TG Therapeutics Stock: Finally Profitable — but Three Quarters of the Record Profit Is a Tax Bonus

TG Therapeutics sells a single drug — BRIUMVI, an infusion against relapsing multiple sclerosis — and is thereby the rare profitable biotech in our value scanner after Joel Greenblatt's Magic Formula. Net product revenue rose from $92 million (2023) to $606.9 million (2025), and the bottom line showed a record profit of $447.2 million. We read the annual report (10-K) for 2025 and the quarterly report (10-Q) as of March 31, 2026: three quarters of that profit is a one-time tax bonus, nearly all the revenue hangs on this one drug, and the rivals are named Roche and Novartis. A sober reckoning behind a genuine success story — and no, this is not investment advice.

There is a reflex that lulls us investors especially gently to sleep: let's call it the redemption reflex. For years a company wrote red numbers, for years you (or a friend) hoped for the breakthrough — and suddenly there it finally is, a fat profit. The body breathes out, the brain ticks off "done" and switches off the critical questions. This is exactly the reflex TG Therapeutics (Nasdaq: TGTX) is serving perfectly right now: a biopharma out of New York that, after more than a decade of losses, is now profitable, whose revenue has multiplied — and which, as a rare exception, shows up in a value scanner, the place where otherwise solid, "cheap" companies stand, not the usual wobbly biotech candidates. Everything shouts: "Here, at last, all is well." So let's make a deal: before you let yourself be redeemed by the word "profit" and the green price, we read together what TG Therapeutics itself reported to the U.S. securities regulator, the SEC — in the annual report (10-K) for 2025 and the quarterly report (10-Q) as of March 31, 2026. An SEC filing is honest under penalty of law. And this one shows what this pretty profit really consists of. In the end, you decide for yourself.

What TG Therapeutics actually does

Picture the immune system as a guard troop that defends the body — but in multiple sclerosis (MS) a part of this troop attacks the body's own nervous system and destroys the protective sheath of the nerve pathways. A particularly effective strategy against this: take out the attackers in a targeted way. For that, TG Therapeutics builds an anti-CD20 antibody — a molecule that docks onto a specific marker (CD20) on the misguided B cells and pulls them out of circulation. The product is called BRIUMVI (active ingredient ublituximab-xiiy), is administered as an infusion and is approved against relapsing multiple sclerosis (RMS). In the United States it came to market in January 2023; outside the U.S. the partner Neuraxpharm has marketed it since 2024.

And here is the peculiarity that carries this analysis: unlike most biotechs we write about, TG Therapeutics is no longer a perpetually loss-making research shop but earns real money — the company began its current business activities in 2012 and, with BRIUMVI, wrote its first full year of profit in 2024. The pipeline behind it is modest: a subcutaneous (under the skin) injectable ublituximab in development and azer-cel, a licensed-in cell therapy. Sounds like the successful leap from lab to pharmaceutical company? In part, it is. But note the central tension of this analysis right now: a profitable biotech that a value filter rightly recognizes as a profit machine — whose 2025 profit, however, comes three quarters from a one-time tax entry, whose revenue hangs almost 100 percent on a single drug, and which competes against two of the largest pharmaceutical corporations in the world. It runs through every chapter. How such a "first profit" can also deceive is shown, for comparison, by our analysis of Affirm — there it was a flattered one-off number, here it is a tax effect.

