Apple Stock: $71 Billion in Profit in Six Months — and Three Courts Are Ruling on the World's Most Profitable Tollbooth

Everyone knows Apple — and that is exactly the problem: holding the product in your hand every day makes you believe you know the stock too. We read the mandatory filings instead: $416.2 billion in revenue in fiscal year 2025, a record iPhone cycle after four years of stagnation, a services segment with a 75 percent margin — but also a Google search contract whose future an appeals court is deciding, an App Store commission under fire from Epic to Brussels, a memory-chip cost surge Apple itself calls "intensifying," and a price-to-earnings ratio of about 34. Our value scanner based on Joel Greenblatt's Magic Formula lights up anyway. Not investment advice — just the instruction manual that never ships with the best-known product in the world.

There is an investor trap that works more powerfully than any advertisement: the familiarity illusion. You hold the product in your hand every day, you know the store downtown, half the family shares the same photo subscription — so the stock feels like an old acquaintance. "Apple? I know it. It's doing fine." Except: knowing the product and knowing the company are two different things. Familiarity answers not a single one of the questions on which the value of the stock is decided — for example, who will still legally own the company's most profitable segment in five years. So let's make a deal: today we treat Apple (Nasdaq: AAPL) like a company you have never heard of. No keynote memories, no nostalgia — only what Apple itself reported, under penalty of law, to the U.S. securities regulator, the SEC: the annual report (10-K, the mandatory yearly filing) for fiscal year 2025 and the quarterly reports (10-Q). The occasion is serious: our in-house stock scanner based on Joel Greenblatt's Magic Formula — a value filter, not a warning system — carries the stock in its hit list. And the read surfaces things that never appear in a product launch: a billion-dollar contract with Google that an appeals court is deliberating right now; a referral to review criminal contempt proceedings; and a memory-chip cost surge Apple itself calls "intensifying." In the end, you decide for yourself.

What Apple actually does — and why its fiscal year ends on the last Saturday of September

