Fortrea Stock: The Labcorp Spin-Off With the Costly Dowry — $798 Million of Goodwill Written Off, $7.7 Billion of Orders on the Books

On June 30, 2023, the lab-diagnostics group Labcorp sent its clinical-trials business to the stock exchange as Fortrea — with 30 years of Covance history, 14,300 employees and a dowry of $1.64 billion in debt plus goodwill from old acquisitions. Two and a half years later the stock sits in our going-concern warning scanner. We read the annual report (10-K) for 2025 and the quarterly report (10-Q) as of March 31, 2026: $797.9 million of goodwill written off, a $986.2 million annual loss, loosened credit covenants, $300 million of receivables sold, one customer at 18.1 percent of revenue — and at the same time an order book above $7.8 billion and a nearly break-even first quarter of 2026. Not investment advice — just the question of what a fine pedigree is worth when the debts ride along in the moving boxes.

Among investors there is an article of faith that has been handed down for decades: spin-offs beat the market. When a large corporation spins off a subsidiary, so goes the legend, hidden value is unlocked — whole books have been written about it. Let's call the reflex behind it the pedigree bonus: the quiet trust that a company from a good family will surely be solid. Hardly any case feeds this reflex as well as Fortrea Holdings (NASDAQ: FTRE): 30 years of experience in contract research, first under the respected name Covance, then as the clinical-trials arm of the lab-diagnostics giant Labcorp, independent on the stock exchange since June 30, 2023. Add 14,300 employees, orders worth $7.7 billion — and a share price that has more than quadrupled from its 2025 low. Good family, cheaply valued, on the way up: sounds like the spin-off fairy tale straight from the textbook. Except the same stock sits in our warning scanner "Going Concern (Distress Proxy)", among companies with serious balance-sheet worries. So let's make a deal: before you believe the pedigree bonus, we read together what Fortrea itself reported to the U.S. securities regulator, the SEC — in the annual report (10-K) for 2025 and the quarterly report (10-Q) as of March 31, 2026. An SEC filing is honest under penalty of law. And there it says what the fine family really packed for its daughter: a dowry of $1.64 billion in debt and a mountain of goodwill, of which almost $800 million was written off in 2025. In the end, you decide for yourself.

What Fortrea actually does

Picture a pharmaceutical company with a new compound — and now comes the most expensive, slowest, most tightly regulated part: proving in humans that the drug works and does no harm. That is exactly what CROs ("contract research organizations") exist for — the general contractors of drug development. Fortrea plans and runs clinical trials from Phase I (first tolerability tests, often on healthy volunteers in company-owned trial clinics — the segment is called "Clinical Pharmacology") through Phase IV (post-approval monitoring): finding trial sites, recruiting patients, collecting data, feeding regulatory dossiers — in about 100 countries, across more than 20 therapeutic areas. Payment comes through long-running contracts stretching over years; what has been won but not yet worked through accumulates in the order backlog: $7.7 billion as of December 31, 2025, $7.8 billion as of March 31, 2026. The customers are pharma and biotech companies as well as medical-device firms; on offer is either the full package ("full service") or the staff-leasing model ("functional service provider", FSP), in which Fortrea teams work directly inside the customer's processes.

The truth includes the backstory, because it explains almost everything about this case: Fortrea was not founded — it was spun off. On June 30, 2023, Labcorp distributed the shares of its clinical-trials arm to its own shareholders; the stock has traded on the Nasdaq since July 3, 2023. Into independence the daughter took two things: $1,640 million in freshly borrowed debt — the proceeds of which largely flowed to the parent — and the goodwill from Labcorp's 2015 Covance acquisition, a balance-sheet item of most recently $1.7 billion. Remember the central tension of this analysis: a real, globally sought-after business with a bulging order book — carried by a balance sheet that bears debt and acquisition legacies as its dowry and felt both painfully in 2025. It runs through every chapter. One more detail: the third leg, "Enabling Services" (patient-access and trial software), was sold back in the second quarter of 2024 for a final $340 million to the financial investor Arsenal Capital — at a $19.6 million book loss. What it looks like when a company can only service its interest bill by selling the silverware is something we analyzed at Sabre — Fortrea is not there (yet), but the direction of the questions is the same.

