Aurinia Stock: A Profitable Lupus Biotech at a P/E of 8 — and a Patent Clock That Rings in October 2027

Aurinia sells a single drug — LUPKYNIS, the first approved tablet against the kidney inflammation caused by lupus — and is thus the rare, genuinely profitable biotech in our value scanner built on Joel Greenblatt's Magic Formula. Revenue climbed from $158.5 million (2023) to $271.3 million (2025), operating income swung into the black, and the price-to-earnings ratio sits at about 8. We read the annual report (10-K) for 2025 and the quarterly report (10-Q) as of March 31, 2026: a third of the record profit is a one-time tax benefit, all of the revenue hangs on this one drug — and the composition-of-matter patent expires in 2027, with eight generic drugmakers already waiting. A cash count that tells a cheap price-to-earnings ratio from a genuine bargain.

There is a reflex that lulls us investors into a sense of safety at exactly the moment we should be alert: call it the calendar blind spot. We are excellent at reacting to what lies directly in front of us — and astonishingly bad at taking seriously a danger that carries a fixed date in the future. A restaurant with a first-class kitchen, full tables, gleaming numbers — and at city hall, the demolition permit for a specific day has long been on file. The guests keep booking as if that day would never come. Exactly this blind spot is what Aurinia Pharmaceuticals (Nasdaq: AUPH) is serving right now: a biopharma that after years of losses finally earns real money, whose stock looks strikingly cheap at a price-to-earnings ratio of about 8 — and which shows up as a rare exception in a value scanner, the place where solid, inexpensive companies usually stand, not the usual biotech wobblers. Everything signals: "Someone here is making real money, and at a bargain price." So let's make a deal: before you let the low price-to-earnings ratio seduce you, we read together what Aurinia itself reported to the U.S. securities regulator, the SEC — in the annual report (10-K) for 2025 and the quarterly report (10-Q) as of March 31, 2026. An SEC filing is honest under penalty of law. And this one contains a date the calendar blind spot likes to overlook. In the end, you decide for yourself.

What Aurinia actually does

In the autoimmune disease lupus, the immune system — normally the body's guard force — mistakenly attacks the body's own tissue. When it hits the kidneys, doctors speak of lupus nephritis (LN): a kidney inflammation that, untreated, can lead all the way to kidney failure. Aurinia's drug LUPKYNIS (active ingredient voclosporin) dampens this misdirected immune response. The special part, and the actual selling advantage: it is the first oral therapy approved by the U.S. drug regulator FDA — that is, a tablet — for active lupus nephritis. It reached the market in January 2021; outside the United States, the Japanese partner Otsuka markets it (for Europe and Japan). Aurinia itself is legally seated in Alberta (Canada) but runs its business out of Rockville in the U.S. state of Maryland, with a lean 128 employees (as of December 31, 2025).

And here is the peculiarity that carries this analysis: unlike most biotechs we write about, Aurinia is no longer a perpetually loss-making research shop — it earns real money, and not just on paper but operationally. The pipeline behind it is modest: aritinercept (formerly AUR200), a drug candidate that blocks two immune messengers at once (the specialists call them BAFF and APRIL) and is meant to help against further autoimmune diseases — still in clinical development, so without revenue. Sounds like the successful leap from lab to pharmaceutical company? In part, it is. But note the central tension of this analysis right now: a genuinely profitable biotech with a strikingly low price-to-earnings ratio — whose 2025 profit, however, is one-third a one-time tax entry, whose revenue hangs 100 percent on a single drug, and whose most important patent expires in October 2027. It runs through every chapter. How quickly a one-product biotech becomes vulnerable is shown, for comparison, by our analysis of TG Therapeutics — there it is a tax effect and overpowering competition, here a ticking patent clock.

