Bit Digital Stock: An Ether Hoard and an AI Cloud — Two Stories, Paid for With Three Times the Shares

Bit Digital has reinvented itself: from bitcoin miner to Ethereum treasury with a publicly listed AI data-center subsidiary. We read the annual report (10-K) and the quarterly reports (10-Q): about 140,000 ether that sat almost a third below cost as of March 31, 2026; an AI anchor customer that brought 70.7 percent of cloud revenue and whose services are now paused; an $865 million contract starting June 2026 — and a share count that has more than tripled since the end of 2023. Not investment advice — just a fitting of both promises.

There's a sales pitch few investors can resist: two stories for the price of one. Bit Digital offers exactly that — up front the shiny Ethereum treasury with staking yield, in back an AI data-center subsidiary with Nvidia chips and a billion-dollar pipeline. Sounds like double insurance: if one story wobbles, the other carries. But that's exactly where the thinking trap sits, and it has a name: whoever has two reasons to like a stock ends up properly checking neither of them. If the ether price sags, you console yourself with the AI cloud; if the AI cloud disappoints, you point at the ether hoard. That way, an investment turns into a merry-go-round of thoughts that never lands on selling. So let's make a deal: we check both stories separately — using what Bit Digital (NASDAQ: BTBT) itself reported to the U.S. securities regulator, the SEC, in the annual report (10-K) for 2025 and in the quarterly reports (10-Q) through March 31, 2026. An SEC filing is honest under penalty of law. In the end, you decide for yourself whether two half stories add up to one whole one.

What Bit Digital actually does — and how much of it is yours

Bit Digital today is something of a twin company. Pillar one: an Ethereum treasury. The company buys the cryptocurrency ether (ETH) and puts it into "staking" — plainly put, interest for locking it up. Whoever locks ETH into the network and helps secure its transactions earns a steady trickle of new ETH for it — like a term deposit, except both the interest and the principal are paid out in the same fluctuating currency. Pillar two: WhiteFiber, an AI computing provider. WhiteFiber buys graphics processors (GPUs) from Nvidia and rents out their computing power by the day to AI companies — a digital machine-leasing operation for training and running artificial intelligence — and is building its own data centers in Canada, Iceland and North Carolina to go with it. The annual report sums up the transformation this way:

"In June 2025, the Company announced that it had initiated a strategic transition to become a pure play ETH staking and treasury company. In connection with the transition, the Company has been converting its bitcoin (BTC) holdings into ETH over time and has undertaken a strategic alternatives process for its bitcoin mining operations, which is expected to result in a sale or wind-down, with any net proceeds to be re-deployed into ETH."

— Bit Digital, SEC annual report 10-K 2025, Item 1 "Business"

There are two things you should know here. First: the company describing itself as a "pure play" Ethereum firm earned the lion's share of its 2025 money from AI computing power, not from ether — the numbers on that in a moment. Second: the AI segment belongs to you as a BTBT shareholder only proportionally. WhiteFiber itself went public on August 8, 2025 (NASDAQ: WYFI); per the annual report (10-K), Bit Digital retained about 70.5 percent. So out of every dollar the AI subsidiary earns, only a bit over 70 cents belong to you. And one more detail for the company portrait: Bit Digital is a holding company founded in 2017 in the Cayman Islands, headquartered in New York — descended from Golden Bull Limited, a Chinese loan broker; from February 2020 to June 2021 the company still mined bitcoin in China. These skin changes are remarkable: P2P loans, bitcoin mining, now Ethereum plus AI. A company that switches its story this often gets watched extra closely on the current one. For a sense of how a different ex-miner wears the AI label, our Riot Platforms analysis is worth a look — BTBT is the case where actual AI revenue really does sit behind the label. Just with side effects.

Where the stock shows up in our scanner

Every day we run about 3,500 stocks through our scanners. BTBT lights up in 4 scanners (data as of July 9, 2026) — and the combination is a contradiction with a headline. On one side, two buy signals from the inside: "CEO buying" and "institutions + CEO buying" — the fundamental-data feed reports insider purchases and more buying than selling institutions (21 net-buying institutions in the month). On the other side, the market technicals: Stan Weinstein: Stage 3 — the phase in which an uptrend tops out and distribution takes hold — and "below 50- & 200-SMA," meaning the price sits below both of its key moving averages. Translated: someone with a name and an address is signaling confidence, but the price chart itself has shifted into reverse. A look at the insider filings (Form 4) from December 2025 through April 2026 tempers the first signal further: they're dominated by option exercises and share grants from compensation programs — we found no large open-market purchases in the filings we checked. A few honesty-check metrics on top (all data as of July 9, 2026): daily swings of about 9.3 percent — a roller coaster, not a savings account; up roughly 40 percent over three months, down roughly 17 percent over twelve months; and the price sits about 93 percent below its all-time high from the 2021 crypto euphoria. Remember the tension running through this analysis: two bets on the future in one stock — and both keep getting paid for with new shares.