Where the stock shows up in our scanner

Every day we run about 3,500 stocks through our scanners. Fortrea sits in the warning scanner "Going Concern (Distress Proxy)" — we cross-checked the membership live on the platform on July 14, 2026. "Going concern" is the technical term for a company's ability to continue operating; our scanner is a proxy, an approximation built from balance-sheet metrics — expressly not an auditor's verdict. What the metrics (data as of July 8, 2026) report: the Altman Z-Score, a classic insolvency early warning built from several balance-sheet ratios, stands at 0.78 — the historical danger zone begins below 1.1. The Piotroski F-Score, a nine-point test of balance-sheet quality, stands at 4 of 9 — okay, not good; a thoroughly healthy company scores 8 or 9. Interest coverage is negative at about minus 4: the earnings of the last four quarters were not even arithmetically enough to earn the interest — they were deep in the red themselves. Four distress flags in total, fundamental rating D. How to read such warning lists — a smoke detector, not a demolition notice — is explained in our article "Insolvency Radar: the Top 10".

And now the other side of the same scanner picture, because it is at least as loud: Fortrea shows up at the same time in three valuation rankings — in the P/S ranking with a price-to-sales ratio of about 0.6 (the market pays a good 50 cents for a dollar of annual revenue), plus in the rankings by price to cash flow (about 7) and price to free cash flow (about 8). The Weinstein phase analysis puts the stock in Stage 2, the advancing phase; the price trades above the 50- and the 200-day lines and has gained 93 percent in three months (all values: data as of July 8, 2026). The look back puts that in context: in June 2025 the stock at times cost less than $5 — it has more than quadrupled from its 52-week low, yet still trades about 58 percent below its high from the period just after the spin-off; over six months the price has on balance barely moved. This side-by-side — distress metrics from the catastrophe year 2025, momentum from the present, a cheap-looking price — is the typical fingerprint of a stock in which the market is playing a comeback bet whose proof is still outstanding. Exactly the right address for the pedigree bonus. And exactly why the filings are worth reading.

