Sabre Stock: The Invisible Travel Giant Earns $296 Million — and Pays $448 Million in Interest

If you have ever flown, chances are you have used Sabre without knowing it: 365 million bookings ran through the travel-booking network of the Texas group in 2025 — a company that lately calls itself "AI-native". The stock still shows up in our insolvency warning scanner. We read the annual report (10-K) for 2025 and the quarterly report (10-Q) as of March 31, 2026: $4,438.8 million of debt at interest rates up to 11.125 percent, equity of minus $1,036.5 million, operating cash flow below zero — and a 2025 annual profit that stems solely from the sale of the hotel business. Not investment advice — just a security check before you board.

There is a feeling that is bigger than any metric: "a company half the world travels through can't seriously be in danger." Call it the indispensability illusion — the reflex of confusing invisible infrastructure with invulnerability. And hardly any company feeds that reflex as well as Sabre Corporation (NASDAQ: SABR): born in 1960 as American Airlines' reservation system, today one of the three big global booking networks, through which 365.3 million billable bookings ran in 2025. If you have ever flown via a travel agency or a comparison portal, chances are you have used Sabre — without knowing it. And lately the group calls itself "AI-native" on top. Sounds like a rock in the surf. And yet the stock shows up in our warning scanner "Thomas Inso Kandidat", among companies with serious balance-sheet worries. So let's make a deal: before you rely on the feeling of indispensability, we read together what Sabre itself reported to the U.S. securities regulator, the SEC — in the annual report (10-K) for 2025 and the quarterly report (10-Q) as of March 31, 2026. An SEC filing is honest under penalty of law. And it contains a sentence about $4.3 billion of debt that you should have read. In the end, you decide for yourself.

What Sabre actually does

Picture the travel industry as a giant wholesale market: hundreds of airlines, hotel chains and car-rental firms want to sell, tens of thousands of travel agencies and booking portals want to buy. So that not everyone has to phone everyone else individually, there are GDS — "global distribution systems", the switchboards of the world travel market. Sabre operates one of the three big ones worldwide: the system bundles flights, prices and availability and collects a transaction fee for every booking that passes through. In 2025 that was 365.3 million billable bookings — 58 percent of them in North America. The second pillar is software for airlines: reservation systems, network planning, operations management, billed mostly as a SaaS fee per passenger boarded — 695.4 million of them in 2025. Since the first quarter of 2026 the two revenue streams are called "Marketplace" (first quarter of 2026: $618.0 million in revenue) and "Airline Technology" ($142.3 million). Until recently there was a third pillar: booking software for hotels. It was sold in July 2025 to a fund of the financial investor TPG — why, is one of the uncomfortable truths. What remains are 4,650 employees, run from Southlake, Texas.

And the AI story? It is more than a label: in 2024 Sabre launched SabreMosaic, an airline platform for personalized selling ("Offer and Order"), which the annual report describes as built on a modular, AI-enabled open technology architecture. The booking and price-search systems run on machine learning, airline customers get generative AI chatbots — and, genuinely interesting, agentic interfaces: docking points through which external AI assistants (which are just learning to book trips on their own) can reach directly into Sabre's marketplace. In February 2026, one executive was explicitly handed responsibility for innovation and agentic AI. Sounds like the future? It may well be. But note, already here, the central tension of this analysis: an indispensable network with genuine AI potential — carried by a balance sheet in which the interest eats the entire operating profit and equity has long been below zero. It runs through every chapter. How differently travel platforms can be positioned financially is shown, by the way, by our analysis of Tripadvisor — there the problem is not the balance sheet but the business model.