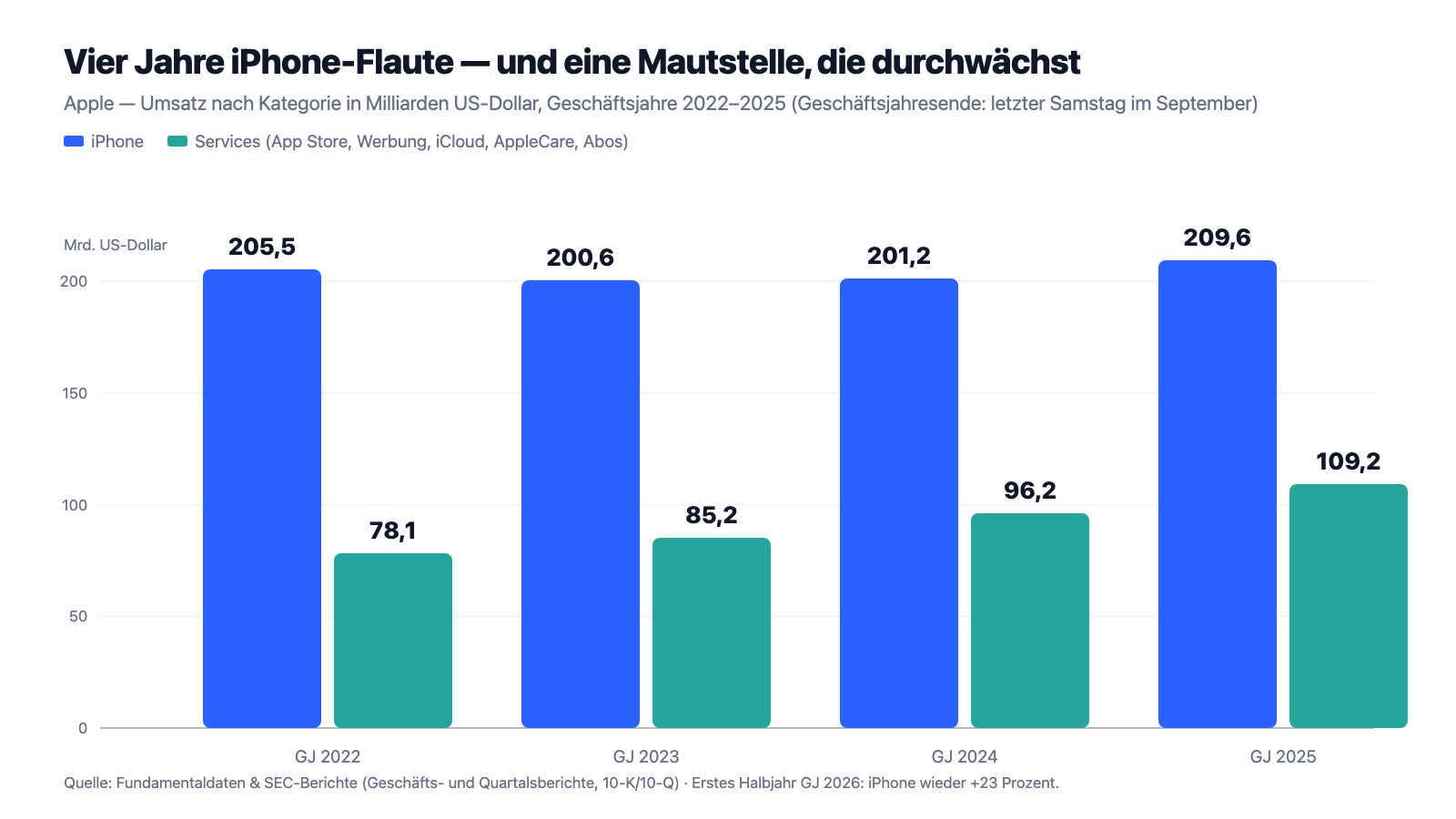

Apple's business model has two floors. Everyone knows the first: selling devices — iPhone, Mac, iPad, Apple Watch, AirPods. The iPhone alone brought in $209.6 billion in fiscal year 2025, a bit more than half of total revenue of $416.2 billion; the company employs roughly 166,000 people for this, but has practically all devices built by contract manufacturers — per the annual report predominantly in China, India, Japan, South Korea, Taiwan and Vietnam. The second floor is the more interesting one, and it works like a tollbooth: once you own an Apple device, you keep paying small amounts for everything that runs across it — app purchases (the App Store keeps a commission), iCloud storage, AppleCare warranties, music and video subscriptions. And even those who buy nothing bring in money: Google pays Apple to be the preset search engine on iPhones — soberly called "licensing arrangements" in the filing, booked under advertising. This services floor generated $109.2 billion in 2025 (+14 percent) — at a 75.4 percent gross margin, more than twice that of the device business (36.8 percent). Translated: a good one in four revenue dollars is a services dollar, but a good 42 percent of gross profit comes from the tollbooth.

One detail up front, so the year labels don't confuse you: Apple has an offset fiscal year — it always ends on the last Saturday of September. "Fiscal year 2025" therefore means: September 29, 2024 through September 27, 2025. The current "fiscal year 2026" began in late September 2025; its first half ended on March 28, 2026 — and exactly this half-year was the best in the company's history. Also note the central tension of this analysis, it runs through every chapter: Apple earns more than ever, and the growing part of that profit comes from a tollbooth — whose gates are being litigated from three sides at once: the Google contract in Washington, the App Store commission in California and Brussels, the entire ecosystem in New Jersey.

Where the stock shows up in our scanner

Every day we run about 3,500 stocks through our scanners. AAPL lit up on July 8, 2026 in four scanners — value/quality scanners without exception, not a single warning signal: "Joel Greenblatt: Magic Formula", "Terry Smith: Quality", "Martin Zweig: Growth with Reason" and "Altman-Z: Balance Sheet Fortress" (in the live cross-check on July 14, 2026 Greenblatt and Terry Smith were still active; the stock had since dropped out of the other two). Greenblatt's formula looks, plainly put, for good companies at fair prices — measured by exactly two numbers: the return on capital (how much operating profit per dollar of operating capital employed?) and the earnings yield (how much operating profit per dollar of enterprise value?). At Apple it is worth a close look at why the formula fires: the return on capital is astronomical — but also because the factories belong to the contract manufacturers and the buyback machine has depleted the equity (more on that later); on paper, Apple generates its profit almost without capital of its own. The earnings yield, by contrast, is solid at about 3.7 percent — a market value of roughly $4,041 billion against an operating annual profit in the neighborhood of $147 billion — but no bargain signal. So the formula mostly finds quality here — and it has the same blind spot as at Alphabet, the other mega-cap surprise on this hit list: it sees the profit, but not the courts ruling on its source.

The remaining metrics sketch a quality giant in stable, unexcited condition: the Piotroski F-Score, a nine-point test of balance sheet quality, stands at a strong 8 of 9 — a thoroughly healthy company scores 8 or 9, and Apple does. The Altman-Z score, a classic bankruptcy early-warning gauge, sits at 6.6 (danger begins below 1.8) — payment problems are simply not a topic. The relative strength of 65 says: a bit better than average, no rocket; over twelve months the price gained about 46 percent and stood roughly 7 percent below the all-time high at the cut-off date (all scanner figures: data as of July 8, 2026). One drop of bitterness here too: the in-house fundamental rating stands at only B (38), mid-table — past growth was meager for four years, and that is exactly what the next chapter is about.