The numbers over the years — honestly appraised

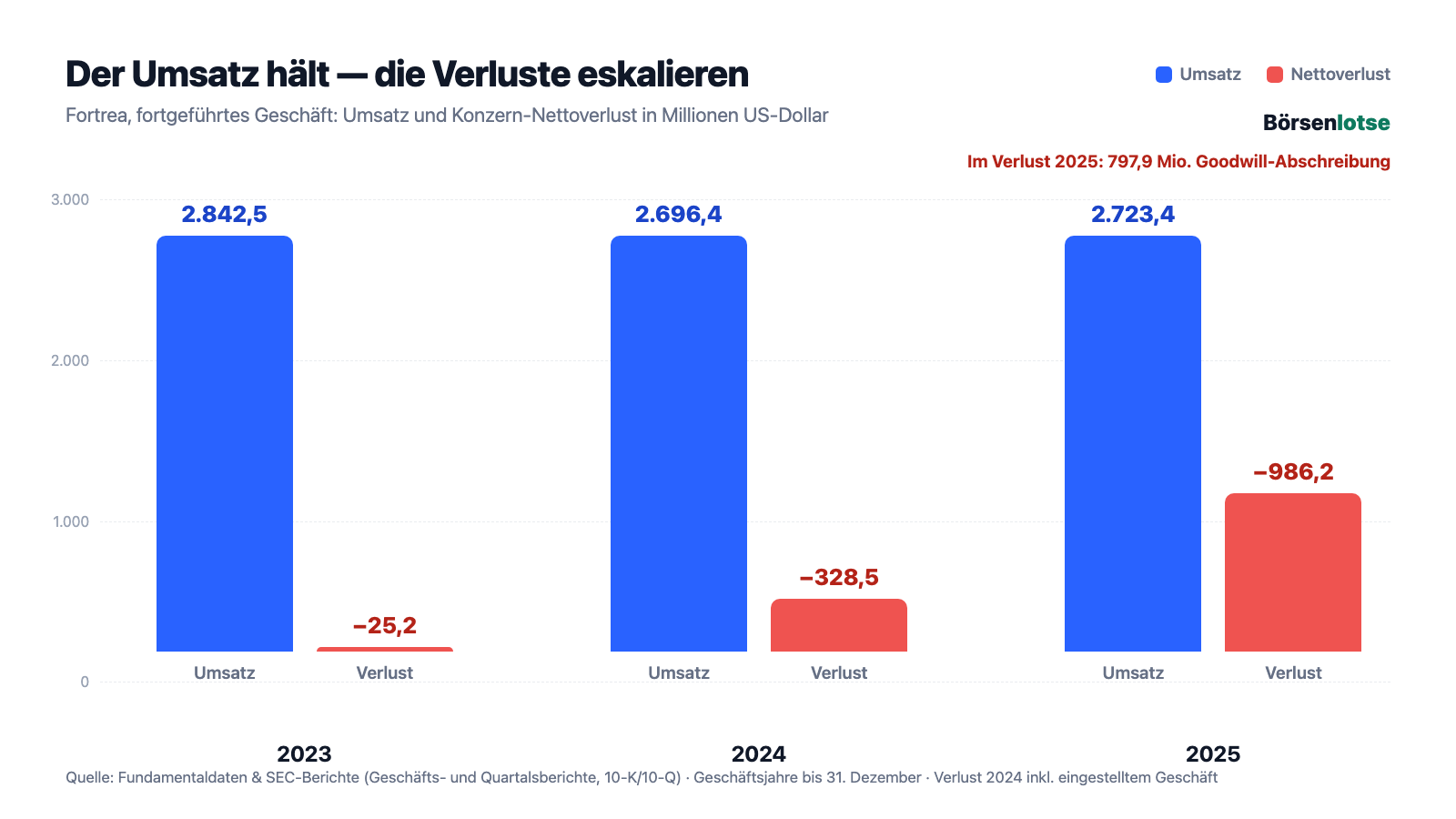

First, what genuinely has substance — and at Fortrea that is more than the warning scanner suggests. Revenue is remarkably stable: $2,842.5 million (2023), $2,696.4 million (2024), $2,723.4 million (2025) — no growth miracle, but no crash either, carried by an order backlog that grew to $7.8 billion as of March 31, 2026. On cost-cutting, management has visibly delivered: selling, general and administrative expenses fell 18.6 percent in 2025 to $456.4 million — mainly because the expensive transition services from the ex-parent (after the spin-off, Labcorp provided IT and administration for a fee) ran out — and fell another 17.5 percent in the first quarter of 2026. The restructuring ($44.1 million of expense in 2025 after $50.1 million in 2024) is showing effect: in the first quarter of 2026 the operating loss was only $3.4 million — after $520.1 million in the prior-year quarter, which admittedly contained a goodwill impairment. Operating cash flow stayed positive in 2025 at $113.5 million (2024: $262.8 million — flattered by the first-time sale of receivables, more on that shortly). That is one half of the truth. The other stands in the same report:

The bottom line for 2025 was a net loss of $986.2 million — minus $10.81 per share — after a $328.5 million loss in 2024 and $25.2 million in 2023. The lion's share is the goodwill impairment of $797.9 million, a book loss with no cash outflow. But beware the reflex of simply backing it out: even without the impairment, 2025 would have ended with an operating loss of about $75 million, plus $91.4 million in interest and $26.9 million in currency losses. A business with $2.7 billion in revenue that earns no money after interest — that is the condition the warning scanner measures. And three side notes from the same year belong in the picture: on June 2, 2025 a shareholder class action was filed (the allegation: misrepresentations toward investors; Fortrea considers the suit unfounded and moved to dismiss in January 2026), on June 11, 2025 the board installed a poison pill with a 10 percent threshold, and in August 2025 a new chief executive, Anshul Thakral, took over (his employment agreement in the annual report is dated August 4, 2025). Remember the sentence: at Fortrea, 2025 was not one bad quarter — it was a year in which the balance sheet, the courtroom and the executive floor all moved at once. Which brings us to the uncomfortable truths.

What the filings say — the uncomfortable truths

Uncomfortable truth no. 1: $797.9 million of goodwill gone — written off because the company's own share price collapsed

Goodwill is the premium a buyer pays in an acquisition beyond the substance value — it then sits on the balance sheet as an intangible "firm value" and must be tested regularly for impairment. Fortrea's goodwill stems at its core from Labcorp's 2015 Covance acquisition; the daughter had it placed in her books as a dowry at the spin-off: most recently $1,710.4 million. In 2025 this item broke against reality — and the trigger is remarkable:

"During the first and second quarters of 2025, due to sustained declines in the Company's share price and uncertainties in global macroeconomic conditions, the Company determined that indicators of impairment existed. […] Based upon the results of the quantitative assessment as of March 31, 2025, the Company concluded that the fair value of the Clinical Development reporting unit was less than its carrying value and recorded a goodwill impairment of $488.8."

