Exelixis Stock: $2.1 Billion in Revenue From a Single Molecule — and a Patent Cliff That Isn't One

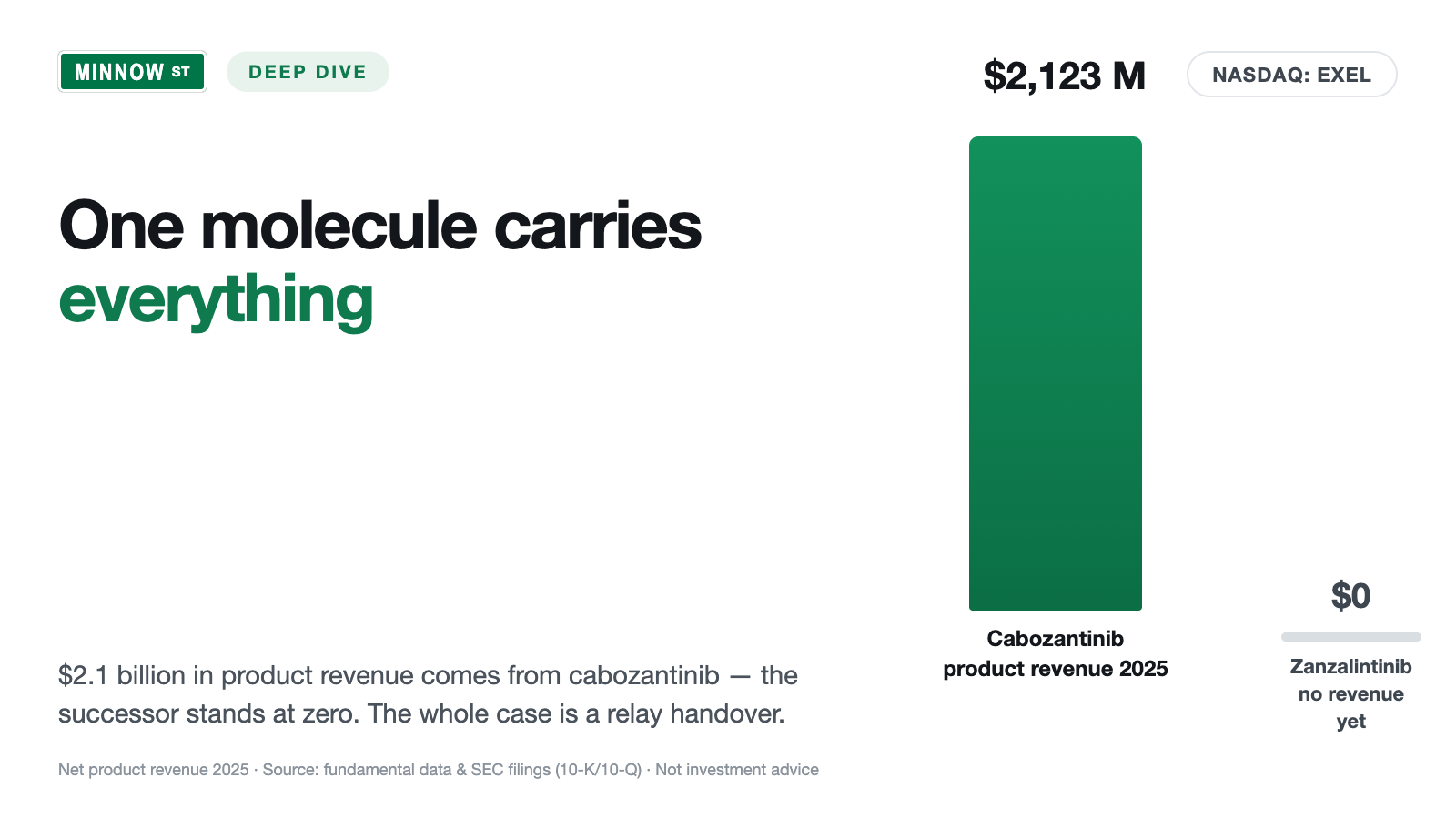

Exelixis earns almost all its revenue with a single cancer drug — cabozantinib, sold as CABOMETYX — and is thus the rare, genuinely profitable biopharma in our value scanner after Joel Greenblatt's Magic Formula. Net product revenue rose from $1,628.9 million (2023) to $2,122.8 million (2025), 2025 was the ninth consecutive profitable year, and $782.6 million remained at the bottom line. We read the annual report (10-K) for 2025 and the quarterly report (10-Q) as of April 3, 2026: the composition-of-matter patent expires in August 2026, several generic makers stand ready, two wholesalers account for 41 percent of revenue — and the actual price of the stock hangs on a successor that has yet to earn a dollar. Why the 2026 patent expiry is still no cliff, but a staircase down to 2030.