Where the stock shows up in our scanner

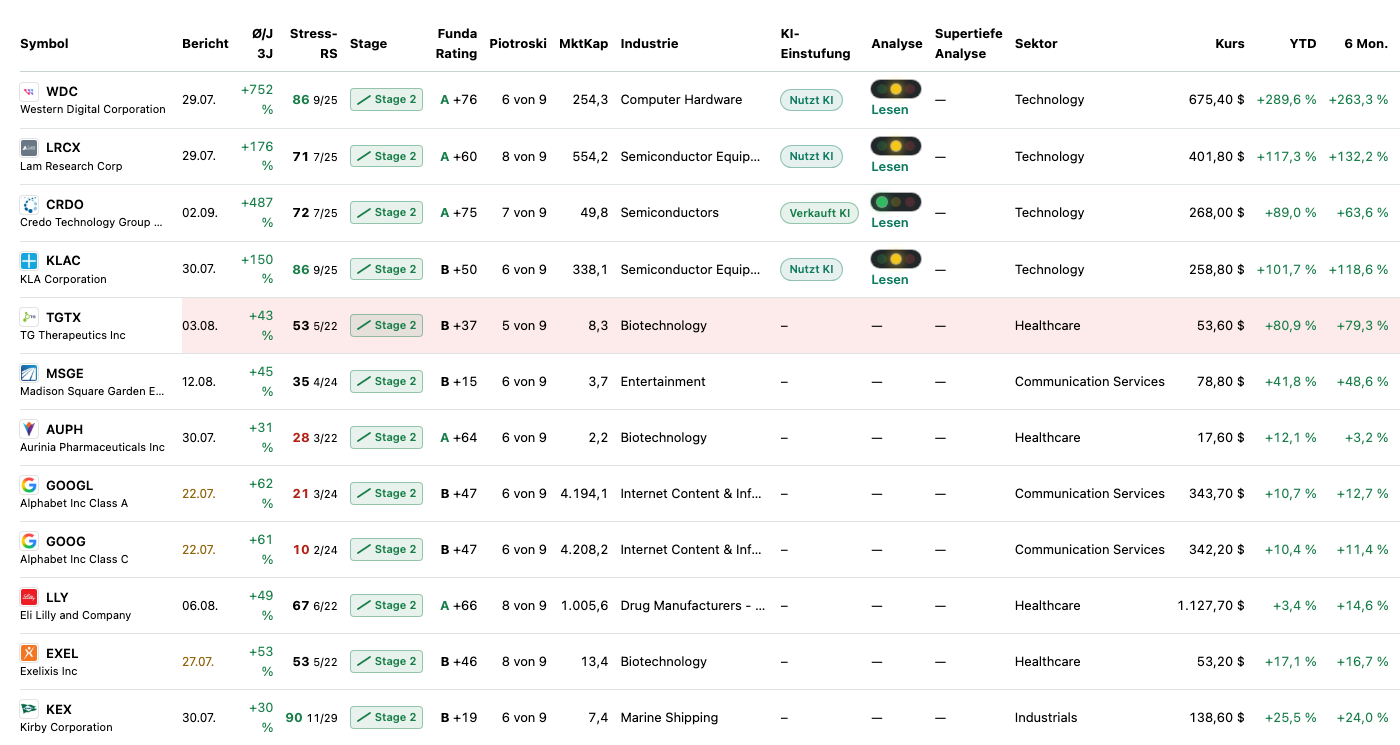

Every day we run about 3,500 stocks through our scanners. TG Therapeutics lights up in 27 filters (data as of July 8, 2026) — and this time not a single warning scanner is among them. The most interesting hit is the Magic Formula of value investor Joel Greenblatt. His idea, in everyday language: buy good companies at a fair price — measured by two figures. First, the return on capital (how much operating profit comes out per dollar of working capital employed?); second, the earnings yield (how much operating profit do I get per dollar of enterprise value?). Added to that are hits in quality and momentum scanners: Weinstein Stage 2 (intact uptrend), institutional accumulation, "quality growth", William O'Neil (CAN SLIM), the Levermann ranking. The hard balance-sheet metrics confirm the clean picture: Altman-Z score 6.15 (a classic bankruptcy early-warning — danger begins only below 1.8, so green here), Piotroski F-Score 5 of 9 (a nine-point balance-sheet test — 5 is okay, not outstanding), fundamental rating B. Positive equity of $583.1 million (March 31, 2026) rounds off the picture. No distress, no going-concern doubt — unlike many biotechs we otherwise dissect here.

Before you read that as a free pass, you need to know the best-known weakness of the Magic Formula — Greenblatt himself has never hidden it: the formula calculates with the most recently reported earnings. If that profit is inflated by a special effect, the stock looks "cheaper" than the actual business justifies. And that is exactly the case at TG Therapeutics — more on that in a moment. The scanner recognizes a real, profitable, growing company; but it says nothing about what this profit consists of and how vulnerable a business with only one product is. The filter is a good metal detector. Whether the signal is gold or a tin can is only revealed by the dig. Let's start digging.