— Fortrea Holdings, SEC annual report 10-K 2025, Note 10 "Goodwill and Intangible Assets"

Read the trigger twice, calmly: the sustained decline of the company's own share price. In an impairment test, the computed firm value has to be reconciled with the market valuation — and when Fortrea was valued at only $4.94 per share as of June 30, 2025 (March 31: $7.55), the carrying value could no longer be justified. In two installments ($488.8 plus $309.1 million), $797.9 million was written off — almost half the item. The consequences: equity halved within one year from $1,362.4 to $563.5 million, and the accumulated deficit grew to $1,383.2 million. And one uncomfortable observation remains: even after the impairment, $960.0 million of goodwill still sits on the balance sheet — more than total equity. The report itself warns that further impairments are possible should new orders fail to come in or customers cancel. Honesty requires adding: the annual test in October 2025 found no further impairment need, and a book loss costs no liquidity. But it tells you what the examiners think of the dowry's earning power — and the answer of 2025 was: distinctly less than assumed.

Uncomfortable truth no. 2: a $1.1 billion debt dowry — and the credit covenants already had to be loosened

The second dowry is more tangible: debt. At the spin-off, Fortrea borrowed $1,640 million — not to invest, but as part of the separation agreement with the parent. The annual report describes the situation soberly:

"We have an aggregate principal amount of indebtedness of approximately $1,066.3 million, which consists of borrowings under senior secured term loan facilities and senior secured notes. […] Our level of debt could have important consequences. For example, it could: require us to dedicate a substantial portion of our cash flow from operations to the payment of debt service, reducing the availability of our cash flow to fund working capital, capital expenditures, acquisitions, and other general corporate purposes […]"

— Fortrea Holdings, SEC annual report 10-K 2025, Item 1A "Risk Factors"