The numbers over the years — honestly appraised: the AI cloud carries the group, not the ether

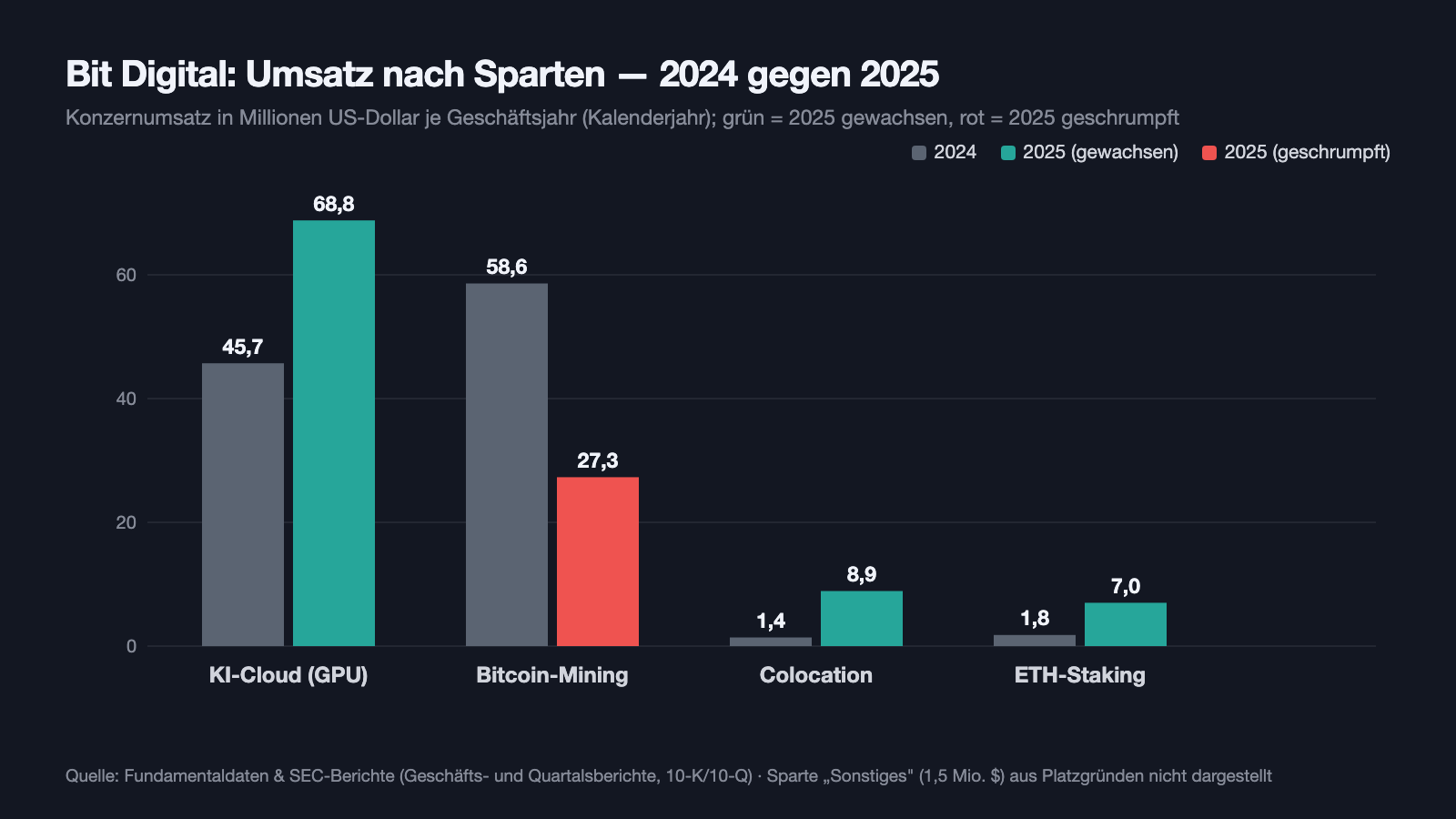

First, what genuinely impresses, honestly appraised: Bit Digital is not an empty story shell. The group posted $113.6 million in revenue in 2025 (up from $108.1 million in 2024) — and the composition shows where the action is: $68.8 million from the AI GPU cloud (+50 percent), $8.9 million from colocation (data-center rental: customers park their own hardware in WhiteFiber's halls and pay for space, power and cooling), $27.3 million from the shrinking bitcoin-mining business (−53 percent), and $7.0 million from ETH staking. Read that last figure twice: the segment the company has recently defined itself by delivered a good 6 percent of 2025 revenue — less than administration costs in a single quarter.

And now the whole truth: the bottom line, the group lost $84.9 million in 2025 (versus a $28.3 million profit in 2024, owed mainly to rising crypto prices). Administrative costs exploded from $41.5 to $81.0 million — nearly a doubling, driven in part by stock-based compensation and the cost of running two public-company existences (BTBT and WYFI) at once. In the first quarter of 2026 it got starker: $27.9 million in revenue faced a $150.3 million loss, of which $146.7 million was attributable to Bit Digital shareholders. The main driver wasn't an operating disaster but the book value of the ether hoard: a $121.1 million price loss on the crypto holdings in 13 weeks. Since the accounting rule ASU 2023-08 took effect, every price move of the holdings flows straight into the income statement — so with its treasury, the company has built itself a built-in earnings amplifier in both directions. Which brings us to the first uncomfortable truth.