Where the stock shows up in our scanner

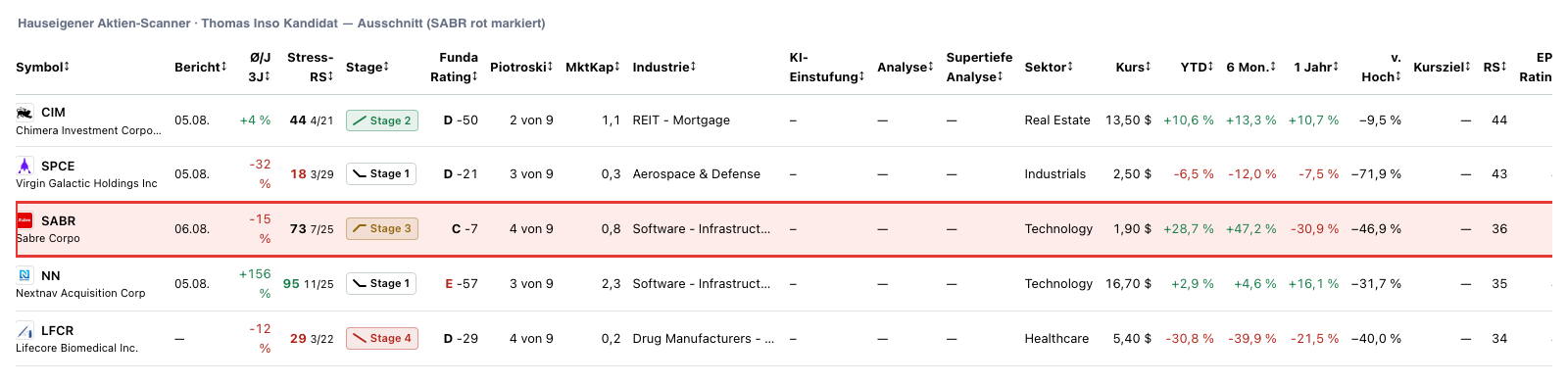

Every day we run about 3,500 stocks through our scanners. Sabre lights up in 7 scanners (data as of July 8, 2026) — and at first glance the hits contradict each other fiercely. On the warning side stands an entire distress trio: "Thomas Inso Kandidat" (a weak balance sheet with several warning flags, interest not covered by earnings, revenue falling year over year), the "Going-Concern-Distress-Proxy" and the "Altman-Z-Distress-Zone". Sabre's Altman Z-Score — a classic insolvency early-warning gauge built from several balance-sheet ratios — sits around zero; the danger zone historically begins below 1.1. The Piotroski F-Score, a nine-point test of balance-sheet quality, stands at 4 of 9 — a thoroughly healthy company stands at 8 or 9. And the interest coverage is negative: based on the last four quarters, earnings are not enough to earn the interest. How to read such warning lists — a smoke detector, not a demolition order — is something we explained in the article "Insolvency Radar: the Top 10".

On the other side, four hits report a comeback: the price trades above the 50- and the 200-day line, the price-to-sales ranking lists the stock at a price-to-sales ratio of about 0.27 — the market pays just over a quarter for a dollar of annual revenue —, Sabre sits in the "Profis 80%" scanner because roughly 90 percent of the shares are in the hands of institutions, and the Weinstein stage analysis puts the stock in Stage 3: topping out after an advance — the uptrend is running out of steam, the price action turns erratic. Exactly this coexistence — distress signals, cheap optics, a strong six-month rally — is the scanner fingerprint of a stock on which the market has not yet decided between "turnaround" and "debt trap". A low price-to-sales ratio next to three insolvency warning scanners is not proof of a bargain; it is a price tag for risk.

