Eli Lilly Stock: One Trillion Dollars, One Molecule — and the Government Now Sits at the Table

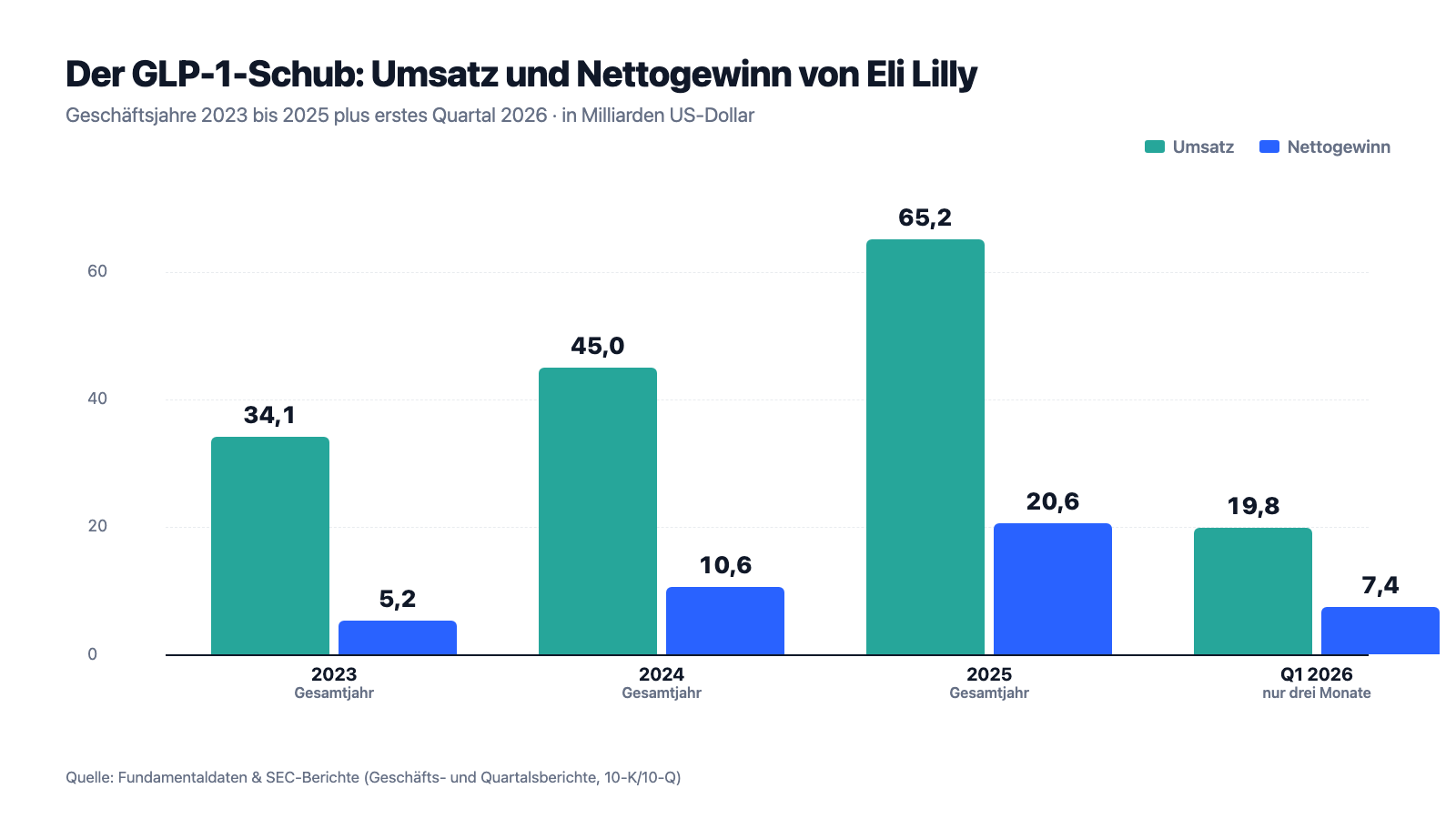

Eli Lilly is the most valuable pharmaceutical company in the world: $65.2 billion in revenue in 2025 (plus 45 percent), $20.6 billion in net income, and another plus 56 percent in the first quarter of 2026 — carried by the weight-loss and diabetes drugs Mounjaro and Zepbound. Our value scanner built on Joel Greenblatt's Magic Formula lists the stock among its hits. We read the annual report (10-K) and the latest quarterly report (10-Q): both blockbusters are one and the same compound — tirzepatide, lately 65 percent of revenue —, the U.S. government is already setting prices for the first Lilly products, and the patent clock is ticking at the predecessor Trulicity. Not investment advice — just a look at how much weight a single domino can carry.