What the filings say — the uncomfortable truths

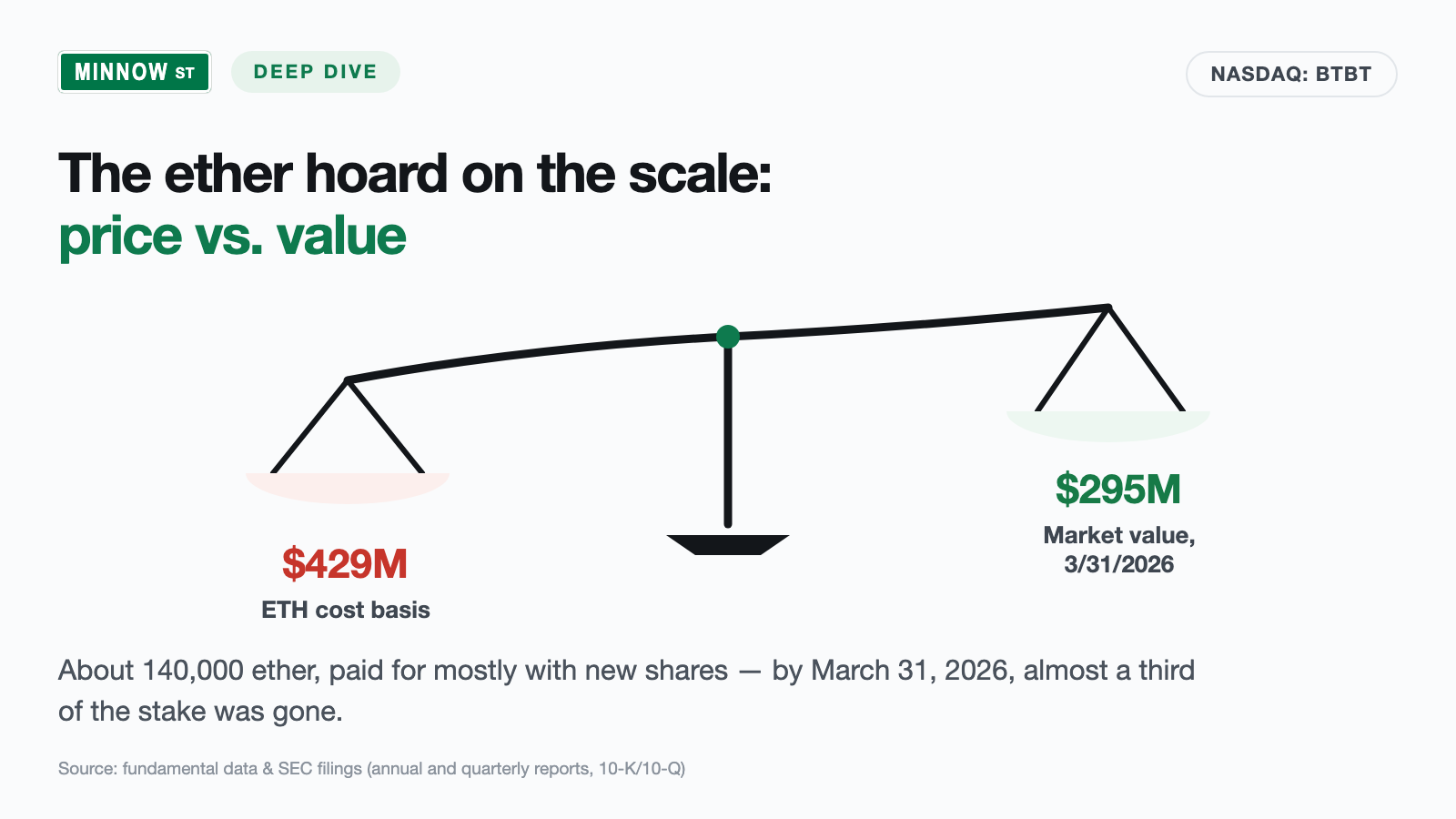

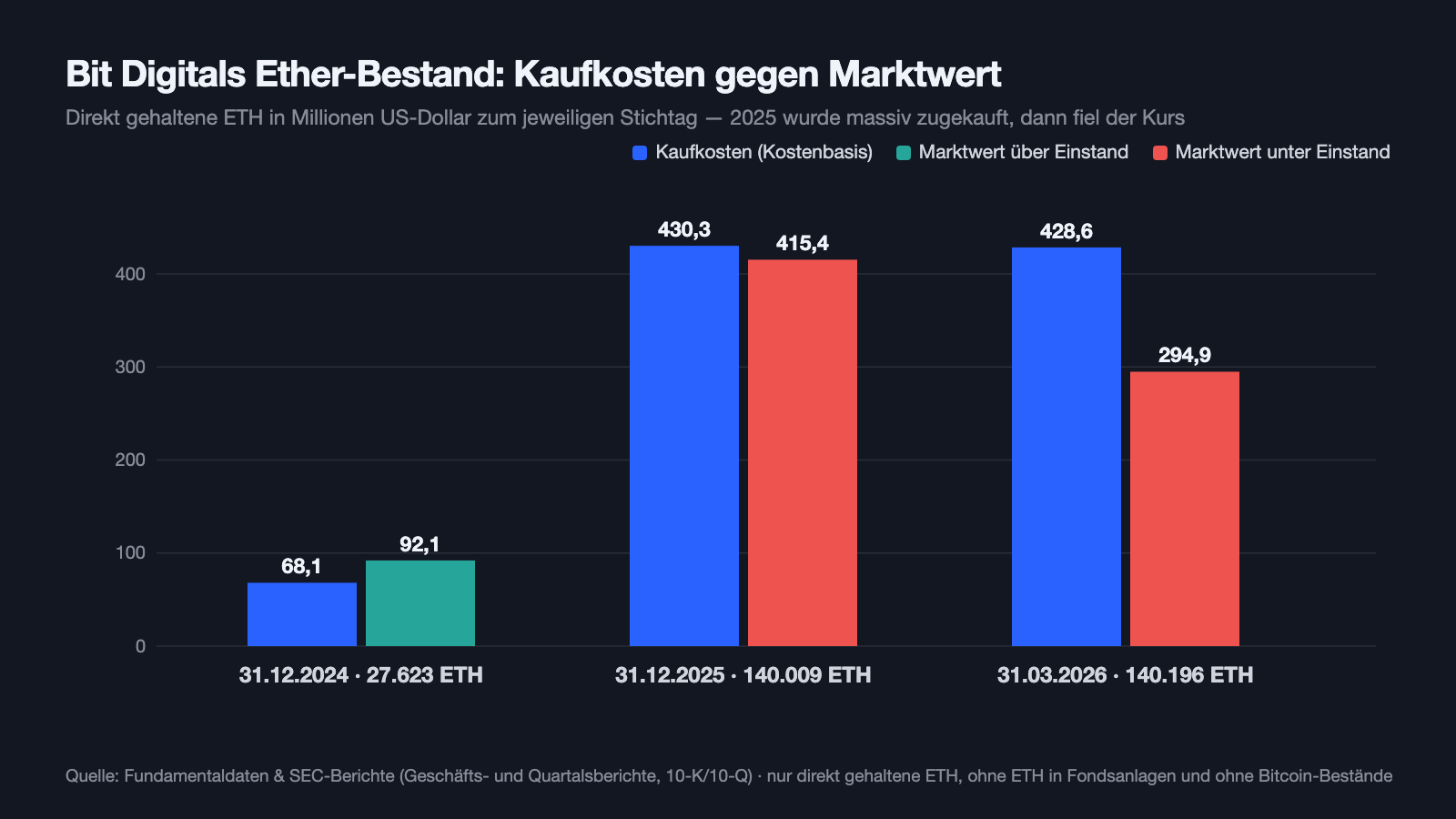

Uncomfortable truth no. 1: the ether hoard cost $429 million — and was worth $295 million on the reporting date

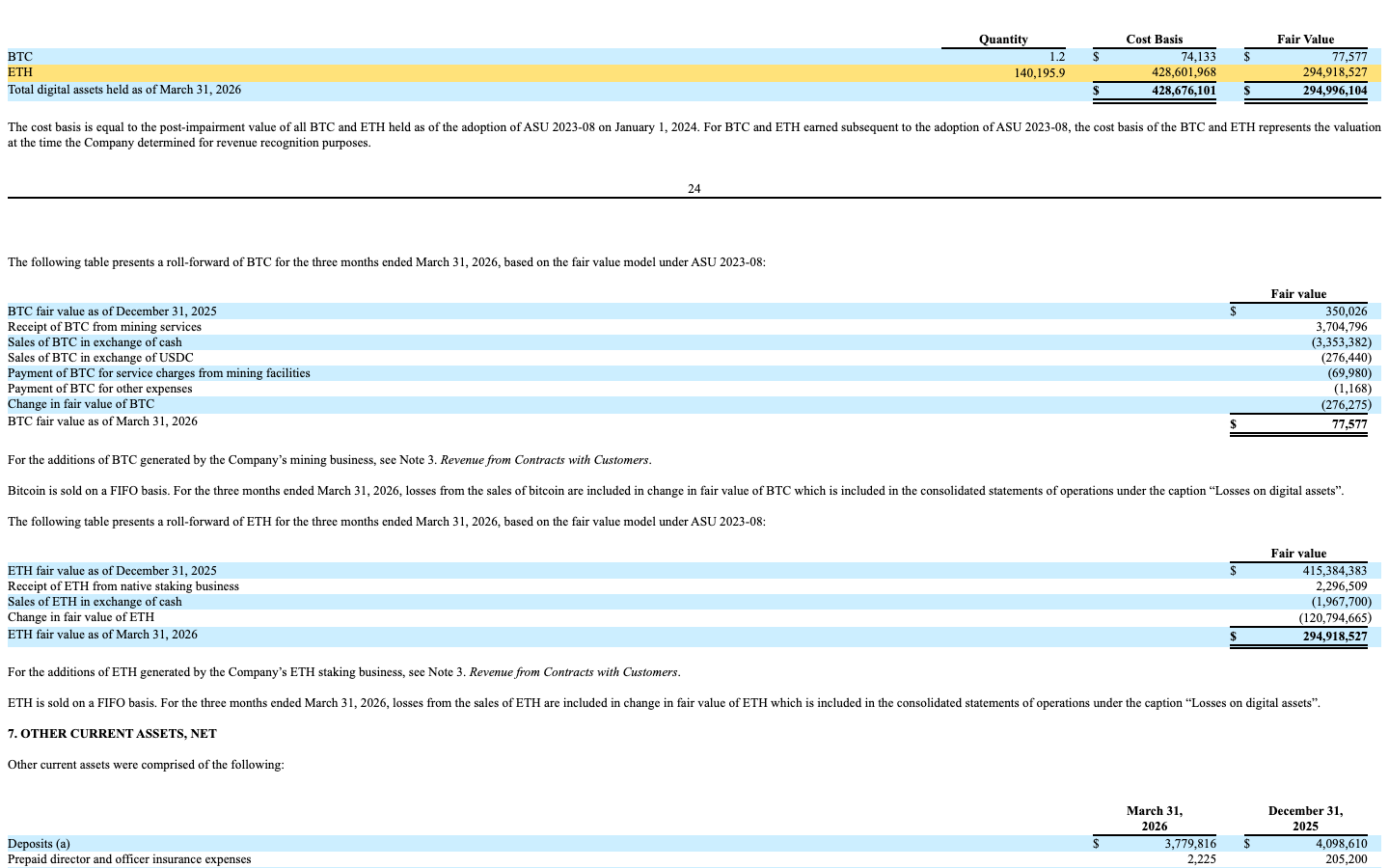

In 2025, Bit Digital went on a large-scale buying spree: per the annual report, $292.7 million in cash alone flowed into new ether, and bitcoin holdings worth $106.9 million were swapped into ETH on top. Result: 140,009 ETH as of December 31, 2025, booked at an average of about $3,070 per unit. Then the price fell. As of March 31, 2026, 140,196 ETH with a cost basis of $428.6 million faced a market value of only $294.9 million — almost a third below cost. The company names the risk itself, with remarkable clarity:

"ETH price declines or prolonged underperformance versus other digital assets could adversely affect our financial position and capital access. Our strategy is focused on ETH as our primary treasury asset. Sustained price declines in ETH or underperformance relative to other assets could reduce the carrying value of our digital assets, increase the frequency or magnitude of impairment charges under applicable accounting policies, and diminish our ability to raise capital or maintain compliance with exchange listing standards."

— Bit Digital, SEC annual report 10-K 2025, Item 1A "Risk Factors"

To be fair: a book loss isn't a realized loss, and the roughly 150,000 ETH (including fund holdings) throw off staking income — $2.3 million in the first quarter of 2026 alone. But you should understand the mechanics: this balance sheet breathes with the ether price, on a quarterly rhythm and in the hundreds of millions. Whoever buys BTBT first buys a leveraged ether tracker — this analysis doesn't answer the question "what will Ethereum be worth in 2027?", and nobody else can honestly answer it either.

Uncomfortable truth no. 2: the most important AI customer hit pause — and the number-two customer got terminated

Now to the second story, the AI cloud. Its growth is real — but its foundation was alarmingly narrow in 2025. WhiteFiber's cloud business hung on a single customer, kept anonymous in the report as the "Initial Customer" — the very buyer with whom the GPU business began in late 2023. The annual report makes no secret of it:

"Our Initial Customer accounted for approximately 70.7% of its revenue during the 12 months ended December 31, 2025 and 96.6% of its revenues through December 31, 2024. As of the report date, WhiteFiber and the Initial Customer are engaged in ongoing discussions regarding a potential resolution of the existing service agreements following the agreed pause of services."

— Bit Digital, SEC annual report 10-K 2025, Item 1 "Business — Customers"

Customer concentration, translated: if your neighbor tells you his rental business is booming, but seven out of every ten dollars come from a single customer who is currently "pausing by mutual agreement" and negotiating a contract resolution — would you pause too? Exactly. Per the report, the talks concern the remaining, non-refundable prepayment of what was once $30 million, outstanding receivables, and a possible termination payment of 40 percent of the remaining contract fees. And it wasn't the only departure: the second-largest cloud customer, an AI fund managed by DNA Holdings (11.5 percent of 2025 revenue), was terminated in November 2025 — with $7.3 million in receivables outstanding, of which only $2.1 million had come in by the report date. The good news sits right next to it: the freed-up GPUs were redeployed to three other customers, service agreements worth $50.2 million (24 months) and $18.1 million among others were added in the first quarter of 2026, and customers paid $65.7 million upfront in that quarter alone. But the biggest hope carrier is a name you should remember: Nscale. WhiteFiber signed a colocation agreement worth about $865 million over ten years with the British AI infrastructure provider in November 2025, at the new North Carolina site — billing for the first 20 megawatts expected from June 2026, with power costs passed through. On top, a five-year contract with AI-chip pioneer Cerebras has been running in Montreal since November 2025 (roughly $1 million a month, converted). One catch: Nscale is a young company not subject to SEC reporting — you can't verify the ten-year contract in the counterparty's own mandatory filings. So the pattern "one anchor carries almost everything" isn't being resolved, just replaced with a new, bigger anchor. We dissected how quickly something like that can turn in our analysis of Applied Optoelectronics — there the AI rally hung on two customers.

Uncomfortable truth no. 3: everything gets paid for with your shares — the share count has tripled