There is a thinking error that catches us investors precisely when a company has done everything right for years: call it the extrapolation reflex. We see a clean line out of the past — nine profitable years in a row, rising revenue, a full war chest — and our mind simply draws it straight on into the future. Picture a relay race: the runner on the track is strong, has opened a comfortable lead, and we cheer as if the team had already won. But it is a relay — the result is decided only at the handover of the baton to a second runner we have never seen run. This is exactly the situation of Exelixis (Nasdaq: EXEL): a cancer biopharma that generates more than two billion dollars a year with a single active ingredient — cabozantinib — that turns a profit nine years running and therefore shows up as a rare exception in a value scanner, where otherwise solid, cheap companies sit. The strong runner is unmistakable. So let's make a deal: before you extend its lane straight into the future, we look together at the baton it has to pass on — and at a date on the calendar that is often misunderstood. The basis is what Exelixis itself reported to the U.S. securities regulator, the SEC, in the annual report (10-K) for 2025 and in the quarterly report (10-Q) as of April 3, 2026. An SEC filing is honest under penalty of law. In the end, you decide for yourself.

What Exelixis actually does

Exelixis makes no devices and sells no software — the company researches, develops and markets cancer drugs. Its heart is the active ingredient cabozantinib, a so-called kinase inhibitor. Translated into an everyday image: cancer cells grow and build new blood vessels because certain switches inside them are stuck permanently on "on"; cabozantinib flips several of these switches at once and thereby slows growth and vessel formation. It is sold as CABOMETYX (a tablet, approved among other things against advanced kidney cancer, liver cancer, a certain thyroid cancer and, more recently, neuroendocrine tumors) and as COMETRIQ (a capsule against a rare form of thyroid cancer). In the United States Exelixis sells directly; outside the U.S. the partners Ipsen (worldwide except the U.S. and Japan) and Takeda (Japan) take over and pay royalties for it. The company is incorporated in Delaware but works out of Alameda, California, and employs 1,077 people (as of December 31, 2025).

And here is the peculiarity that carries this analysis: unlike most biotechs we write about, Exelixis is not a perpetual research loss-maker but has been solidly profitable for years — and the profit is real, not dressed up by one-off effects. The future, however, is meant to be carried by a new active ingredient: zanzalintinib (formerly XL092), a successor from the same drug class, meant to work more broadly and more modernly, for which Exelixis has already filed for approval — but it has not yet brought in a single dollar of revenue. Note already the central tension of this analysis: a genuinely profitable one-product business with a fat profit — whose entire value hangs on whether the baton is passed from cabozantinib to zanzalintinib in time and intact, before patent expiry and generics eat up the lead. It runs through every chapter. How vulnerable a profitable one-product biopharma is despite a full war chest is shown, by comparison, in our analysis of Aurinia Pharmaceuticals — there it is a hard patent cliff in 2027, here a gentler staircase down to 2030. And how hard it is even for a giant to break free from a dependence on a single molecule strand is demonstrated, on an entirely different scale, by Eli Lilly.

Where the stock shows up in our scanner

Every day we run about 3,500 stocks through our scanners. Exelixis lights up in 13 filters (data as of July 8, 2026) — and this time not a single warning scanner is among them. The most interesting hit is the Magic Formula of value investor Joel Greenblatt. His idea, in everyday language: buy good companies at a fair price — measured by two numbers. First, the return on capital (how much operating profit comes out per dollar of operating capital employed?), second, the earnings yield (how much operating profit do I get per dollar of enterprise value?). On top come hits in further quality and value scanners: "Buffett criteria", "Buffett: owner-earnings yield", "QARP — quality at a fair price" and the EBIT-margin ranking, rounded out by trend signals such as "Stan Weinstein: Stage 2" and "Above the 50- and 200-day SMA". The hard balance-sheet metrics confirm the clean picture: Altman Z-score 10.74 (a classic insolvency early-warning — danger begins only below 1.8, so deep green here), Piotroski F-score 8 of 9 (a nine-point balance-sheet test — 8 is nearly flawless), EBIT margin 41 percent, return on equity 41 percent, fundamental rating B. About $1.66 billion in cash and investments (December 31, 2025) and a debt-to-equity ratio of only about 0.09 round out the picture. No distress, no going-concern doubt.

