Firy Stock: The Renamed Skillz Has More Cash in the Till Than the Market Pays for It — and Is Suing Its Most Important Partner

On June 18, 2026, Skillz renamed itself Firy — the mobile-gaming platform's stock has more than doubled since the start of 2026, and there is $185.4 million of cash in the till against a market value of only about $131 million. Sounds like a fresh start at a bargain price? We read the annual report (10-K) for 2025 and the quarterly report (10-Q) as of March 31, 2026: the partner behind 51 percent of revenue has terminated and meets Firy in court in August 2026, a $129.7 million note at 10.25 percent comes due in December 2026, and the internal accounting controls have been demonstrably leaky for years. Not investment advice — just the question of what a new name is worth when the old numbers move in with it.

There is hardly an impulse that softens us humans as reliably as a second chance. The smoker who becomes a new person as of Monday. The team that, with a new coach, is suddenly supposed to win the title again. Let's call it the fresh-start belief — the quiet conviction that a fresh name disposes of the old problems along with it. And hardly any stock feeds that belief as well right now as Firy Inc. (NYSE: FIRY): on June 18, 2026, the mobile-gaming group Skillz renamed itself — the same Skillz whose stock trades about 99 percent below its all-time high after the SPAC hype of 2021 (data as of July 8, 2026). A new name, a new story, and the price has more than doubled since the start of 2026. Add a detail that electrifies every bargain hunter: there is $185.4 million in cash in the till (March 31, 2026) — more than the whole company costs on the stock market. So let's make a deal: before you believe the new name, we read together what the company itself reported to the U.S. securities regulator, the SEC — in the annual report (10-K) for 2025 and the quarterly report (10-Q) as of March 31, 2026. An SEC filing is honest under penalty of law, and it does not recognize renamings: in there stand the termination by the most important partner, a note due in December 2026 and three unresolved holes in the accounting controls. In the end, you decide for yourself.

What Firy actually does

Picture a fairground booth where two strangers throw at cans for money — and the booth owner supplies equally strong opponents, collects the stakes and keeps a stall fee. That is exactly the core business: on the Skillz platform, mobile players compete against each other in games of skill — solitaire, bowling, bubble shooters — for real money. Firy does not build the games itself; they come from independent developer studios that build Firy's technology (the "SDK", a software toolkit) into their apps. Firy handles the matchmaking — real players against real players of similar skill, the "fair play" promise —, the deposits and withdrawals, the fraud prevention, and keeps a margin of the entry stakes: the entry-fee revenue, $78.2 million in 2025. Because skill rather than luck decides, this does not count as gambling in most U.S. states — a regulatory sleight of hand on which the entire model rests. The second pillar is called RZR (pronounced "Razor", "Aarki" until 2025): an advertising platform that uses machine learning and neural networks to optimize ad campaigns for mobile apps and brands — per the annual report, an AI-powered advertising technology segment. RZR contributed $26.3 million in 2025, up 153 percent. All of it is run by 370 employees out of Las Vegas, with offices in San Francisco and Bangalore.