There is a kind of stock at which the investor brain quietly switches off its inspection mode: the celebrated giant. A company that has existed for 150 years, whose products millions of people take and whose price has been climbing for years — an inner voice whispers: "You can't go wrong with one of these." Psychologists call this the halo effect: one radiant feature (size, success, fame) outshines everything you actually ought to check. Hardly any stock invites this reflex in 2026 as much as Eli Lilly (NYSE: LLY) — the pharmaceutical company from Indianapolis that the boom in weight-loss injections has turned into the first trillion-dollar pharma company in stock-market history. And this time even a serious tool nods along: our in-house stock scanner built on Joel Greenblatt's Magic Formula — a value filter that looks for good companies at fair prices, not a warning system — lists Lilly among its hits. So let's make a deal: before the halo effect decides for you, we read together what Lilly itself reported to the U.S. securities regulator, the SEC — in the annual report (10-K, the yearly mandatory filing) and the quarterly report (10-Q). Such filings are honest under penalty of law. And these particular ones contain three sentences about a single molecule, a negotiating government and a ticking patent clock that measure the halo rather precisely. In the end, you decide for yourself.

What Eli Lilly actually does

Eli Lilly was founded in Indianapolis in 1876 by the pharmacist and colonel Eli Lilly and for long stretches of the 20th century was above all one thing: the insulin company. Today the group employs about 50,000 people (roughly 12,000 of them in research) and sells medicines in about 90 countries — for diabetes and obesity, cancer (Verzenio), psoriasis (Taltz), migraine (Emgality) and Alzheimer's. So much for the portrait. Since 2022, though, the stock-market story has at its core consisted of a single word: tirzepatide. That is a so-called incretin — translated: a satiety-hormone mimic. The compound imitates two of the body's own messengers at once (GLP-1 and GIP) that signal "full" to the brain and regulate blood sugar. One molecule, two labels: as Mounjaro, tirzepatide is sold against type 2 diabetes; as Zepbound, against obesity. Sounds like marketing? It partly is — but behind it stands the biggest new drug market in decades, in which Lilly and its Danish rival Novo Nordisk share a de facto duopoly. And Lilly is adding to it: in April 2026 the U.S. drug regulator FDA approved Foundayo (orforglipron) — the first weight-loss pill of this class, which needs neither syringe nor refrigerator.

Note the central tension right away — it is the connecting thread of this analysis: Eli Lilly delivers the best growth in big pharma — but two thirds of it hang on a single molecule whose price is set less and less by the market and more and more at the negotiating table. A company town in which every second paycheck comes from a single factory can live splendidly. It just ought to know what happens when the factory coughs.