Where the stock shows up in our scanner

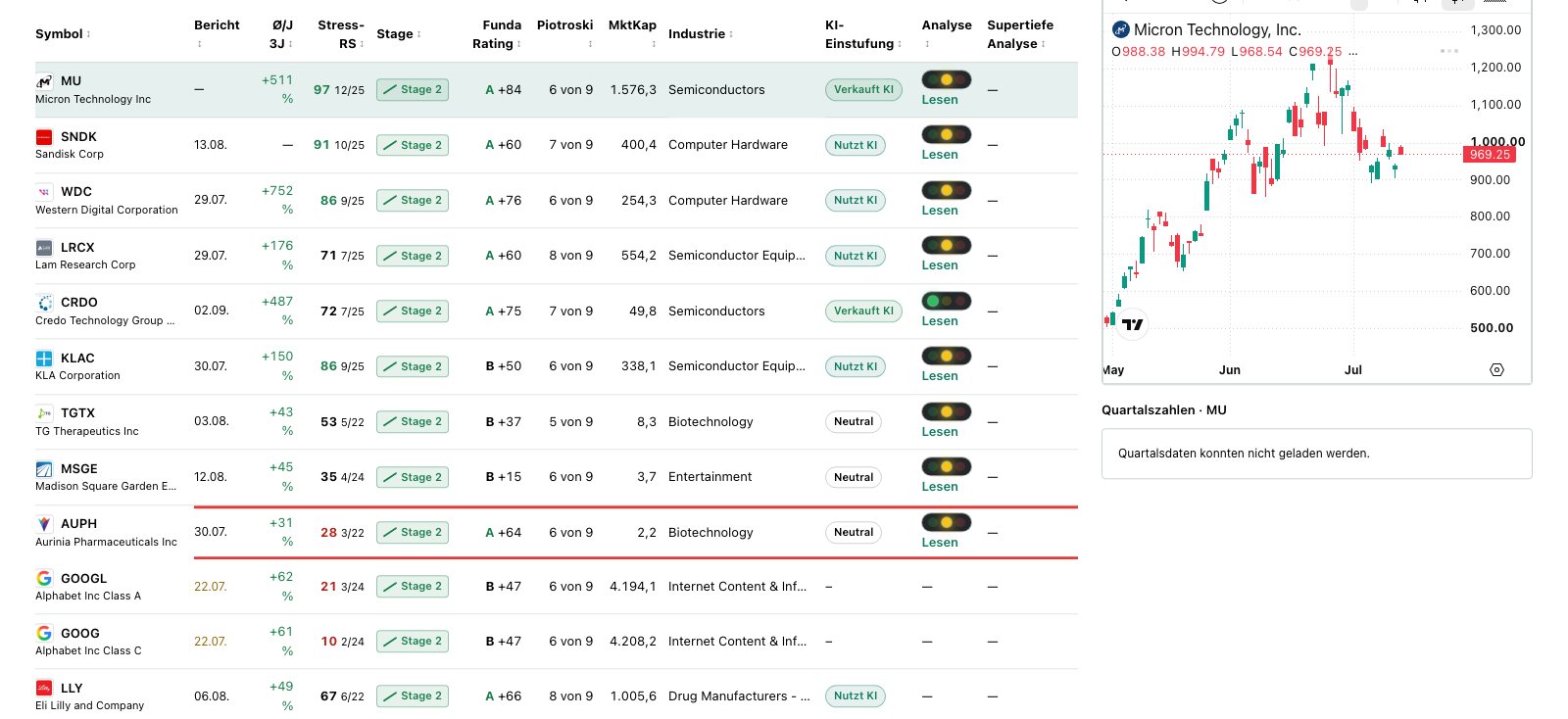

Every day we run about 3,500 stocks through our scanners. Aurinia lights up in 7 filters (data as of July 8, 2026) — and this time not a single warning scanner is among them. The most interesting hit is the Magic Formula of value investor Joel Greenblatt. His idea, in everyday language: buy good companies at a fair price — measured by two numbers. First, the return on capital (how much operating profit comes out per dollar of operating capital employed?); second, the earnings yield (how much operating profit do I get per dollar of enterprise value?). Add hits in further quality and value scanners: "quality stocks", "Buffett criteria", "Buffett: owner-earnings yield", the EBIT-margin ranking, the P/E ranking and "Peter Lynch: PEG ≤ 1". The hard balance-sheet metrics confirm the clean picture: Altman Z-Score 9.18 (a classic early warning of insolvency — danger begins only below 1.8, so this is deep green), Piotroski F-Score 6 of 9 (a nine-point balance-sheet test — 6 is solid, not outstanding), fundamental rating A. About $398 million in cash and investments (December 31, 2025) and very low debt round out the picture. No distress, no going-concern doubt — unlike many of the biotechs we usually dissect here.

Before you read that as a free pass, you have to know the best-known weakness of the Magic Formula — Greenblatt himself never concealed it: the formula calculates with the last reported earnings. If that profit is inflated by a special effect, the stock looks "cheaper" than the underlying business supports. That is exactly the case at Aurinia — more on that in a moment. And one more thing the scanner cannot do: all seven filters judge the past and the present — today's returns, margins, balance-sheet quality. Not one of them looks into the calendar, where October 2027 marks the expiry of the core patent. The filter is a good metal detector. Whether the signal is gold or a tin can with an expiry date is revealed only by digging. Let's start digging.