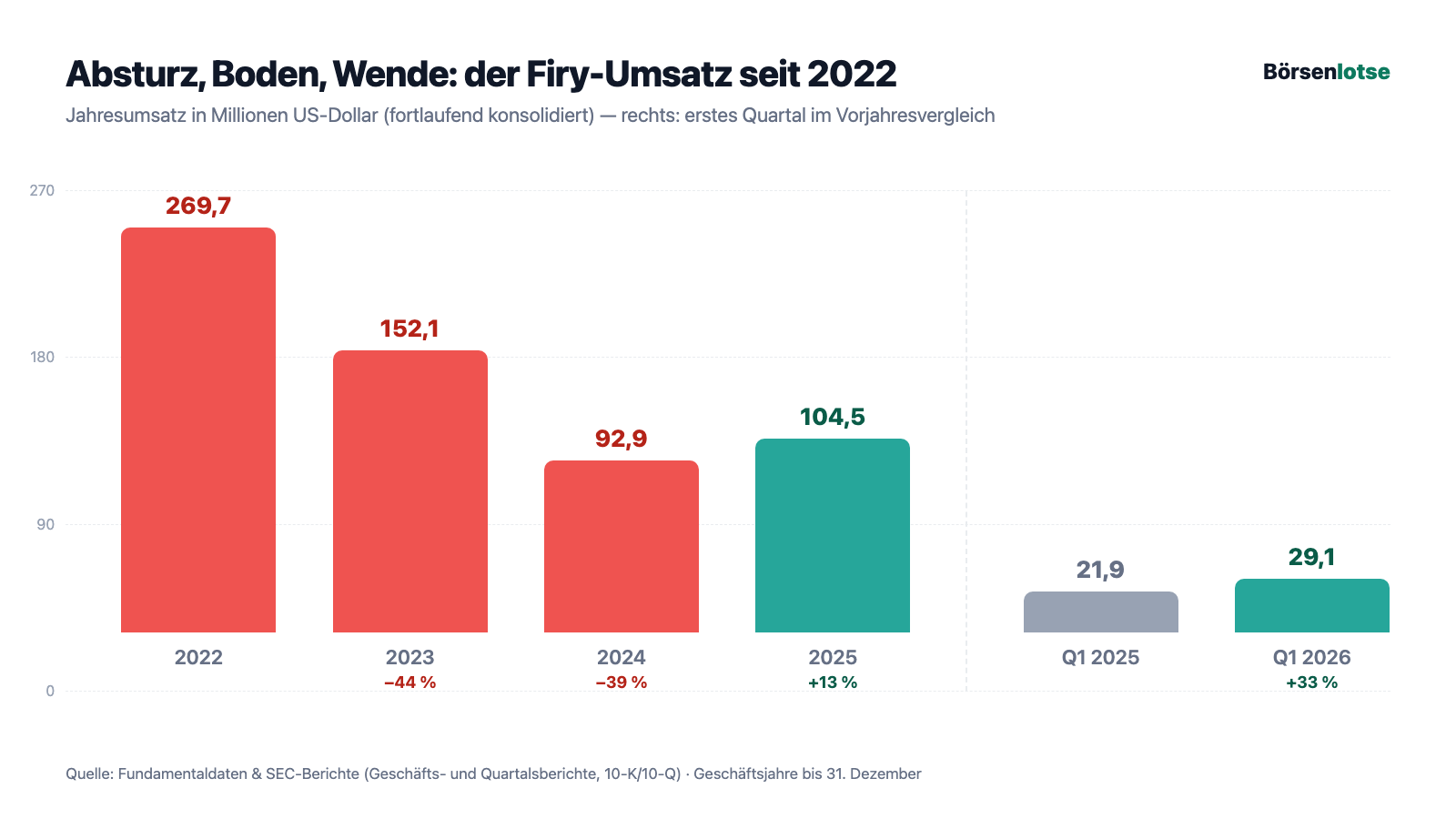

Honesty includes the backstory, because it explains the name change: Skillz came public in December 2020 via SPAC merger (through the shell "Flying Eagle Acquisition Corp.") and was at times valued in the billions during the hype. Then the house of cards collapsed — revenue fell from $269.7 million (2022) via $152.1 million (2023) to $92.9 million (2024), and in June 2023 every 20 shares had to be merged into one (a 1-for-20 reverse split) so the price would not optically languish in penny-stock territory. The new name Firy, announced by mandatory filing (Form 8-K) on June 8, 2026 and completed on June 18, is meant to draw a visible line under all that. Note the central tension of this analysis: a cash pile larger than the market value and a business that is finally growing again — against a partner who delivers half the revenue and is fighting in court over the separation, a note due in December 2026, and books whose controls have been leaky for years. It runs through every chapter. How such a SPAC crash ends when the cash does not suffice is, by the way, what we dissected at Virgin Galactic — the comparison is worth it.

Where the stock shows up in our scanner

Every day we run about 3,500 stocks through our scanners. Firy sits in the warning scanner "Going Concern (Distress-Proxy)" — we cross-checked the membership live on the platform on July 14, 2026; in addition, the stock shows up there in the "Beneish M-Score" scanner, which hunts for statistical patterns of embellished numbers. "Going concern" is the technical term for a company's ability to keep operating; our scanner is a proxy, an approximation built from balance-sheet ratios — not an auditor's verdict. What the metrics (data as of July 8, 2026) report: the Altman Z-Score, a classic insolvency early warning built from several balance-sheet ratios, sits at Firy around minus 9 — the historical danger zone begins below 1.1; deeply negative values arise when years of losses have eaten through the accounts. The Piotroski F-Score, a nine-point test of balance-sheet quality, stands at 4 of 9 — okay, not good; a thoroughly healthy company stands at 8 or 9. The interest coverage is negative at around minus 3: operating income is not enough to earn the interest — it is negative itself. Four distress flags in total. How to read such warning lists — a smoke detector, not a demolition notice — is explained in our article "Insolvency Radar: the Top 10".

And now the other side of the same scanner picture: the relative strength sits at 95 of 99 — over the past twelve months the stock has left almost the entire market behind it, including a gain of 112 percent since the start of 2026 and about 79 percent over six months (all values: data as of July 8, 2026). The Weinstein phase analysis classes the stock in Stage 2, the uptrend phase; the price trades above the 50- and the 200-day lines. At the same time the stock swings around 10 percent per day on average, and only about 38 percent of the shares sit with institutional investors — little for an NYSE name; the professionals are mostly keeping their distance while the price runs. This side-by-side — distress metrics from the past, momentum from the present — is the typical fingerprint of a stock on which the market is playing a comeback bet whose proof is still pending. Exactly the right address for the fresh-start belief. And exactly why the look into the filings pays off.