Where the stock shows up in our scanner

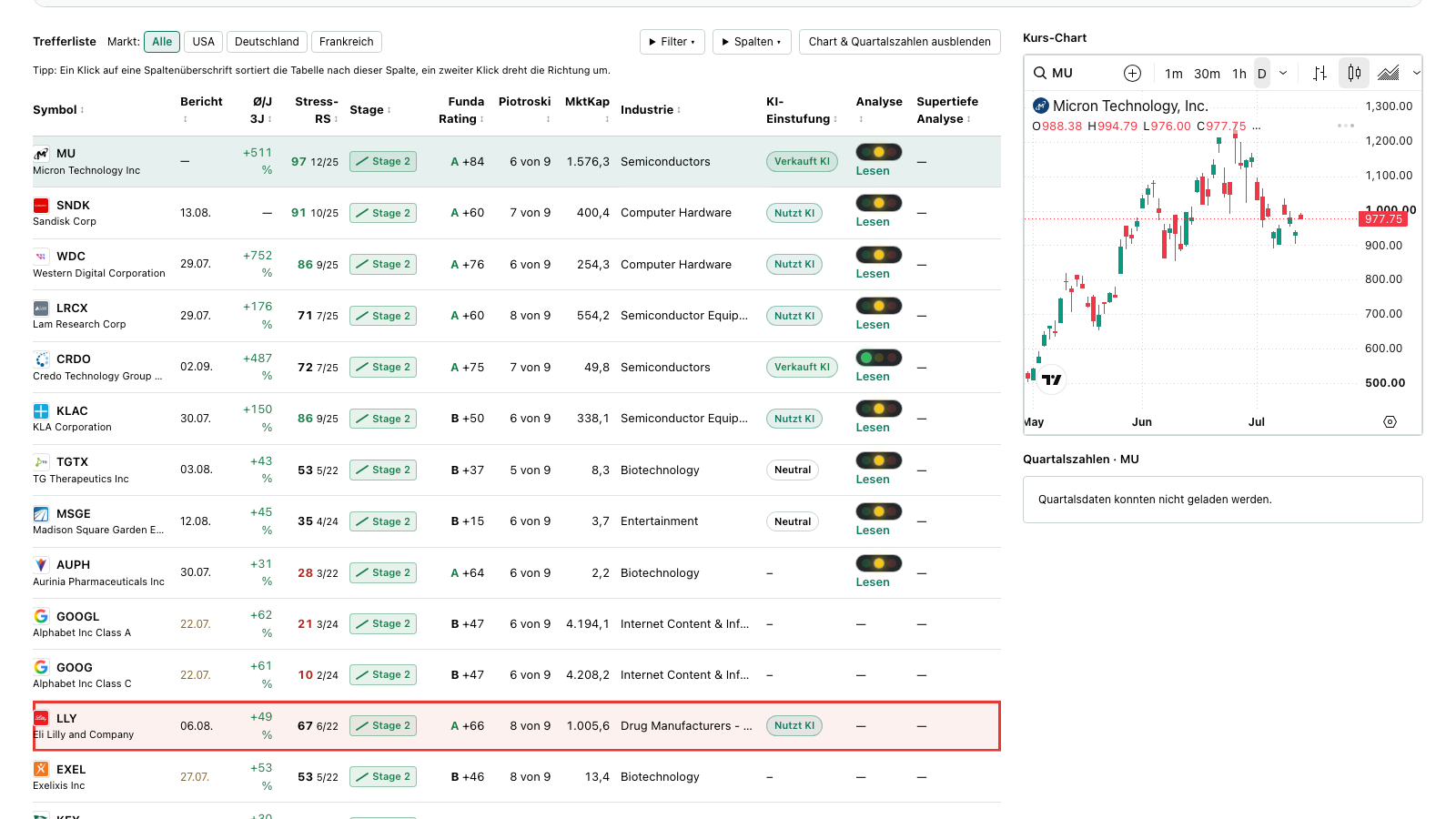

Every day we run about 3,500 stocks through our scanners. Eli Lilly lights up in five filters in our evaluation (data as of July 8, 2026) — and not a single one of them is a warning scanner. The most interesting hit is the Magic Formula of value investor Joel Greenblatt. His idea in one sentence: buy above-average companies at a reasonable price — measured by return on capital (how much operating profit per dollar of working capital employed?) and earnings yield (how much operating profit per dollar of enterprise value?). Lilly qualifies via the quality track: the EBIT margin sits around 49 percent, the return on equity is in the triple digits. Added to that are hits in the Levermann ranking, in "Martin Zweig: growth with reason", in the EBIT-margin ranking and in the "Altman-Z: balance-sheet fortress" (our live check on July 14, 2026 additionally brought up dividend and growth scanners). The individual grades, translated: the Piotroski F-Score, a nine-point test of balance-sheet quality, stands at 8 of 9 — genuinely good, a thoroughly healthy company. The Altman-Z score, a classic early warning of insolvency, sits at a relaxed 7.3 (it gets critical below 1.8). The fundamental rating stands at A. In short: the scanner sees a model student. What a scanner cannot see: where the shiny numbers come from — and how many eggs sit in one basket for them.

One footnote for context: unlike the memory-chip cyclical Micron, which the same formula currently catches at its earnings peak, Lilly is no cyclical — demand for medicines does not swing with the business cycle. The Greenblatt weakness looks different here: the formula measures today's earning power and knows nothing of patent calendars, price negotiations and concentration risks. That is exactly what the mandatory filings are for.

The numbers over the years — honestly appraised

First, what genuinely impresses — and at Lilly that is a lot. Group revenue jumped from $34.1 billion (2023) via $45.0 billion (2024, plus 32 percent) to $65.2 billion (2025, plus 45 percent). Net income quadrupled in two years: from $5.2 via $10.6 to $20.6 billion (plus 95 percent in 2025). And the pace holds: in the first quarter of 2026 revenue grew 56 percent to $19.8 billion, net income 168 percent to $7.4 billion — earnings per share rose from $3.06 to $8.26. The gross margin stood at 83 percent in 2025; operating cash flow nearly doubled in 2025 to $16.8 billion. For a company of this size, such growth rates are simply extraordinary — for perspective: in 2025 Lilly grew, in percentage terms, roughly as fast as many a start-up, only from a $45 billion base. Whoever hears only bubble talk here is not doing the numbers justice.

The use of the windfall is presentable too: in 2025, $13.3 billion flowed into research (plus 21 percent), $7.8 billion into new plants (after $5.1 billion in 2024 — and the report announces significantly higher investment), $4.1 billion into share buybacks and $5.4 billion into dividends; the quarterly dividend was raised to $1.73 at the start of 2026. The flip side is in the balance sheet as well: total debt rose within one year from $33.6 to $42.5 billion ($43.4 billion as of March 31, 2026), against $5.3 billion in cash plus $3.3 billion in securities. Growth, factories, acquisitions, buybacks and a dividend all at once — even at Lilly, that only works with borrowed money. It is solid nonetheless: interest coverage is ample, the Altman-Z score stands at 7.3. The filings pose the exciting questions elsewhere.