The numbers over the years — honestly appraised

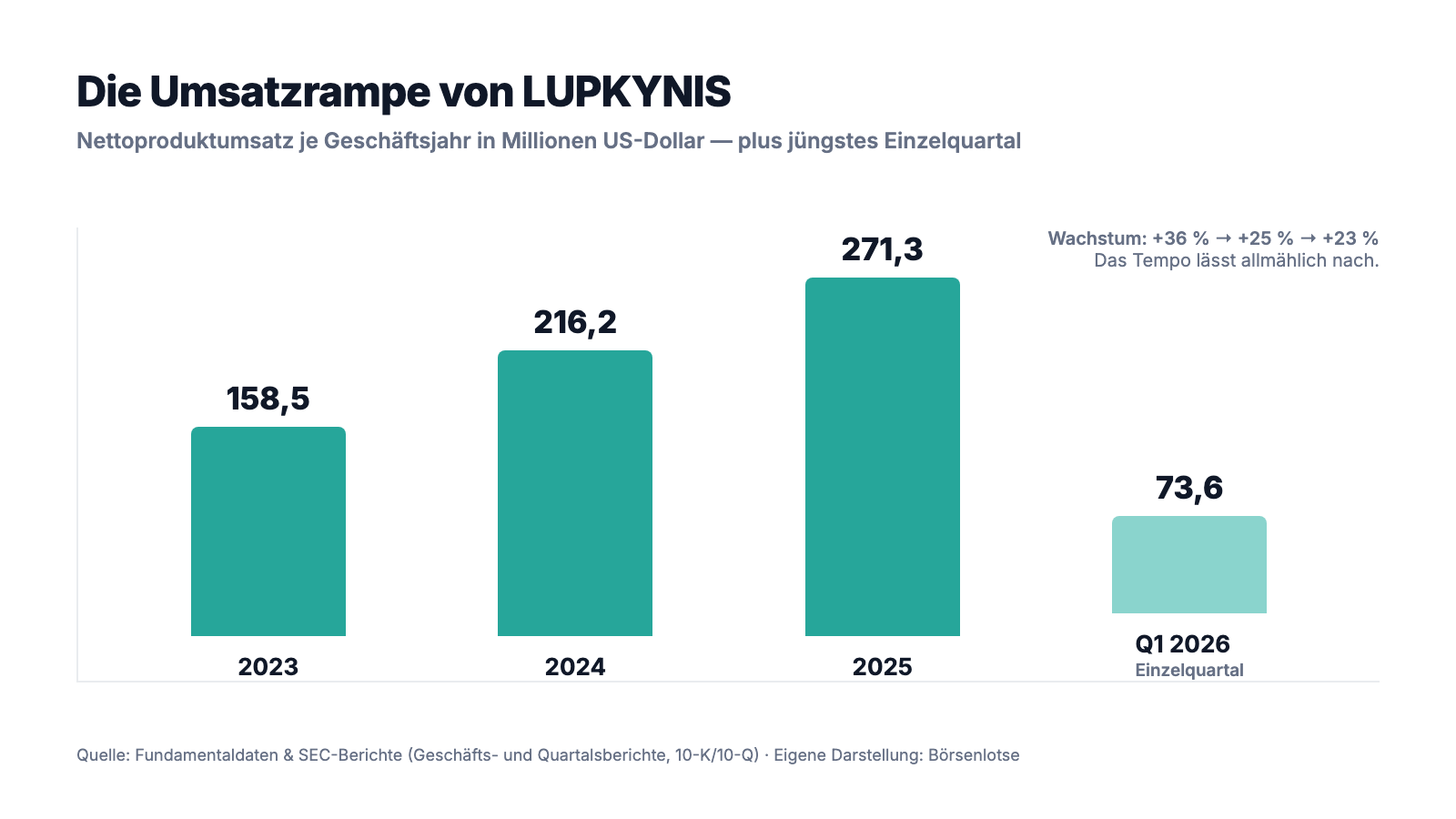

First, what genuinely impresses — and here that is a lot. LUPKYNIS net product revenue reads like a clean market ramp-up: $158.5 million in 2023, $216.2 million in 2024 (plus 36 percent), $271.3 million in 2025 (plus 25 percent). And the momentum holds: in the first quarter of 2026 the company took in $73.6 million, after $60.0 million in the prior-year quarter — a gain of about 23 percent. An honest detail to go with it: the growth rate is falling (36 → 25 → 23 percent), so the ramp-up is maturing. But unlike at a research-stage biotech, this curve no longer ends in nothing but losses: operating income swung from minus $4.7 million (2024) to plus $104.9 million (2025), and operating cash flow rose 206 percent to $135.7 million. That is the good news, and it is real — here the day-to-day business earns money, not just the balance sheet.

But now look at the profit line — and then one line higher. The bottom line for 2025 showed net income of $287.2 million. Pre-tax income, however, stood at only $114.2 million. The difference — $173.0 million — is a tax benefit, not a drug sold. Remember this image: about a third of the record 2025 profit comes not from the business but from the bookkeeping. Unlike at many another biotech, the operating core here remains genuinely profitable — but for the flattering price-to-earnings ratio, the inflated headline is what counts. Why that is so is the second uncomfortable truth.

What the filings say — the uncomfortable truths

Uncomfortable truth no. 1: everything hangs on a single drug

Of the $283.1 million in total revenue for 2025, $271.3 million came from product sales — and that product revenue is 100 percent LUPKYNIS. The company says it in the report itself, entirely soberly:

"LUPKYNIS is our only approved product and our only source of net product sales. Prior to the year ended December 31, 2024, we had negative cash flows from operating activities for multiple years."

— Aurinia Pharmaceuticals, SEC annual report 10-K 2025, Item 7 MD&A "Liquidity and Capital Resources"

Translated into an image: picture a friend who proudly tells you his company is doing splendidly — until you learn that a single product supplies all of the revenue. You would swallow for a moment. As long as LUPKYNIS grows, that is a turbocharger; if it stalls — through a safety incident, a reimbursement decision, a copycat — there is no second leg to cushion the fall. Concentration risk means: one problem, and it hits not a quarter of the business but all of it. To make matters worse, the competition section notes that LUPKYNIS may be the only approved tablet against lupus nephritis, but it is not alone in the market: BENLYSTA (belimumab, from GSK) and GAZYVA (obinutuzumab, from Genentech) are also approved for LN as injections — from two pharma giants with far deeper pockets.