The numbers over the years — honestly appraised

First, what hardly anyone knows about Apple, because it fits the familiarity illusion so poorly: until recently, Apple was a growth slump. Revenue stood at $394.3 billion in fiscal year 2022, fell to $383.3 billion in 2023 (−3 percent), recovered to $391.0 billion in 2024 (+2 percent) — and only 2025 brought a genuine new record with $416.2 billion (+6 percent). The iPhone, half the company, marked time for four years: 205.5 — 200.6 — 201.2 — 209.6 billion dollars. That net income nonetheless jumped to $112.0 billion in 2025 (after $93.7 billion) was partly a one-off tax effect: in 2024 the European Court of Justice had confirmed the Irish back-tax payment, saddling Apple with $10.2 billion in extra tax expense; in 2025 the tax rate normalized from 24.1 to 15.6 percent. What really grew during the slump years was the tollbooth: services climbed from $78.1 billion (2022) via $85.2 and $96.2 to $109.2 billion (2025) — double-digit percentage growth year after year, with a rising margin.

And then came the half-year that changed everything. In the first six months of fiscal year 2026 (ended March 28, 2026), revenue jumped 16 percent to $254.9 billion, net income 17 percent to $71.7 billion. The holiday quarter (through December 27, 2025) was the largest quarter in company history at $143.8 billion in revenue. The driver is unmistakable: the iPhone grew 23 percent in the half-year to $142.3 billion — per the filing, carried by the Pro models of the iPhone 17 generation. Even the region that shrank for years turned around: Greater China had slipped from $72.6 billion (fiscal year 2023) to $64.4 billion (2025) — in the first half of 2026 it suddenly grew 33 percent. On top of that, the group gross margin rose to 48.6 percent (prior-year half: 47.0), and operating cash flow reached $82.6 billion in six months. That is the honest appraisal: this half-year was operationally flawless. The equally honest framing: a product cycle is a wave, not a sea level — the years 2022 through 2024 sit in the same set of accounts and are a reminder of how flat it can get after a wave.