The numbers over the years — honestly appraised

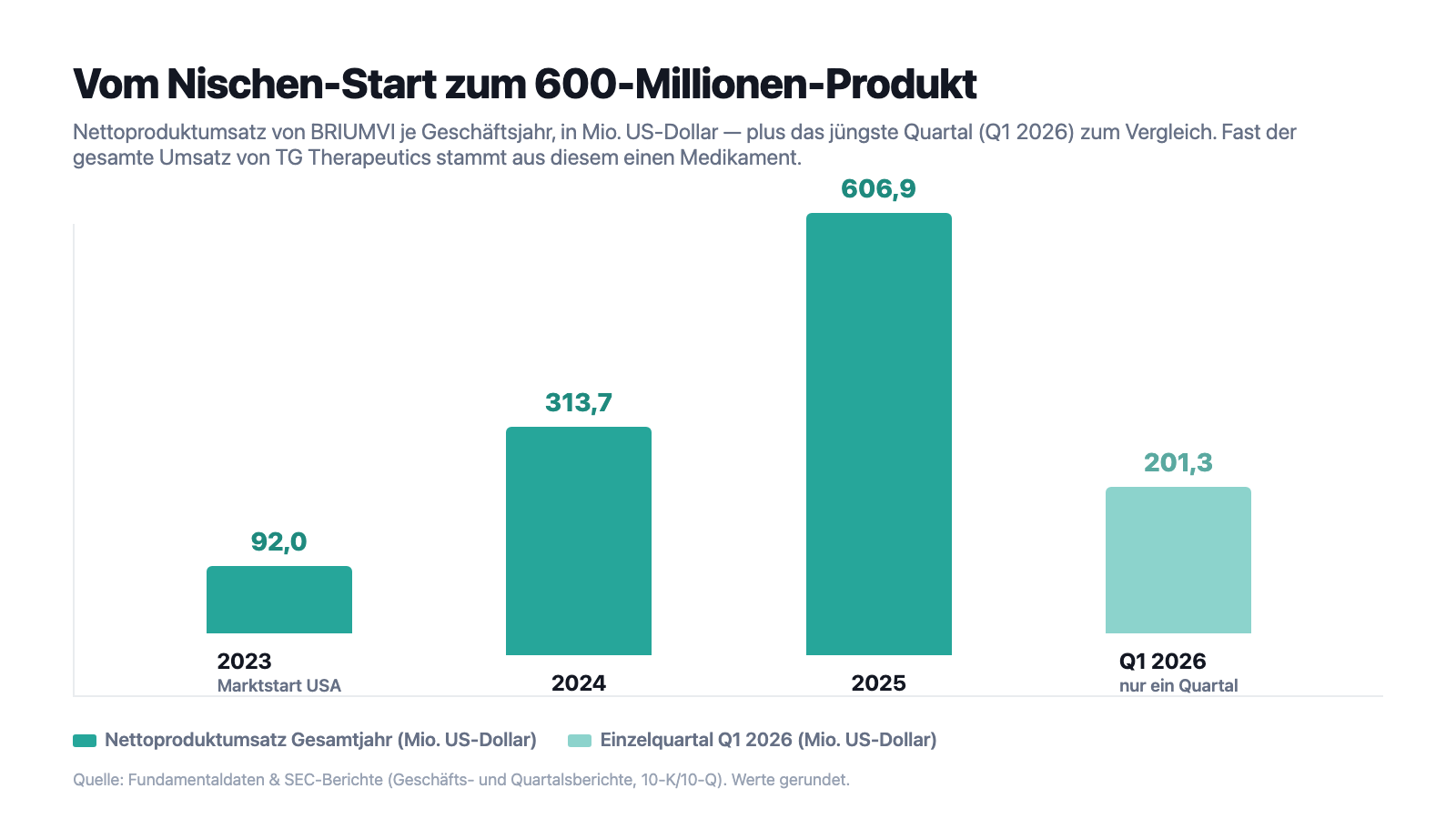

First, what genuinely impresses, and that is a lot here. BRIUMVI's net product revenue reads like a picture-book market entry: $92.0 million in the launch year 2023, $313.7 million in 2024, $606.9 million in 2025 — a doubling year after year. And the momentum holds: in the first quarter of 2026 alone the company booked $201.3 million, after $119.7 million in the prior-year quarter — a gain of about 68 percent. For a drug that has only been on the market since early 2023, that is a remarkable curve. And unlike a research-stage biotech, this curve no longer ends only in a loss: in 2024 TG Therapeutics earned money over a full year for the first time ($23.4 million), in the first quarter of 2026 it was $19.8 million in net profit ($0.14 per share). That is the good news, and it is real.