Uncomfortable truth no. 2: the composition-of-matter patent expires in October 2027 — and eight generic drugmakers are already waiting

Here is the date the calendar blind spot likes to suppress. A drug's most important protective wall is the patent on the active ingredient itself (the "composition of matter"). For voclosporin, after the most recent extension, that protection reaches only to October 2027:

"Our application for patent term extension for U.S. Patent No. 7,332,472 related to the composition of matter of voclosporin was approved by the U.S. Patent and Trademark Office (“USPTO”) in December 2025, resulting in a term extending to October 2027."

— Aurinia Pharmaceuticals, SEC annual report 10-K 2025, Item 1 "Patents and Proprietary Rights"

Honesty requires adding: there are further patents — for instance on the dosing protocol, which runs in the United States until December 2037. But the core patent on the active ingredient is the real moat, and it has an expiry date. That the matter is serious is shown by the second passage: in spring 2025, no fewer than eight copycats stepped forward.

"In February and March 2025, we received a paragraph IV notice of certification (a “Notice Letter”) from each of Hikma Pharmaceuticals USA Inc., Lotus Pharmaceutical Co. Ltd., Galenicum Health S.L.U., Zydus Pharmaceuticals (USA) Inc., Teva Pharmaceuticals, Inc., Dr. Reddy’s Laboratories, Inc., DifGen Pharmaceuticals LLC and Sandoz Inc. advising that each company had submitted an Abbreviated New Drug Application (“ANDA”) to the FDA seeking authorization to manufacture, use or sell a generic version of LUPKYNIS in the U.S."

— Aurinia Pharmaceuticals, SEC annual report 10-K 2025, Item 1 "Patents and Proprietary Rights" (Hatch-Waxman / ANDA)

Weigh this honestly. In favor: Aurinia is fighting back, has filed patent-infringement suits within the deadline, and the automatic stay under U.S. drug law (Hatch-Waxman) buys time — generics may enter the market at the earliest 7.5 years after the LUPKYNIS approval, unless a court topples the patents sooner. Against: the sheer number of attackers. When eight manufacturers line up at once, the product is lucrative enough to be worth copying — and the outcome of patent litigation is never certain. A one-product business with a dated expiry of its core protection is no sure thing, no matter how pretty the current revenue curve looks.

Uncomfortable truth no. 3: a third of the record profit is a one-time tax benefit

Here is the resolution of the low price-to-earnings ratio. Why did 2025 net income ($287.2 million) sit so far above pre-tax income ($114.2 million)? Because a tax position flipped — in the company's favor, but only once:

"Income tax (benefit) expense was $(173.0) million, compared to $1.7 million in 2024. The change is primarily due to the release of the Company’s valuation allowance on deferred tax assets that the Company now expects to realize."

— Aurinia Pharmaceuticals, SEC annual report 10-K 2025, Item 7 MD&A "Income Tax (Benefit) Expense"

What is behind it? A company that makes losses for years accumulates deferred tax assets — credits, in effect, against future taxes. As long as profits are uncertain, it must write these credits down on its balance sheet (the "valuation allowance"). Once the company tips sustainably into profit, it may release that write-down — and the whole pent-up advantage lands in the profit in one stroke as income. That is entirely legal and even a good sign (the company trusts itself to earn future profits). But it brought in no cash, and it flows exactly once. For the valuation, that is decisive: whoever considers Aurinia "dirt cheap" at a price-to-earnings ratio of about 8 is calculating with the inflated profit. Strip out the tax benefit and calculate on pre-tax income ($114.2 million), and the stock is considerably more expensive than the "8" suggests — and in the first quarter of 2026, Aurinia was already paying normal taxes again ($9.6 million on $43.9 million of pre-tax income). Remember: a low price-to-earnings ratio is sometimes not a discount but an optical illusion — always ask what the earnings are made of.