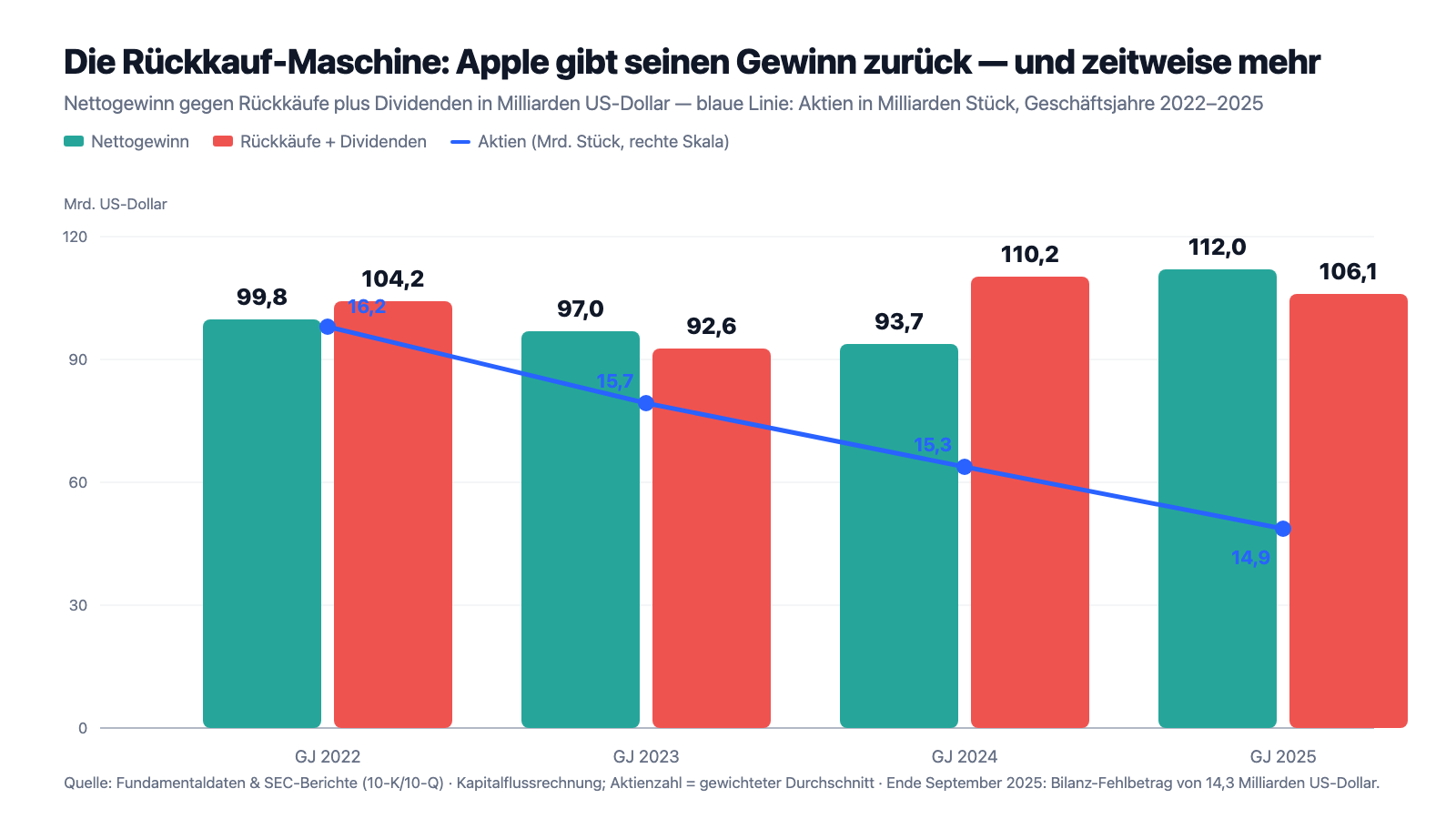

That leaves the balance sheet — and at Apple it is a curiosity of its own. As of March 28, 2026, $146.6 billion in cash and securities stood against $84.7 billion in debt: net cash of a good $60 billion, plus Piotroski 8 of 9 — a fortress. But the same balance sheet showed, at the end of fiscal year 2025, an accumulated deficit of $14.3 billion in the "Accumulated deficit" line: where the profits of decades pile up at other corporations, Apple shows a minus. No loss is to blame, but the buyback machine: in fiscal years 2022 through 2025, Apple paid out roughly $413 billion via buybacks and dividends — more than it earned over the same period (roughly $403 billion). The share count fell from 16.2 to 14.9 billion as a result, which let earnings per share grow even in the slump years. In May 2025 came a new $100 billion buyback program, in April 2026 straightaway the next one for another $100 billion, plus the umpteenth dividend increase (to $0.27 per quarter). Remember two things here: buybacks are not a trick, but an amplifier — they turn stagnant profits into growing earnings per share, and they render metrics like return on equity (arithmetically over 140 percent) meaningless. What they did not do for four years is replace growth.

What the filings say — the uncomfortable truths

Uncomfortable truth no. 1: Google billions sit inside the services profit — and an appeals court is deciding their future right now

The services segment is considered Apple's future, and its 2025 growth came, per the filing, primarily from advertising, the App Store and cloud services. What hides behind the word "advertising," among other things, is in the risk chapter — the licensing payments from Google for the slot as the preset search engine on Apple's devices. And about this foundation, Apple itself writes:

"For example, the Company earns revenue from licensing arrangements with Google LLC (“Google”) and other companies to offer their search services on the Company’s platforms and applications, and certain of these arrangements are currently subject to government investigations and legal proceedings. […] A reversal of the order on appeal could result in imposition of certain remedies initially proposed by the DOJ, such as those prohibiting Google from offering the Company commercial terms for search distribution. If implemented, these remedies could materially adversely affect the Company’s ability to earn revenue from such licensing arrangements."

— Apple Inc., SEC quarterly report 10-Q as of March 28, 2026, Part II, Item 1A "Risk Factors"

Some background: in August 2024 the district court in Washington found that Google had violated U.S. antitrust law; in September 2025 it ordered remedies that let the search contract with Apple stand — the U.S. Department of Justice had originally proposed a ban on commercial terms for search distribution. Both sides have appealed this order. For Apple that means: the mildest outcome is already the current one, and any tightening on appeal would hit a revenue source that runs into profit practically without costs. How large it is exactly, Apple does not reveal — the payments are hidden in the advertising line of services. That the company devotes a paragraph of its own to them in the risk chapter says enough. The irony on the side: the same ruling that sits in Alphabet's filing as a risk appears at Apple once more — a single contract, two trillion-dollar corporations, both carrying it in their risk chapters.

Uncomfortable truth no. 2: the App Store commission is up for grabs in three jurisdictions at once — up to and including the review of criminal steps