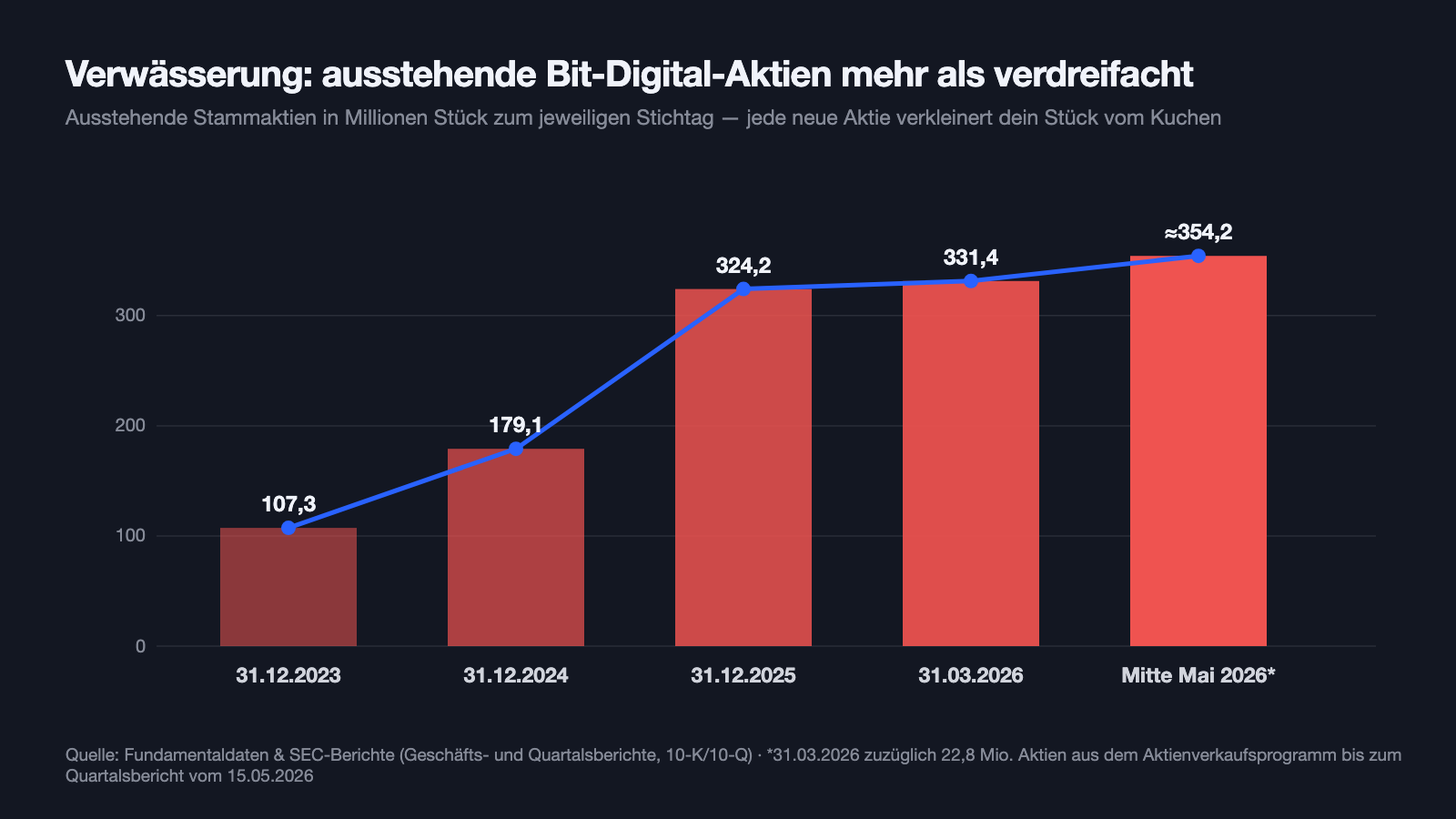

Where did the hundreds of millions for ether purchases and data centers come from? Not from operations — those burned $288.9 million at the group level in 2025 (largely because the ETH purchases run through operating cash flow in the accounting). They came from the capital markets, at an impressive pace: 2025 brought in $599.1 million net from financings — the WhiteFiber IPO ($166.5 million including the overallotment), a public share placement ($162.9 million), a direct placement ($63.5 million), ongoing at-the-market share sales ($63.4 million), and a $150 million convertible note (4.0 percent interest, maturing 2030). In January 2026 the subsidiary followed up with a WhiteFiber convertible note of $230 million (4.5 percent, maturing 2031). A convertible note is a loan with a built-in equity option — if the bet pays off, you repay it later in dilutive shares. What all this means for your slice of the pie shows up in the share count: 107.3 million at the end of 2023, 179.1 million at the end of 2024, 324.2 million at the end of 2025, 331.4 million at the end of March 2026. And the tap kept running — right after the quarter closed:

"Subsequent to March 31, 2026, the Company sold 22,761,994 ordinary shares for aggregate proceeds of approximately $34.6 million pursuant to the at-the-market offering agreement with H.C. Wainwright & Co., LLC. The Company received net proceeds of $33.9 million, net of offering costs."

— Bit Digital, SEC quarterly report 10-Q as of March 31, 2026, Note 22 "Subsequent Events"

Go ahead and check the math on that last sale: $34.6 million for just under 23 million shares comes to about $1.52 per share gross — while the balance sheet as of March 31, 2026 showed equity of $469 million against 331 million shares, or about $1.42 in book value per share. So the company is selling its shares only just above book value in order to hold ether it bought at a considerably higher price. Remember the sentence: a treasure that has to be guarded with fresh shares every quarter belongs to you a little less with every one of them.

Uncomfortable truth no. 4: two executives, two public companies, a record year in pay — in a loss year

A look at the proxy statement (DEF 14A dated June 8, 2026) shows who's certainly earning from the transformation: CEO Sam Tabar received total 2025 compensation of about $4.1 million, CFO Erke Huang about $4.5 million — in a year with an $84.9 million group loss. Both have also run WhiteFiber since the subsidiary's IPO: Tabar as its CEO, Huang as its CFO. Stock-based compensation at the group level jumped to $13.0 million in the first quarter of 2026 alone (prior-year quarter: $0.3 million) — that too is dilution, just in slow motion. None of it is illegal, all of it is disclosed; that's how we know about it. But it belongs in the inventory: the twin structure of two public companies pays for two administrations, two auditors, two executive suites — and the group's administrative costs nearly doubled in 2025.

And the AI? It's real here — but it's only 70 percent yours

Because almost every crypto company waves an AI sign in 2026, we checked the filings against our own criteria catalog. Finding: Bit Digital really does sell AI computing power — the GPU cloud for generative AI training and inference was the group's largest revenue source in 2025 at $68.8 million, with another $8.9 million from AI data-center colocation. WhiteFiber is an Nvidia partner, rents out H200, B200 and GB200 systems, and is building toward a capacity target of about 76 megawatts by the end of 2026. That's not a label, that's a business — with the clusters described above. For you as a BTBT shareholder, the 70 percent rule applies: since the subsidiary's IPO in August 2025, the AI story belongs to you only proportionally (about 70.5 percent per the annual report), and any future WhiteFiber capital raise can dilute that share further. Whoever wants only the AI infrastructure has been able to buy WYFI directly since August 2025 — BTBT is always the combo ticket with the ether hoard attached.