Valuation: about $2.2 billion in market value — for a one-product business with a patent clock

In early July 2026 the Aurinia stock cost about $17.60; at about 133 million shares, that makes a market value of about $2.2 billion (data as of July 8, 2026). The price-to-earnings ratio sits at about 8 — but beware: it calculates with the tax-inflated 2025 profit. Strip out the one-time tax benefit and calculate on normalized earnings, and it lands rather in the mid-to-upper teens. The price-to-sales ratio of about 7 and the price-to-book ratio of about 4 are not extreme for a profitable biopharma, but they show what is really being priced here: not today's record profit, but the question of what remains of the business after October 2027 — whether LUPKYNIS fends off the generic attacks and whether the pipeline (aritinercept) delivers a second leg in time. The analyst consensus (about 6 firms) leans toward buy on average, but that is the "professionals' view" of a future scenario, not a certainty. Precisely the fact that the stock trades no higher despite a record profit and a price-to-earnings ratio of 8 is the best evidence that the market hears the patent clock very well — only the calendar blind spot likes to tune it out.

Opportunities and risks at a glance

What speaks for Aurinia:

- Genuine, operating profitability: net product revenue up from $158.5 million (2023) to $271.3 million (2025), operating income swung from minus $4.7 million to plus $104.9 million, operating cash flow up 206 percent — the rare case of a truly profitable biotech (annual report 10-K 2025, quarterly report 10-Q Q1 2026).

- Clean balance-sheet signals: about $398 million in cash and investments (December 31, 2025), very low debt, Altman Z 9.18, fundamental rating A — no distress; hits exclusively in value and quality scanners.

- A genuine product advantage: LUPKYNIS is the first and only FDA-approved oral therapy (a tablet) for active lupus nephritis — more convenient than the approved injections of the competition.

- Shareholder-friendly capital policy: buyback program topped up in July 2025 to a total of $300 million; international partner Otsuka carries the business in Europe and Japan.

- Optically cheap valuation: price-to-earnings ratio about 8, price-to-sales about 7, price-to-book about 4 — not a high price for a profitable pharma (data as of July 8, 2026).

What speaks against it:

- The patent clock: composition-of-matter protection for voclosporin expires in October 2027; eight generic drugmakers (among them Teva, Sandoz, Dr. Reddy's, Hikma) have already filed approval applications (ANDA) — the outcome of the patent litigation is open.

- One-product concentration risk: 100 percent of product revenue hangs on LUPKYNIS — "our only approved product"; no second approved leg, the pipeline (aritinercept) is still in development.

- Earnings quality: the record 2025 net income of $287.2 million contains a $173.0 million one-time, non-cash tax benefit — the price-to-earnings ratio of 8 thereby looks cheaper than reality.

- Competition and a growth dent: BENLYSTA (GSK) and GAZYVA (Genentech) are also approved for lupus nephritis as injections; revenue growth is slowing (36 → 25 → 23 percent).

- Use of the cash pile: instead of into a second product, much of the capital flows into share buybacks — a bet that the till stays full even after the 2027 patent expiry.

A human conclusion

Back to the calendar blind spot from the opening. It has a true core: something really has succeeded at Aurinia that most biotechs never achieve — the leap from perpetual loss to an operationally profitable company with a real, growing product and a well-stuffed till. That is no mirage, that is substance, and a value filter recognizes it rightly. But exactly here lurks the thinking error this case can teach you: a low price-to-earnings ratio answers only half the question. The other half stands as a date in the filing: the core protection of the only product ends in October 2027, eight generic drugmakers are already lining up, and a third of the record profit is a tax accounting entry that flows exactly once. Aurinia is thus neither a bankruptcy candidate nor a sure thing, but a bet with an expiry date: it pays off if LUPKYNIS survives the patent trials, the pipeline arrives in time and the cash pile finances a second leg. It goes wrong if copycats squeeze the price from 2027 on and no new product stands ready. Both are in the same report, only a few pages apart. Whoever buys in here should do so because they have seen the expiry date in the calendar and priced it in — not because an "8" looks so reassuringly cheap. What you make of it is your decision. And that is exactly as it should be.