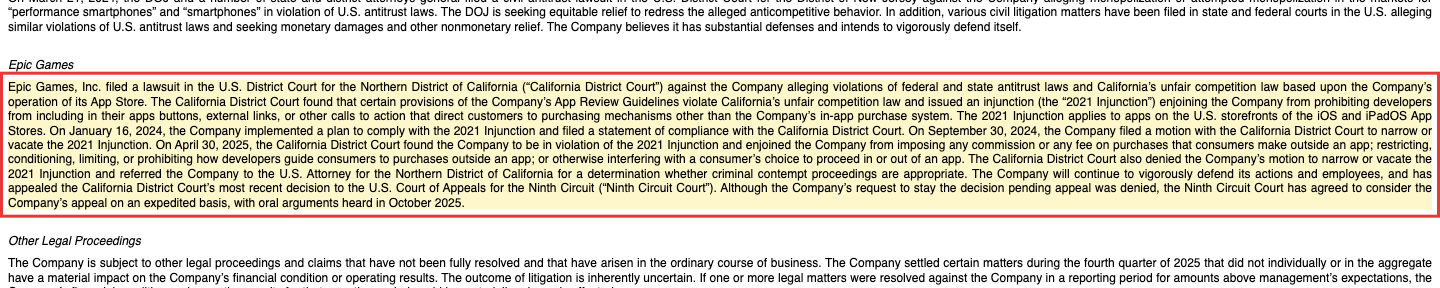

The second pillar of the tollbooth is the App Store commission — and its litigation dossier reads like a world atlas. In the U.S., the Epic Games case escalated in 2025 in a way that practically never happens at companies of this size:

"On April 30, 2025, the California District Court found the Company to be in violation of the 2021 Injunction and enjoined the Company from imposing any commission or any fee on purchases that consumers make outside an app […] The California District Court also denied the Company’s motion to narrow or vacate the 2021 Injunction and referred the Company to the U.S. Attorney for the Northern District of California for a determination whether criminal contempt proceedings are appropriate."

— Apple Inc., SEC annual report 10-K FY 2025, Part I, Item 3 "Legal Proceedings — Epic Games"

In fairness, the sequel belongs here: in December 2025 the appeals court (Ninth Circuit) partially defused the order — Apple may, in principle, again charge a commission on "link-out" purchases, but must allow equal treatment between its own payment system and external purchase links; the exact design is back with the district court. A partial victory, then — but the quarterly report words the residual worry itself: should Apple ultimately be unsuccessful in defending its commission structure, or should similar restrictions arrive in other countries, this could materially and adversely affect its results of operations. And the other countries are long since here: in April 2025 the European Commission imposed a fine of €500 million under the DMA (Digital Markets Act — the EU's special rules for large platforms), along with an order to end the "steering" restrictions; Apple has appealed. In the second DMA proceeding, per the filing, fines of up to 10 percent of worldwide annual revenue loom — at Apple that would be over $40 billion. And in New Jersey the U.S. Department of Justice has been suing the entire ecosystem since March 2024: the accusation is monopolization of the smartphone market. None of these cases is decided; Apple is defending itself in all of them. But keep count: it is the same tollbooth that Washington, California and Brussels are rattling at the same time — and it generates the most profitable part of the group's earnings.

Uncomfortable truth no. 3: one product, one manufacturing region — the cluster remains Apple's blueprint

The third truth has been in the risk chapter for years, and the record run makes it larger rather than smaller. First, the product: the iPhone stood for a good 50 percent of revenue in fiscal year 2025, and in the record half of 2026 for as much as 56 percent — and Apple writes it itself: "the Company generates a significant portion of its net sales from a single product category and a decline in demand for that product could significantly impact net sales and gross margins." (10-Q as of March 28, 2026, risk chapter.) Second, manufacturing: final assembly of practically all devices sits, per the annual report, with contract manufacturers mainly in Asia, the supply chain hangs on single-source partners for many components, and the Greater China region is at the same time the third-largest sales market ($64.4 billion in revenue in 2025). Third, trade policy in between: since spring 2025, new U.S. tariffs apply to imports from, among others, China, India and Vietnam — exactly Apple's manufacturing countries; the annual report explicitly names tariff costs as a margin burden, and even though the Supreme Court struck down part of the tariffs in February 2026 (Apple is seeking a refund), the filing already lists the next possible instruments. Translated into an everyday image: Apple is a house standing on a single, outstanding pillar, built on rented ground in a geopolitical earthquake zone. The house has held for fifteen years — but the blueprint is written in the mandatory filing, not in the keynote.

Uncomfortable truth no. 4: in AI, Apple is the payer, not the collector — and its own filing now says so itself

Perhaps the most revealing passage of the latest quarterly report is one that did not exist before: in spring 2026, Apple added a standalone AI risk factor to its filing for the first time. It begins with a statement of fact — and then becomes remarkably concrete on the question of whether all of this pays off:

"Artificial intelligence technologies are increasingly integrated into the Company’s products and services and its business and operations. […] For example, the Company’s artificial intelligence efforts may give rise to risks related to: competition and strategy; recouping costs and returns on investments; product liability; intellectual property infringement; data privacy; cybersecurity; sanctions and export controls; exposing users to harmful, inaccurate or other negative content or experiences; bias and discrimination; and online safety and protection of minors; among other issues."