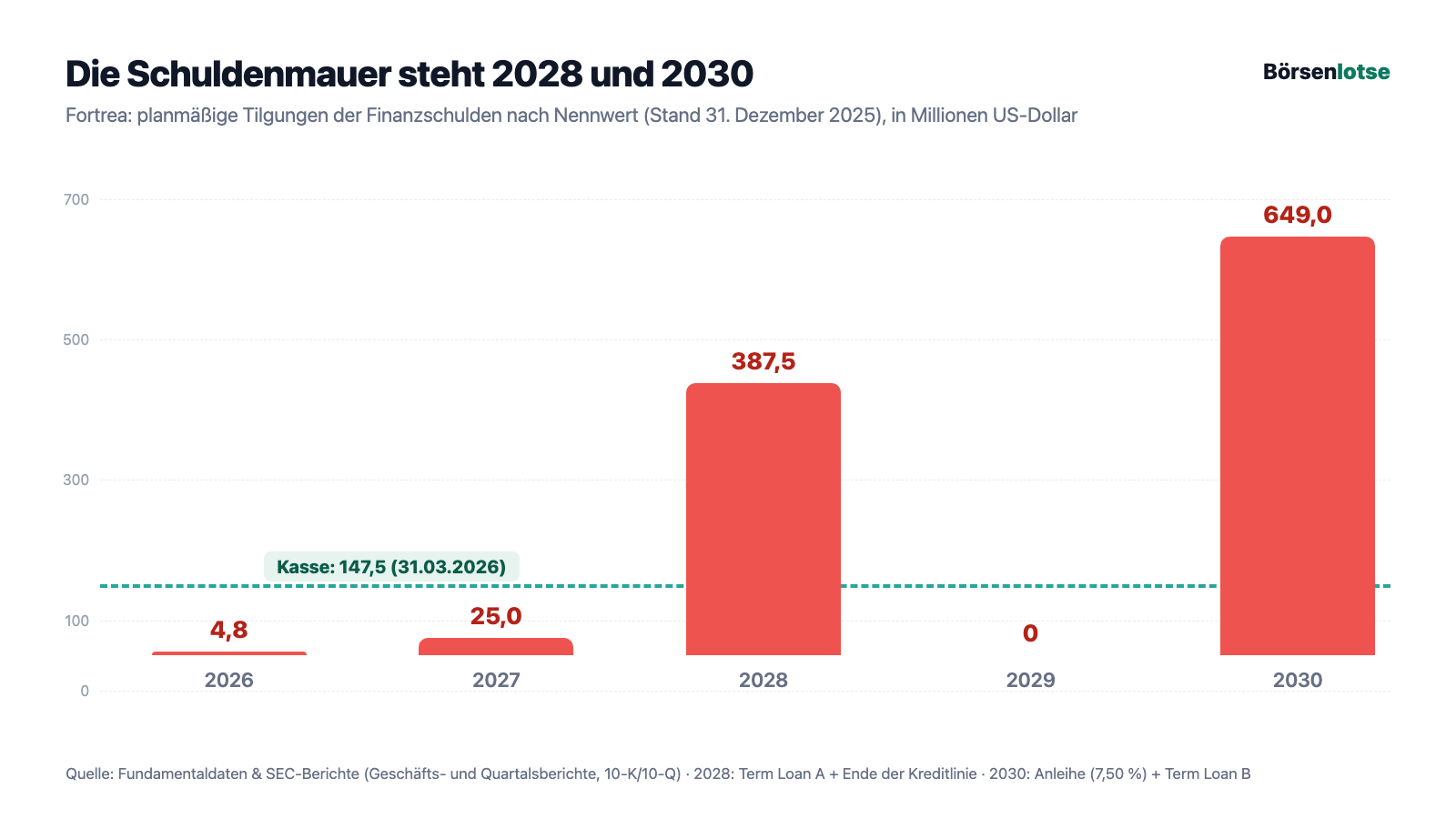

In detail: a $494.3 million note at 7.50 percent (due 2030; Fortrea had to repurchase $75.7 million of it early in 2025 because the note terms required it after the sale of the Enabling Services business), a Term Loan A of $412.5 million (due June 2028, effectively 5.72 percent) and a Term Loan B of $154.7 million (due June 2030, effectively 7.47 percent). In 2025 that cost $91.4 million in interest — money an operationally loss-making business first has to earn. And two sentences from Note 11 deserve special attention: first, Fortrea is required to maintain certain leverage and interest-coverage ratios ("covenants" — contractual loan conditions whose breach can trigger immediate repayment). Second: "On February 28, 2025, the Company entered into an amendment to modify certain financial covenants for additional flexibility" — in plain terms: on February 28, 2025 the conditions were loosened, "for additional flexibility". Banks do not grant additional flexibility out of sympathy, but when things could get tight without it. As of March 31, 2026, Fortrea was in compliance with all covenants and expects to remain so for the next twelve months. The maturities show what the time has to be enough for:

Honesty again requires both sides: there is no going-concern qualification, the auditor signed off without reservation, only about $30 million comes due in 2026 and 2027 combined, and the $450 million credit line was practically untouched at the balance-sheet date. But the 2028/2030 wall stands — and whether Fortrea works it off out of its own strength or has to refinance at whatever rates then apply will be decided by the question of whether the $7.8 billion order book turns back into reliable profit.

Uncomfortable truth no. 3: a single customer accounts for 18.1 percent of revenue — and the concentration is growing

The third truth concerns the customer base. Customer concentration is the technical term — translated: if your neighbor told you his workshop was doing great, but a single client provided almost a fifth of the income, you would swallow for a moment. Exactly that is written in Fortrea's risk chapter:

"For the year ended December 31, 2025, our top ten customers based on revenue accounted for approximately 57% of our consolidated revenue and our top ten customers based on backlog accounted for approximately 54% of our total backlog. For the year ended December 31, 2025, one customer accounted for approximately 18.1% of revenue."

— Fortrea Holdings, SEC annual report 10-K 2025, Item 1A "Risk Factors"

Three things make the number more explosive than it already sounds. First, the direction: the twenty largest customers accounted for 61 percent of revenue in 2023, 64 percent in 2024, 69 percent in 2025 — the dependence grows year after year. Second, the contract mechanics: per the report, most trial contracts can be terminated by the customer on short notice, typically 30 to 90 days — which also tempers the comfort of the thick order book, because Fortrea itself warns the backlog is "not a reliable indicator" of future revenue. Third, the market situation: the revenue decline in the first quarter of 2026 (minus 2.3 percent to $636.5 million) came, of all places, from the FSP business — the very model in which large customers flexibly order capacity up and down. What happens when a major customer gets truly serious is currently on display elsewhere in the industry; at a company whose largest customer arithmetically brings in about $490 million of annual revenue, any termination would be an earthquake. There is no indication that one is imminent — but it is the predetermined breaking point you have to know about.

Uncomfortable truth no. 4: the cash flow also lives on sold receivables — $300 million is already off the balance sheet

Which leaves the question of how much money the business really earns. The cash flow statement says: $113.5 million flowed in operationally in 2025, but $17.0 million flowed out again in the first quarter of 2026. And inside both numbers sits a tool you need to know — factoring, the sale of customer receivables for immediate cash:

"As of March 31, 2026, the Company had sold $300.0 of receivables, which were derecognized from the Company's consolidated balance sheet […] Total costs associated with the sale were $4.7 and $4.4 for the three months ended March 31, 2026 and 2025, respectively, and are included within selling, general and administrative costs in the condensed consolidated statements of operations."