The numbers over the years — honestly appraised

First, what has genuinely improved — and that is more than skeptics would expect. Revenue is growing again: $104.5 million in 2025, up 13 percent from the $92.9 million of 2024 — the first increase since the crash. And the pace is picking up: in the first quarter of 2026, revenue rose 33 percent to $29.1 million (prior-year quarter: $21.9 million). The driver is above all RZR: the advertising technology segment grew 153 percent in 2025 to $26.3 million and expanded again in the first quarter of 2026 from $4.4 to $9.8 million — more than a doubling. But the core business is turning too: entry-fee revenue of the Skillz segment rose in the first quarter of 2026 from $17.2 to $19.4 million, and the number of paying monthly active users rose to 141,000 in 2025 (2024: 118,000) — remarkable, because the total user count fell at the same time from 816,000 to 658,000. Translated: the platform is getting smaller, but the remaining players pay more often. The cost side has delivered as well: sales and marketing costs, which still devoured $277.0 million in 2022 — more than that year's entire revenue —, stood at $71.1 million in 2025. That was the old Skillz problem in one number: growth that cost more than a dollar of advertising per dollar of revenue. That wheel no longer spins.

The cash-burn trend is real too: the operating cash outflow stood at $68.9 million in 2025 — but that included one-off effects such as $14.0 million for the termination of the old San Francisco lease. In the first quarter of 2026, only $6.7 million flowed out of operations (prior-year quarter: $10.9 million). Honesty, however, also demands the counter-calculation: the bottom line for 2025 was a net loss of $70.4 million — more than the $46.8 million of 2024. How so, with revenue growing? Because 2024 was flattered: back then, a one-off gain of $46.0 million from a litigation settlement with the competitor AviaGames padded the result (Skillz had sued the rival over the use of computer bots and was awarded $80 million; since then an additional $7.5 million per year flows in as a license fee — including in the first quarter of 2026). Strip out the litigation wins and the actual business keeps losing money year after year; since inception, $1,091.7 million of losses have piled up. Remember the sentence: at Firy, revenue is growing again — but so far the profit comes from the courtroom, not from the game. Which brings us to the uncomfortable truths.

What the filings say — the uncomfortable truths

Uncomfortable truth no. 1: the partner behind 51 percent of revenue has terminated — the trial starts August 25, 2026

Firy's platform lives on other people's games — and dramatically concentrated on the games of two studios: Tether Studios ("Solitaire Cube", "21 Blitz") stood for 51 percent of group revenue in 2025, Big Run Studios for another 23 percent. Together: 74 percent. The jargon calls this customer concentration — translated: if your neighbor told you his corner shop was doing great, but a single regular provided half the takings, you would swallow briefly. Now swallow twice, because this regular has given notice:

"As previously disclosed, on August 29, 2025, we received a notice (“Notice”) from Tether indicating that Tether is terminating all of its various agreements with us (the “Tether Agreements”), including our terms or services, effective as of September 1, 2025. […] We believe the termination notice to be invalid and in breach of Tether's obligations under the Tether Agreements."

— Firy Inc. (filed as Skillz Inc.), SEC annual report 10-K 2025, Item 1A "Risk Factors"

Since September 1, 2025, the partners have been fighting before the Delaware Court of Chancery, a court specialized in corporate law: Firy is suing for an injunction and a declaration that the termination is invalid; Tether counters with counterclaims (breach of contract, trademark infringement); in March 2026 Firy expanded the suit with the accusation that Tether is monetizing its games past the Skillz system through an affiliated company named Aim Games. The trial is scheduled for August 25 to 27, 2026. Firy's safety net: the agreements bind the two most important Tether games to the platform for at least 18 months after termination — so the clock runs into the spring of 2027, no longer. It is remarkable that entry-fee revenue grew in the first quarter of 2026 despite the dispute. But nobody should fool themselves: if Tether wins in court and pulls its games, the core business loses half its base in one stroke — and no name change in the world alters that.

Uncomfortable truth no. 2: three holes in the accounting controls — known for years, still open at the end of 2025

The second truth concerns the foundation of every analysis: can you trust the numbers at all? Firy's own answer in the annual report is uncomfortable. The company has already had to correct financial statements ("restatements", most recently for interim reports through mid-2023 — among other things, liabilities to its own players had been understated), filed the annual report for 2024 a good seven months late on November 6, 2025 — after a formal notice from the New York Stock Exchange dated April 2, 2025 for violating the listing rules — and delivered the three quarterly reports of 2025 in a batch on a single day, December 11, 2025. The report itself names the cause behind it, with remarkable candor:

"Based on the results of this assessment, management concluded that internal control over financial reporting was not effective as of December 31, 2025, due to the existence of material weaknesses described below. […] Additionally, there was an inadequate review of complex accounting assumptions, together with a lack of qualified accounting personnel employed during the year."