The numbers over the years — honestly appraised

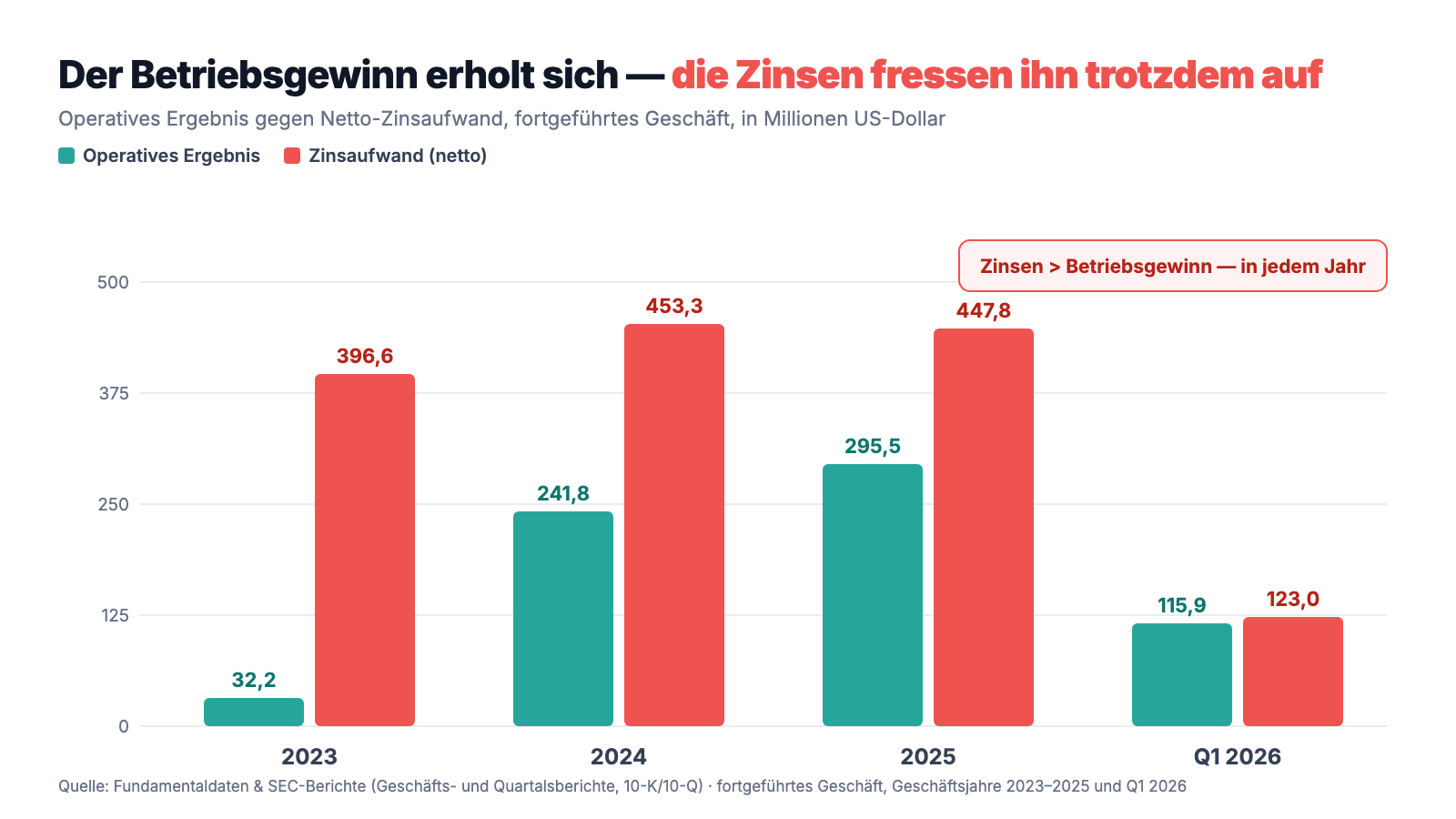

First, what genuinely has substance — and at Sabre there is quite a bit of it. Revenue from continuing operations is growing again: $2,642.1 million (2023), $2,744.8 million (2024), $2,771.0 million (2025) — and in the first quarter of 2026 another plus 8 percent to $760.3 million, carried by 5 percent more bookings (101 million in the quarter) and better rates. On cost cutting, management has delivered: technology costs fell from $950.7 million (2023) via $780.7 million (2024) to $711.1 million (2025) — the years-long migration from the mainframe to the cloud is paying off. Operating income has thereby increased almost tenfold: from $32.2 million (2023) to $295.5 million (2025); adjusted EBITDA rose from $289.5 to $500.2 million. For 2026, a program is under way to keep costs flat despite inflation (restructuring charges: $51 million were booked in 2025, about $65 million expected in total). That is a genuine operating turnaround — not an accounting trick. And now look at where all this fine progress flows:

In 2025, Sabre earned $295.5 million operationally — and wired $447.8 million in net interest to its creditors. 2024: $241.8 against $453.3. 2023: $32.2 against $396.6. Even in the strong first quarter of 2026, interest ($123.0 million) exceeded operating income ($115.9 million). On top of that, 2023 through 2025 brought another $237.3 million combined in redemption costs for debt refinanced early ("Loss on extinguishment of debt"). The bottom line of continuing operations therefore stayed red: −$491.5 million (2023), −$271.5 million (2024), −$255.5 million (2025). The small plus of $9.4 million in the first quarter of 2026 owes itself entirely to a tax credit of $11.4 million — pre-tax, there too, stood a minus of $2.0 million. Remember the sentence: at Sabre, the entire business currently works for the creditors. Which brings us to the uncomfortable truths.

What the filings say — the uncomfortable truths

Uncomfortable truth no. 1: $4.4 billion of debt at interest rates up to 11.25 percent — and the wall stands in 2029