— Fortrea Holdings, SEC quarterly report 10-Q as of March 31, 2026, Note "Accounts Receivable" / "Receivables Securitization Program"

Factoring is legal, widespread and, taken by itself, no alarm signal. But it shifts the optics: the cash balance of $147.5 million (March 31, 2026) looks more solid than it would be without the $300 million pulled forward; the strong 2024 operating cash flow was, per the annual report, driven largely by the first-time sale of receivables; and the tool costs real money — almost $19 million on an annual basis, booked inconspicuously in administrative expenses. Add a detail from the contract extension of February 24, 2026: it grants the administering bank special rights should one of two rating agencies downgrade Fortrea's creditworthiness. The intra-year rhythm also counsels sobriety: in 2025 Fortrea drew a cumulative $453.9 million from its credit line and repaid it — at the balance-sheet date it stood at zero. None of this is forbidden or hidden; it is all right there in the report. But remember: anyone who looks only at Fortrea's cash balance and point-in-time balance sheet is looking at a flattering still from a very fast-moving film.

Valuation: the market pays half a year of revenue — and has already advanced half the comeback

In early July 2026 the Fortrea stock cost about $17.70; at about 93 million shares that makes a market value of roughly $1.6 billion (data as of July 8, 2026). Against that stand $2,723.4 million in annual revenue — a price-to-sales ratio of about 0.6. For comparison: the peer group named in the annual report itself — ICON, IQVIA, Medpace, Charles River, Thermo Fisher — traditionally trades at a multiple of that; the discount is the price tag for losses, debt and concentration risk. A price-to-earnings ratio does not exist for lack of earnings; based on the adjusted earnings for 2026 expected by twelve analyst firms (about $0.81 per share, data as of July 8, 2026), the multiple would be a good twenty — so the comeback thesis is already half priced in: only the revenue is cheap here, not the hoped-for profit. Price to cash flow sits at about 7. And do not forget the drop height: the stock swings almost 7 percent a day on average, has more than quadrupled from its June 2025 low — and still trades about 58 percent below its high from the early post-spin-off period, as well as slightly down since the start of 2026 (all values: data as of July 8, 2026). This is not a sleep-well investment; it is a bet with a calendar attached: quarterly reports, covenant tests, the 2028 refinancing.

Opportunities and risks at a glance

What speaks for Fortrea:

- A real, global business with substance: $2,723.4 million in 2025 revenue, about 14,300 employees, trials in roughly 100 countries, more than 30 years of experience (Covance/Labcorp Drug Development) — and an order backlog of $7.8 billion as of March 31, 2026 (annual report 10-K for 2025, quarterly report 10-Q).

- The cost-cutting measurably bites: selling, general and administrative expenses minus 18.6 percent in 2025 and minus 17.5 percent in the first quarter of 2026; the operating loss shrank to $3.4 million in the first quarter of 2026 (prior-year quarter: $520.1 million including the impairment) — the threshold to operating profit is within sight.

- No going-concern qualification, an unqualified audit opinion, all credit covenants met as of March 31, 2026; only about $30 million of debt comes due through the end of 2027, and the $450 million credit line was untouched at the balance-sheet date.

- Cheap revenue optics with a tailwind: price-to-sales about 0.6, price to cash flow about 7, Weinstein Stage 2, plus 93 percent in three months (data as of July 8, 2026) — and the goodwill impairment is a book loss that cost no liquidity; the annual test in October 2025 found no further need.

- A fresh start: a new chief executive since August 2025 (Anshul Thakral), an ongoing restructuring, AI-supported tools for trial design and execution per the annual report — and a sector whose demand hangs on the growing research budgets of the pharmaceutical industry.

What speaks against it:

- The loss year 2025 in full breadth: a $986.2 million net loss (minus $10.81 per share), including a $797.9 million goodwill impairment — triggered by the company's own share-price collapse ($4.94 per share as of June 30, 2025); equity halved to $563.5 million, and at $960.0 million the remaining goodwill exceeds total equity.

- The debt dowry: about $1,066.3 million in principal at up to 7.50 percent, $91.4 million of interest expense in 2025 against an operating loss even before the impairment (about $75 million); the credit covenants were loosened on February 28, 2025 "for additional flexibility"; $387.5 million and $649.0 million come due in 2028 and 2030 respectively — against $147.5 million of cash.

- Concentration risk with a rising trend: one customer at 18.1 percent of revenue, top 10 = 57 percent, top 20 = 69 percent (2023: 61 percent); most contracts can be terminated on 30 to 90 days' notice, the report itself calls the backlog no reliable revenue indicator; revenue fell 2.3 percent in the first quarter of 2026.