— Firy Inc. (filed as Skillz Inc.), SEC annual report 10-K 2025, Item 9A "Controls and Procedures"

Concretely, the report lists three continuing material weaknesses — deficiencies serious enough that a wrong number in the financial statements might not be caught in time: first, an insufficiently formalized risk-assessment process; second, leaky IT access controls (in short: who is allowed to change what in the finance systems — segregation of duties was not assured); third, the just-quoted gaps in reviews and qualified staff. To be fair: management asserts that the financial statements are, despite the weaknesses, correct in all material respects; the annual report for 2025 arrived on time on March 31, 2026, the quarterly report followed on schedule — the filing backlog is cleared, and remediation of the weaknesses is promised for 2026. But hold on to the sequence: the same company whose numbers you need for the comeback thesis tells you itself that its control mechanisms did not work recently. A fresh name changes nothing about that — the same weaknesses already stood in the previous year's late report.

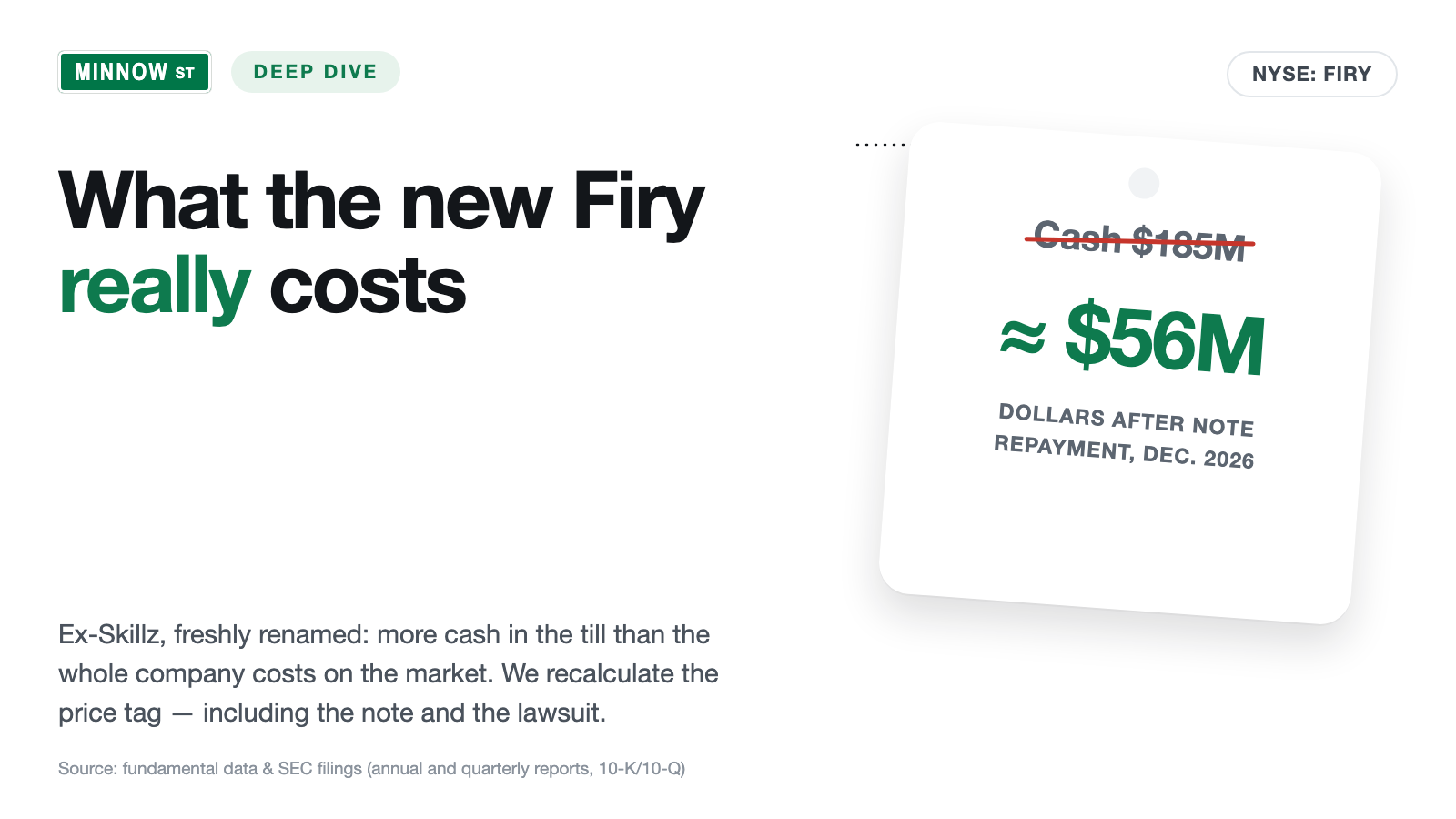