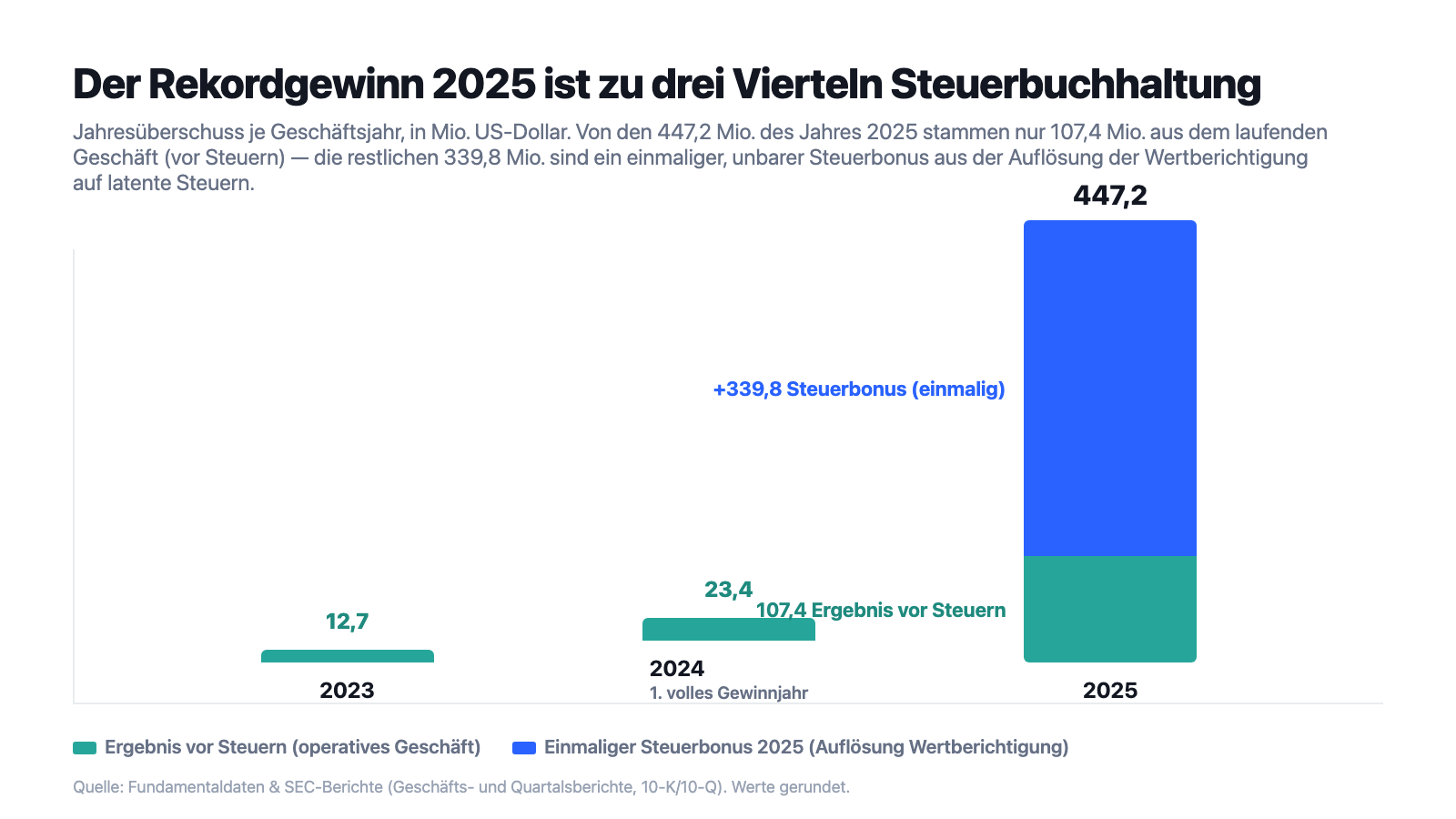

But now look at the profit line — and then one line higher. The bottom line for 2025 showed net income of $447.2 million. Pretax income, however, was only $107.4 million. The difference — $339.8 million — is a tax bonus, not a sold drug. Remember this image: three of every four profit dollars of the record year 2025 come not from the business but from accounting. Why that is so and what it means for the valuation is the core of the uncomfortable truths.