- Cash flow with an auxiliary engine: operating inflow of only $113.5 million in 2025 (2024: $262.8 million, driven by the first-time receivables sale), minus $17.0 million in the first quarter of 2026; $300 million of receivables are sold and derecognized, the program costs about $19 million a year and has contained a rating trigger since February 2026.

- Legal and governance construction sites: a shareholder class action since June 2, 2025 (motion to dismiss January 2026, outcome open), a poison pill with a 10 percent threshold since June 11, 2025; early-warning systems: Altman Z 0.78, Piotroski 4 of 9, four distress flags, about 7 percent daily volatility (data as of July 8, 2026).

A human conclusion

Back to the pedigree bonus from the opening. It is not plucked out of thin air — behind Fortrea really do stand 30 years of craft, real customers, an order book that many companies in our warning scanner would beg for. But this case shows you what the pedigree bonus systematically overlooks: whoever comes from a good family brings along not only the name, but also whatever the family packs for the journey. Labcorp packed its daughter $1.64 billion of debt and the goodwill of a ten-year-old acquisition — in 2025 the first parcel cost the flexibility of the credit agreements, and the second cost almost $800 million of book value. Since then Fortrea has been visibly working to turn the dowry into a balance sheet of its own: costs down, a new boss, a first quarter of 2026 that was almost break-even operationally. The market has already advanced 93 percent in three months for it. Whether it turns out to be right will be decided by three sober questions: Does the $7.8 billion order book turn back into reliable profit before the first debt wall stands in 2028? Does the largest customer, carrying almost a fifth of revenue, hold still? And does it stay at loosened covenants — or does the next request for "additional flexibility" follow? The pedigree bonus whispers: "Good family, it'll be fine." The filings answer: the family gave the daughter the bills to take along, too. What you make of it is your decision. And that is exactly as it should be.

Sources

All original documents used in this analysis — to read for yourself:

- Fortrea Holdings Inc. — SEC annual report 10-K for 2025 (filed February 26, 2026)

- Fortrea Holdings Inc. — SEC quarterly report 10-Q as of March 31, 2026 (filed May 5, 2026)

- Fortrea Holdings Inc. — SEC annual report 10-K for 2024 (filed March 3, 2025)

- Fortrea Holdings Inc. — SEC quarterly report 10-Q as of September 30, 2025, 10-Q as of June 30, 2025 and 10-Q as of March 31, 2025

- Fortrea's complete SEC filing history: EDGAR overview (sec.gov)

- Fundamental data (metrics, price history, valuation, shareholder structure; data as of July 8, 2026), reconciled with the SEC filings.

- Screener and rating data: in-house stock scanner (data as of July 8, 2026; scanner membership verified live on July 14, 2026).

Transparency & disclaimer: This analysis is a journalistic contextualization of publicly available information and is not investment advice, not a financial analysis in the regulatory sense, and not a solicitation to buy or sell securities. It expressly contains no judgment on whether an insolvency will occur. Stock investments carry substantial risks up to total loss. All information without guarantee; the data cut-off is noted in the text in each case. The author holds no position in Fortrea stock at the time of publication.

Our Bottom Line at a Glance

- Business model & order book positive

- An established, global CRO business with more than 30 years of history, about 14,300 employees and an order backlog of $7.8 billion (March 31, 2026) — revenue stayed remarkably stable from 2023 through 2025 at $2.7 to $2.8 billion. The report's own caveat: the backlog is not a reliable revenue indicator, and most contracts can be terminated on 30 to 90 days' notice.

- Turnaround progress positive

- The cost-cutting works: administrative expenses minus 18.6 percent (2025) and minus 17.5 percent (Q1 2026), an operating loss of only $3.4 million in the first quarter of 2026 after $520.1 million in the prior-year quarter; a new CEO since August 2025. The threshold to operating profit is reachable — it is not yet proven.

- Balance sheet & goodwill negative

- A $797.9 million goodwill impairment in 2025 (trigger: the company's own share-price slide to $4.94), a net loss of $986.2 million, equity halved from $1,362.4 to $563.5 million — and the remaining goodwill ($960.0 million) exceeds total equity. The report itself warns of possible further impairments.

- Debt & liquidity negative

- About $1,066.3 million in principal debt as the spin-off dowry, $91.4 million of interest in 2025 against an operating loss even before the impairment; credit covenants loosened on February 28, 2025 "for additional flexibility"; maturities of $387.5 million (2028) and $649.0 million (2030) against $147.5 million of cash — in addition, $300 million of receivables are sold (with a rating trigger since February 2026).