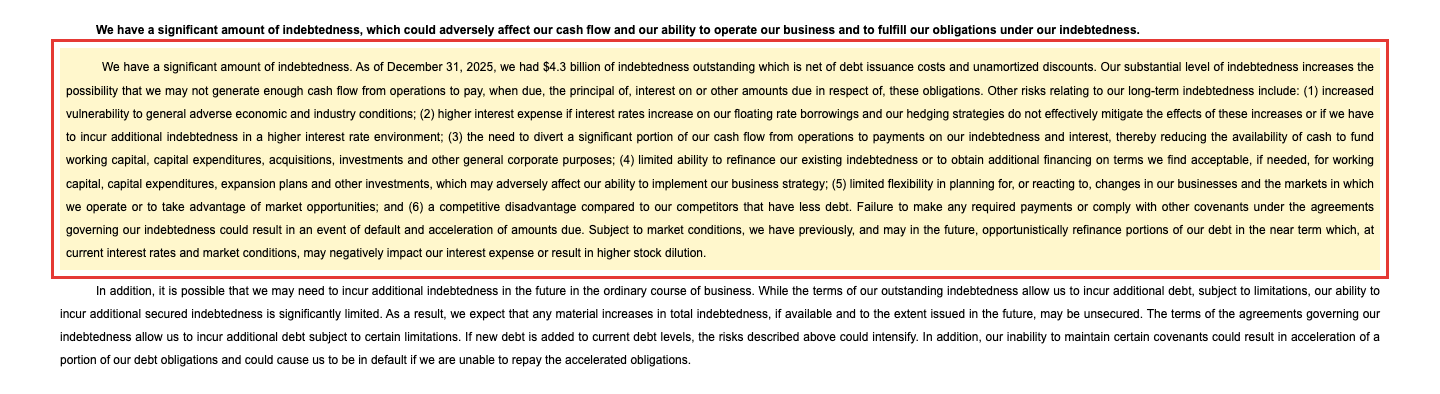

Sabre's mountain of debt has a history: the 2014 IPO itself was the legacy of a leveraged buyout (in 2007, financial investors had taken the group private), and the pandemic piled on — hardly any flights, hardly any bookings, hardly any revenue, but a full interest bill. As of March 31, 2026, the par value of the debt stands at $4,438.8 million. The annual report (10-K) for 2025 describes the risk itself — it hardly gets more sober:

"We have a significant amount of indebtedness. As of December 31, 2025, we had $4.3 billion of indebtedness outstanding which is net of debt issuance costs and unamortized discounts. Our substantial level of indebtedness increases the possibility that we may not generate enough cash flow from operations to pay, when due, the principal of, interest on or other amounts due in respect of, these obligations."

— Sabre Corporation, SEC annual report 10-K 2025, Item 1A "Risk Factors"