What the filings say — the uncomfortable truths

Uncomfortable truth no. 1: everything hangs on a single drug

Of the $616.3 million in total revenue in 2025, $606.9 million comes from product sales — and this product revenue is 100 percent BRIUMVI. So about 98 percent of the business hangs on a single agent. The company says it in the report itself, quite soberly:

"BRIUMVI is currently our only marketed product. […] Because of the numerous risks and uncertainties associated with developing and commercializing pharmaceutical products, we are unable to predict the extent of any future losses, or for how long we may continue to experience profitability. We may not be able to sustain or increase our profitability on a quarterly or annual basis."

— TG Therapeutics, SEC annual report 10-K 2025, Item 1A "Risk Factors" (Financial Position)

Translated into an image: picture a friend who proudly tells you his business is running splendidly — until you learn that a single customer accounts for almost all the revenue. You would swallow hard for a moment. It is exactly like that here, except the one "customer" is a single product. As long as BRIUMVI grows, it is a turbo; if it stalls — through a safety incident, a pricing or reimbursement decision, a superior competitor — there is no second leg to cushion the fall. Concentration risk means: one problem, and it hits not a quarter of the business but nearly all of it.

Uncomfortable truth no. 2: three quarters of the record profit is a one-time tax bonus

Here is the resolution of the scanner signal. Why did 2025 net income ($447.2 million) sit so far above pretax income ($107.4 million)? Because a tax item tipped — in the company's favor, but only a single time. The report explains it like this:

"Income tax benefit totaled $339.8 million for the year ended December 31, 2025, as compared to income tax expense of $2.2 million during the comparable period ended December 31, 2024. The increase in income tax benefit is primarily driven by the release of our deferred tax asset valuation allowance during the year ended December 31, 2025."

— TG Therapeutics, SEC annual report 10-K 2025, Item 7 MD&A "Income Tax Benefit (Expense)"

What is behind it? A company that makes losses for years accumulates deferred tax assets — credits on future taxes, so to speak. As long as profits are uncertain, it must write these credits down on the balance sheet ("valuation allowance"). Once the company tips sustainably into the profit zone, it may release the write-down — and the whole pent-up benefit lands all at once as income in the profit. That is entirely legal and even a good sign (the company trusts itself to make future profits). But it brought in no cash, and it flows exactly once. For the valuation that is decisive: whoever considers TG Therapeutics "cheap" at a price-to-earnings ratio of about 20 is calculating with the inflated profit. Subtract the tax bonus and calculate on the operating result, and the stock is far more expensive than the value metric suggests. Remember: a profit is not simply a profit — always ask whether it comes from the business or from accounting.

Uncomfortable truth no. 3: the rivals are named Roche and Novartis

The pretty revenue has to be fought for in a market where two of the largest pharmaceutical corporations in the world already sit. The report names them unmistakably:

"Currently, BRIUMVI directly competes with ocrelizumab, the only other approved intravenously administered anti-CD20 monoclonal antibody (Roche Holdings AG). BRIUMVI also competes with a subcutaneous version of ocrelizumab administered by healthcare providers. In addition, BRIUMVI competes with ofatumumab (Novartis AG), a patient/self-administered subcutaneous anti-CD20 monoclonal antibody approved for MS."

— TG Therapeutics, SEC annual report 10-K 2025, Item 1 "Business — Competition"

Appraise that honestly. In favor: BRIUMVI has a real advantage — it is given as a comparatively short infusion and has carved out a growing niche with rapidly rising sales figures. Against it stands the sheer size of the opponents: ocrelizumab (Roche, a billion-dollar blockbuster under the brand name Ocrevus) was in the market before BRIUMVI and is the top dog of infusion therapies; ofatumumab (Novartis, Kesimpta) offers convenient self-injection at home. Both corporations have incomparably more money for sales, studies and rebate negotiations — the report itself stresses that many competitors have "significantly greater financial, product development, manufacturing and commercialization resources". And on the horizon, per the report, stands a possible new drug class (BTK inhibitors) that could shift the treatment landscape. Growth that has to be wrestled from an established brand rival is never as safe as a steep revenue curve makes it look.