What the filings say — the uncomfortable truths

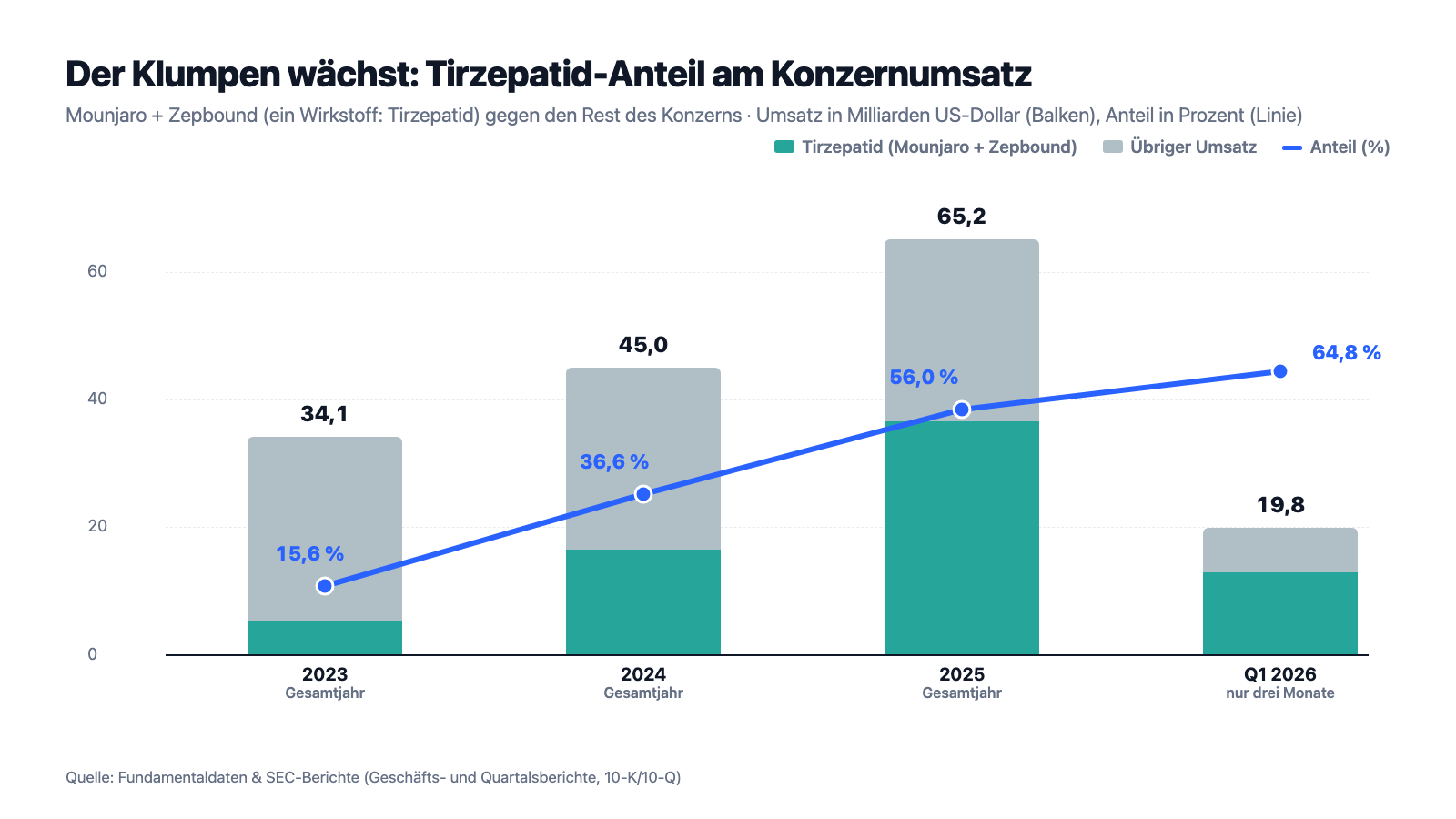

Uncomfortable truth no. 1: two brands, one molecule — 65 percent of revenue hangs on tirzepatide

Mounjaro and Zepbound sound like two legs to stand on. Chemically they are the same leg. The annual report makes no secret of it — it lists the concentration itself as a risk factor:

"We derived direct product and/or collaboration and other revenues of more than $3 billion for each of Mounjaro, Zepbound, Verzenio, Trulicity, Taltz, and Jardiance (including Glyxambi, Synjardy, and Trijardy XR) that collectively accounted for 82 percent of our total revenues in 2025. In particular, Mounjaro and Zepbound accounted for 56 percent of our total revenues in 2025, and we expect cardiometabolic health products will continue to represent a significant and growing portion of our business, revenues, and prospects."

— Eli Lilly, SEC annual report 10-K 2025, Item 1A "Risk Factors"

And the concentration is growing: in the latest quarterly report the 56 percent have already become 65 percent (three months through March 31, 2026: Mounjaro $8.7 billion, plus 125 percent; Zepbound $4.2 billion, plus 80 percent). You may know customer concentration from small companies — at our Greenblatt neighbor TG Therapeutics, 98 percent hangs on one drug. But a trillion-dollar company whose valuation exceeds Novo Nordisk, Pfizer, Merck and AstraZeneca combined, hanging by two thirds on one compound — that is historically fairly unique. In fairness: the cluster is not one customer but a world market with billions of potential patients, and Lilly is actively broadening it (the Foundayo pill, cardiovascular approvals, trials from sleep apnea to fatty liver). Still: every piece of news about tirzepatide — a side-effect study, a rival product, a pricing decision — now moves two thirds of the business. The company's own report names the possible consequence: "significant and sudden declines or volatility" of the stock price and market value.