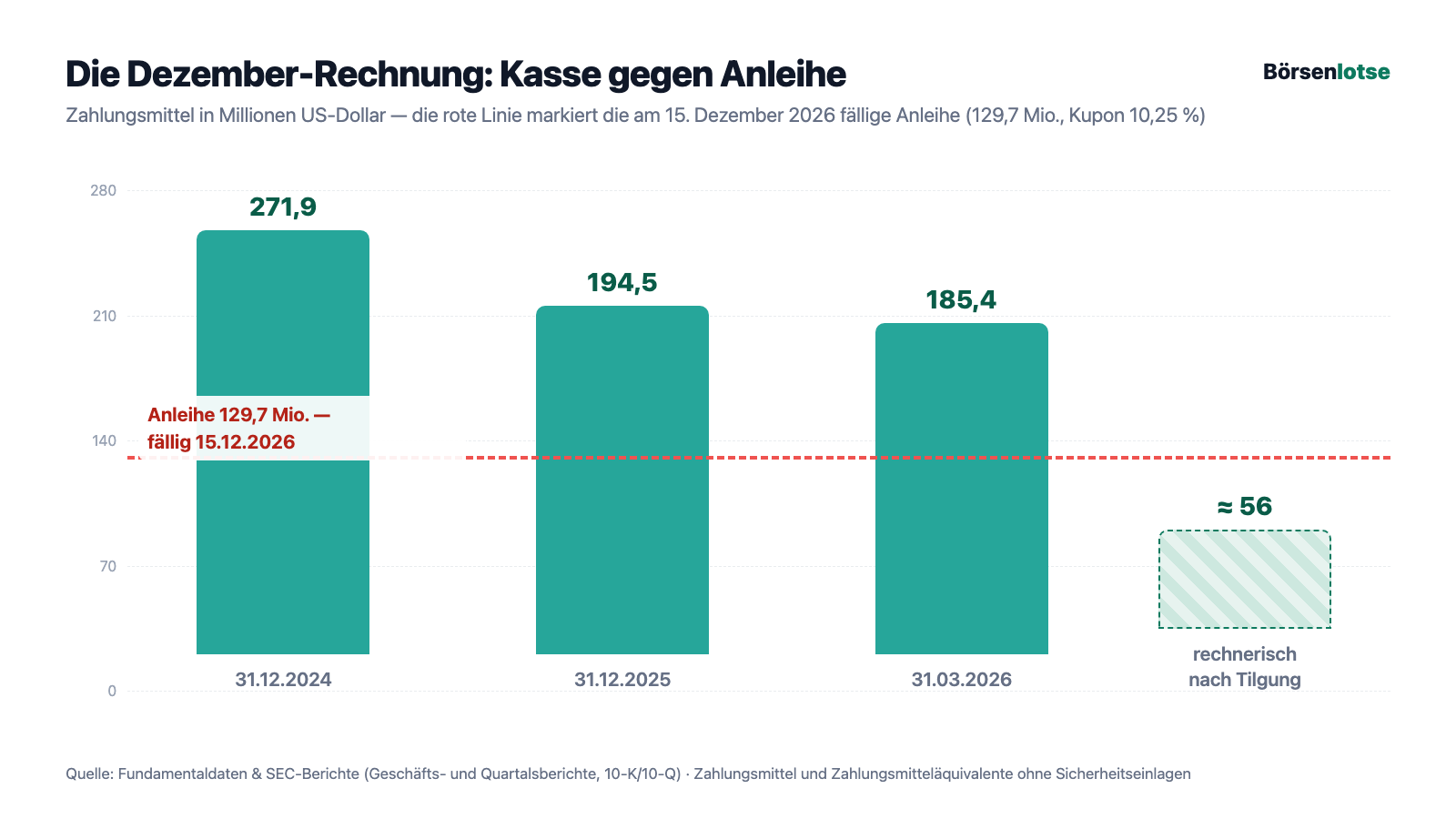

Uncomfortable truth no. 3: $129.7 million comes due on December 15, 2026 — then the cash advantage is gone

That leaves the buyers' strongest argument: the cash. $185.4 million as of March 31, 2026, more than the market value — what could go wrong? The answer is in note 7 of the balance sheet: in December 2021, at the peak of the euphoria, Skillz had issued a note of $300 million at 10.25 percent interest. Part of it the company has bought back cheaply over the years — but $129.7 million of principal is still outstanding, and it comes due for repayment on December 15, 2026. The position has already migrated in the balance sheet from long-term to current liabilities. Management sounds relaxed:

"After giving effect to open market repurchases of our senior secured notes, $129.7 million of the senior secured notes remained outstanding as of March 31, 2026. […] We believe our existing sources of liquidity are sufficient to fund our operating activities on a short- and long-term basis. […] However, we cannot assure you that cash provided by operating activities or cash and cash equivalents will be sufficient to meet our future needs."