Uncomfortable truth no. 4: profitable yes — but the road there was expensive, and the road back is not ruled out

For all the justified joy about the profit zone: the report itself dampens the euphoria with a sentence you should have read before you tick off "finally made it":

"We have incurred substantial operating losses since our inception, and we may incur losses in the future."

— TG Therapeutics, SEC annual report 10-K 2025, Item 1A "Risk Factors" (Financial Position and Need for Additional Capital)

This fits the capital side, which is easily overlooked in the success story. Over the years the losses added up to an accumulated deficit of about $1.1 billion (March 31, 2026) — so today's positive equity stands on a lot of raised capital. And the company keeps refueling: on March 18, 2026 TG Therapeutics paid off its existing loan and closed a new $750 million loan with the financial investor Blue Owl — three times as much as the previous $250 million, secured by "substantially all of the assets" of the company. As of March 31, 2026 this did put a comfortable $572.8 million in cash and investments on the books (at the end of 2025 it was only $199.5 million), but at a price: interest cost and security interests over the entire company. A company that still carries about half a billion in operating costs annually remains, despite the profit zone, reliant on good growth to carry this load easily. "Profitable" and "invulnerable" are two different things.

Valuation: about $8.3 billion market value — for a one-product business

In early July 2026 the TG Therapeutics stock cost about $53.60; at about 155 million shares that makes a market value of about $8.3 billion (data as of July 8, 2026). The price-to-earnings ratio sits around 20 — but beware: it calculates with the tax-inflated 2025 profit. Subtract the one-time tax bonus and calculate on the pretax income of $107.4 million, and the stock is a multiple more expensive than the "20" suggests. The price-to-sales ratio of about 12 and the price-to-book ratio of about 15 are ambitious for a biopharma and show what is really being paid for here: not today's ongoing business, but the expectation that BRIUMVI keeps growing strongly, that the subcutaneous version and azer-cel move up — and that all of it succeeds against Roche and Novartis. The analyst consensus (about 9 firms) is on average buy-leaning, but that is the "professionals' view" of a future scenario, not a certainty. The price has multiplied over the past years (about 79 percent gain over six months alone, data as of July 8, 2026) — for a stock that has run this far, plenty of success is already priced in. The height of the fall arises where the expectation already stands high.

Opportunities and risks at a glance

What speaks for TG Therapeutics:

- Real, growing profitability: net product revenue from $92.0 million (2023) to $606.9 million (2025), first full year of profit in 2024, still rising (Q1 2026: $201.3 million revenue, $19.8 million net profit) — the rare case of a profitable biotech (annual report 10-K 2025, quarterly report 10-Q Q1 2026).

- Clean balance-sheet signals: positive equity ($583.1 million, 31.03.2026), Altman-Z 6.15, fundamental rating B — no distress, no going-concern doubt; hits exclusively in value, quality and momentum scanners.

- Clear product advantage: BRIUMVI is given as a comparatively short infusion and has quickly carved out a growing niche in the MS market.

- Full coffers after refinancing: about $572.8 million in cash and investments (31.03.2026); the company sees liquidity secured for "more than twelve months".

- Tailwind from market and professionals: Weinstein Stage 2, institutional accumulation, about 79 percent price gain over six months and an on-average buy-leaning analyst consensus.

What speaks against it:

- Earnings quality: the record 2025 net income of $447.2 million consists of only $107.4 million from the business; $339.8 million is a one-time, non-cash tax bonus — the value metrics therefore look cheaper than reality.

- One-product concentration risk: about 98 percent of revenue hangs on BRIUMVI; the company itself calls it "our only marketed product" and cannot guarantee it will stay profitable.

- Overpowering competition: ocrelizumab (Roche, Ocrevus) and ofatumumab (Novartis, Kesimpta) — both from significantly larger corporations, with more sales and study budget; on the horizon possible new BTK inhibitors.