Valuation: a vault, a cloud, and a discount for the space between

How do you value a twin like this? The market recently did it around 1.5 times book value and about 6 times annual revenue (data as of July 9, 2026). A price-to-earnings ratio doesn't exist for lack of earnings. For a comparison of substance (as of March 31, 2026): $79.5 million in cash, $294.9 million in ether, $452 million in fixed assets (mostly GPUs and data centers) — against that stand $380 million in convertible notes (face value) and $144.5 million in prepayments received; equity attributable to BTBT shareholders: $469.2 million. Translated: you're paying a premium of about half over that substance — for the prospect that the ether price turns and the AI contracts deliver starting June 2026. Both can happen; the Nscale contract alone promises roughly $86 million in average annual revenue over ten years. But both have to happen for that premium to pay off — and the dilution counter keeps running in the meantime. The next reality check comes with the second-quarter 2026 report: that's when it will first show whether Nscale is paying as planned since June 2026.

Opportunities and risks at a glance

What speaks for Bit Digital:

- A genuine AI infrastructure business instead of just a label: $68.8 million in cloud revenue in 2025 (+50 percent), an Nvidia partnership, own data centers in Montreal, Iceland and North Carolina with a capacity target of about 76 megawatts by the end of 2026.

- A long contract pipeline: a colocation agreement with Nscale worth about $865 million over ten years (billing expected from June 2026), a five-year contract with Cerebras, $65.7 million in customer prepayments in the first quarter of 2026 alone.

- Substance on the balance sheet: $294.9 million in ether plus $79.5 million in cash (March 31, 2026), $469 million in attributable equity — the roughly 150,000 ETH (including fund holdings) generate ongoing staking income.

- Capital-market access works: $599 million in financing inflows in 2025 via the subsidiary IPO, share placements and a convertible note; another $230 million at WhiteFiber in January 2026, plus credit lines in Canada and Iceland.

- Insider and institutional signals: our scanner reports "CEO buying" and net-buying institutions (data as of July 9, 2026) — a counterpoint to the weak market technicals, with all due caution.

What speaks against it:

- The ether hoard sat almost a third below cost as of March 31, 2026 ($294.9 versus $428.6 million) — and every price move has flowed straight into earnings since ASU 2023-08: a $121.1 million book loss in the first quarter of 2026 alone.

- Customer concentration is documented: the anchor customer (70.7 percent of 2025 cloud revenue) is paused and negotiating a contract resolution; the second-largest customer was terminated in November 2025 — the new anchor, Nscale, isn't subject to SEC reporting and is hard to verify from outside.

- Ongoing dilution: share count tripled from 107.3 to about 354 million in two and a half years, with recent sales at about $1.52 gross just above book value; $380 million in convertible notes await conversion or repayment.

- A loss- and cost-heavy profile: an $84.9 million group loss in 2025, administrative costs nearly doubled ($81.0 million), two public-company structures with double the costs; combined executive pay of about $8.6 million in the loss year.

- Market technicals and history: Weinstein Stage 3, price below the 50- and 200-day lines, about 93 percent below the all-time high, daily swings of about 9.3 percent (data as of July 9, 2026); plus the third business-model skin change in eight years — from Chinese loan broker via bitcoin mining to ether plus AI.

A human conclusion

Back to the department-store trick from the opening: two stories for the price of one. After the fitting, you know what's actually in the package. Story one, the ether hoard, is real — 140,196 ETH, held cleanly, mostly staked. But it was bought at about $3,060 per unit and was worth almost a third less on the reporting date; its price decides hundred-million-dollar swings in the earnings on a quarterly rhythm. Story two, the AI cloud, is real too — with growing revenue, its own data centers and an $865 million contract starting June 2026. But it's only 70 percent yours, its biggest customer to date is paused, and the new anchor is barely verifiable from the outside. And over both hangs the tap that keeps pouring new shares into the market: three times as many shares as at the end of 2023. Two reasons to like a stock are, after all, also two reasons not to have to face up to either one properly — which is exactly why we weighed both separately. If you put BTBT on the watchlist, do it with two concrete checkpoints: does the second-quarter 2026 report show that Nscale has actually been paying since June? And is the ether holding growing per share — or just the ether holding? What you make of it is your decision. And that is exactly as it should be.

Sources

All original documents used in this analysis — to read for yourself:

- Bit Digital, Inc. — SEC annual report 10-K for fiscal year 2025 (filed March 27, 2026)

- Bit Digital, Inc. — SEC quarterly report 10-Q as of March 31, 2026 (filed May 15, 2026)

- Bit Digital, Inc. — SEC quarterly report 10-Q as of September 30, 2025 (filed November 14, 2025)

- Bit Digital, Inc. — SEC quarterly report 10-Q as of June 30, 2025 (filed August 14, 2025)

- Bit Digital, Inc. — Proxy statement (DEF 14A, filed June 8, 2026)

- Bit Digital's complete SEC filing history: EDGAR overview (sec.gov)

- Fundamental data (metrics, valuation; data as of July 9, 2026), reconciled with the SEC filings and the SEC's XBRL database.

- Screener and rating data: in-house stock scanner (data as of July 9, 2026).