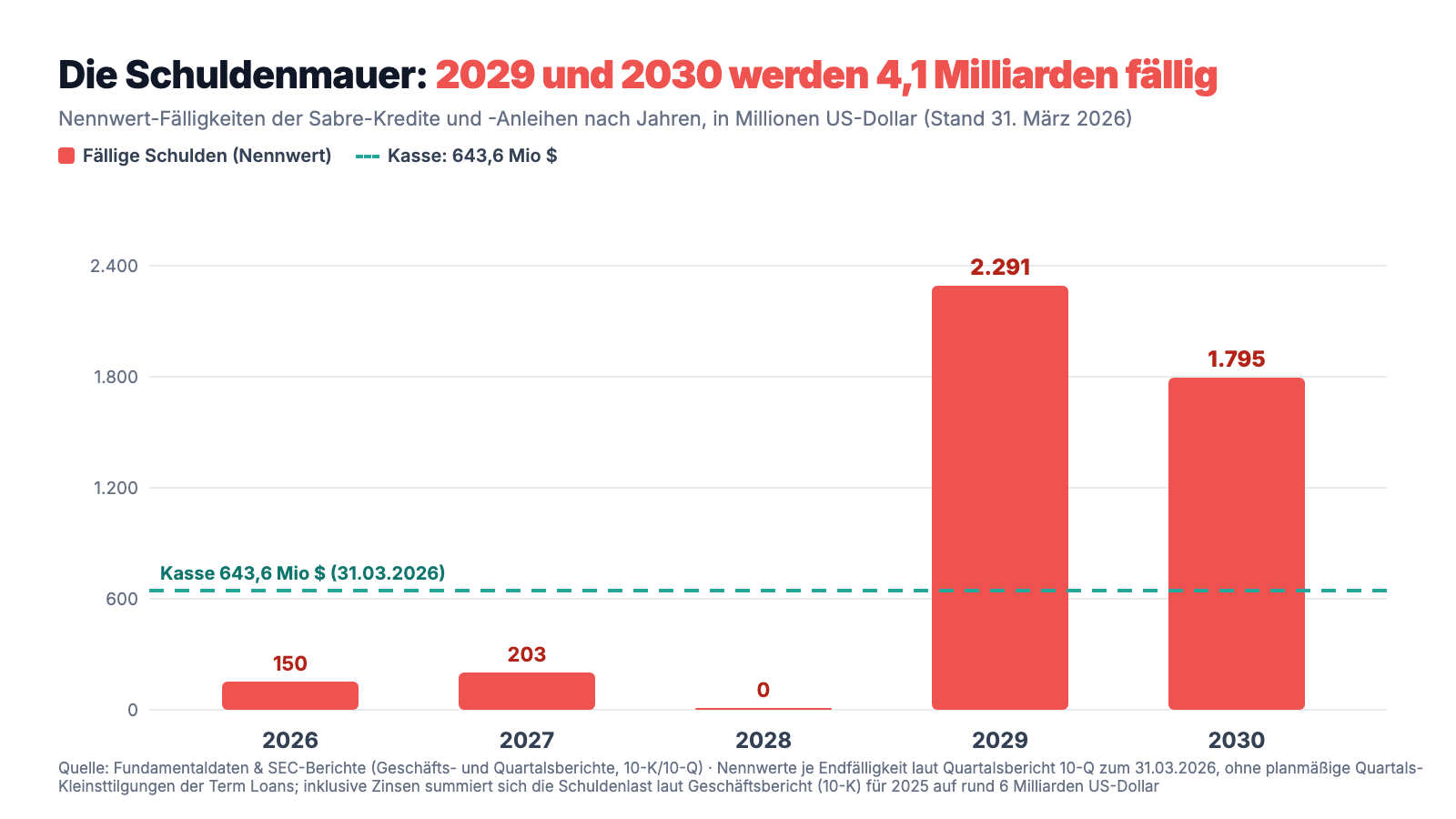

The devilish part is the price of this debt. In the 2024 and 2025 refinancings, Sabre had to accept terms otherwise known from junk bonds of the lowest category: $1,000 million at 11.125 percent (due June 2029), $1,325 million at 11.125 percent (July 2030), $469.8 million at 10.75 percent (March 2030), $445.7 million at 10.75 percent (November 2029) — plus term loans at SOFR plus 6.0 to 6.25 percentage points and a receivables credit facility whose FILO tranche costs SOFR plus 8 percent. The annual report calculates that the debt load including all interest adds up to about $6 billion. And the maturities cluster:

Honesty requires adding: there is no going-concern note, the auditor signed off without qualification, and there is time before the wall — in 2026 only a $150 million convertible bond comes due (7.32 percent, August 2026), in 2027 $203 million of the receivables facilities expire, 2028 is free. But you should have understood the mechanics behind it: with the double-digit coupons, Sabre has bought time, not solved problems. Every postponement raises the annual interest bill — the report itself names, as a consequence of the 2024/2025 refinancings, higher interest rates than in prior years that increase current and future interest expense. For the math to work out in 2029, operating income must grow well past the interest burden by then — or the capital market must be willing to lend Sabre money at normal terms again by then.

Uncomfortable truth no. 2: the 2025 "profit" came from selling the family silver — and equity still remains a billion below zero

Anyone who in 2025 looked only at the headline "Sabre is back in the black" (group result: plus $531.7 million) missed the footnote: continuing operations lost $255.5 million. The difference stems almost entirely from a single event:

"On April 27, 2025, we entered into a definitive agreement with an affiliate of TPG (the “Buyer”) pursuant to which the Buyer agreed to purchase our Hospitality Solutions business, an extensive suite of leading software solutions for hoteliers. On July 3, 2025, we closed the transaction (the “Hospitality Solutions Sale”), resulting in cash proceeds of $965 million, net, which was used primarily to repay our outstanding indebtedness."

— Sabre Corporation, SEC annual report 10-K 2025, Item 7 MD&A "Sale of Hospitality Solutions Business"

The sale produced a book gain of $822 million pre-tax ($724 million after tax) — it alone flipped the annual result. From a business standpoint it was consistent: $299 million flowed, per the agreement, straight into repaying a term loan, further notes were bought back, and the par value of the debt fell within one year from $5,220.9 to $4,532.0 million. But be honest in the framing: a gain on a sale is not earned profit — it is moving assets from the future into the present. Sabre gave up a growing software business to service debt, and there is no second hotel business to sell. How deep the hole still is despite everything is shown by the equity line of the balance sheet: minus $1,036.5 million as of December 31, 2025 (after minus $1,604.7 million at the end of 2024), with $3,802.5 million in accumulated losses since the company's existence. Translated: if Sabre sold all its assets at book values today and repaid all its debt, not only would nothing be left for shareholders — a billion would still be missing. The stock price therefore prices exclusively the future, not the substance.

Uncomfortable truth no. 3: operating cash flow is negative — despite $500 million of "adjusted EBITDA"

Now it gets uncomfortable for the turnaround narrative. In presentations, Sabre shines with adjusted EBITDA of $500.2 million (2025). But "adjusted" means: before everything unpleasant — above all, before the interest. In the cash flow statement, where nothing can be adjusted away, 2025 shows operating cash flow of minus $108.9 million (2024: plus $70.2 million) — and the first quarter of 2026 minus $134.2 million, after minus $64.0 million in the prior-year quarter. Cash shrank accordingly from $791.6 million (December 31, 2025) to $643.6 million (March 31, 2026); the receivables credit facility is fully drawn at $83.1 million, freely available beneath it: zero. Management phrases its confidence in the annual report like this — with a remarkable subordinate clause:

"We believe that we have resources to sufficiently fund our liquidity requirements over at least the next twelve months, including the aggregate payment of approximately $248 million of principal due or committed to be redeemed early under our current debt facilities; however, given the uncertain economic environment and the leveling off of industry air distribution volume growth, we will continue to monitor our liquidity levels and take additional steps should we determine they are necessary."