Uncomfortable truth no. 2: the government now sits at the price tag — and Lilly itself expects "accelerating revenue erosion"

To investors, American drug prices long counted as a nature preserve. That is over. Since the Inflation Reduction Act (IRA) of 2022, the U.S. Department of Health and Human Services (HHS) may effectively set prices for high-revenue Medicare drugs — for pills as early as nine years after approval, for biologics after thirteen. Lilly has already experienced what that means in practice: for Jardiance, a government-set price applies from 2026 — 66 percent below the 2023 list price. And the calendar is filling up:

"In January 2026, HHS selected Trulicity and Verzenio as additional medicines subject to government-set prices to be effective in 2028. Given our product portfolio, we expect additional of our significant products will be selected in future years, which would have the effect of accelerating revenue erosion prior to expiry of exclusivities."

On top comes a second, brand-new channel: in November 2025 Lilly concluded voluntary agreements with the U.S. government — finalized in the first quarter of 2026. Their content per the quarterly report: lower Medicaid prices, more balanced pricing across developed markets for new medicines (translated: America is no longer supposed to subsidize the world's research on its own — so lower U.S. prices or higher prices elsewhere), discounted Lilly weight-loss drugs for Medicare beneficiaries from July 1, 2026 (the "Bridge Program"), a government direct-purchase platform with substantial discounts to list prices — and in return three years of grace from possible pharma tariffs, provided Lilly keeps its U.S. factory commitments. You can read that as smart peacekeeping: Lilly buys itself predictability and at the same time opens the huge Medicare market for Zepbound. But you must also see the direction: this company's prices, rebates and even tariffs increasingly come into being in negotiations with governments. For the Magic Formula that is invisible — it measures yesterday's margins, not tomorrow's bargaining power. And the IRA has one more punchline: for pills, government price-setting kicks in after just nine years. Of all products, Foundayo — the new weight-loss pill and Lilly's most important bet on the future — falls under this shorter deadline; the company's own report dryly notes that the nine-year rule diminishes the appeal of investing in small molecules.

Uncomfortable truth no. 3: the patent clock — Trulicity is showing live what expiry looks like

Pharma business models have a built-in expiration date: when patent and data protection end, the branded product turns into a commodity overnight — generic and biosimilar makers copy legally, prices collapse. The annual report says so with a candor you have to credit — right under the heading stating that the loss of protections has led to rapid and severe revenue declines in the past and is expected to keep doing so:

"In the ordinary course of their lifecycles, our products lose significant patent protection and/or data protection after a specified period of time. For example, Trulicity will lose significant patent and remaining data protections in the next few years."

— Eli Lilly, SEC annual report 10-K 2025, Item 1A "Risk Factors — Risks Related to Our Intellectual Property"

You can watch what that feels like live in the same filings: Trulicity, Lilly's GLP-1 predecessor, still brought in $7.1 billion in 2023, only $4.3 billion in 2025 — in the first quarter of 2026, revenue fell another 16 percent. The U.S. compound patent expires in 2027 per the report, and on top of that HHS has selected the product for government price-setting from 2028: cliff and price cap at once. At the crown jewel tirzepatide, the calendar looks friendlier — compound patent in the United States until 2036, Europe 2037, Japan 2040. But one line in the patent table deserves attention: U.S. data exclusivity for tirzepatide ends as early as 2027. That does not open the generics floodgates immediately (the compound patent remains), but it lets imitators base their approval applications on Lilly's trial data — and the report lists several routes by which patents can fall early: Hatch-Waxman lawsuits, IPR proceedings at the patent office, rich incentives for generic makers — attacks on the U.S. patents of major products, it says in substance, are routine. Ten years of protection sounds long. Against a valuation that prices in decades of growth, it is not.

Uncomfortable truth no. 4: copies, gatekeepers and the rebate scissors — between list price and cash register lies half a company

The fourth truth is about everything that happens between the prescription pad and Lilly's account. First: the copies. During the tirzepatide shortage of 2022 through 2024, U.S. compounding pharmacies were legally allowed to sell remixed versions — the emergency backdoor became a barn door through which a gray billion-dollar market emerged. The shortage has been officially over since late 2024 per the FDA, mass production prohibited. But the latest quarterly report sounds anything but relaxed:

"We continue to see the production, marketing, and sale of counterfeit, misbranded, adulterated, and mass-compounded incretins. These practices may impact patient safety and undermine regulatory drug approval processes. While the FDA confirmed in late 2024 that the previous shortage of tirzepatide had ended and that compounding pharmacies are required to cease mass production, we cannot guarantee adequate regulation or compliance."