Before you read that as a free pass, you must know what the scanner cannot do: all 13 filters assess the past and the present — return, margin, balance-sheet quality of today. None of them looks into the relay race: at the fact that practically all revenue hangs on one molecule whose core patent falls in 2026, and that the successor has yet to win its races. The filter is a good metal detector. Whether the signal is a gold nugget or a solid coin you cannot get at a bargain price is revealed only by the spade. Let's start digging.

The numbers over the years — honestly appraised

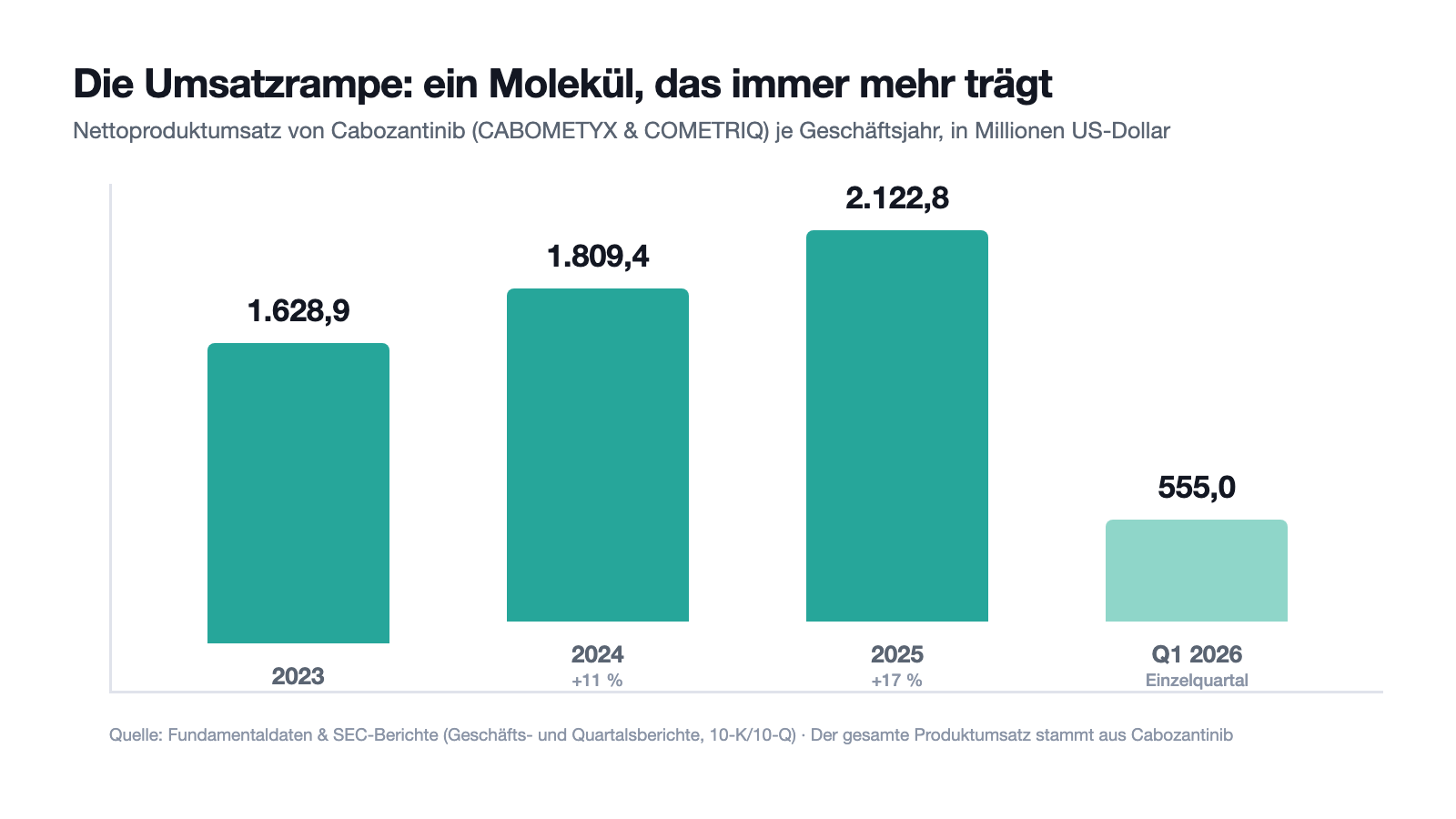

First, what genuinely impresses, and here that is a lot. The net product revenue of cabozantinib reads like a clean market build-out: $1,628.9 million in 2023, $1,809.4 million in 2024 (plus 11 percent), $2,122.8 million in 2025 (plus 17 percent). The momentum holds: in the first quarter of 2026 the company booked $555.0 million, after $513.3 million in the prior-year quarter — a gain of about 8 percent, carried above all by the growing prescription of CABOMETYX in combination with the immunotherapy nivolumab as first-line treatment for advanced kidney cancer. On top come royalties from the foreign partners ($179.2 million in 2025). And unlike at some other biotechs, at the end of this curve stands real profit: 2025 was the ninth consecutive year with a profit, net income came to $782.6 million ($2.78 per share, diluted), after $521.3 million in 2024. In the first quarter of 2026 it was $210.5 million ($0.79 per share, diluted). Important — and the pleasant difference from many an optical bargain: this profit is operationally earned, not inflated by a one-off tax benefit.

What the filings say — the uncomfortable truths

Uncomfortable truth no. 1: the entire product revenue hangs on a single molecule

Of the $2,320.1 million in total revenue in 2025, $2,122.8 million comes from product sales — and this product revenue is 100 percent cabozantinib (CABOMETYX plus COMETRIQ). The company says so itself in the report, quite soberly:

"In 2025, 2024 and 2023, we generated $2,122.8 million, $1,809.4 million and $1,628.9 million, respectively, in net product revenues from sales of CABOMETYX and COMETRIQ."

— Exelixis, Inc., SEC annual report 10-K 2025, Item 1 "Business — Commercial Products"

Translated into an image: picture a friend who proudly tells you his business is booming — until you learn that a single active ingredient accounts for all product revenue. You would swallow hard for a moment. As long as cabozantinib grows, that is a turbocharger; if it stalls — through a safety incident, a reimbursement decision, a copycat — there is no second approved product to cushion the fall. Concentration risk means: one problem, and it doesn't hit a quarter of the business, but all of it. That is exactly why the successor zanzalintinib is not a nice add-on but the real existential question.