— Firy Inc. (filed as Skillz Inc.), SEC quarterly report 10-Q as of March 31, 2026, Item 2 MD&A "Liquidity and Capital Resources"

Let's do the sober math: $185.4 million of cash minus $129.7 million of repayment leaves about $56 million — for a business that still loses money in operations ($6.7 million of outflow in the first quarter of 2026 alone, plus interest coming due: the note costs about $13 million of interest per year, payable half each in June and December). There are three ways out, and all of them stand between the lines of the filing: first, keep buying back notes below par and repay the rest from the till — that consumes the cash advantage on which the bargain thesis rests. Second, refinance — at what rate, the capital market decides, for a company with distress metrics. Third, issue new shares — your slice of the pie would get smaller. Honesty also demands this here: there is no going-concern qualification — the auditor issued the 2025 opinion without a continuation warning, and the cash fully covers the note today. The question is not whether Firy survives December 2026. The question is what remains of the safety cushion afterwards.

Uncomfortable truth no. 4: whoever buys Firy becomes junior partner to a founder with 87 percent of the votes

The fourth truth stands in the chapter on shareholder rights, and it puts every voting-power fantasy in its place: Firy has two share classes. The exchange-traded Class A shares carry one vote each — the Class B shares of co-founder and CEO Andrew Paradise carry 20 votes each:

"Shares of our Class B common stock carry 20 votes per share, compared to one vote per share for our Class A common stock. As a result, Mr. Paradise can control the outcome of matters submitted to stockholders, including the election of directors, amendments to our charter documents, and approval of mergers or other significant transactions."

— Firy Inc. (filed as Skillz Inc.), SEC annual report 10-K 2025, Item 1A "Risk Factors"

As of December 31, 2025, Paradise thereby controlled 87 percent of the voting power — with well under half of the capital. Firy is therefore a "controlled company" under NYSE rules and may forgo protective mechanisms other corporations must have: no requirement for a majority-independent board, no independent committees for compensation and director nominations. Translated: as a Class A shareholder you participate economically, but you have no real say — renaming, merger or strategy pivot, Paradise decides alone. That can work out; founders with skin in the game have pulled off many a turnaround, and as the largest of all shareholders Paradise has the same economic incentive as you. But it belongs on the price tag — especially since a shareholder suit in Delaware (Hanna v. Paradise, since March 2024) is currently examining whether insiders abused their knowledge when selling shares in the boom March of 2021. The freely tradable float had a market value of just $80.3 million as of June 30, 2025 — despite its NYSE listing, Firy is a micro cap, with everything that means for price swings.

Valuation: the market pays for the cash — and gets the business almost for free. Why might that be?

In early July 2026 the Firy stock cost about $8.40; at about 15.6 million shares (12.2 million Class A plus 3.4 million Class B, as of March 27, 2026) that makes a market value of about $131 million (data as of July 8, 2026). Against that stand: $185.4 million of cash, minus the $129.7 million note — net about $56 million —, plus a stake in a non-listed company with a book value of $52.8 million and outstanding settlement payments from AviaGames ($7.5 million per year through 2028). Equity stood at about $112 million at the end of 2025. A price-to-earnings ratio does not exist for lack of earnings; the price-to-sales ratio sits around 1.2 (revenue of the last four quarters: about $112 million), the price-to-book ratio at about 1.3. Translated: the market essentially pays for the substance and throws in the operating business — $104.5 million of growing annual revenue, the RZR advertising platform, the AviaGames royalties — almost for free. On the stock market this is called a "cigar butt" valuation, and it is never a gift but a vote of no confidence: the market is pricing in that the Tether trial can go wrong, that the December repayment halves the till and that the losses keep running. Amid all this, do not forget the volatility: around 10 percent of daily movement on average, up 112 percent since the start of 2026 — after minus 98 percent in the five years before (all values: data as of July 8, 2026). That is not investing speed, that is casino speed — a certain irony for a group that insists in court that it is not a gambling operator.

Opportunities and risks at a glance

What speaks for Firy:

- Revenue is growing again for the first time since the SPAC crash: up 13 percent to $104.5 million (2025), up 33 percent in the first quarter of 2026; paying monthly users rose in 2025 from 118,000 to 141,000 (annual report 10-K for 2025, quarterly report 10-Q as of March 31, 2026).

- RZR (formerly Aarki) is a genuine second pillar: AI-powered advertising technology with revenue up 153 percent in 2025 ($26.3 million) and another doubling in the first quarter of 2026 — largely independent of the gaming litigation.

- Substance cushion: $185.4 million of cash (March 31, 2026) above the market value of about $131 million (July 8, 2026), plus $52.8 million of investment book value and $7.5 million of AviaGames license fees per year through 2028; a share buyback program of $41.1 million is authorized.

- The cash burn is falling steeply: operating outflow from $68.9 million (2025, including the $14 million one-off payment for the legacy lease) to $6.7 million in the first quarter of 2026; the SEC filing backlog has been cleared since March 2026.

- A founder with skin in the game: Andrew Paradise is the largest owner and has the same economic incentive in the comeback as the shareholders; the litigation offensive against bot operators has already brought in $80 million.