— Eli Lilly, SEC quarterly report 10-Q as of March 31, 2026, Item 2 MD&A "Executive Overview — Incretin Medicines"

Second: the gatekeepers. Between Lilly and patients in the United States stand pharmacy benefit managers (PBMs) — the insurers' rebate negotiators who decide which drug makes the preferred list (the "formulary"). How much power that is stands soberly in the 10-K: in July 2025, CVS Caremark, the biggest of these gatekeepers, removed Zepbound as a preferred weight-loss drug on some insurance plans — in favor of the rival product. A single negotiating partner can thus reroute millions of patients. Third: the rebate scissors. Between list price and actual proceeds lies an entire rebate system in the United States — for the most important U.S. programs alone, Lilly deducted about $62 billion in rebates and discounts from gross revenue in 2025, almost as much as the entire reported group revenue. Realized prices per unit are already falling: the quarterly report expressly attributes the revenue gain to volume, partially offset by lower realized prices — in the United States as internationally (in China, for instance, Mounjaro made it onto the national reimbursement list NRDL, against a hefty price concession). And on the margins run the product-liability mass proceedings: two multidistrict litigations (MDLs) over alleged gastrointestinal and optic-nerve injuries from incretins are collecting lawsuits against Lilly and Novo Nordisk — at a company that is largely self-insured for liability cases, as the report notes. Remember: Lilly's boom is a volume boom at falling net prices. That is healthier than the reverse — as long as volume keeps exploding.

Valuation: one trillion dollars — what you pay for is the decade, not the year

In early July 2026, Eli Lilly stock cost about $1,128; that makes a market value of about $1,006 billion — the first trillion in pharma history (all valuation figures: data as of July 8, 2026). For that you get, as of today: a price-to-earnings ratio of about 43, a price-to-sales ratio of about 14, a price-to-book ratio of about 32 and about 49 times operating cash flow. For perspective: classic pharma giants such as Pfizer or Merck traditionally trade at 10 to 15 times earnings — Lilly is priced more like a software growth stock. The optimists' counter-calculation: if profit grows as the professionals expect (31 analysts, consensus clearly at "buy"; for 2026 about $36 in adjusted earnings per share, for 2027 about $44), the price-to-earnings ratio falls to roughly 31 and then 25 — no moon price for sustained double-digit growth. And exactly there lies the core: what is paid for is not the record year 2025 but a whole decade of continued success — Foundayo must become a blockbuster, Medicare volumes must overcompensate the rebates, retatrutide and company must deliver, and neither price regulators nor copies nor the duopoly rival may crash the party. The dividend yield of about 0.6 percent ($6.92 annual rate in 2026) is, at this price, more symbol than argument. Still: unlike many a high-flyer, real, growing cash flows stand behind this — $16.8 billion operating in 2025. It is not a house of cards. It is a very solid house with a very athletic price tag, built on a single foundation stone.

Opportunities and risks at a glance

What speaks for Eli Lilly:

- A duopoly in the biggest new drug market in decades: tirzepatide grows at triple-digit rates (Mounjaro +125 percent, Zepbound +80 percent in Q1 2026), Mounjaro has been launched in all major international markets, and Medicare access from July 2026 opens another mass market (10-Q as of March 31, 2026).

- The pipeline delivers: Foundayo (orforglipron), the first weight-loss pill, was approved by the FDA in April 2026; behind it stand retatrutide, eloralintide and trials from type 1 diabetes via sleep apnea to fatty liver — plus acquisitions (pending in 2026: up to about $12 billion).

- Outstanding metric quality: 83 percent gross margin, EBIT margin about 49 percent, $16.8 billion operating cash flow 2025, Piotroski 8 of 9, Altman-Z 7.3, fundamental rating A — the Greenblatt hit comes from real earning power, not a balance-sheet trick (data as of July 8, 2026).

- Shareholder-friendly capital allocation from a position of strength: $13.3 billion in research (+21 percent), $7.8 billion in factory investment, plus a dividend raise to a $6.92 annual rate for 2026 and ongoing buybacks ($15 billion program; 10-K 2025).

- The November 2025 agreement with the U.S. government creates predictability: Medicare access for weight-loss drugs, three years of tariff grace in exchange for U.S. investment commitments — Lilly has contractually secured its political peace (10-K 2025; 10-Q as of March 31, 2026).

What speaks against it:

- Extreme concentration: Mounjaro + Zepbound = one molecule = 56 percent of revenue in 2025, 65 percent in Q1 2026; the top-6 products stand for 82 percent — the company's own risk factor warns of "significant and sudden" stock-price declines on bad news (10-K 2025).

- Prices increasingly come into being politically: Jardiance at a government-set price from 2026 (minus 66 percent), Trulicity and Verzenio from 2028, more products per Lilly expected — with "accelerating revenue erosion prior to expiry of exclusivities"; plus lower Medicaid prices and international price alignment from the government agreement (10-K 2025).

- Patent and copy risks: Trulicity loses significant protections "in the next few years" (U.S. compound patent 2027) and shows live what erosion looks like ($7.1 to $4.3 billion since 2023); tirzepatide's U.S. data exclusivity ends in 2027; mass-compounded incretins remain an uncontrolled nuisance per the 10-Q.