— Apple Inc., SEC quarterly report 10-Q as of March 28, 2026, Part II, Item 1A "Risk Factors" (new AI risk factor)

"Competition and strategy" and "recouping costs" — that is, in the cautious language of a mandatory filing, the admission of a catch-up race at its own expense. The costs sit a few pages earlier: research and development spending jumped 34 percent to $11.4 billion in the quarter ended March 28, 2026 — per the filing mostly because of higher infrastructure costs, that is: computing power. What is not there is also striking: the entire annual report for 2025 does not mention Apple's own AI system "Apple Intelligence" a single time — in the prior year's report it was still listed as a product novelty. An AI revenue source disclosed as such exists nowhere in the filings. And the cost side has a second front, one that should look familiar if you have read our Micron analysis — there it is the boom, here it is the bill:

"The Company is experiencing a period of supply constraints and increasing costs for components driven by factors such as industry supply-demand imbalances for components, including advanced semiconductors, storage (NAND) and memory (DRAM). The Company expects these trends to intensify […]"

— Apple Inc., SEC quarterly report 10-Q as of March 28, 2026, Item 2 MD&A "Macroeconomic Conditions"

The AI boom drives up the prices of memory chips — every AI server devours DRAM that would otherwise go into iPhones. For memory makers like Micron that is the jackpot; for Apple, one of the largest memory buyers in the world, it is a cost wave with advance warning, still masked in the record half-year by the strong product mix. Remember the constellation: Apple pays for the AI boom three times over — through its own infrastructure, through more expensive components, and through the risk that the platform competition is faster with AI. What it has earned from it so far: nothing disclosed.

Valuation: $4 trillion — quality at a quality price, records as the yardstick

In early July 2026 the stock cost about $275, the market value stood at roughly $4,041 billion — after a price gain of about 46 percent within twelve months and roughly 7 percent below the all-time high (all valuation figures: data as of July 8, 2026). The price-to-earnings ratio sits at about 34 based on the last four quarters — that is, including the record half-year. For comparison within the same scanner hit list: Alphabet costs 26 times its earnings with recently higher growth. The price-to-sales ratio is about 9, price to free cash flow about 31 — and the dividend yield, despite yearly increases, a meager 0.4 percent; the real payout vehicle remains the buybacks ($63.8 billion in remaining authorization as of March 28, 2026, plus a new $100 billion program dated April 30, 2026). The "professionals' view": 48 analysts, consensus clearly on "buy" — though at the best-known company in the world that is more ambient temperature than information. Better to run the counter-check: a P/E of 34 assumes that the iPhone 17 surge was not a one-off wave, that memory costs do not claw back the 48 percent gross margin — and that the tollbooth keeps its gates. Remember the core: what you get here is perhaps the best company in the world — but at a price that already prices in the best six months of its history as the new normal.

Opportunities and risks at a glance

What speaks for Apple:

- A record run with substance: $254.9 billion in revenue (+16 percent) and $71.7 billion in net income (+17 percent) in the first half of fiscal year 2026, a 48.6 percent gross margin, $82.6 billion in operating cash flow (10-Q as of March 28, 2026).

- The iPhone 17 cycle turns after four years of stagnation: iPhone revenue +23 percent in the half-year, Greater China +33 percent after years of shrinking (10-Q as of March 28, 2026).

- The tollbooth keeps growing at double digits: services at $109.2 billion in fiscal year 2025 (+14 percent) at a 75.4 percent gross margin — plannable subscription, commission and licensing revenue across the entire device fleet (10-K FY 2025).

- Fortress balance sheet plus shareholder machine: roughly $60 billion in net cash, Piotroski 8 of 9, Altman-Z 6.6, two $100 billion buyback programs (May 2025, April 2026) and the umpteenth dividend increase (10-Q as of March 28, 2026; scanner data as of July 8, 2026).

- Four value/quality scanner hits on July 8, 2026 (Greenblatt, Terry Smith, Zweig, Altman-Z Balance Sheet Fortress; Greenblatt and Terry Smith confirmed live on July 14) — and not a single warning scanner.

What speaks against it:

- Three legal fronts at the most profitable segment: the Google search contract in the antitrust appeal (a possible ban on commercial terms), the Epic case with a temporary commission ban and a referral to review criminal steps, the EU with a €500 million DMA fine plus a second proceeding threatening up to 10 percent of worldwide revenue, and on top the DOJ monopolization suit (10-K FY 2025; 10-Q as of March 28, 2026).

- Clusters in the blueprint: a good half of revenue from a single product category, final assembly of practically all devices at contract manufacturers mainly in Asia, Greater China both market and manufacturing hub, a tariff regime in permanent flux (10-K FY 2025).

- A cost wave with advance warning: supply constraints and rising prices for DRAM/NAND that, per Apple's own filing, are expected to "intensify" — a headwind for the record gross margin (10-Q as of March 28, 2026).