Sources

All original documents used in this analysis — to read for yourself:

- Aurinia Pharmaceuticals Inc. — SEC annual report 10-K for 2025 (filed February 26, 2026)

- Aurinia Pharmaceuticals Inc. — SEC annual report 10-K for 2024 (filed February 27, 2025)

- Aurinia Pharmaceuticals Inc. — SEC quarterly report 10-Q as of March 31, 2026 (filed May 7, 2026)

- Aurinia Pharmaceuticals Inc. — SEC quarterly report 10-Q as of September 30, 2025 (filed November 4, 2025)

- Aurinia Pharmaceuticals Inc. — SEC quarterly report 10-Q as of June 30, 2025 (filed July 31, 2025)

- Aurinia Pharmaceuticals Inc. — SEC quarterly report 10-Q as of March 31, 2025 (filed May 12, 2025)

- Aurinia's complete SEC filing history: EDGAR overview (sec.gov)

- Fundamental data (metrics, quarterly series, valuation; data as of July 8, 2026), reconciled with the SEC filings.

- Screener and rating data: in-house stock scanner (data as of July 8, 2026).

Transparency & disclaimer: This analysis is a journalistic contextualization of publicly available information and is not investment advice, not a financial analysis in the regulatory sense, and not a solicitation to buy or sell securities. It expressly contains no judgment on whether a drug will be commercially successful, whether patents will hold up in court, or whether profitability will last. Stock investments carry substantial risks up to total loss — with biopharma stocks in particular. All information without guarantee; the data cut-off is noted in the text in each case. The author holds no position in Aurinia stock at the time of publication.

Our Bottom Line at a Glance

- Product & growth positive

- LUPKYNIS is growing solidly: net product revenue up from $158.5 million (2023) to $271.3 million (2025), Q1 2026 at $73.6 million (up about 23 percent). As the only approved oral therapy for lupus nephritis it has a genuine usage advantage; the pace of growth is easing, however (36 → 25 → 23 percent).

- Profitability & earnings quality neutral

- Unlike many biotechs, Aurinia is genuinely profitable operationally (operating income of $104.9 million in 2025, operating cash flow up 206 percent). But the record net income of $287.2 million contains a $173.0 million one-time, non-cash tax benefit; pre-tax income stood at $114.2 million. The price-to-earnings ratio of 8 thereby looks cheaper than justified.

- Balance sheet & financing positive

- About $398 million in cash and investments (December 31, 2025), very low debt, Altman Z 9.18, fundamental rating A — no distress. Buyback program topped up in July 2025 to a total of $300 million; capital flows back to shareholders instead of into a second product.

- Concentration risk & patent clock negative

- 100 percent of product revenue hangs on a single drug — "our only approved product". The composition-of-matter protection for voclosporin expires in October 2027; eight generic drugmakers (among them Teva, Sandoz, Dr. Reddy's, Hikma) have filed approval applications, and Aurinia is suing them. Outcome open.

- Valuation & competition neutral

- Market value about $2.2 billion, P/E about 8, P/S about 7, P/B about 4 — optically cheap, but the market is visibly pricing in the 2027 patent risk. In the LN market, BENLYSTA (GSK) and GAZYVA (Genentech) compete as injections (data as of July 8, 2026).

Aurinia is the rare, operationally genuinely profitable biotech in a value scanner: LUPKYNIS, the first approved tablet against the kidney inflammation caused by lupus, has driven revenue to $271.3 million and swung operating income into the black. But a third of the record 2025 profit is a one-time tax benefit, 100 percent of the business hangs on this one product, and the composition-of-matter protection ends in October 2027 — eight generic drugmakers are already waiting. A full till and low debt stand against a dated expiry of the core protection. Not investment advice.