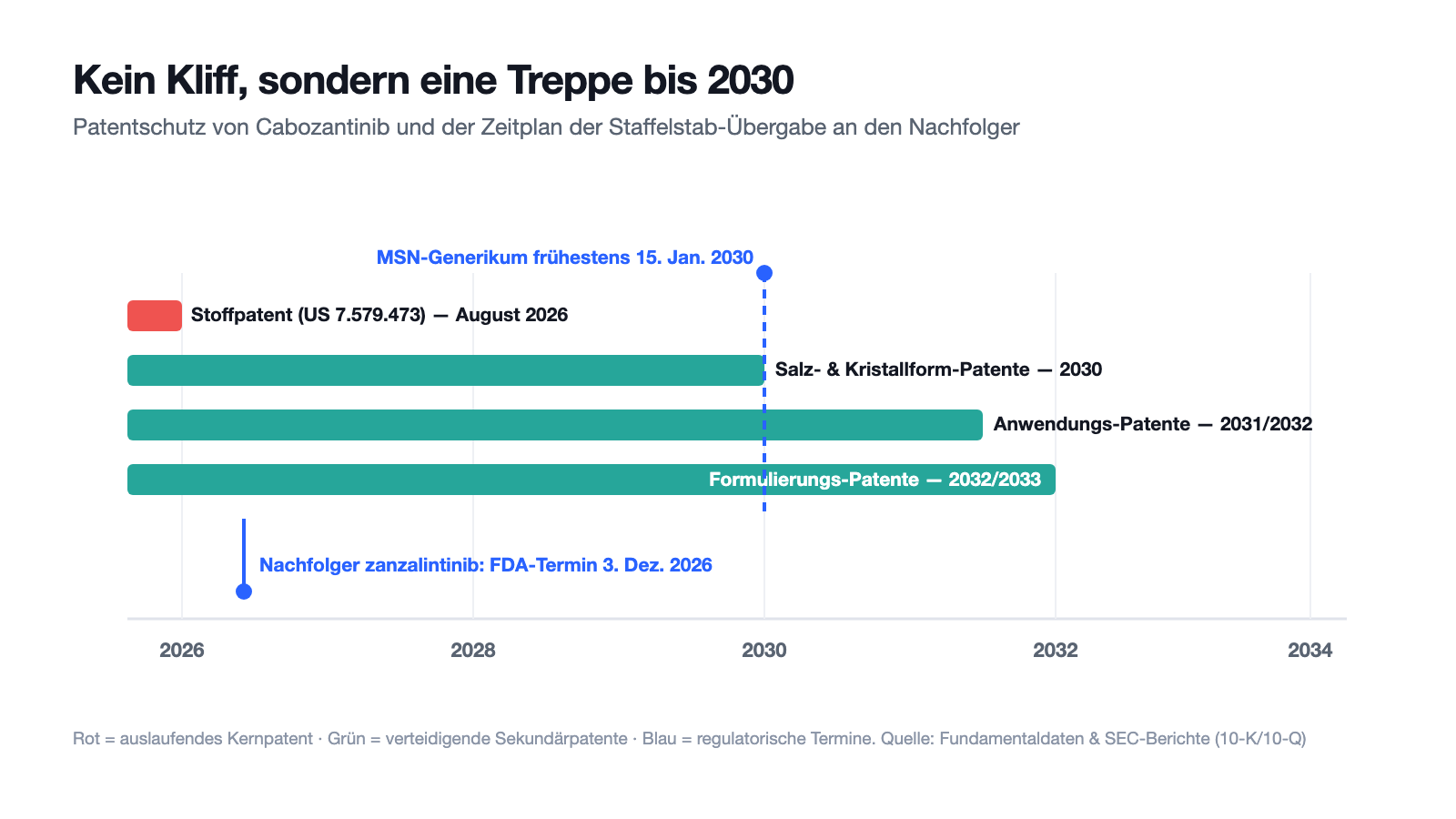

Uncomfortable truth no. 2: the composition-of-matter patent ends in August 2026 — and several generic makers stand ready

Here is the date the extrapolation reflex likes to overlook. The most important protective wall of a drug is the patent on the active ingredient itself (the "composition of matter"). For cabozantinib this core protection falls as early as 2026:

"Cabozantinib is covered by more than 15 issued patents in the U.S., building from U.S. Patent No. 7,579,473, for the composition of matter of cabozantinib and pharmaceutical compositions thereof. This composition of matter patent, with patent term extension, will expire in August 2026."

— Exelixis, Inc., SEC annual report 10-K 2025, Item 1 "Patents and Proprietary Rights"

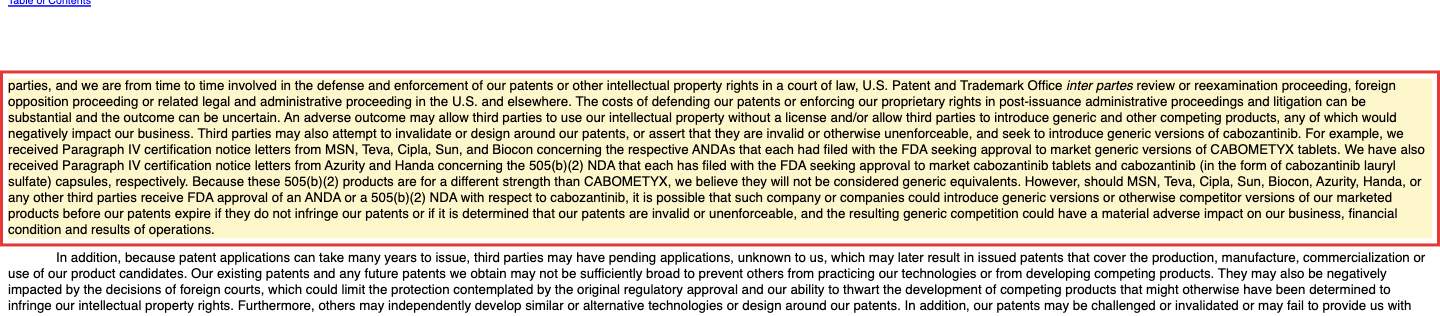

That it is serious is shown by the second passage: several generic makers have registered so-called Paragraph IV notices — the formal announcement that they have applied for a copycat version at the FDA:

"For example, we received Paragraph IV certification notice letters from MSN, Teva, Cipla, Sun, and Biocon concerning the respective ANDAs that each had filed with the FDA seeking approval to market generic versions of CABOMETYX tablets."

— Exelixis, Inc., SEC annual report 10-K 2025, Item 1A "Risk Factors" (Hatch-Waxman / ANDA)

But — and this is the honest nuance: the patent expiry of 2026 is not a cliff but a staircase

Here premature panic parts from careful reading. Whoever reads only the headline "composition-of-matter patent 2026" pictures a cliff: in 2026 protection falls, and afterward revenue plunges. But that is not how it works for cabozantinib. Beyond the expiring composition-of-matter patent, secondary patents protect the business — on certain salts and crystal forms (to 2030), on formulations (to 2032/2033) and on methods of use (to 2031/2032). And the decisive passage sits in the legal proceedings: a U.S. court in Delaware ruled in October 2024 that an FDA approval of the most important copycat (MSN) may not take effect before 2030:

"…the effective date of any such approval of MSN's ANDA shall not be a date earlier than January 15, 2030, the expiration date of each of the '439, '440, and '015 Patents, subject to our potential additional regulatory exclusivity."