- Middleman power and falling net prices: CVS Caremark removed Zepbound from preferred lists in July 2025; realized prices are falling in the United States and internationally (China NRDL), and between list price and cash register lay about $62 billion in rebates in 2025 (10-K 2025; 10-Q as of March 31, 2026).

- A demanding valuation with rising debt: price-to-earnings ratio about 43, price-to-book about 32, market value about $1,006 billion (data as of July 8, 2026); debt rose within five quarters from $33.6 to $43.4 billion, while product-liability mass lawsuits (the incretin MDLs) run with no meaningful insurance cover.

A human conclusion

Back to the halo effect. The treacherous thing about it: it is usually right — until the one time it is expensively wrong. Eli Lilly really is an extraordinary company: the fastest growth in big pharma, a research machine that has just brought the first weight-loss pill through the FDA, balance-sheet grades straight from the textbook. The Greenblatt scanner made no mistake here. But the halo has three documented dents, and all three stand not in forums but in Lilly's own mandatory filings: two thirds of the business hang on one molecule. The industry's most important customer — the government — now sits at the price tag and will, per Lilly itself, keep "accelerating revenue erosion". And the patent clock that is audibly striking at Trulicity is ticking for tirzepatide too — 2036 sounds far away, but it is closer than the decade the price has already paid for. Whoever holds or buys the stock is not betting on a house of cards but on the opposite: that an excellently run company broadens its cluster faster than politics, patents and copies can grind it down. That can work out very well. It is just a bet — not a certainty, even if the halo effect makes it feel like one. The filings hand you both halves of the truth; which one you give more weight is your decision. And that is exactly as it should be.

Sources

All original documents used in this analysis — for your own reading:

- Eli Lilly and Company — SEC annual report 10-K for fiscal year 2025 (filed February 12, 2026)

- Eli Lilly and Company — SEC annual report 10-K for fiscal year 2024 (filed February 19, 2025)

- Eli Lilly and Company — SEC quarterly report 10-Q as of March 31, 2026 (filed April 30, 2026)

- Eli Lilly and Company — SEC quarterly report 10-Q as of September 30, 2025 (filed October 30, 2025)

- Eli Lilly and Company — SEC quarterly report 10-Q as of June 30, 2025 (filed August 7, 2025)

- Eli Lilly and Company — SEC quarterly report 10-Q as of March 31, 2025 (filed May 1, 2025)

- Complete SEC filing history of Eli Lilly: EDGAR overview (sec.gov)

- Fundamental data (metrics, valuation, analyst consensus; data as of July 8, 2026), reconciled with the SEC filings.

- Screener and rating data: in-house stock scanner (data as of July 8, 2026; scanner membership checked live on July 14, 2026).

Transparency & disclaimer: This analysis is a journalistic contextualization of publicly available information and is not investment advice, not a financial analysis in the regulatory sense and not a solicitation to buy or sell securities. Stock investments involve substantial risks up to total loss. All information without guarantee; the data cut-off is noted in the text. The author holds no position in Eli Lilly shares at the time of publication.

Our Bottom Line at a Glance

- Growth & pipeline positive

- Revenue plus 45 percent in 2025 ($65.2 billion), plus 56 percent in Q1 2026 — the fastest growth in big pharma. The pipeline delivers: Foundayo (the first weight-loss pill) approved in April 2026, behind it retatrutide, eloralintide and broad indication expansions for tirzepatide (10-K 2025; 10-Q as of March 31, 2026).

- Earning power & balance-sheet quality positive

- 83 percent gross margin, EBIT margin about 49 percent, $16.8 billion operating cash flow in 2025, Piotroski 8 of 9, Altman-Z 7.3, fundamental rating A — the value-scanner hit rests on real earning power (data as of July 8, 2026).

- Concentration on one molecule negative

- Mounjaro and Zepbound are the same compound (tirzepatide) and stood for 56 percent of revenue in 2025 and 65 percent in Q1 2026; the top-6 products for 82 percent. The company's own risk factor warns of "significant and sudden" stock-price declines on bad news about these products (10-K 2025).

- Price regulation & patent protections negative

- Government-set prices hit Jardiance from 2026 (minus 66 percent), Trulicity and Verzenio from 2028 — more products expected per Lilly, with accelerated revenue erosion before exclusivities expire. Trulicity loses its U.S. compound patent in 2027 and shows live how fast revenues fall ($7.1 to $4.3 billion since 2023); tirzepatide's U.S. data exclusivity ends in 2027, and copies remain a running theme (10-K 2025; 10-Q as of March 31, 2026).

- Valuation & debt neutral

- About $1,006 billion in market value, P/E about 43, P/B about 32 (data as of July 8, 2026) — on the 2027 consensus estimate the P/E falls to about 25, provided growth holds. Debt rose within five quarters from $33.6 to $43.4 billion; the dividend (yield ~0.6 percent) and buybacks run in parallel with the giant factory build-out.