- Capital engineering: accumulated deficit of about $1.1 billion; in March 2026 the loan was increased from $250 million to $750 million (secured by all assets) with a simultaneous share buyback.

- High expectation is priced in: market value about $8.3 billion, price-to-sales ratio about 12, price-to-book about 15, price after a strong rally — plenty of success already sits in the price (data as of July 8, 2026).

A human conclusion

Back to the redemption reflex from the beginning. It has a true core: at TG Therapeutics something has genuinely succeeded that most biotechs never manage — the leap from perpetual loss to a profitable company with a real, growing product. That is no mirage, that is substance, and a value filter rightly recognizes it. But this is exactly where the thinking error lurks that this case can show you: "profitable" is a beginning, not an all-clear. The 2025 record profit is three quarters a tax accounting entry that flows exactly once; the whole business rests on a single drug; and the real fight for every future MS revenue dollar against Roche and Novartis is only just beginning. TG Therapeutics is thereby neither a bankruptcy candidate nor a sure thing, but a bet with clear conditions: it pays off if BRIUMVI keeps growing fast, the pipeline moves up and the operating earning power catches up over time with the one-time tax headline. It goes wrong if growth stalls against the giants — because then a high expectation meets a company that still lives off one product and has just loaded its balance sheet with fresh debt. Both stand in the same report, only a few pages apart. Whoever gets in here should do so because they have understood the bet — not because the word "profit" sounds so reassuring. What you make of it is your decision. And that is exactly as it should be.

Sources

All original documents used in this analysis — to read for yourself:

- TG Therapeutics, Inc. — SEC annual report 10-K for 2025 (filed February 27, 2026)

- TG Therapeutics, Inc. — SEC annual report 10-K for 2024 (filed March 3, 2025)

- TG Therapeutics, Inc. — SEC quarterly report 10-Q as of March 31, 2026 (filed May 6, 2026)

- TG Therapeutics, Inc. — SEC quarterly report 10-Q as of September 30, 2025 (filed November 5, 2025)

- TG Therapeutics, Inc. — SEC quarterly report 10-Q as of June 30, 2025 (filed August 8, 2025)

- TG Therapeutics, Inc. — SEC quarterly report 10-Q as of March 31, 2025 (filed May 9, 2025)

- TG Therapeutics' complete SEC filing history: EDGAR overview (sec.gov)

- Fundamental data (metrics, quarterly series, valuation; data as of July 8, 2026), reconciled with the SEC filings.

- Screener and rating data: in-house stock scanner (data as of July 8, 2026).

Transparency & disclaimer: This analysis is a journalistic contextualization of publicly available information and is not investment advice, not a financial analysis in the regulatory sense, and not a solicitation to buy or sell securities. It expressly contains no judgment on whether a drug will be commercially successful or whether the profitability will hold. Stock investments carry substantial risks up to total loss — with biopharma stocks to a particular degree. All information without guarantee; the data cut-off is noted in the text in each case. The author holds no position in TG Therapeutics stock at the time of publication.

Our Bottom Line at a Glance

- Product & growth positive

- BRIUMVI is growing impressively: net product revenue from $92.0 million (2023) to $606.9 million (2025), Q1 2026 alone $201.3 million (plus about 68 percent). The rare case of a profitable biotech with a clear product advantage (short infusion) in a growing MS segment.

- Earnings quality negative

- The record 2025 net income of $447.2 million consists of only $107.4 million from the business; $339.8 million is a one-time, non-cash tax bonus from the release of the valuation allowance on deferred taxes. The price-to-earnings ratio therefore looks cheaper than the operating result justifies.

- Balance sheet & financing neutral

- Positive equity ($583.1 million, 31.03.2026), Altman-Z 6.15, about $572.8 million in cash — no distress. At the same time an accumulated deficit of about $1.1 billion, and in March 2026 the loan was increased from $250 million to $750 million (secured by all assets) with a simultaneous share buyback.

- Concentration risk & competition negative

- About 98 percent of revenue hangs on a single drug — "our only marketed product". In the MS market BRIUMVI competes with ocrelizumab (Roche, Ocrevus) and ofatumumab (Novartis, Kesimpta), both from significantly larger corporations; on the horizon possible new BTK inhibitors.