— Exelixis, Inc., SEC annual report 10-K 2025, Note 12 "Commitments and Contingencies — Legal Proceedings"

Appraise that honestly. In favor: the feared crash does not come in 2026 but spreads over several years; Exelixis gains time to pass the baton. Against: the number of attackers is large, the outcome of patent lawsuits is never certain (the cases against MSN, Sun and Azurity were consolidated for a trial starting November 2026), and even a staircase leads downward. Remember: with a patent date, always check whether it is the core patent or a secondary one — otherwise you buy or sell on a cliff that is in truth a staircase.

Uncomfortable truth no. 3: the entire value leans on a runner who has not yet won a race

Here the circle to the relay race closes. If cabozantinib loses strength over the years, a successor must take over — and that successor is zanzalintinib. The good news: it is no longer a distant lab idea. In the STELLAR-303 trial in colorectal cancer it showed a statistically significant survival advantage over the comparator drug in 2025 (the risk of death fell by 20 percent), and in December 2025 Exelixis filed a marketing application (NDA) for it; the FDA has accepted it and set a decision date (PDUFA) for December 3, 2026. Further pivotal trials (such as STELLAR-304 in a form of kidney cancer) are expected to deliver results in 2026.

The uncomfortable truth behind it: to this day zanzalintinib has brought in not a single dollar of revenue. The entire premium the stock carries above pure asset value is a bet that the handover succeeds — that zanzalintinib is approved, widely used, and catches the revenue cabozantinib loses to generics after 2030. If an important trial fails or approval is delayed, the strong first runner keeps going to the finish, but no one stands ready to take the baton. A relay race is not won by a strong first runner alone — but by a clean handover.

Valuation: about $13.4 billion in market value — solid, but not cheap

In early July 2026 the Exelixis stock cost about $53; that yields a market value of about $13.4 billion (data as of July 8, 2026). The price-to-earnings ratio sits at about 18 — and here is the important difference from an optical bargain like Aurinia (price-to-earnings ratio 8): Exelixis' profit is real and recurring, and for that the stock is also fairly paid, no junk price. The price-to-sales ratio of about 6 and the price-to-book ratio of about 7 confirm it: the market pays here for quality, not for a discount. That Exelixis shows up in a value filter like the Magic Formula at all is due to the high return on capital (a low-debt, highly profitable company ties up little capital) — not to a low price. The analyst consensus (about 20 firms) is on average cautiously optimistic, but that is the "professionals' view" of the same relay race: they price in that cabozantinib carries for years yet and zanzalintinib takes over in time. These two assumptions are the real price of the stock — not today's numbers.

Opportunities and risks at a glance

What speaks for Exelixis:

- Real, recurring profitability: net product revenue from $1,628.9 (2023) to $2,122.8 million (2025), 2025 the ninth consecutive profitable year, net income $782.6 million — operationally earned, without one-off tax effects (annual report 10-K 2025, quarterly report 10-Q Q1 2026).

- A rock-solid balance sheet: about $1.66 billion in cash and investments (December 31, 2025), almost no debt (ratio about 0.09), Altman Z 10.74, Piotroski 8 of 9, EBIT margin and return on equity each about 41 percent — no distress; hits exclusively in value, quality and trend scanners.

- A patent staircase instead of a cliff: despite the 2026 composition-of-matter patent expiry, secondary patents defend into the early 2030s; the most important generic (MSN) may start no earlier than January 15, 2030 — Exelixis gains years for the transition.

- A real successor in approval: zanzalintinib showed a significant survival advantage in STELLAR-303 (colorectal cancer); the FDA has accepted the application, decision date December 3, 2026, further trial results expected in 2026.

- Shareholder-friendly capital policy: buyback programs totaling $1.75 billion; the international partners Ipsen and Takeda carry the foreign business and pay royalties.

What speaks against it:

- One-molecule concentration risk: 100 percent of product revenue hangs on cabozantinib; no second approved pillar, the successor zanzalintinib has no revenue yet.

- Patent and generic pressure: the composition-of-matter patent ends in August 2026, several ANDA makers (MSN, Teva, Cipla, Sun, Biocon) and two 505(b)(2) applicants stand ready; the outcome of the patent lawsuits (consolidated trial from November 2026) is open.

- Distribution concentration risk: two wholesalers (Cencora 22 percent, McKesson 19 percent) account for 41 percent of total revenue in 2025.