What speaks against it:

- Extreme concentration risk in the core business: Tether stood for 51 percent, Big Run for 23 percent of 2025 revenue — and Tether terminated all agreements on August 29, 2025; the trial (Delaware Court of Chancery) is scheduled for August 25 to 27, 2026, and the game commitment ends after 18 months.

- On December 15, 2026, $129.7 million of notes (10.25 percent) come due — after repayment from the till, as of March 31, 2026, arithmetically about $56 million would remain for a business still running at a loss; refinancing or dilution are the alternatives.

- Three material weaknesses in internal financial controls remained unresolved as of December 31, 2025 (risk assessment, IT access controls, accounting review including staff shortages); there were restatements, a 10-K for 2024 filed seven months late, and an NYSE notice dated April 2, 2025.

- The profit comes from the courtroom: a 2025 net loss of $70.4 million despite $7.5 million of litigation license fees; 2024 was flattered by the $46 million one-off gain from the AviaGames settlement; accumulated losses: $1,091.7 million; total users fell in 2025 from 816,000 to 658,000.

- Minority shareholders without a voice: Paradise controls 87 percent of the voting power (Class B: 20 votes per share), Firy is a "controlled company"; the float is worth only $80.3 million (June 30, 2025), with around 10 percent daily swings; early-warning systems: Altman Z around minus 9, Piotroski 4 of 9, four distress flags (data as of July 8, 2026).

A human conclusion

Back to the fresh-start belief from the beginning. It is not stupid — people, like companies, really can change, and at Firy the change is measurable: growing revenue, shrinking cash burn, a second pillar that works, a cleared filing backlog. That is more of a fresh start than most renamed stock-market shells ever show. But exactly here sits the thinking error this case can teach you: a new name is a promise — the filings test whether it is kept. And Firy's filings give the promise three deadlines: on August 25, 2026, the trial over the partner behind half the revenue begins. On December 15, 2026, the note comes due that decides the cash cushion. And at some point in 2026, management must deliver what it promised: accounting controls that work. Whoever buys the stock bets that all three tests turn out well — as the voteless junior partner of a founder who decides alone. Whoever waits may pay more after the tests are passed, but then knows the second chance was earned. The fresh-start belief asks: "Why not now, while everything sounds fresh?" The filings answer: because freshness is not evidence, it is a coat of paint — and the evidence has deadlines. What you make of it is your decision. And that is exactly as it should be.

Sources

All original documents used in this analysis — to read for yourself:

- Firy Inc. (filed as Skillz Inc.) — SEC annual report 10-K for 2025 (filed March 31, 2026)

- Firy Inc. (filed as Skillz Inc.) — SEC quarterly report 10-Q as of March 31, 2026 (filed May 15, 2026)

- Skillz Inc. — SEC annual report 10-K for 2024 (filed November 6, 2025 — late)

- Skillz Inc. — SEC annual report 10-K for 2023 (filed August 29, 2024 — late)

- Skillz Inc. — SEC quarterly report 10-Q as of March 31, 2025 (late-filed December 11, 2025), 10-Q as of June 30, 2025 and 10-Q as of September 30, 2025 (both likewise December 11, 2025)

- Skillz Inc. — Form 8-K of April 8, 2025 (NYSE notice over the late 10-K)

- Skillz Inc. — Form 8-K of June 8, 2026 (announcement of the renaming to Firy Inc.) and Form 8-K of June 18, 2026 (completion of the renaming)

- Firy/Skillz's complete SEC filing history: EDGAR overview (sec.gov)

- Fundamental data (metrics, price history, valuation; data as of July 8, 2026), reconciled with the SEC filings.

- Screener and rating data: in-house stock scanner (data as of July 8, 2026; scanner membership verified live on July 14, 2026).

Transparency & disclaimer: This analysis is a journalistic contextualization of publicly available information and is not investment advice, not a financial analysis in the regulatory sense, and not a solicitation to buy or sell securities. It expressly contains no judgment on whether an insolvency will occur. Stock investments carry substantial risks up to total loss. All information without guarantee; the data cut-off is noted in the text in each case. The author holds no position in Firy stock at the time of publication.

Our Bottom Line at a Glance

- Business model & growth neutral

- The tournament platform is growing again (2025 revenue: +13 percent to $104.5 million; Q1 2026: +33 percent), and paying users rose in 2025 from 118,000 to 141,000 — but the total user count fell from 816,000 to 658,000, and the model hangs on the regulatory sleight of hand that skill is not gambling.

- Second pillar RZR positive

- The AI advertising technology segment (formerly Aarki) grew 153 percent in 2025 to $26.3 million and doubled again in the first quarter of 2026 ($9.8 million) — a real growth driver, largely independent of the gaming litigation per the annual report (10-K) for 2025.

- Concentration risk Tether negative

- Tether Studios delivered the games behind 51 percent of 2025 revenue (Big Run: another 23 percent) and terminated all agreements on August 29, 2025; the trial before the Delaware Court of Chancery is scheduled for August 25 to 27, 2026, and the contractual game commitment carries only 18 months.