- AI as an open flank: a new standalone risk factor ("competition and strategy," "recouping costs"), research spending +34 percent in the quarter, no disclosed AI revenue source — Apple funds the catch-up race out of its margin (10-Q as of March 28, 2026).

- Valuation at the upper edge: a P/E of about 34 based on a record half-year, price to free cash flow about 31, a 0.4 percent dividend yield — the years 2022 through 2024 show how quickly Apple growth can become Apple stagnation (data as of July 8, 2026; 10-K FY 2025).

A human conclusion

Back to the familiarity illusion. It whispers: "You know Apple, don't you?" After reading the mandatory filings, you can say more precisely what you know: the product, the brand, the reliability of a machine that threw off ninety billion dollars in profit even in its slump years and has just delivered the best half-year of its history. What familiarity does not show you is in the filings: that the highest-margin part of this profit is a tollbooth whose gates are being negotiated in Washington, California and Brussels at the same time; that the company builds on a single product pillar in a geopolitical earthquake zone; that memory costs are rising and, per Apple itself, will "intensify"; and that on AI, of all things, the company with the record profits writes in its risk chapter about "recouping costs" instead of revenue. None of this is hidden — it sits in the same documents as the records. The Greenblatt scanner did its job: it found an exceptionally good company whose profit is not absurd relative to its price. What it cannot do: price appeals rulings, commission models and product cycles. Nobody takes that check off your hands — least of all the device in your hand. Now you know both sides. What you make of it is your decision. And that is exactly as it should be.

Sources

All original documents used in this analysis — to read for yourself:

- Apple Inc. — SEC annual report 10-K for fiscal year 2025 (ended September 27, 2025; filed October 31, 2025)

- Apple Inc. — SEC annual report 10-K for fiscal year 2024 (ended September 28, 2024; filed November 1, 2024)

- Apple Inc. — SEC quarterly report 10-Q as of March 28, 2026 (filed May 1, 2026)

- Apple Inc. — SEC quarterly report 10-Q as of December 27, 2025 (filed January 30, 2026)

- Apple Inc. — SEC quarterly report 10-Q as of June 28, 2025 (filed August 1, 2025)

- Apple Inc. — SEC quarterly report 10-Q as of March 29, 2025 (filed May 2, 2025)

- Apple's complete SEC filing history: EDGAR overview (sec.gov)

- Fundamental data (metrics, valuation, analyst consensus; data as of July 8, 2026), reconciled with the SEC filings.

- Screener and rating data: in-house stock scanner (data as of July 8, 2026; scanner membership verified live on July 14, 2026).

Transparency & disclaimer: This analysis is a journalistic contextualization of publicly available information and is not investment advice, not a financial analysis in the regulatory sense, and not a solicitation to buy or sell securities. Stock investments carry substantial risks up to total loss. All information without guarantee; the data cut-off is noted in the text in each case. The author holds no position in Apple stock at the time of publication.

Our Bottom Line at a Glance

- Market position & product positive

- The most valuable consumer ecosystem in the world: an iPhone 17 cycle with +23 percent half-year growth after four years of stagnation, a comeback in Greater China (+33 percent), plus the services tollbooth with $109.2 billion in annual revenue and a 75.4 percent gross margin (10-K FY 2025; 10-Q as of March 28, 2026).

- Earning power & balance sheet positive

- A record half-year with $254.9 billion in revenue and $71.7 billion in net income, $82.6 billion in operating cash flow, roughly $60 billion in net cash, Piotroski 8 of 9 and Altman-Z 6.6 — plus two fresh $100 billion buyback programs (10-Q as of March 28, 2026; scanner data as of July 8, 2026).

- Legal & regulatory risk negative

- Three fronts at the most profitable segment: a possible ban on commercial Google terms in the antitrust appeal, the Epic case with a temporary commission ban plus a referral to review criminal steps, a €500 million DMA fine plus a second EU proceeding threatening up to 10 percent of worldwide revenue, and on top the DOJ monopolization suit (10-K FY 2025; 10-Q as of March 28, 2026).

- Clusters, costs & AI negative

- A good half of revenue from a single product category, final assembly almost entirely at contract manufacturers in Asia, a tariff regime in permanent flux; memory costs (DRAM/NAND) are rising with an "intensifying" tendency per Apple's own filing, and the new AI risk factor names competition and cost risks of the catch-up race — with no disclosed AI revenue source (10-K FY 2025; 10-Q as of March 28, 2026).

- Valuation & profit quality neutral

- A P/E of about 34, price to free cash flow of about 31, a 0.4 percent dividend yield (data as of July 8, 2026) — what is being paid for is the best half-year in company history as the new normal; the buyback machine amplifies earnings per share but does not replace growth, as fiscal years 2022 through 2024 show.