- Valuation & momentum neutral

- Market value about $8.3 billion, P/S about 12, P/B about 15 — ambitious for a one-product business; Weinstein Stage 2, institutional accumulation, about 79 percent price gain over six months and a buy-leaning analyst consensus. Plenty of success is priced in (data as of July 8, 2026).

TG Therapeutics is the rare profitable biotech in the value scanner: BRIUMVI, an anti-CD20 agent against multiple sclerosis, has driven revenue from $92 million to $606.9 million and pushed the company into the profit zone. But the 2025 record profit is three quarters a one-time tax bonus, about 98 percent of the business hangs on this one product, and the rivals are named Roche and Novartis. Positive equity and full coffers stand against a loan freshly increased to $750 million. Not investment advice.

What Our Rating Means

- If you don't own the stock

- As long as the question raised in the bottom line stays open, we see no basis for an entry.

- If you hold it in your portfolio

- Our findings offer no acute reason to sell — the checkpoints named remain decisive.

A journalistic assessment by our editorial team at the time of the deep dive, based on public sources — not investment advice and not a solicitation to buy or sell. Your personal circumstances (investment goals, risk capacity, taxes) cannot be taken into account. What our categories mean, how verdicts are formed, and what conflicts of interest exist →

Worth Noting

- Membership in the value scanner "Joel Greenblatt: Magic Formula" (not a warning scanner) was confirmed locally and live on July 14, 2026; TGTX shows up in 27 value, quality and momentum scanners, in no warning scanner.

- All earnings and balance-sheet figures come from the verified annual report 10-K for 2025 (filed 27.02.2026) and the quarterly report 10-Q as of 31.03.2026; the 2025 net income contains a one-time income tax benefit of $339.8 million from the release of the valuation allowance on deferred taxes.

- Price and valuation figures dated to July 8, 2026 (about $53.60, about 155 million shares); analyses are evergreen, daily prices are not a buy argument.

Frequently Asked Questions

TG Therapeutics (Nasdaq: TGTX) of New York is a commercial biopharma for B-cell diseases. Its only marketed drug is BRIUMVI (ublituximab-xiiy), an infusion-administered anti-CD20 antibody against relapsing multiple sclerosis (RMS). In development are a subcutaneous version of ublituximab and the licensed-in cell therapy azer-cel.

Yes. 2024 was the first full year of profit, in 2025 net income of $447.2 million stood on the books, and in the first quarter of 2026 it was $19.8 million. Important: of the $447.2 million in 2025, only $107.4 million comes from the ongoing business (pretax) — the remaining $339.8 million is a one-time, non-cash tax bonus.

Because TG Therapeutics released the valuation allowance on its deferred tax assets in 2025. A company that makes losses for a long time accumulates tax credits it may only recognize once profits become probable. This release brought a one-time income tax benefit of $339.8 million in 2025 — accounting income, not a sold drug and not a cash inflow.

Because it is the rare case of a profitable, growing biotech. The scanner "Joel Greenblatt: Magic Formula" looks for companies with a high return on capital and a lot of profit for the money. TG Therapeutics meets that — but on the basis of the most recently reported profit, which in 2025 is inflated by the one-time tax bonus. No warning scanner is among the hits.

Per the annual report, above all against ocrelizumab (Roche, brand name Ocrevus), the only other approved anti-CD20 antibody for infusion, and against ofatumumab (Novartis, Kesimpta) for self-injection. Both come from significantly larger corporations with more sales and study budget. In addition, a new class of BTK inhibitors could change the market.

No. In the analyzed SEC filings, AI is neither a product nor a material source of revenue or efficiency; the company only mentions it "may" incorporate AI into its IT systems in the future and otherwise treats AI as a regulatory risk topic. In our company-specific AI classification, TG Therapeutics is therefore rated as "Neutral".

The facts clearly speak against it: positive equity ($583.1 million as of March 31, 2026), a healthy Altman-Z score of 6.15, about $572.8 million in cash and investments, and a profitable, growing business. At the same time everything hangs on one product, and the company increased its debt to $750 million in March 2026 — solid, but not invulnerable.

Found an error?

Did you spot a factual error, an outdated number, or a typo in this deep dive? Let us know briefly — your report goes straight to the editorial team.