- Balance sheet & December 2026 maturity neutral

- $185.4 million of cash exceeds the market value (about $131 million, July 8, 2026) — but on December 15, 2026, $129.7 million of notes at 10.25 percent come due; afterwards, arithmetically about $56 million would remain for a business with a $70.4 million loss in 2025. No going-concern qualification; the cash burn fell to $6.7 million in Q1 2026.

- Control & reporting quality negative

- Three material weaknesses in internal financial controls remained unresolved as of December 31, 2025, there were restatements, a 10-K for 2024 filed seven months late including an NYSE notice — and co-founder Andrew Paradise controls 87 percent of the voting power (Class B: 20 votes per share, "controlled company").

Firy is more than a renamed stock-market shell: revenue is growing at double-digit rates, the AI adtech segment RZR is booming, the cash burn is falling, and the cash exceeds the market value. But the filings hang three weights on the fresh start: a trial over the partner behind half the revenue (from August 25, 2026), a $129.7 million note due on December 15, 2026 that halves the cash cushion, and accounting control weaknesses unresolved for years — with a founder who decides alone with 87 percent of the votes. Not investment advice.

What Our Rating Means

- If you don't own the stock

- In our view, the documented risks clearly outweigh — we see no basis for an entry.

- If you hold it in your portfolio

- In our view, the findings carry enough weight to warrant a critical look at your own position.

A journalistic assessment by our editorial team at the time of the deep dive, based on public sources — not investment advice and not a solicitation to buy or sell. Your personal circumstances (investment goals, risk capacity, taxes) cannot be taken into account. What our categories mean, how verdicts are formed, and what conflicts of interest exist →

Worth Noting

- Firy operated as Skillz Inc. until June 18, 2026; all SEC filings quoted here were submitted under the name Skillz Inc. (ticker SKLZ). The scanner membership ("Going Concern (Distress-Proxy)", additionally "Beneish M-Score") was verified live on the platform on July 14, 2026.

- The 2024 net loss (−$46.8 million) includes a one-off gain of $46.0 million from the AviaGames settlement; 2025 and the first quarter of 2026 each include $7.5 million of annual license payments from the same settlement.

- Price and valuation figures dated July 8, 2026 (about $8.40, about 15.6 million Class A and B shares); analyses are evergreen, daily prices are not a buy argument.

Frequently Asked Questions

Firy (NYSE: FIRY, Las Vegas) — Skillz Inc. until June 2026 — operates a platform for mobile skill-based tournaments for real money: independent developer studios plug in their games, Firy handles matchmaking, payments and fraud prevention and keeps a margin of the entry fees. Added to that is RZR (formerly Aarki), an AI-powered advertising platform. Revenue in 2025: $104.5 million.

The renaming was announced by Form 8-K on June 8, 2026 and completed on June 18, 2026; since then the stock has traded under the ticker FIRY. The mandatory filings give no official reason — they refer to an investor presentation for the 2026 annual meeting. In effect, the new name draws a visible line under the SPAC era, in which the stock lost about 99 percent.

Tether Studios ("Solitaire Cube", "21 Blitz") stood for 51 percent of Firy's revenue in 2025 — and terminated all agreements on August 29, 2025. Firy considers the termination invalid and is suing before the Delaware Court of Chancery; Tether counters with counterclaims. The trial is scheduled for August 25 to 27, 2026. The two most important games remain bound to the platform for at least 18 months after termination.

As of March 31, 2026, there was $185.4 million of cash in the till — more than the market value of about $131 million (July 8, 2026). But on December 15, 2026, $129.7 million of notes at 10.25 percent come due; after repayment, arithmetically about $56 million would remain. Operating cash outflow fell to $6.7 million in the first quarter of 2026; management considers the liquidity sufficient, and no going-concern qualification exists.

No. 2025 ended with a net loss of $70.4 million — more than 2024 ($46.8 million), which, however, was flattered by a one-off gain of $46 million from the AviaGames litigation settlement. Since inception, losses add up to $1,091.7 million. On the positive side: revenue is growing again (up 13 percent in 2025, up 33 percent in the first quarter of 2026), and the cash burn is falling markedly.

Control lies with co-founder and CEO Andrew Paradise: his Class B shares carry 20 votes each, which gave him 87 percent of the voting power as of December 31, 2025. Firy is thereby a "controlled company" under NYSE rules and exempt from several governance requirements. Institutional investors held about 38 percent of the shares, and the float was worth only $80.3 million as of June 30, 2025.

This analysis expressly issues no insolvency verdict. The facts: the 2025 audit opinion contains no going-concern qualification, and the cash ($185.4 million) fully covers the note due in December 2026 ($129.7 million). At the same time, our early-warning systems report an Altman Z-Score around minus 9, Piotroski 4 of 9 and four distress flags — and the Tether trial decides half the revenue.

Found an error?

Did you spot a factual error, an outdated number, or a typo in this deep dive? Let us know briefly — your report goes straight to the editorial team.