Transparency & disclaimer: This analysis is a journalistic contextualization of publicly available information and is not investment advice, not a financial analysis in the regulatory sense, and not a solicitation to buy or sell securities. Cryptocurrencies and stock investments carry substantial risks up to total loss. All information without guarantee; the data cut-off is noted in the text in each case. The author holds no position in Bit Digital or WhiteFiber stock at the time of publication.

Our Bottom Line at a Glance

- AI infrastructure positive

- A genuine business instead of just a label: $68.8 million in cloud revenue in 2025 (+50 percent), an Nvidia partnership, data centers in Montreal, Iceland and North Carolina; an Nscale contract worth about $865 million over ten years starting June 2026, a five-year contract with Cerebras.

- Balance-sheet substance positive

- $294.9 million in ether plus $79.5 million in cash (March 31, 2026), $469 million in attributable equity, $65.7 million in customer prepayments in the first quarter of 2026 — the company is no empty hope stock.

- ETH concentration risk negative

- The ether hoard (bought at about $3,060 per ETH) sat almost a third below cost as of March 31, 2026; a $121.1 million book loss in a single quarter — the income statement breathes with the crypto price on a quarterly rhythm.

- Customer concentration negative

- The anchor customer (70.7 percent of 2025 cloud revenue) is paused and negotiating a contract resolution; the second-largest customer was terminated in November 2025; the new anchor, Nscale, isn't subject to SEC reporting and is hard to verify from outside.

- Dilution negative

- Share count tripled from 107.3 to about 354 million (mid-May 2026); ongoing share sales at about $1.52 gross just above book value; $380 million in convertible notes outstanding (Bit Digital 2030, WhiteFiber 2031).

- Market technicals negative

- Weinstein Stage 3 (a fading trend), price below the 50- and 200-day lines, about 93 percent below the all-time high, daily swings of about 9.3 percent (data as of July 9, 2026) — the insider/institutional buy signals are the only counterpoint.

Bit Digital is two bets in one stock: an ether hoard that sat almost a third below cost on the reporting date and dominates earnings on a quarterly rhythm, and a genuine but only 70.5-percent-owned AI infrastructure subsidiary whose main customer to date is paused. Both have been financed for years with an ever-growing share count — the count has tripled since the end of 2023. Not investment advice.

What Our Rating Means

- If you don't own the stock

- In our view, the documented risks clearly outweigh — we see no basis for an entry.

- If you hold it in your portfolio

- In our view, the findings carry enough weight to warrant a critical look at your own position.

A journalistic assessment by our editorial team at the time of the deep dive, based on public sources — not investment advice and not a solicitation to buy or sell. Your personal circumstances (investment goals, risk capacity, taxes) cannot be taken into account. What our categories mean, how verdicts are formed, and what conflicts of interest exist →

Worth Noting

- Book losses on the ether holding aren't realized losses: the company holds the position and earns staking income; if the ETH price turns, the reported result turns with it. The same holds in reverse.

- Fiscal year = calendar year; "2025" means January through December 2025. Key checkpoints: the second-quarter 2026 report (first Nscale billings expected from June 2026) and the trend in the ether holding per share.

- Whoever wants only the AI data centers can find them listed separately since August 8, 2025 (WhiteFiber, Nasdaq: WYFI); BTBT always adds the ether hoard and the holding costs of two public-company structures on top.

Frequently Asked Questions

Bit Digital (NASDAQ: BTBT) is a holding company with two legs: an Ethereum treasury with about 140,000 ETH (March 31, 2026), generating income mostly through staking, and a majority stake of about 70.5 percent in the AI data-center company WhiteFiber (NASDAQ: WYFI), which rents out GPU computing power for AI training. Per the annual report (10-K), the former core business, bitcoin mining, is slated for sale or wind-down.

As of March 31, 2026, Bit Digital held 140,195.9 ETH directly on the balance sheet per the quarterly report (10-Q): cost basis $428.6 million, market value $294.9 million — almost a third below cost. Including fund holdings, the annual report (10-K) put the total at over 150,000 ETH, mostly staked. Staking brought in $7.0 million in income in 2025.

The group loss of $150.3 million (of which $146.7 million was attributable to BTBT shareholders) came mainly from the book valuation of the crypto holdings: a $121.1 million price loss on ether and bitcoin in a single quarter. Since the accounting rule ASU 2023-08 took effect, every price move of the holdings flows straight into the income statement — upward as well as downward.

WhiteFiber is Bit Digital's AI segment: a GPU cloud ($68.8 million in revenue in 2025) and data centers in Montreal, Iceland and North Carolina. Since the IPO on August 8, 2025 (Nasdaq: WYFI), Bit Digital has held about 70.5 percent — so out of every dollar of AI profit, only a bit over 70 cents belong to BTBT shareholders, and future WhiteFiber capital raises can dilute that share further.

Substantial, and it has already materialized: the anonymously held anchor customer accounted for 70.7 percent of cloud revenue in 2025; per the annual report (10-K), the services are paused by mutual agreement, and talks are underway on a contract resolution. The second-largest customer was terminated in November 2025. New anchors are a ten-year contract with Nscale worth about $865 million (billing expected from June 2026) and a five-year contract with Cerebras.

Massively: shares outstanding rose from 107.3 million (end of 2023) to about 354 million (mid-May 2026) — more than tripling. In the roughly six weeks after March 31, 2026 alone, nearly 23 million new shares were sold at about $1.52 gross. On top come outstanding convertible notes of $150 million (Bit Digital) and $230 million (WhiteFiber).

Found an error?

Did you spot a factual error, an outdated number, or a typo in this deep dive? Let us know briefly — your report goes straight to the editorial team.