— Sabre Corporation, SEC annual report 10-K 2025, Item 7 MD&A "Travel Industry and Liquidity Outlook"

Why is cash flow negative when the business earns $295.5 million operationally? Because the interest has to be paid in cash — and because the business has peculiarities that tie up cash: Sabre pays travel agencies incentive payments ("subscriber incentives"; at the end of 2025, $289.1 million in accrued incentives sat on the balance sheet) so that they book through its network. Bookings growth has also become thin: 365.3 million (2025) against 363.2 million (2024) — plus 0.6 percent —, and passengers boarded in the software business suffered from de-migrations: airlines that have left Sabre's systems. In short: the network is stable, but it is no longer a growth engine that could pump against a $448 million interest bill on its own. A quarter with plus 8 percent revenue (Q1 2026) is a good sign — but one quarter does not make a deleveraging.

Uncomfortable truth no. 4: "AI-native" stands at the front of the report — at the back it says others could be faster

That leaves the AI story, the promise of the future. Sabre opens its latest quarterly report with a self-image that could hardly be more confident: "Sabre is an AI-native technology leader, backed by one of the world's largest travel data clouds." The substance behind it we described above: SabreMosaic, machine-learning booking systems, chatbots, agentic interfaces for external AI assistants, and since February 2026 a product executive with explicit responsibility for agentic AI. That is real — and at the same time it is a race whose outcome the company's own annual report names remarkably openly:

"Our competitors or other third parties may incorporate AI into their products more quickly or more successfully than we do, which could impair our ability to compete effectively and adversely affect our results of operations."

— Sabre Corporation, SEC annual report 10-K 2025, Item 1A "Risk Factors"

Two things you should keep apart here. First, the opportunity: if AI assistants book trips on their own in the future, they will need exactly what Sabre has — a machine-readable marketplace with inventory, prices and booking processing. The agentic interfaces are the attempt to make the travel market's switchboard indispensable for AI callers too. Second, the risk, and it is twofold: the risk factors concede that the generative AI in Sabre's products is bought in from third parties — with all the follow-on risks, up to and including hallucinating behavior, meaning freely invented results. And the AI-drivenness of the industry can turn against any middleman: if airlines and AI assistants one day talk to each other directly, the switchboard becomes a bypass road. A group with $4.4 billion of debt and negative cash flow has the shortest breath in that race — which is exactly what the report means when it lists, as debt consequence number six, a competitive disadvantage against competitors with less debt. Incidentally, the market of professionals has just voted on this, in both directions: in March 2026, Constellation Software — arguably the most successful software acquirer in the world — reported, via Schedule 13D, a Sabre stake of more than 5 percent and, after a brief defensive fight (poison pill included), secured the appointment of a new director to the board, against a standstill commitment capped at 15 percent. At the same time, major shareholder Vanguard most recently reported a position reduced by 17.8 percent. The professionals are split — like our scanners.

Valuation: a $0.77 billion market value — but whoever buys it all pays six times that

In early July 2026 the Sabre stock cost about $1.90; at about 395 million shares that makes a market value of about $0.77 billion (data as of July 8, 2026). Measured against the revenue of the last four quarters, that is a price-to-sales ratio of about 0.27 — optically almost a giveaway for a group with this market position. But this is where the cursory glance takes its revenge: a price-to-earnings ratio does not exist for lack of sustainable earnings, a price-to-book ratio is meaningless with negative equity — and the most honest calculation runs through the enterprise value (market value plus debt minus cash). Anyone who wanted to take over Sabre completely would get the shares for $0.77 billion but assume $4,438.8 million of debt minus $643.6 million of cash: together about $4.6 billion — six times the market value. Put differently: about five sixths of this company already belong, economically, to the creditors; the stock is the thin residual lever on top. That is exactly why it moves so violently: about plus 47 percent in six months, minus 31 percent over twelve months, on average around 7 percent of daily swing — and still about 86 percent below the high from the years after the 2014 IPO (all values: data as of July 8, 2026). With leveraged instruments like this, the rule is: small changes in the interest or business outlook, large price swings — in both directions.

Opportunities and risks at a glance

What speaks for Sabre:

- Indispensable infrastructure with a network effect: one of only three big global distribution systems, 365.3 million billable bookings and 695.4 million passengers boarded in 2025, transaction-based recurring revenue (annual report 10-K for 2025).

- A genuine operating turnaround: operating income lifted from $32.2 to $295.5 million (2023 to 2025), technology costs cut by $240 million, adjusted EBITDA up from $289.5 to $500.2 million; plus 8 percent revenue and plus 5 percent bookings in the first quarter of 2026.

- Deleveraging has begun: debt par value cut within five quarters from $5,220.9 to $4,438.8 million (thanks also to the Hospitality sale), no meaningful maturities before 2029, $643.6 million of cash (March 31, 2026).

- An AI story with substance: the SabreMosaic platform, machine-learning booking systems, agentic interfaces for external AI assistants — if AI agents book trips, machine-readable marketplaces like Sabre's are needed.