What Our Rating Means

- If you don't own the stock

- As long as the question raised in the bottom line stays open, we see no basis for an entry.

- If you hold it in your portfolio

- Our findings offer no acute reason to sell — the checkpoints named remain decisive.

A journalistic assessment by our editorial team at the time of the deep dive, based on public sources — not investment advice and not a solicitation to buy or sell. Your personal circumstances (investment goals, risk capacity, taxes) cannot be taken into account. What our categories mean, how verdicts are formed, and what conflicts of interest exist →

Worth Noting

- Membership in the value scanner "Joel Greenblatt: Magic Formula" (not a warning scanner) was confirmed locally and live on July 14, 2026; AUPH shows up in 7 value and quality scanners (Buffett criteria, EBIT-margin ranking, Magic Formula, P/E ranking, Peter Lynch PEG, quality stocks, owner-earnings yield), in no warning scanner.

- All earnings and balance-sheet figures come from the audited annual report 10-K for 2025 (filed 26.02.2026) and the quarterly report 10-Q as of 31.03.2026; the 2025 net income contains a one-time tax benefit of $173.0 million from the release of the valuation allowance on deferred taxes.

- Price and valuation figures are dated July 8, 2026 (about $17.60, about 133 million shares); analyses are evergreen, daily prices are not a buy argument. The composition-of-matter patent on voclosporin expires in October 2027.

Frequently Asked Questions

Aurinia (Nasdaq: AUPH) is a commercial-stage biopharma, legally seated in Alberta (Canada) and operating out of Rockville in the U.S. state of Maryland. Its only marketed drug is LUPKYNIS (voclosporin), the first FDA-approved oral therapy for active lupus nephritis (LN), a kidney inflammation caused by lupus. In development is the drug candidate aritinercept.

Yes, and unlike at many biotechs, the day-to-day business earns real money: operating income swung from minus $4.7 million (2024) to plus $104.9 million (2025), and net income came to $287.2 million. Important: $173.0 million of that is a one-time, non-cash tax benefit; pre-tax income was $114.2 million. In the first quarter of 2026, net income stood at $34.4 million.

The price-to-earnings ratio of about 8 (data as of July 8, 2026) calculates with the record 2025 profit, which is inflated by a one-time tax benefit of $173.0 million. On normalized earnings it sits higher. In addition, the market is pricing in the 2027 expiry of the composition-of-matter patent — the optically cheap ratio is therefore partly an illusion, partly a warning.

The core patent on the active ingredient voclosporin (U.S. Patent 7,332,472) was extended in December 2025 through October 2027. A further patent on the dosing protocol runs in the United States until 2037. As early as 2025, eight generic drugmakers filed approval applications (ANDA); Aurinia is suing them for patent infringement, which triggers an automatic FDA stay under the Hatch-Waxman Act.

LUPKYNIS may be the only approved oral therapy (a tablet) for active lupus nephritis, but it does not stand alone in the market: BENLYSTA (belimumab, from GSK) and GAZYVA (obinutuzumab, from Genentech) are also approved for LN as injectable treatments. In addition, doctors treat lupus nephritis off-label with older drug combinations.

No. In all six SEC filings evaluated (two annual reports 10-K, four quarterly reports 10-Q), artificial intelligence does not appear as a product, a source of revenue or a material business risk. In our company-specific AI classification, Aurinia is therefore rated "Neutral".

The facts speak clearly against it: about $398 million in cash and investments (December 31, 2025), a healthy Altman Z-Score of 9.18, very low debt and an operationally profitable, growing business. The main risk is not solvency but the 2027 expiry of the composition-of-matter patent in a one-product business.

Found an error?

Did you spot a factual error, an outdated number, or a typo in this deep dive? Let us know briefly — your report goes straight to the editorial team.