- Customers & legal risks negative

- A single customer accounted for 18.1 percent of 2025 revenue, the top 20 for 69 percent with a rising trend; revenue fell 2.3 percent in the first quarter of 2026. On top of that, a shareholder class action has been running since June 2025 (motion to dismiss January 2026), and the board has installed a poison pill with a 10 percent threshold.

Fortrea is not an empty warning-scanner ghost but a genuine global contract research company with stable revenue, a bulging order book and measurable cost progress. But the filings show what the ex-parent Labcorp packed for its daughter: a debt dowry of originally $1.64 billion whose covenants already had to be loosened, and an acquisition goodwill of which almost $800 million was written off in 2025 — triggered by the company's own share-price crash. Add one customer at 18.1 percent of revenue, $300 million of sold receivables and an ongoing class action. Not investment advice.

What Our Rating Means

- If you don't own the stock

- In our view, the documented risks clearly outweigh — we see no basis for an entry.

- If you hold it in your portfolio

- In our view, the findings carry enough weight to warrant a critical look at your own position.

A journalistic assessment by our editorial team at the time of the deep dive, based on public sources — not investment advice and not a solicitation to buy or sell. Your personal circumstances (investment goals, risk capacity, taxes) cannot be taken into account. What our categories mean, how verdicts are formed, and what conflicts of interest exist →

Worth Noting

- Scanner membership ("Going Concern (Distress Proxy)", plus the P/S, price-to-cash-flow and price-to-free-cash-flow rankings) verified live on the platform on July 14, 2026; metrics data as of July 8, 2026.

- The 2025 net loss (−$986.2 million) contains $797.9 million of non-cash goodwill impairment; without it, an operating loss of about $75 million would have remained. The 2024 loss (−$328.5 million) contains −$57.0 million from the discontinued Enabling Services business.

- Price and valuation figures dated July 8, 2026 (about $17.70, about 93 million shares); analyses are evergreen, daily prices are not a buy argument.

Frequently Asked Questions

Fortrea (NASDAQ: FTRE, Durham/North Carolina) is a global contract research organization (CRO): about 14,300 employees plan and run Phase I through IV clinical trials in roughly 100 countries for pharma, biotech and medical-device customers — as a full-service package or a staff-leasing model (FSP). Revenue 2025: $2,723.4 million; order backlog: $7.8 billion (March 31, 2026).

Fortrea is the former clinical-trials arm of Labcorp (before that: Covance) and was spun off on June 30, 2023; the stock has traded on the Nasdaq since July 3, 2023. Into independence the company took $1,640 million in freshly borrowed debt and the goodwill from Labcorp's 2015 Covance acquisition — both shape the balance sheet to this day.

Because of its own share-price collapse: per the annual report (10-K) for 2025, "sustained declines in the Company's share price" ($7.55 at the end of March, $4.94 at the end of June 2025) triggered impairment tests. The result: $488.8 plus $309.1 — a total of $797.9 million of goodwill impairment on the Clinical Development unit. $960 million of goodwill remained — more than the equity of $563.5 million.

About $1,066.3 million in principal (December 31, 2025): a 7.50 percent note of $494.3 million (due 2030), Term Loan A of $412.5 million (2028) and Term Loan B of $154.7 million (2030). On February 28, 2025 the credit covenants were loosened; as of March 31, 2026 Fortrea was in compliance with all covenants. Cash: $147.5 million — in addition, $300 million of receivables have been sold.

Our distress proxy fires because several early-warning metrics warn at the same time (data as of July 8, 2026): Altman Z-Score 0.78 (danger zone below 1.1), Piotroski 4 of 9, negative interest coverage and four distress flags. That is an approximation built from balance-sheet metrics — not an auditor's verdict: the 2025 audit opinion expressly contains no going-concern qualification.

This analysis expressly passes no insolvency verdict. The facts: no going-concern qualification, covenants met, only about $30 million due through the end of 2027, a $450 million credit line untouched, and a first quarter of 2026 that was operationally almost break-even. Against that stand the maturities of $387.5 million (2028) and $649.0 million (2030), $147.5 million of cash and a business that still runs at an operating loss.

The stock is held predominantly by institutional investors (data basis: fundamental data, spring 2026): BlackRock held about 16 percent, Vanguard just under 9, Goldman Sachs about 8.6; plus hedge funds such as Corvex Management and Sessa Capital at about 5 percent each. Since June 11, 2025 a poison pill with a 10 percent threshold has protected the company against unwanted takeovers.

Found an error?

Did you spot a factual error, an outdated number, or a typo in this deep dive? Let us know briefly — your report goes straight to the editorial team.