- The smart money is watching: roughly 90 percent professional ownership, and Constellation Software — a legendarily disciplined software house — reported more than 5 percent in March 2026 (Schedule 13D) and secured a new seat on the board of directors (standstill cap: 15 percent).

What speaks against it:

- The interest burden has exceeded operating income in every year since 2023 (2025: $447.8 against $295.5 million; Q1 2026: $123.0 against $115.9) — all of the operating progress currently flows to the creditors.

- $4,438.8 million of debt at par (March 31, 2026) at coupons up to 11.25 percent, about $6 billion of total load including interest, a debt wall of about $4.1 billion in 2029/2030 — refinancing at bearable terms is the existential question.

- Equity of minus $1,036.5 million, $3,802.5 million in accumulated losses; the 2025 group profit stems solely from the $822 million gain on the sale of the hotel business — there is no second piece of family silver.

- Operating cash flow negative (2025: −$108.9 million; Q1 2026: −$134.2 million), cash down $148 million in the quarter, the receivables credit facility fully drawn; bookings growth of only 0.6 percent (2025), passenger counts weighed down by airline migrations away.

- AI cuts both ways: the generative AI in Sabre's products comes from third parties (hallucination risk included, per the risk factors), competitors could be faster — and direct connections between airlines and AI assistants could bypass the middleman in the long run; early-warning systems: Altman Z around zero, Piotroski 4 of 9, five distress flags (data as of July 8, 2026).

A human conclusion

Back to the indispensability illusion from the beginning. It has a true core: Sabre's network is something like infrastructure, and infrastructure rarely disappears. But precisely here sits the thinking error this case can show you: that a network survives does not mean its shareholders do. A company with negative equity and a 2029 debt wall can keep operating its systems every single day — including after a restructuring in which the creditors take over the firm and the old shares are worth almost nothing. The bookings would simply keep flowing; only the owners' address would have changed. That is why Sabre is not a case for a gut feeling but for a sober bet with clear conditions: the operating turnaround is real, the AI interfaces are a genuine future asset, and if earnings grow faster than the interest burden, the same mass of debt levers the thin market value upward — the 47 percent in six months hinted at it, and an investor of Constellation's caliber evidently considers the scenario possible. If not, about $2.3 billion come up for refinancing in 2029, at coupons that are already double-digit today. Both stand in the same report, only a few pages apart. Whoever gets in here should do so because they have understood the bet — not because the company seems too familiar to fail. What you make of it is your decision. And that is exactly as it should be.

Sources

All original documents used in this analysis — to read for yourself:

- Sabre Corporation — SEC annual report 10-K for 2025 (filed February 18, 2026)

- Sabre Corporation — SEC annual report 10-K for 2024 (filed February 20, 2025)

- Sabre Corporation — SEC quarterly report 10-Q as of March 31, 2026 (filed May 7, 2026)

- Sabre Corporation — SEC quarterly report 10-Q as of September 30, 2025 (filed November 5, 2025)

- Sabre Corporation — SEC quarterly report 10-Q as of June 30, 2025 (filed August 7, 2025)

- Sabre Corporation — SEC quarterly report 10-Q as of March 31, 2025 (filed May 7, 2025)

- Sabre Corporation — Form 8-K of March 2, 2026 (Rights Agreement / "poison pill")

- Sabre Corporation — Form 8-K of March 5, 2026 (Strategic Governance Agreement with Constellation Software)

- Sabre's complete SEC filing history: EDGAR overview (sec.gov)

- Fundamental data (metrics, quarterly series, valuation; data as of July 8, 2026), reconciled with the SEC filings.

- Screener and rating data: in-house stock scanner (data as of July 8, 2026).

Transparency & disclaimer: This analysis is a journalistic contextualization of publicly available information and is not investment advice, not a financial analysis in the regulatory sense, and not a solicitation to buy or sell securities. It expressly contains no judgment on whether an insolvency will occur. Stock investments carry substantial risks up to total loss. All information without guarantee; the data cut-off is noted in the text in each case. The author holds no position in Sabre stock at the time of publication.

Our Bottom Line at a Glance

- Market position & network positive

- One of three big global distribution systems (GDS) with a genuine network effect: 365.3 million billable bookings and 695.4 million passengers boarded in 2025, transaction-based recurring revenue, 58 percent of bookings in North America (annual report 10-K for 2025).

- Operating turnaround neutral

- Operating income rose from $32.2 million (2023) to $295.5 million (2025), technology costs fell by about $240 million, and the first quarter of 2026 brought +8 percent revenue. But bookings growth stood at just 0.6 percent in 2025, and so far all of the progress flows into the interest bill.

- Debt & interest burden negative

- $4,438.8 million at par (March 31, 2026) at coupons up to 11.25 percent; net interest expense (2025: $447.8 million) has exceeded operating income in every year since 2023; about $4.1 billion come due in 2029/2030. The 10-K itself warns that operating cash flow may not suffice for principal and interest.