- A full, but not cheap, valuation: price-to-earnings ratio about 18, price-to-sales about 6, price-to-book about 7 — for a one-product business with transition risk, no safety discount (data as of July 8, 2026).

- State price pressure: the IRA exemption for cabozantinib runs only through the price year 2027 — after that, on top of generic competition, a Medicare price negotiation looms; the cash is shrinking at the same time through share buybacks.

A human conclusion

Back to the extrapolation reflex from the start. It has a true core: at Exelixis something really has succeeded that most biotechs never achieve — an active ingredient that throws off a profit nine years in a row, a debt-free balance sheet, a return on capital for which a value filter rightly lights up. The runner on the track is strong, and that is no illusion. But precisely here lurks the thinking error this case can show you: a straight line out of the past is no guarantee for the future when the future demands a handover. The entire value of the stock hangs on two questions that today's numbers do not answer: how gently does the patent staircase carry cabozantinib to 2030 and beyond — and does zanzalintinib take the baton in time? Unlike the hard cliff of some one-product biotechs, Exelixis has bought time and has a real successor in the race. But the relay race is won only with the handover, not with the lead. Whoever gets in here should do so because he considers the second runner strong enough — not because the first ran so beautifully evenly. What you make of it is your decision. And that is exactly as it should be.

Sources

All original documents used in this analysis — to read for yourself:

- Exelixis, Inc. — SEC annual report 10-K for fiscal year 2025 (filed February 10, 2026)

- Exelixis, Inc. — SEC annual report 10-K for fiscal year 2024 (filed February 11, 2025)

- Exelixis, Inc. — SEC quarterly report 10-Q as of April 3, 2026 (filed May 5, 2026)

- Exelixis, Inc. — SEC quarterly report 10-Q as of October 3, 2025 (filed November 4, 2025)

- Exelixis, Inc. — SEC quarterly report 10-Q as of July 4, 2025 (filed July 28, 2025)

- Exelixis, Inc. — SEC quarterly report 10-Q as of April 4, 2025 (filed May 13, 2025)

- Exelixis' complete SEC filing history: EDGAR overview (sec.gov)

- Fundamental data (metrics, quarterly series, valuation; data as of July 8, 2026), reconciled with the SEC filings.

- Screener and rating data: in-house stock scanner (data as of July 8, 2026).

Transparency & disclaimer: This analysis is a journalistic contextualization of publicly available information and is not investment advice, not a financial analysis in the regulatory sense, and not a solicitation to buy or sell securities. It expressly contains no judgment on whether a drug will be commercially successful, whether patents will hold up in court, or whether an approval will be granted. Stock investments carry substantial risks up to total loss — with biopharma stocks to a particular degree. All information without guarantee; the data cut-off is noted in the text in each case. The author holds no position in Exelixis stock at the time of publication.

Our Bottom Line at a Glance

- Product & growth positive

- Cabozantinib grows robustly: net product revenue from $1,628.9 (2023) to $2,122.8 million (2025, plus 17 percent), Q1 2026 $555.0 million. Carried above all by CABOMETYX plus nivolumab as first-line treatment in kidney cancer and the new indication of neuroendocrine tumors. The catch: it is a single molecule.

- Profitability & earnings quality positive

- Unlike many biotechs, Exelixis is sustainably profitable — 2025 the ninth consecutive profitable year, net income $782.6 million, EBIT margin and return on equity each about 41 percent. The profit is operationally earned, not dressed up by a one-off tax benefit. That is real substance.

- Balance sheet & financing positive

- About $1.66 billion in cash and investments (December 31, 2025), almost no debt, Altman Z 10.74, Piotroski 8 of 9 — no distress. Critical only: buyback programs totaling $1.75 billion draw down the war chest (cash fell from $1.75 to $1.66 billion) instead of hoarding it for the transition.

- Concentration risk & patent timeline negative

- 100 percent of product revenue hangs on cabozantinib; two wholesalers account for 41 percent of revenue. The composition-of-matter patent ends in August 2026, several generic makers stand ready. Honest nuance: secondary patents defend into the early 2030s, the MSN generic may start no earlier than January 15, 2030 — a cliff becomes a staircase, but the staircase leads downward.

- Successor & valuation neutral

- The entire premium of the stock hangs on zanzalintinib: in STELLAR-303 (colorectal cancer) a significant survival advantage, FDA decision date December 3, 2026 — but still no revenue. At a price-to-earnings ratio of about 18 the stock is fairly, not cheaply, paid (data as of July 8, 2026); the price is a bet on a successful baton handover.