Eli Lilly is the rare case in which the halo effect is almost right: the best growth in big pharma, outstanding margins, a delivering pipeline and balance-sheet grades straight from the textbook. But the trillion-dollar valuation prices in a decade of continued success — and the company's own mandatory filings document three structural dents: 65 percent of revenue hangs on a single molecule, the government is already setting prices for the first Lilly products and expressly expects to select more, and the patent clock is running — audibly at Trulicity, until 2036 at tirzepatide, with U.S. data exclusivity only until 2027. Quality is not the question here; the price of that quality is. Not investment advice.

What Our Rating Means

- If you don't own the stock

- At the current price level, we don't see a sufficient margin of safety for an entry.

- If you hold it in your portfolio

- Our findings offer no reason to sell.

A journalistic assessment by our editorial team at the time of the deep dive, based on public sources — not investment advice and not a solicitation to buy or sell. Your personal circumstances (investment goals, risk capacity, taxes) cannot be taken into account. What our categories mean, how verdicts are formed, and what conflicts of interest exist →

Worth Noting

- Price and valuation figures dated July 8, 2026 (about $1,128 per share, about $1,006 billion in market value); analyses are evergreen, daily prices are not a buy argument.

- The Q1 2026 figures ($19.8 billion in revenue, $7.4 billion in net income) are three-month values; growth rates refer to the prior-year quarter. The Mounjaro/Zepbound U.S. revenue for Q1 2026 also contains a favorable one-off effect from adjusted rebate estimates (10-Q as of March 31, 2026).

- Analyst estimates (about $36 and $44 in adjusted earnings per share for 2026 and 2027; 31 professionals, consensus toward "buy") are forecasts, not facts — and with politically negotiated prices, especially prone to revision.

- Scanner membership: local evaluation with data as of July 8, 2026 (Greenblatt, Levermann, Zweig, EBIT-margin ranking, Altman-Z); checked live on July 14, 2026 — Greenblatt confirmed, additionally dividend and growth scanners.

Frequently Asked Questions

Eli Lilly (NYSE: LLY) of Indianapolis, founded in 1876, is the most valuable pharmaceutical company in the world. It develops and sells medicines for diabetes and obesity (Mounjaro, Zepbound, Trulicity, and since April 2026 the pill Foundayo), cancer (Verzenio), psoriasis (Taltz), migraine and Alzheimer's. In 2025 Lilly posted $65.2 billion in revenue — 45 percent more than the year before.

Tirzepatide is an incretin — a compound that mimics the satiety and blood-sugar messengers GLP-1 and GIP. Lilly sells the same molecule under two brands: as Mounjaro for type 2 diabetes ($23.0 billion in revenue in 2025) and as Zepbound for obesity ($13.5 billion). Together the two stood for 56 percent of group revenue in 2025 and 65 percent in the first quarter of 2026.

Joel Greenblatt's Magic Formula looks for companies with a high return on capital and a high earnings yield. Lilly qualifies through its extraordinary earning power: an EBIT margin of about 49 percent, an 83 percent gross margin, a Piotroski score of 8 of 9 (data as of July 8, 2026). The formula's weakness: it measures today's earning power and sees neither concentration risks nor patent calendars nor government price negotiations.

Very: both brands are chemically the same compound (tirzepatide) and stood for 56 percent of group revenue in 2025 and 65 percent in the first quarter of 2026; the six biggest products together for 82 percent (2025). The company's own annual report warns that bad news about these products can lead to "significant and sudden" stock-price declines.

Since the Inflation Reduction Act, the U.S. Department of Health and Human Services (HHS) sets prices for selected Medicare drugs: Jardiance from 2026 (66 percent below the 2023 list price), Trulicity and Verzenio from 2028. Per its annual report, Lilly expects more of its products to follow — and with them "accelerating revenue erosion". On top comes an agreement with the U.S. government: lower Medicaid prices, Medicare rebates for weight-loss drugs from July 2026, international price alignment.

Per the annual report, Trulicity will lose significant protections "in the next few years" (U.S. compound patent 2027) — its revenue already fell from $7.1 billion (2023) to $4.3 billion (2025). Tirzepatide (Mounjaro/Zepbound) is protected by its compound patent until 2036 in the United States, 2037 in Europe and 2040 in Japan; the shorter U.S. data exclusivity, however, ends as early as 2027.

Foundayo is Lilly's new weight-loss pill with the compound orforglipron — approved by the FDA against obesity in April 2026. As a pill it needs neither syringe nor cold chain and is easier to produce at scale. One catch from the annual report: for pills the U.S. price authority may set government prices as early as nine years after approval, for biologics only after thirteen.

Measured against classic pharma yardsticks, yes: a price-to-earnings ratio of about 43, price-to-sales of about 14, price-to-book of about 32 at about $1,006 billion in market value (data as of July 8, 2026). Based on analyst estimates for 2027 (about $44 in adjusted earnings per share), the P/E would fall to about 25 — so what is being paid for is sustained high growth, not the level already achieved.

Found an error?

Did you spot a factual error, an outdated number, or a typo in this deep dive? Let us know briefly — your report goes straight to the editorial team.