Apple is the rare case of a value scanner hit at the all-time high of its own performance: a record half-year, an iPhone supercycle, net cash, Piotroski 8 of 9 — quality exactly as the Magic Formula loves it. Set against this are three open questions no scanner can price: whether the courts in Washington, California and Brussels leave the tollbooth intact whose licensing and commission revenue carries the highest-margin part of the profit; whether the iPhone 17 surge is a new plateau or just a wave; and whether Apple can fund the AI catch-up race without rising memory and infrastructure costs clawing back the record margin. A P/E of about 34 leaves no room for disappointment on any of the three fronts. Not investment advice.

What Our Rating Means

- If you don't own the stock

- At the current price level, we don't see a sufficient margin of safety for an entry.

- If you hold it in your portfolio

- Our findings offer no reason to sell.

A journalistic assessment by our editorial team at the time of the deep dive, based on public sources — not investment advice and not a solicitation to buy or sell. Your personal circumstances (investment goals, risk capacity, taxes) cannot be taken into account. What our categories mean, how verdicts are formed, and what conflicts of interest exist →

Worth Noting

- Apple has an offset fiscal year (ending: last Saturday of September). "FY 2025" denotes the twelve months through September 27, 2025, the "first half of FY 2026" the six months through March 28, 2026.

- Net income for FY 2024 ($93.7 billion) was depressed by the one-time tax expense of $10.2 billion from the confirmed Ireland back-tax payment (European Court of Justice ruling, September 2024); the 2025 profit jump is partly a base effect.

- Price and valuation figures are dated to July 8, 2026 (about $275 per share, roughly $4,041 billion in market value); analyses are evergreen, daily prices are not a buy argument.

- The scanner membership was checked twice: data as of July 8, 2026 (Greenblatt, Terry Smith, Zweig, Altman-Z Balance Sheet Fortress) and a live check on July 14, 2026 (Greenblatt and Terry Smith confirmed; the other two had since dropped out).

Frequently Asked Questions

With devices and a tollbooth: the iPhone brought in $209.6 of $416.2 billion in revenue in fiscal year 2025 (ended September 27, 2025), plus Mac, iPad and wearables. The services segment (App Store, advertising including the Google search contract, iCloud, AppleCare, subscriptions) generated $109.2 billion — at a 75.4 percent gross margin, a good 42 percent of the group's gross profit.

Apple uses an offset fiscal year: it always ends on the last Saturday of September and spans 52 or 53 weeks. "Fiscal year 2025" ran from September 29, 2024 through September 27, 2025; the first half of fiscal year 2026 ended on March 28, 2026. The important holiday season therefore falls into the first quarter of the fiscal year.

Joel Greenblatt's Magic Formula looks for a high return on capital plus a high earnings yield. Apple's return on capital is extraordinary because the factories belong to the contract manufacturers and buybacks have shrunk the equity; the earnings yield is solid at about 3.7 percent (data as of July 8, 2026). The formula mostly finds quality here — legal risks to the services profit it does not see.

Heavily: the iPhone stood for a good 50 percent of revenue in fiscal year 2025, and for 56 percent in the record half of 2026. Apple itself warns in its risk chapter that a decline in demand for this single product category could significantly impact revenue and gross margins. Before that, iPhone revenue had stagnated at $200 to $210 billion for four years.

Google pays Apple for the slot as the preset search engine; this licensing revenue runs into profit almost without costs. The U.S. antitrust court let the contract stand in September 2025, and both sides appealed. Apple itself warns: a reversal could prohibit Google from offering commercial terms for search distribution — with material consequences for this revenue.

It is up for grabs in several jurisdictions: in the Epic case, a U.S. court in 2025 temporarily barred any commission on purchases outside the app and referred Apple to the prosecutor's office to review criminal steps; in December 2025 the appeals court allowed a commission again in principle. The EU imposed a €500 million DMA fine, and a second proceeding threatens up to 10 percent of worldwide revenue.

Operationally a fortress: roughly $146.6 billion in cash and securities against $84.7 billion in debt (March 28, 2026), Piotroski 8 of 9, Altman-Z 6.6. The curiosity: because Apple paid out more than it earned for years, the balance sheet showed an accumulated deficit of $14.3 billion at the end of September 2025 — which makes metrics like return on equity carry little meaning.

Rather fully valued: a price-to-earnings ratio of about 34, price-to-sales of about 9, price to free cash flow of about 31, a 0.4 percent dividend yield (data as of July 8, 2026) — based on a record half-year. Cheap it is only if the iPhone 17 surge carries on, memory costs do not claw back the margin, and the courts leave the services revenue intact.

Found an error?

Did you spot a factual error, an outdated number, or a typo in this deep dive? Let us know briefly — your report goes straight to the editorial team.