- Equity & cash flow negative

- Equity of minus $1,036.5 million (December 31, 2025), operating cash flow of minus $108.9 million in 2025 and minus $134.2 million in the first quarter of 2026; the 2025 group profit stems solely from the $822 million gain on the hotel business sold to TPG — a non-repeatable one-off effect.

- AI story & owner signals neutral

- Real AI products (SabreMosaic, agentic interfaces, machine-learning booking systems) meet honest risk-factor warnings: third-party AI with hallucination risk, competitors could be faster. Constellation Software reported more than 5 percent in March 2026 and secured a new board seat (standstill cap: 15 percent) — while Vanguard most recently reduced its position by 17.8 percent.

Sabre is the opposite of an empty shell: an indispensable booking network with a genuine operating turnaround and an AI story that is more than a label. But the balance sheet tells the second half: $4.4 billion of debt at double-digit coupons, an interest burden above the entire operating income, negative equity, negative operating cash flow — and a 2025 profit that stems solely from the sale of the hotel business. The stock is the thin residual lever on a company that economically belongs five sixths to its creditors. Not investment advice.

What Our Rating Means

- If you don't own the stock

- In our view, the documented risks clearly outweigh — we see no basis for an entry.

- If you hold it in your portfolio

- In our view, the findings carry enough weight to warrant a critical look at your own position.

A journalistic assessment by our editorial team at the time of the deep dive, based on public sources — not investment advice and not a solicitation to buy or sell. Your personal circumstances (investment goals, risk capacity, taxes) cannot be taken into account. What our categories mean, how verdicts are formed, and what conflicts of interest exist →

Worth Noting

- Unless noted otherwise, all earnings figures in the article refer to continuing operations (excluding the Hospitality Solutions business sold in July 2025, which is reported as discontinued operations).

- The debt-wall chart shows par values by final maturity per the quarterly report 10-Q as of March 31, 2026; scheduled small quarterly amortizations of the term loans (0.25 percent per quarter) are not shown separately in it.

- Price and valuation figures are dated July 8, 2026 (about $1.90, about 395 million shares); analyses are evergreen, daily prices are not a buy argument.

Frequently Asked Questions

Sabre (NASDAQ: SABR) of Southlake, Texas, operates one of the three big global travel booking networks (GDS): it connects airlines, hotels and car-rental firms with travel agencies and booking portals and collects a fee per booking — 365.3 million of them in 2025. On top, Sabre sells airline software (reservations, network planning) as SaaS. In 2025, continuing operations generated $2,771.0 million in revenue.

As of March 31, 2026, $4,438.8 million of debt at par value stood on the books, at interest rates of 7.32 to 11.25 percent; including interest, the annual report (10-K) puts the total load at about $6 billion. Net interest expense in 2025 was $447.8 million — more than the operating income of $295.5 million. In 2029 and 2030 combined, about $4.1 billion come due, against $643.6 million of cash.

Because since the debt-financed buyout of 2007 and through the pandemic years, $3,802.5 million in losses have piled up: as of December 31, 2025, equity stood at minus $1,036.5 million. Total assets of $4,502.1 million are arithmetically not enough to cover all liabilities — so the stock price prices solely the future of the business, not its substance.

Only on the paper of the consolidated accounts: the plus of $531.7 million stems from the gain of $822 million (pre-tax) on the hotel-software business sold to a TPG fund in July 2025. Continuing operations lost $255.5 million, and operating cash flow came in at minus $108.9 million. A gain on a sale is a one-off effect — and there is no second hotel business.

Sabre does sell genuinely AI-enabled products: the airline platform SabreMosaic, machine-learning booking systems, chatbots and agentic interfaces through which external AI assistants can book directly; the quarterly report calls Sabre an "AI-native technology leader". At the same time, its own risk factors warn that competitors could integrate AI faster, and the generative AI comes from third parties. Opportunity and threat stand in the same report.

The Canadian software acquirer built up a Sabre position in early 2026 and submitted a director nomination. Sabre answered on March 1, 2026 with a "poison pill" (rights agreement, 15 percent threshold) — and made peace on March 5: Damian McKay, appointed as part of the agreement, joined the board of directors, Constellation accepted a standstill cap of 15 percent, and the poison pill was buried on March 6 (Form 8-K of March 2 and 5, 2026).

This analysis expressly passes no insolvency judgment. The facts: there is no going-concern note, cash covers the needs for at least twelve months per management, and only $353 million come due before 2029. At the same time, our early-warning systems report five distress signals, the Altman Z-Score sits around zero, and refinancing the 2029/2030 wall of about $4.1 billion is the open existential question.

Found an error?

Did you spot a factual error, an outdated number, or a typo in this deep dive? Let us know briefly — your report goes straight to the editorial team.