Exelixis is a genuinely profitable oncology biopharma in the value scanner: cabozantinib (CABOMETYX) has driven revenue to $2,122.8 million, 2025 was the ninth consecutive profitable year, and $782.6 million remained at the bottom line — operationally earned. But 100 percent of product revenue hangs on this one molecule, the composition-of-matter patent ends in August 2026 (secondary patents and a court ruling, however, stretch protection to at least January 2030), and the entire premium of the stock is a bet on the still revenue-less successor zanzalintinib. A full war chest and a record profit meet a one-molecule business in transition. Not investment advice.

What Our Rating Means

- If you don't own the stock

- As long as the question raised in the bottom line stays open, we see no basis for an entry.

- If you hold it in your portfolio

- Our findings offer no acute reason to sell — the checkpoints named remain decisive.

A journalistic assessment by our editorial team at the time of the deep dive, based on public sources — not investment advice and not a solicitation to buy or sell. Your personal circumstances (investment goals, risk capacity, taxes) cannot be taken into account. What our categories mean, how verdicts are formed, and what conflicts of interest exist →

Worth Noting

- Membership in the value scanner "Joel Greenblatt: Magic Formula" (not a warning scanner) was confirmed live on July 14, 2026; EXEL shows up in 13 value, quality and trend scanners (among them Magic Formula, Buffett criteria, owner-earnings yield, QARP, EBIT-margin ranking, Weinstein Stage 2), in no warning scanner.

- All earnings and balance-sheet figures come from the audited annual report 10-K for fiscal year 2025 (filed February 10, 2026) as well as the quarterly report 10-Q as of April 3, 2026; the 2025 profit is operationally earned and contains no one-off tax effect.

- Price and valuation figures dated to July 8, 2026 (about $53, about $13.4 billion in market value); analyses are evergreen, daily prices are not a buy argument. The composition-of-matter patent on cabozantinib expires in August 2026, secondary patents reach into the early 2030s.

Frequently Asked Questions

Exelixis (Nasdaq: EXEL) is a profitable oncology biopharma from Alameda, California. Its core product is the active ingredient cabozantinib, sold as CABOMETYX (a tablet against kidney, liver and thyroid cancer as well as neuroendocrine tumors) and COMETRIQ (a capsule against thyroid cancer). Outside the United States the partners Ipsen and Takeda handle marketing. In development is the successor zanzalintinib.

Yes, and the profit is real: 2025 was the ninth consecutive profitable year. Net product revenue rose to $2,122.8 million, net income to $782.6 million ($2.78 per share, diluted). In the first quarter of 2026 net income was $210.5 million. Unlike at some other biotechs, this profit is operationally earned and not inflated by a one-off tax benefit.

The composition-of-matter patent on cabozantinib (U.S. Patent 7,579,473) expires in August 2026. But that is no cliff: secondary patents on salts, formulations and uses protect the franchise into the early 2030s. A U.S. court ruled in October 2024 that an approval of the most important generic (MSN) may take effect no earlier than January 15, 2030. Several copycats (MSN, Teva, Cipla, Sun, Biocon) have filed applications.

Exelixis shows up in value filters like the Magic Formula because it has a very high return on capital — a low-debt, highly profitable company ties up little capital. The price itself, however, is fair: the price-to-earnings ratio sits at about 18 (data as of July 8, 2026), no bargain. Unlike optically cheap stocks, the market pays here for quality and for the bet on a successful product handover to zanzalintinib.

Zanzalintinib (formerly XL092) is Exelixis' most important drug successor, a modern kinase inhibitor. In the STELLAR-303 trial in colorectal cancer it showed a significant survival advantage in 2025; Exelixis has filed a marketing application for it, which the FDA has accepted (decision date December 3, 2026). Since all revenue today hangs on cabozantinib, zanzalintinib decides the future — but it has not yet brought in any revenue.

No. In all six evaluated SEC filings (two annual reports 10-K, four quarterly reports 10-Q), artificial intelligence appears substantively only once — as a cyber risk, and with the note that AI software is used "in limited instances" internally as well. AI is neither product nor revenue source. In our company-specific AI classification, Exelixis is therefore rated "Neutral".

The facts speak clearly against it: about $1.66 billion in cash and investments (December 31, 2025), hardly any debt, a healthy Altman Z-score of 10.74, Piotroski 8 of 9 and a business profitable for nine years. The main risk is not solvency but the transition: all revenue hangs on cabozantinib, whose protection begins to crumble from 2030, while the successor zanzalintinib still has to prove itself.

Found an error?

Did you spot a factual error, an outdated number, or a typo in this deep dive? Let us know briefly — your report goes straight to the editorial team.