Price and valuation figures are dated July 8, 2026 (about $78.80 per share, about $3.7 billion in market value, all-time high); analyses are evergreen, daily prices are not a buy argument.

- The metric "about 102 percent institutional ownership" is a free-float artifact: institutional positions are measured against the freely tradable Class A shares; the Dolan family's Class B shares do not trade on the exchange.

Frequently Asked Questions

MSGE (NYSE: MSGE) operates five iconic venues — Madison Square Garden, The Theater at the Garden, Radio City Music Hall, the Beacon Theatre (all New York) and The Chicago Theatre — and produces the Christmas Spectacular starring the Rockettes. Revenue comes from renting the halls to concert promoters, its own Christmas show, food and beverage, suites and sponsorships, plus arena license fees from the Knicks and Rangers. Revenue in fiscal year 2025 (through June 30): $942.7 million.

Joel Greenblatt's Magic Formula looks for a high return on capital at a fair price. Our screener approximation multiplies return on equity by the equity ratio — and MSGE's return on equity sits around 170 percent because equity is almost zero after the spin-off and share buybacks (June 30, 2025: minus $13.3 million). Here the formula measures less the quality of the business than a balance-sheet artifact; the price-to-earnings ratio of about 75 is anything but classic value.

Existential: the 2024 production accounted, per the annual report (10-K), for 18 percent of fiscal year 2025 revenue — about 1.1 million tickets across 200 performances. The holiday quarter (October through December) earned $139.0 million in operating income, more than the full year's $122.1 million; the summer and closing quarters are structurally loss-making. The report itself warns that a loss of popularity could not be replaced.

The free float holds the majority of the capital, but not of the votes: the Dolan family owns all Class B shares (ten votes per share) plus 3.6 percent of the Class A shares and thus commands about 64 percent of the voting power (as of June 30, 2025). MSGE is a "controlled company" under NYSE rules; the same family also controls Sphere Entertainment, MSG Sports (Knicks, Rangers) and AMC Networks.

As of June 30, 2025 the books showed $609.4 million of debt (March 31, 2026: $586.5 million), entirely floating rate at SOFR plus 1.75 to 2.50 percentage points, due June 2030. Interest expense of $50.5 million ate about 41 percent of operating income in fiscal year 2025. Measured against adjusted operating income ($222.5 million) the leverage is moderate; covenants are met, the Altman Z-Score stands at 4.1.

Because of the capital structure from the 2023 spin-off and above all because of share buybacks: since March 2023 MSGE has repurchased about $205 million of its own shares, which sit as a deduction on the balance sheet. As of June 30, 2025 equity was minus $13.3 million; as of March 31, 2026 it was seasonally plus $48.0 million — a ratio of 2.5 percent of total assets. That levers earnings per share but makes the balance sheet more fragile.

Only on paper: of the 2024 net income of $144.3 million, $108.5 million came from the release of a tax valuation allowance — a one-off effect without any cash flow. Without it, fiscal year 2024 would have shown about $36 million in profit, close to the 2025 level ($37.4 million). The honest yardstick is the steadily growing operating income: $105.0 to $111.9 to $122.1 million (fiscal years 2023 through 2025).

After the rally to the all-time high, no longer by classic yardsticks: a market value of about $3.7 billion equals roughly 75 times the net income of the last four quarters and about 32 times operating income (enterprise-value basis, data as of July 8, 2026). Against that stands the argument of uncopyable trophy assets that sit on the balance sheet only at historical cost. Whoever buys pays an icon premium — not value metrics.

Found an error?

Did you spot a factual error, an outdated number, or a typo in this deep dive? Let us know briefly — your report goes straight to the editorial team.